Oracle Stock Offers Investment Opportunity After Recent Pullback

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 5 days ago

0mins

Source: Fool

- Strong Performance Growth: Oracle's revenue in Q3 of fiscal 2026 increased by 22% year-over-year to $17.2 billion, while non-GAAP earnings rose by 21% to $1.79 per share, indicating robust growth potential driven by investments in AI infrastructure.

- Upgraded Guidance: Oracle raised its fiscal 2027 revenue guidance from $85 billion to $90 billion, projecting a remarkable 34% growth next year, which highlights significant progress in converting its $553 billion remaining performance obligations (RPO) into revenue.

- Innovative Customer Payment Models: The company has implemented upfront payments from customers before building cloud computing hardware and allows customers to bring their own hardware, which not only alleviates capital expenditure pressures but also enhances contract signing willingness, resulting in over $29 billion in new contracts signed.

- Significant Stock Price Potential: If Oracle achieves $21 in earnings per share by fiscal 2030 and maintains a forward earnings multiple of 24, its stock price could reach $504 in just over four years, representing a potential 170% increase, underscoring the attractiveness of its current valuation.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ORCL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ORCL

Wall Street analysts forecast ORCL stock price to rise

34 Analyst Rating

25 Buy

9 Hold

0 Sell

Moderate Buy

Current: 189.770

Low

180.00

Averages

309.59

High

400.00

Current: 189.770

Low

180.00

Averages

309.59

High

400.00

About ORCL

Oracle Corporation offers integrated suites of applications plus secure, autonomous infrastructure in the Oracle Cloud. The Company operates through three businesses: cloud and license, hardware and service. Its cloud and license business is engaged in the sale, marketing and delivery of its enterprise applications and infrastructure technologies through cloud and on-premise deployment models including its cloud services and license support offerings, and its cloud license and on-premise license offerings. Its hardware business provides infrastructure technologies including Oracle Engineered Systems, servers, storage, industry-specific hardware, operating systems, virtualization, management and other hardware-related software to support diverse IT environments. Its services business provides services to customers and partners to help maximize the performance of their investments in Oracle applications and infrastructure technologies.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Dow Jones Index Celebrates 130th Anniversary with Key Stock Insights

- Dow Component Changes: Since its establishment in 1896, the Dow Jones Index has seen significant changes in its components, with recent additions like Nvidia and Amazon reflecting economic evolution, shifting investor perception from traditional low-growth stocks to a modern blend of growth and value stocks.

- Nvidia's Dividend Surge: On May 20, Nvidia raised its quarterly dividend from $0.01 to $1 per share, a staggering 2400% increase, which, despite a current yield of only 0.5%, attracts investors seeking passive income and indicates a shift towards a more stable earnings model amid surging AI demand.

- Visa's Strong Financial Performance: Despite economic uncertainties, Visa achieved a 9% increase in payment volume in its latest quarter, with valuations at 30 times free cash flow and 29 times earnings, showcasing the resilience of its business model and providing a compelling buying opportunity for investors despite stock price declines.

- Procter & Gamble's Rising Dividend Yield: Procter & Gamble raised its dividend for the 70th consecutive year in April, with a current yield of 3%, and despite challenges in volume growth, its strong brand portfolio positions it as an ideal choice for risk-averse investors, trading at a P/E of just 21, below its 10-year average of 25.4.

See More

Nvidia Makes Significant Dividend Increase

- Dividend Surge: Nvidia raised its quarterly dividend from $0.01 to $1 per share on May 20, marking a staggering 2,400% increase, which, despite a low yield of 0.5%, makes it more attractive for investors seeking passive income.

- Market Share Expansion: Nvidia has broadened its market share in data centers by delivering new rack-scale solutions, including multi-chip systems to Anthropic, OpenAI, Oracle, and SpaceX on May 18, indicating strong growth potential amid surging AI demand.

- Visa Investment Opportunity: Despite a 6.2% decline in Visa's stock year-to-date, its reasonable valuation at 30 times free cash flow and 29 times earnings presents an excellent buying opportunity, with double-digit revenue and earnings growth reflecting its robust business model.

