Microsoft Faces Quarterly Decline but Bright Growth Prospects Ahead

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy MSFT?

Source: NASDAQ.COM

- Quarterly Performance Decline: Microsoft experienced a 24% drop in share price during Q1 2026, marking its steepest quarterly decline since the 2008 financial crisis, indicating significant challenges and market unease.

- Surge in Capital Expenditures: The company plans to increase capital expenditures to $146 billion in fiscal 2026, primarily aimed at expanding AI infrastructure, which, while increasing short-term financial pressure, is expected to enhance competitiveness in the long run.

- Revenue and Earnings Growth: Despite challenges, Microsoft reported a 17% year-over-year revenue increase to $81.3 billion in Q2 2026, with GAAP earnings soaring 60% year-over-year, demonstrating resilience and growth potential in its business.

- Analysts Remain Bullish: Among 57 analysts, 54 rated Microsoft as a

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 358.960

Low

500.00

Averages

631.36

High

678.00

Current: 358.960

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company that develops and supports software, services, devices, and solutions. Its Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services, spanning a variety of devices and platforms. It comprises Microsoft 365 Commercial products and cloud services; Microsoft 365 Consumer products and cloud services; LinkedIn, and Dynamics products and cloud services. The Intelligent Cloud segment consists of its public, private, and hybrid server products and cloud services. It comprises server products and cloud services, including Azure, and enterprise and partner services, including Enterprise Support Services. Its More Personal Computing segment primarily comprises Windows and Devices, including Windows OEM licensing; Gaming, including Xbox hardware and Xbox content; Search and news advertising, comprising Bing and Copilot, Microsoft News, and Microsoft Edge.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft's AI Business Pullback Triggers Investor Panic

- Market Share Challenges: Microsoft's AI-powered Copilot chatbot holds only a 3% global market share, with around 6% in North America, but the minuscule fraction of paying users indicates difficulties in market penetration, potentially impacting future revenue growth.

- Cloud Growth Slowdown: Revenue growth for Microsoft's Azure has decreased from 39% in September to 38%, with expectations for further deceleration in the current quarter, a trend that lags behind competitors like Alphabet, raising investor concerns about future performance.

- Capital Expenditure Pressure: Microsoft plans to invest $120 billion in AI infrastructure this fiscal year; despite strong demand, the failure to meet return expectations has led to an overreaction in the market, resulting in a 35% stock price decline.

- Long-Term Potential Remains: Despite facing short-term challenges, Microsoft remains a key global technology player, with its Windows operating system installed on two-thirds of desktop computers worldwide, and analysts' target price of $587.77 suggests over 60% upside potential.

See More

Microsoft to Invest Over $1B in Thailand's Cloud and AI Infrastructure

- Investment Initiative: Microsoft plans to invest over $1 billion in Thailand between 2026 and 2028, focusing on cloud and AI infrastructure to enhance the country's global competitiveness and economic prosperity.

- Workforce Upskilling: In partnership with Thailand's Ministry of Labour's Department of Skill Development, Microsoft aims to accelerate workforce readiness by upskilling and certifying 150,000 workers, preparing them for the rapidly evolving AI economy.

- Educational Programs: The launch of Microsoft Elevate for Educators and Microsoft Elevate for Changemakers in Thailand is designed to strengthen the education, workforce, and social impact systems, enabling more individuals to learn, work, and thrive in the AI-driven economy.

- National Strategy: This investment is central to Microsoft's initiative, “Advancing National Growth, Prosperity, and Global Competitiveness with AI,” which seeks to provide inclusive access to cloud and AI technologies for citizens across all sectors of the economy.

See More

Big Tech Continues Billions in AI Data Center Investments

- AI Infrastructure Investment Surge: Statista projects that AI infrastructure investment will reach $902 billion by 2029, a significant increase from $334 billion in 2025, indicating sustained demand and enthusiasm for AI technologies in the market.

