Nvidia's Sovereign AI Revenue Triples in Fiscal 2026

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 28 2026

0mins

Should l Buy NVDA?

Source: NASDAQ.COM

- Strong Earnings Report: Nvidia reported a revenue of $68.1 billion for Q4 fiscal 2026, marking a 73% year-over-year increase and surpassing Wall Street's estimate of $66.2 billion, showcasing robust demand for AI and solidifying its leadership in the GPU market.

- Sovereign AI Business Growth: The company's sovereign AI revenue tripled year-over-year to over $30 billion in fiscal 2026, accounting for 13.9% of total revenue, reflecting accelerated investments in AI infrastructure by countries, particularly driven by defense needs from NATO nations.

- Optimistic Future Outlook: Management guided for Q1 fiscal 2027 revenue of $78 billion, significantly exceeding analysts' expectations of $72 billion, indicating sustained strong performance and confidence in the AI sector.

- Space AI Application Potential: CEO Jensen Huang highlighted the significant potential for AI applications in space, noting that while current economics are poor, advancements will lead to the establishment of more AI data centers in space, further expanding the company's market reach.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 235.740

Low

200.00

Averages

264.97

High

352.00

Current: 235.740

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia Market Cap Surpasses $5.36 Trillion

- Market Recovery: Nvidia (NVDA) saw its market cap dip below $5 trillion earlier this year, but since March, its stock has surged 18%, currently valued at $5.36 trillion, outperforming the S&P 500 and indicating strong market recovery potential.

- AI Technology Leadership: With its deep expertise in GPUs, Nvidia has positioned itself as a key driver of artificial intelligence development, and its latest Vera Rubin architecture is expected to be widely adopted by every cloud model builder, further solidifying its market position.

- Optimistic Earnings Forecast: Nvidia is expected to report a 79% sales increase in its upcoming May 20 earnings report for Q1 2027, with projected earnings per share rising from $0.81 last year to $1.78, showcasing robust profitability and market confidence.

- Investor Confidence Restored: Following strong Q1 earnings reports from major AI developers like Amazon and Alphabet, market confidence in Nvidia's growth prospects has been restored, with CEO Jensen Huang's mention of a $1 trillion sales opportunity further fueling investor optimism.

