MODERNA Q1 EPS at USD -3.4, Beating IBES Estimate of USD -3.96

Moderna's Q1 EPS: Moderna reported an earnings per share (EPS) of $3.4 for the first quarter.

Comparison with Estimates: This EPS figure was higher than the estimated EPS of $3.96 by analysts.

Trade with 70% Backtested Accuracy

Analyst Views on MRNA

About MRNA

About the author

MODERNA REPORTS Q1 REVENUE OF $400 MILLION, EXCEEDING IBES ESTIMATE OF $228 MILLION

Moderna's Q1 Revenue: Moderna reported a revenue of USD 400 million for the first quarter.

Comparison with Estimates: This revenue figure significantly exceeds analysts' estimates, which were around USD 228 million.

MODERNA Q1 EPS at USD -3.4, Beating IBES Estimate of USD -3.96

Moderna's Q1 EPS: Moderna reported an earnings per share (EPS) of $3.4 for the first quarter.

Comparison with Estimates: This EPS figure was higher than the estimated EPS of $3.96 by analysts.

Moderna Set to Report Q1 Earnings Amid Revenue Concerns

- Earnings Report Outlook: Moderna is set to report its Q1 earnings on May 1 before market open, with investors looking for signs of revenue stabilization after a prolonged post-COVID downturn.

- Revenue and Loss Status: The company has faced a 90% revenue decline since 2022, with persistent cash burn exceeding $2 billion annually and no near-term path to profitability, indicating a fragile financial situation.

- Analyst Expectation Volatility: The consensus estimate calls for an EPS loss of -$3.96 on revenue of $236.36 million, with 4 upward revisions in revenue estimates but limited analyst confidence reflecting caution regarding the company's transition.

- Future Prospects and Challenges: While the company shows long-term potential in developing next-generation mRNA vaccines and therapeutics, short-term revenue remains heavily reliant on declining COVID sales, with significant clinical milestones not expected until late 2026.

Moderna Executive States Company is Seeking FDA Guidance on Resuming US Filing for Flu-COVID Combination Vaccine

Moderna's Next Steps: Moderna executives are awaiting guidance from the FDA regarding the next steps for resuming the filing process for their flu-COVID combination vaccine.

Focus on Combination Vaccine: The company is particularly focused on advancing its flu-COVID combination vaccine, which aims to address both illnesses in a single shot.

Moderna Targets 10% Revenue Growth for FY 2026

- Revenue Growth Target: Moderna is targeting a 10% increase in revenue for FY 2026 compared to 2025, with an expected 50% sales split between U.S. and international markets.

- Q1 Performance Exceeds Expectations: In Q1 of FY 2026, Moderna reported net product sales of $389 million, significantly surpassing the Street's estimate of $235.5 million, indicating a strong rebound in COVID vaccine demand.

- Vaccine Review Progress: The U.S. FDA reversed its initial rejection and agreed to review Moderna's mRNA flu vaccine in February, a shift that may reflect changes in regulatory policies and impact the company's future market strategies.

- Market Reaction: Despite retail investor sentiment shifting from 'extremely bearish' to 'bearish', Moderna's shares rose nearly 6% in pre-market trading on Friday, reflecting a positive market response to its Q1 earnings report.

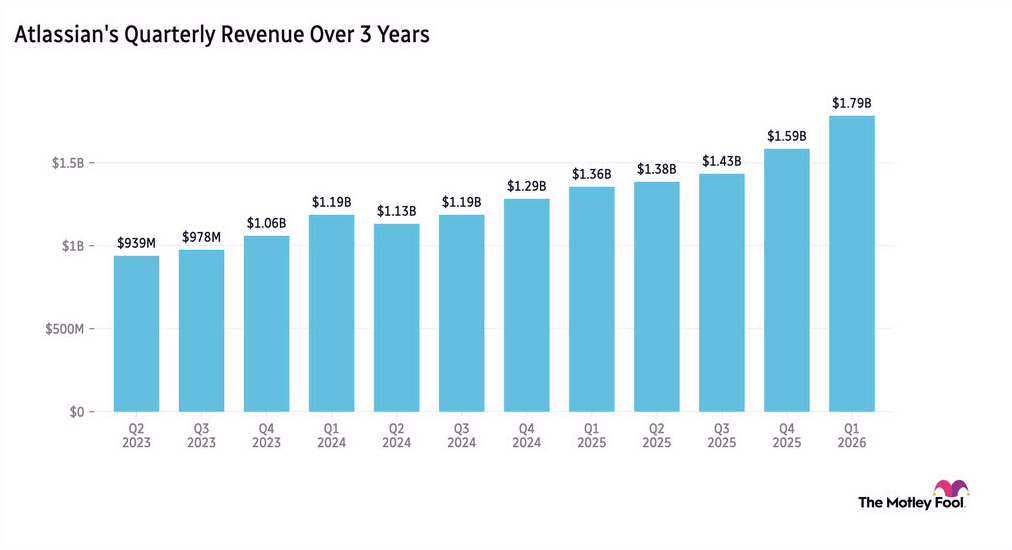

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.