- Procter & Gamble Stability: Procter & Gamble raised its dividend for the 70th consecutive year in April, and despite sluggish volume growth leading to a mere 4.7% stock price increase over five years, its 21 times earnings valuation remains attractive for risk-averse investors.

See More

Snowflake Set to Announce Q1 Fiscal 2027 Results with Strong Growth Indicators

- Strong Earnings Outlook: Snowflake anticipates Q1 fiscal 2027 earnings of 32 cents per share, reflecting a 33.33% year-over-year increase, with revenue expectations at $1.32 billion, indicating a 26.85% growth, showcasing robust performance in AI and client expansion.

- Significant Customer Growth: As of Q4 fiscal 2026, Snowflake's net revenue retention rate reached 125%, with 740 net new customers added, a 40% year-over-year increase, indicating enhanced competitiveness in the market, a trend expected to continue in the upcoming earnings report.

- Product Revenue Projections: The company expects product revenues to range between $1.262 billion and $1.267 billion for Q1, reflecting a 27% year-over-year growth, with the Zacks consensus estimate at $1.26 billion, highlighting strong market demand for its offerings.

- Increased Competitive Pressure: Despite Snowflake's expanding product portfolio, it faces intense competition from major cloud providers like Oracle, Amazon, and Alphabet, particularly in the rapidly evolving AI sector, which may pose threats to its market share.

See More

Microsoft and Oracle Experience Strong Demand for Cloud Services

- Microsoft Cloud Revenue Growth: Microsoft Cloud reported $54 billion in revenue for Q3 FY2023, a 29% year-over-year increase, with Azure revenue surging 40% despite supply constraints, demonstrating the company's strong competitive position in the cloud market.

- Strong AI Product Performance: Microsoft's AI products achieved an annualized revenue run rate of $37 billion, up 123% year-over-year, indicating sustained enterprise demand for AI services despite concerns over spending on AI infrastructure.

- Oracle Cloud Services Surge: Oracle's cloud infrastructure services revenue grew 84% to $4.9 billion in the recent quarter, with multicloud database service demand skyrocketing by 531%, reflecting enterprises' long-term commitment to AI investments.

- Optimistic Future Outlook: Oracle's management raised fiscal 2027 revenue guidance to $90 billion, signaling demand exceeding expectations, while analysts have increased long-term earnings growth forecasts to 23%, providing strong market return potential for investors.

See More

Microsoft and Oracle's Cloud Growth Potential Amid Market Pullback

- Microsoft Cloud Growth: Microsoft's cloud revenue reached $54 billion in the latest fiscal quarter, reflecting a 29% year-over-year increase, indicating that despite supply constraints, Azure's 40% growth remains unaffected by competition, showcasing the company's strong position in the cloud market.

- Copilot User Surge: Microsoft 365 Copilot paid seats have exceeded 20 million, representing a 250% year-over-year increase, which indicates a rapidly growing demand for AI assistants among enterprises, further solidifying Microsoft's market share in the AI sector.

- Oracle Debt Risks and Opportunities: Oracle's long-term debt has surged 71% over the past two years to $159 billion; however, management does not expect to issue new debt beyond 2026, potentially setting the stage for a stock rebound, especially as cloud services continue to show robust growth.

- Cloud Services Contract Growth: Oracle's remaining performance obligations grew 325% year-over-year to $553 billion, demonstrating a long-term commitment from enterprises to AI, providing high visibility into future demand and supporting the company's $90 billion revenue forecast for fiscal 2027.