See More

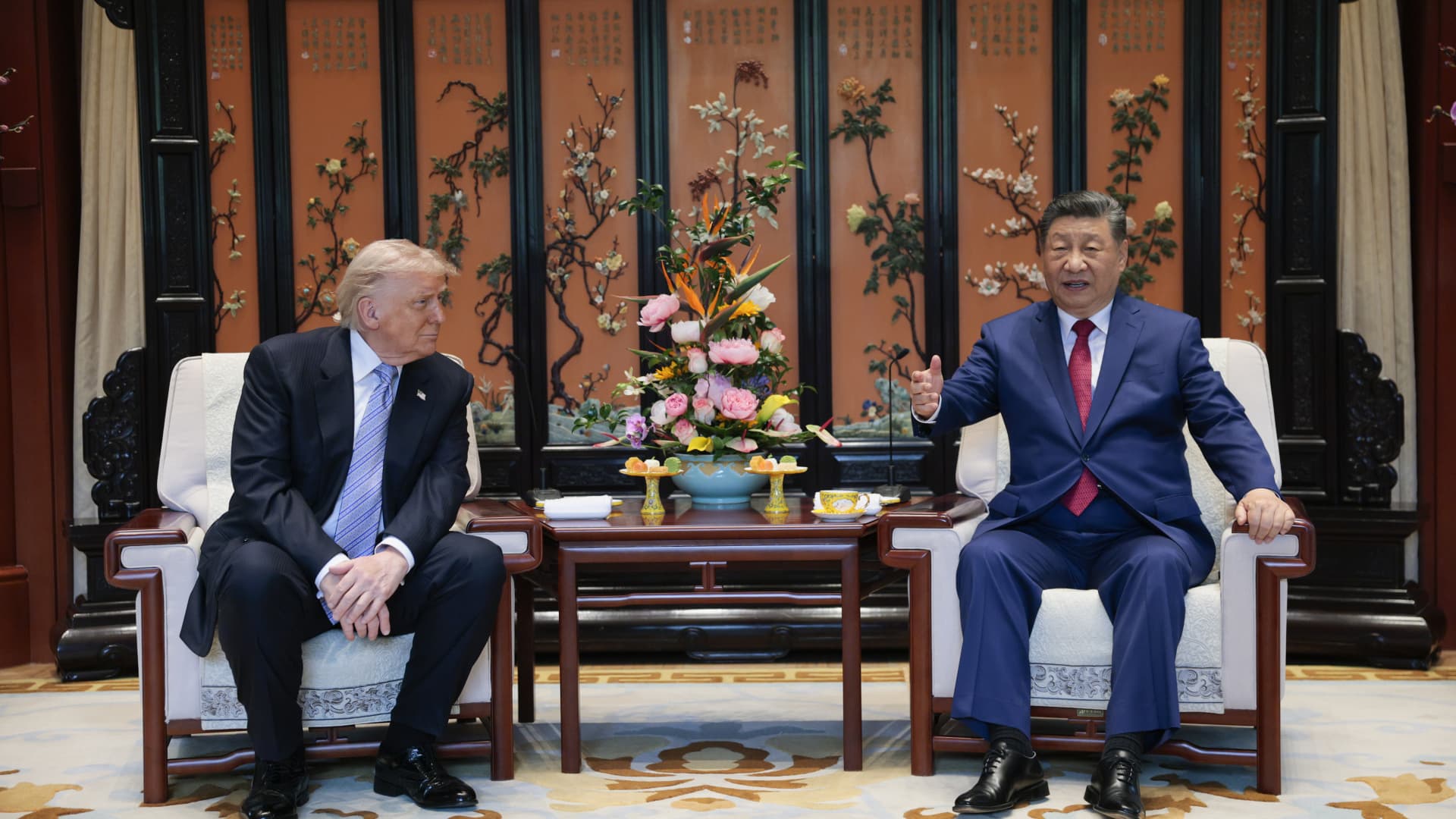

Trump Invites Xi to White House for Trade Talks

- Meeting Context: On May 15, 2026, U.S. President Trump met with Chinese President Xi Jinping at Zhongnanhai Garden in Beijing, discussing future trade negotiations, highlighting the complexity and significance of U.S.-China relations.

- White House Invitation: Trump announced at a state dinner his invitation for Xi to visit the White House on September 24, indicating that trade talks will extend beyond this week's two-day summit in Beijing, potentially influencing future economic policy directions.

- Strategic Stability Framework: Xi stated that both nations agreed to a framework of 'strategic stability' for the next three years, which could lay the groundwork for long-term development in bilateral relations, although specific agreements remain unconfirmed.

- Future Meeting Arrangements: The two leaders may meet again during the UN General Assembly in September, the APEC meeting in November, and the G20 meeting in December, providing opportunities for further economic cooperation in these significant international forums.

See More

Global Memory Shortage Impacts Gaming Industry

- Memory Shortage Affects Prices: The global shortage of memory and storage components has led Microsoft and Sony to raise console prices, with the Xbox Series X increasing from $499 to $649, indicating a direct impact of rising costs on consumers.

- Declining Sales Trend: Microsoft reported a 33% year-over-year decline in hardware revenue, while Sony's PlayStation 5 shipments plummeted 46% from 2.8 million to 1.5 million units, reflecting the negative impact of price increases on sales.

- Pressure on Nintendo: Nintendo plans to implement a $50 price increase on September 1, just before the holiday shopping season, which may lead consumers to purchase without realizing the price hike, further affecting its market performance.

- Game Release Impact on Sales: While Grand Theft Auto 6 is expected to be one of the best-selling games in history, potentially boosting Xbox and PlayStation sales, Nintendo's exclusion from this release may leave it at a competitive disadvantage.

See More

Can the AI Rally Sustain Amid Inflation Fears?