- Nvidia's Market Dominance: Nvidia's data center business accounted for over 90% of its revenue last quarter, growing 75% year-over-year, with an impressive $120 billion net income on $215 billion total revenue, solidifying its core position in AI infrastructure.

- Iren's Power Assurance: Iren has secured over 4.5 gigawatts of power supply and focuses on designing, building, and operating data centers, expecting to achieve an annualized revenue run rate of $3.4 billion by 2026, showcasing its strong capability to meet tech giants' demands.

- Long-Term Investment Potential: Despite significant stock price increases for both Nvidia and Iren, analysts expect Nvidia's earnings to grow by 38% annually over the next five years, while Iren's market valuation still has room for upside, indicating both companies remain attractive in the AI boom.

See More

AI Infrastructure Spending to Reach $902 Billion by 2029

- Market Growth Forecast: Statista projects that AI infrastructure spending will reach $902 billion by 2029, a significant increase from $334 billion in 2025, indicating strong demand and investment potential in AI technologies.

- Nvidia's Market Dominance: Nvidia's data center business accounted for over 90% of its revenue last quarter, growing 75% year-over-year, highlighting its critical role and high margins in the AI infrastructure landscape.

- Iren's Strategic Advantage: Iren has secured over 4.5 gigawatts of power and signed a $9.7 billion contract with Microsoft, expecting to generate $3.4 billion in annualized revenue by 2026, showcasing its strong execution capabilities and market opportunities in data center construction.

- Long-Term Investment Outlook: While Nvidia's valuation reflects strong growth, its projected earnings growth of 38% over the next five years, combined with Iren's untapped market potential, suggests both companies remain compelling investment opportunities amid the AI boom.

See More

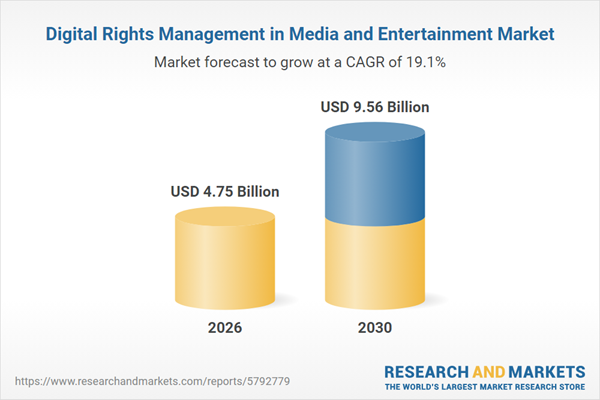

Digital Rights Management Market on Rapid Growth Trajectory

- Market Size Growth: The digital rights management market is projected to grow from $3.97 billion in 2025 to $4.75 billion in 2026, reflecting a 19.1% CAGR, driven by the proliferation of digital media channels and video-on-demand platforms.

- Surge in OTT Consumption: The OTT audience in India reached over 481 million in 2023, marking a 13.5% increase from 2022, significantly fueling the demand for digital rights management to protect content from unauthorized duplication.

- Strengthened Strategic Collaborations: CDNetworks' partnership with Irdeto integrates DRM capabilities into its media delivery platform, expected to enhance content protection, while Vobile Group Inc.'s acquisition of Pex Inc. aims to solidify its leadership through advanced content identification technologies.

- Diverse Market Participants: Key players include Google, Microsoft, and Apple, with North America being the largest market in 2025, highlighting the region's significance in the digital rights management landscape and reflecting broad global participation.

See More

Institutional Concentration in Tech Stocks Persists

- High Concentration: According to a Bank of America report, Microsoft (MSFT) and Amazon (AMZN) are among the most overweight positions held by institutional investors, indicating their significant importance in portfolios and reflecting market confidence in their continued growth potential.

- AI Infrastructure Role: Nvidia (NVDA) and Alphabet's Google (GOOGL, GOOG) also maintain overweight positions, underscoring their central roles in artificial intelligence and cloud ecosystems, which further solidifies their market leadership.