See More

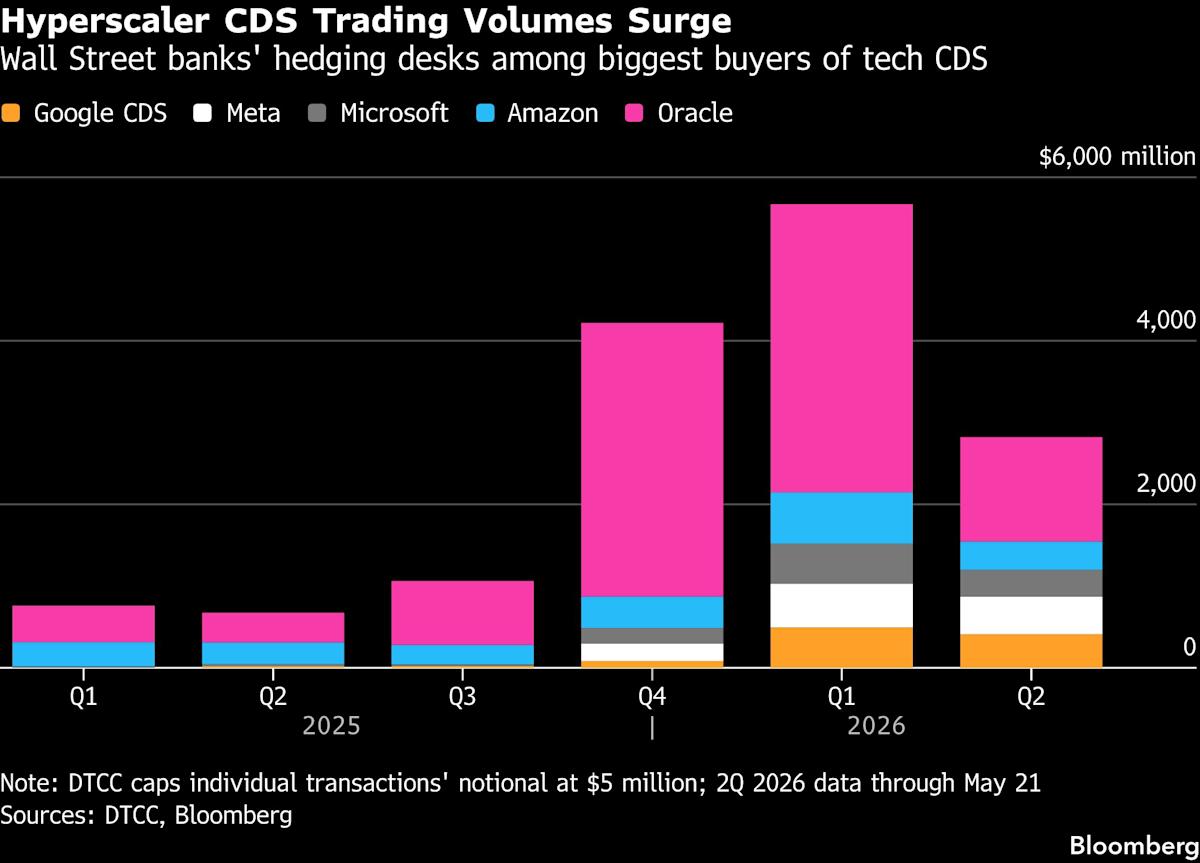

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Dow Jones Index Celebrates 130th Anniversary with Key Stock Insights

- Dow Component Changes: Since its establishment in 1896, the Dow Jones Index has seen significant changes in its components, with recent additions like Nvidia and Amazon reflecting economic evolution, shifting investor perception from traditional low-growth stocks to a modern blend of growth and value stocks.

- Nvidia's Dividend Surge: On May 20, Nvidia raised its quarterly dividend from $0.01 to $1 per share, a staggering 2400% increase, which, despite a current yield of only 0.5%, attracts investors seeking passive income and indicates a shift towards a more stable earnings model amid surging AI demand.

- Visa's Strong Financial Performance: Despite economic uncertainties, Visa achieved a 9% increase in payment volume in its latest quarter, with valuations at 30 times free cash flow and 29 times earnings, showcasing the resilience of its business model and providing a compelling buying opportunity for investors despite stock price declines.

- Procter & Gamble's Rising Dividend Yield: Procter & Gamble raised its dividend for the 70th consecutive year in April, with a current yield of 3%, and despite challenges in volume growth, its strong brand portfolio positions it as an ideal choice for risk-averse investors, trading at a P/E of just 21, below its 10-year average of 25.4.

See More

Nvidia Makes Significant Dividend Increase

- Dividend Surge: Nvidia raised its quarterly dividend from $0.01 to $1 per share on May 20, marking a staggering 2,400% increase, which, despite a low yield of 0.5%, makes it more attractive for investors seeking passive income.