MODERNA REPORTS Q1 REVENUE OF $400 MILLION, EXCEEDING IBES ESTIMATE OF $228 MILLION

Moderna's Q1 Revenue: Moderna reported a revenue of USD 400 million for the first quarter.

Comparison with Estimates: This revenue figure significantly exceeds analysts' estimates, which were around USD 228 million.

MODERNA Q1 EPS at USD -3.4, Beating IBES Estimate of USD -3.96

Moderna's Q1 EPS: Moderna reported an earnings per share (EPS) of $3.4 for the first quarter.

Comparison with Estimates: This EPS figure was higher than the estimated EPS of $3.96 by analysts.

Moderna Set to Report Q1 Earnings Amid Revenue Concerns

- Earnings Report Outlook: Moderna is set to report its Q1 earnings on May 1 before market open, with investors looking for signs of revenue stabilization after a prolonged post-COVID downturn.

- Revenue and Loss Status: The company has faced a 90% revenue decline since 2022, with persistent cash burn exceeding $2 billion annually and no near-term path to profitability, indicating a fragile financial situation.

- Analyst Expectation Volatility: The consensus estimate calls for an EPS loss of -$3.96 on revenue of $236.36 million, with 4 upward revisions in revenue estimates but limited analyst confidence reflecting caution regarding the company's transition.

- Future Prospects and Challenges: While the company shows long-term potential in developing next-generation mRNA vaccines and therapeutics, short-term revenue remains heavily reliant on declining COVID sales, with significant clinical milestones not expected until late 2026.

Moderna Executive States Company is Seeking FDA Guidance on Resuming US Filing for Flu-COVID Combination Vaccine

Moderna's Next Steps: Moderna executives are awaiting guidance from the FDA regarding the next steps for resuming the filing process for their flu-COVID combination vaccine.

Focus on Combination Vaccine: The company is particularly focused on advancing its flu-COVID combination vaccine, which aims to address both illnesses in a single shot.

Moderna Targets 10% Revenue Growth for FY 2026

- Revenue Growth Target: Moderna is targeting a 10% increase in revenue for FY 2026 compared to 2025, with an expected 50% sales split between U.S. and international markets.

- Q1 Performance Exceeds Expectations: In Q1 of FY 2026, Moderna reported net product sales of $389 million, significantly surpassing the Street's estimate of $235.5 million, indicating a strong rebound in COVID vaccine demand.

- Vaccine Review Progress: The U.S. FDA reversed its initial rejection and agreed to review Moderna's mRNA flu vaccine in February, a shift that may reflect changes in regulatory policies and impact the company's future market strategies.

- Market Reaction: Despite retail investor sentiment shifting from 'extremely bearish' to 'bearish', Moderna's shares rose nearly 6% in pre-market trading on Friday, reflecting a positive market response to its Q1 earnings report.

Atlassian Shares Surge 25% on AI-Driven Revenue Growth

- Revenue Surge: Atlassian's third-quarter revenue rose 32% year-over-year, leading to a 25% jump in pre-market trading, and despite restructuring costs impacting profitability, non-GAAP earnings per share soared by 80%, reflecting strong demand for AI services.

- Cloud Transition: CFO James Chuong cautioned that the shift of customers to cloud services would result in a more muted level of data center expansion, with expectations for moderated revenue growth in Q4, which could impact future market performance.

- Product Advantage: Analyst Meilin Quinn noted that while workflows may be taken over by agents, there remains a need for trusted company knowledge and systems, providing Atlassian with a stronger foothold in engineering processes and enhancing its competitive edge.

- Market Reaction: Major stock indexes hit new highs amid continued growth in AI spending, with the S&P 500 closing above 7,200 points for the first time, reflecting strong market confidence in tech stocks and further boosting Atlassian's stock performance.