- Market Performance Review: The S&P 500 has surged approximately 19% since its March low, surpassing 7,500 for the first time this week, reflecting a revival in enthusiasm for artificial intelligence, yet the absence of cyclical sectors raises concerns.

- Internal and External Pressures: Despite a 3% rise in the S&P 500 this month, it remains nearly flat on an equal-weight basis, with the financial sector being the worst performer year-to-date, down over 6%, indicating potential impacts of high inflation on the economy.

- Nvidia Earnings Outlook: Nvidia is set to report earnings, with high expectations that CEO Jensen Huang will once again deliver a beat, although its market cap nearing $6 trillion marks a historic high, its valuation appears relatively attractive compared to peers.

- Retail Market Dynamics: Retailers like Walmart and Target are about to release earnings, and the low consumer sentiment may affect sales performance, particularly for lower-income consumers under pressure from rising oil prices, with Walmart's low-price strategy potentially giving it a competitive edge.

See More

Cerebras IPO Surges, Nears $100 Billion Market Cap

- Strong IPO Performance: Cerebras closed its first day of trading with a market cap nearing $100 billion, marking it as one of the largest IPOs in tech history and signaling robust market demand for AI chips.

- Chip Technology Innovation: The WSE-3 chip from Cerebras is 57 times larger than traditional GPUs and contains 50 times the number of transistors, providing a competitive edge in AI applications despite using a less advanced 5-nanometer process.

- Robust Market Demand: The CFO of Cerebras noted that the overwhelming demand for their fast inference products has led to supply challenges, with expectations of tight capacity until 2027, highlighting the immense potential of the AI chip market.

- Intensifying Industry Competition: The successful IPO of Cerebras paves the way for other custom ASIC startups, particularly as demand for AI chips surges, with competitors like Groq and SambaNova actively vying for market share.

See More

Trump Makes Significant Investments in Palantir Stock

- Significant Investment: Trump purchased between $247,008 and $630,000 worth of Palantir stock in Q1 2026, indicating strong confidence in the company's potential, particularly in the AI sector.

- Frequent Transactions: In March alone, Trump executed at least seven trades totaling up to $530,000 in Palantir shares, suggesting an active strategy to capitalize on short-term price fluctuations amid market volatility.

- Market Reaction: Trump's praise for Palantir coincided with the stock's worst week in over a year, reflecting investor concerns about its future prospects; his endorsement may help bolster investor confidence in the company.

- Diversified Investments: In addition to Palantir, Trump also invested in Nvidia, ServiceNow, and other tech firms during the same period, demonstrating a broad interest in AI and software, potentially aiming to mitigate risks and seize growth opportunities across the sector.

See More

Nvidia Market Cap Surpasses $5.36 Trillion

- Market Recovery: Nvidia (NVDA) saw its market cap dip below $5 trillion earlier this year, but since March, its stock has surged 18%, currently valued at $5.36 trillion, outperforming the S&P 500 and indicating strong market recovery potential.

- AI Technology Leadership: With its deep expertise in GPUs, Nvidia has positioned itself as a key driver of artificial intelligence development, and its latest Vera Rubin architecture is expected to be widely adopted by every cloud model builder, further solidifying its market position.

- Optimistic Earnings Forecast: Nvidia is expected to report a 79% sales increase in its upcoming May 20 earnings report for Q1 2027, with projected earnings per share rising from $0.81 last year to $1.78, showcasing robust profitability and market confidence.

- Investor Confidence Restored: Following strong Q1 earnings reports from major AI developers like Amazon and Alphabet, market confidence in Nvidia's growth prospects has been restored, with CEO Jensen Huang's mention of a $1 trillion sales opportunity further fueling investor optimism.

See More

Trump Invites Xi to White House for Trade Talks

- Meeting Context: On May 15, 2026, U.S. President Trump met with Chinese President Xi Jinping at Zhongnanhai Garden in Beijing, discussing future trade negotiations, highlighting the complexity and significance of U.S.-China relations.

- White House Invitation: Trump announced at a state dinner his invitation for Xi to visit the White House on September 24, indicating that trade talks will extend beyond this week's two-day summit in Beijing, potentially influencing future economic policy directions.