- Market Share Expansion: Nvidia has broadened its market share in data centers by delivering new rack-scale solutions, including multi-chip systems to Anthropic, OpenAI, Oracle, and SpaceX on May 18, indicating strong growth potential amid surging AI demand.

- Visa Investment Opportunity: Despite a 6.2% decline in Visa's stock year-to-date, its reasonable valuation at 30 times free cash flow and 29 times earnings presents an excellent buying opportunity, with double-digit revenue and earnings growth reflecting its robust business model.

- Procter & Gamble Stability: Procter & Gamble raised its dividend for the 70th consecutive year in April, and despite sluggish volume growth leading to a mere 4.7% stock price increase over five years, its 21 times earnings valuation remains attractive for risk-averse investors.

See More

Snowflake Set to Announce Q1 Fiscal 2027 Results with Strong Growth Indicators

- Strong Earnings Outlook: Snowflake anticipates Q1 fiscal 2027 earnings of 32 cents per share, reflecting a 33.33% year-over-year increase, with revenue expectations at $1.32 billion, indicating a 26.85% growth, showcasing robust performance in AI and client expansion.

- Significant Customer Growth: As of Q4 fiscal 2026, Snowflake's net revenue retention rate reached 125%, with 740 net new customers added, a 40% year-over-year increase, indicating enhanced competitiveness in the market, a trend expected to continue in the upcoming earnings report.

- Product Revenue Projections: The company expects product revenues to range between $1.262 billion and $1.267 billion for Q1, reflecting a 27% year-over-year growth, with the Zacks consensus estimate at $1.26 billion, highlighting strong market demand for its offerings.

- Increased Competitive Pressure: Despite Snowflake's expanding product portfolio, it faces intense competition from major cloud providers like Oracle, Amazon, and Alphabet, particularly in the rapidly evolving AI sector, which may pose threats to its market share.

See More

Microsoft and Oracle Experience Strong Demand for Cloud Services

- Microsoft Cloud Revenue Growth: Microsoft Cloud reported $54 billion in revenue for Q3 FY2023, a 29% year-over-year increase, with Azure revenue surging 40% despite supply constraints, demonstrating the company's strong competitive position in the cloud market.

- Strong AI Product Performance: Microsoft's AI products achieved an annualized revenue run rate of $37 billion, up 123% year-over-year, indicating sustained enterprise demand for AI services despite concerns over spending on AI infrastructure.

- Oracle Cloud Services Surge: Oracle's cloud infrastructure services revenue grew 84% to $4.9 billion in the recent quarter, with multicloud database service demand skyrocketing by 531%, reflecting enterprises' long-term commitment to AI investments.

- Optimistic Future Outlook: Oracle's management raised fiscal 2027 revenue guidance to $90 billion, signaling demand exceeding expectations, while analysts have increased long-term earnings growth forecasts to 23%, providing strong market return potential for investors.

See More

Microsoft and Oracle's Cloud Growth Potential Amid Market Pullback

- Microsoft Cloud Growth: Microsoft's cloud revenue reached $54 billion in the latest fiscal quarter, reflecting a 29% year-over-year increase, indicating that despite supply constraints, Azure's 40% growth remains unaffected by competition, showcasing the company's strong position in the cloud market.

- Copilot User Surge: Microsoft 365 Copilot paid seats have exceeded 20 million, representing a 250% year-over-year increase, which indicates a rapidly growing demand for AI assistants among enterprises, further solidifying Microsoft's market share in the AI sector.

- Oracle Debt Risks and Opportunities: Oracle's long-term debt has surged 71% over the past two years to $159 billion; however, management does not expect to issue new debt beyond 2026, potentially setting the stage for a stock rebound, especially as cloud services continue to show robust growth.

- Cloud Services Contract Growth: Oracle's remaining performance obligations grew 325% year-over-year to $553 billion, demonstrating a long-term commitment from enterprises to AI, providing high visibility into future demand and supporting the company's $90 billion revenue forecast for fiscal 2027.

See More

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More