- Strategic Stability Framework: Xi stated that both nations agreed to a framework of 'strategic stability' for the next three years, which could lay the groundwork for long-term development in bilateral relations, although specific agreements remain unconfirmed.

- Future Meeting Arrangements: The two leaders may meet again during the UN General Assembly in September, the APEC meeting in November, and the G20 meeting in December, providing opportunities for further economic cooperation in these significant international forums.

See More

Global Memory Shortage Impacts Gaming Industry

- Memory Shortage Affects Prices: The global shortage of memory and storage components has led Microsoft and Sony to raise console prices, with the Xbox Series X increasing from $499 to $649, indicating a direct impact of rising costs on consumers.

- Declining Sales Trend: Microsoft reported a 33% year-over-year decline in hardware revenue, while Sony's PlayStation 5 shipments plummeted 46% from 2.8 million to 1.5 million units, reflecting the negative impact of price increases on sales.

- Pressure on Nintendo: Nintendo plans to implement a $50 price increase on September 1, just before the holiday shopping season, which may lead consumers to purchase without realizing the price hike, further affecting its market performance.

- Game Release Impact on Sales: While Grand Theft Auto 6 is expected to be one of the best-selling games in history, potentially boosting Xbox and PlayStation sales, Nintendo's exclusion from this release may leave it at a competitive disadvantage.

See More

Can the AI Rally Sustain Amid Inflation Fears?

- Market Performance Review: The S&P 500 has surged approximately 19% since its March low, surpassing 7,500 for the first time this week, reflecting a revival in enthusiasm for artificial intelligence, yet the absence of cyclical sectors raises concerns.

- Internal and External Pressures: Despite a 3% rise in the S&P 500 this month, it remains nearly flat on an equal-weight basis, with the financial sector being the worst performer year-to-date, down over 6%, indicating potential impacts of high inflation on the economy.

- Nvidia Earnings Outlook: Nvidia is set to report earnings, with high expectations that CEO Jensen Huang will once again deliver a beat, although its market cap nearing $6 trillion marks a historic high, its valuation appears relatively attractive compared to peers.

- Retail Market Dynamics: Retailers like Walmart and Target are about to release earnings, and the low consumer sentiment may affect sales performance, particularly for lower-income consumers under pressure from rising oil prices, with Walmart's low-price strategy potentially giving it a competitive edge.

See More

Cerebras IPO Surges, Nears $100 Billion Market Cap

- Strong IPO Performance: Cerebras closed its first day of trading with a market cap nearing $100 billion, marking it as one of the largest IPOs in tech history and signaling robust market demand for AI chips.

- Chip Technology Innovation: The WSE-3 chip from Cerebras is 57 times larger than traditional GPUs and contains 50 times the number of transistors, providing a competitive edge in AI applications despite using a less advanced 5-nanometer process.

- Robust Market Demand: The CFO of Cerebras noted that the overwhelming demand for their fast inference products has led to supply challenges, with expectations of tight capacity until 2027, highlighting the immense potential of the AI chip market.

- Intensifying Industry Competition: The successful IPO of Cerebras paves the way for other custom ASIC startups, particularly as demand for AI chips surges, with competitors like Groq and SambaNova actively vying for market share.

See More

Trump Makes Significant Investments in Palantir Stock

- Significant Investment: Trump purchased between $247,008 and $630,000 worth of Palantir stock in Q1 2026, indicating strong confidence in the company's potential, particularly in the AI sector.

- Frequent Transactions: In March alone, Trump executed at least seven trades totaling up to $530,000 in Palantir shares, suggesting an active strategy to capitalize on short-term price fluctuations amid market volatility.

- Market Reaction: Trump's praise for Palantir coincided with the stock's worst week in over a year, reflecting investor concerns about its future prospects; his endorsement may help bolster investor confidence in the company.

- Diversified Investments: In addition to Palantir, Trump also invested in Nvidia, ServiceNow, and other tech firms during the same period, demonstrating a broad interest in AI and software, potentially aiming to mitigate risks and seize growth opportunities across the sector.

See More