- Meta's Relative Strength: Meta Platforms (META) shows significant overweight relative to its S&P 500 weight, indicating that institutional investors are optimistic about its future growth prospects, as evidenced by the high allocation levels.

- Apple and Tesla Divergence: While Apple (AAPL) is widely held, its overweight positioning is more moderate, suggesting stability as a core holding, whereas Tesla (TSLA) is closer to benchmark weight, reflecting a more cautious stance among institutional investors.

See More

Microsoft's AI Business Pullback Triggers Investor Panic

- Market Share Challenges: Microsoft's AI-powered Copilot chatbot holds only a 3% global market share, with around 6% in North America, but the minuscule fraction of paying users indicates difficulties in market penetration, potentially impacting future revenue growth.

- Cloud Growth Slowdown: Revenue growth for Microsoft's Azure has decreased from 39% in September to 38%, with expectations for further deceleration in the current quarter, a trend that lags behind competitors like Alphabet, raising investor concerns about future performance.

- Capital Expenditure Pressure: Microsoft plans to invest $120 billion in AI infrastructure this fiscal year; despite strong demand, the failure to meet return expectations has led to an overreaction in the market, resulting in a 35% stock price decline.

- Long-Term Potential Remains: Despite facing short-term challenges, Microsoft remains a key global technology player, with its Windows operating system installed on two-thirds of desktop computers worldwide, and analysts' target price of $587.77 suggests over 60% upside potential.

See More

Microsoft to Invest Over $1B in Thailand's Cloud and AI Infrastructure

- Investment Initiative: Microsoft plans to invest over $1 billion in Thailand between 2026 and 2028, focusing on cloud and AI infrastructure to enhance the country's global competitiveness and economic prosperity.

- Workforce Upskilling: In partnership with Thailand's Ministry of Labour's Department of Skill Development, Microsoft aims to accelerate workforce readiness by upskilling and certifying 150,000 workers, preparing them for the rapidly evolving AI economy.

- Educational Programs: The launch of Microsoft Elevate for Educators and Microsoft Elevate for Changemakers in Thailand is designed to strengthen the education, workforce, and social impact systems, enabling more individuals to learn, work, and thrive in the AI-driven economy.

- National Strategy: This investment is central to Microsoft's initiative, “Advancing National Growth, Prosperity, and Global Competitiveness with AI,” which seeks to provide inclusive access to cloud and AI technologies for citizens across all sectors of the economy.

See More

Big Tech Continues Billions in AI Data Center Investments

- AI Infrastructure Investment Surge: Statista projects that AI infrastructure investment will reach $902 billion by 2029, a significant increase from $334 billion in 2025, indicating sustained demand and enthusiasm for AI technologies in the market.

- Nvidia's Market Dominance: Nvidia's data center business accounted for over 90% of its revenue last quarter, growing 75% year-over-year, with an impressive $120 billion net income on $215 billion total revenue, solidifying its core position in AI infrastructure.

- Iren's Power Assurance: Iren has secured over 4.5 gigawatts of power supply and focuses on designing, building, and operating data centers, expecting to achieve an annualized revenue run rate of $3.4 billion by 2026, showcasing its strong capability to meet tech giants' demands.

- Long-Term Investment Potential: Despite significant stock price increases for both Nvidia and Iren, analysts expect Nvidia's earnings to grow by 38% annually over the next five years, while Iren's market valuation still has room for upside, indicating both companies remain attractive in the AI boom.

See More

AI Infrastructure Spending to Reach $902 Billion by 2029

- Market Growth Forecast: Statista projects that AI infrastructure spending will reach $902 billion by 2029, a significant increase from $334 billion in 2025, indicating strong demand and investment potential in AI technologies.

- Nvidia's Market Dominance: Nvidia's data center business accounted for over 90% of its revenue last quarter, growing 75% year-over-year, highlighting its critical role and high margins in the AI infrastructure landscape.

- Iren's Strategic Advantage: Iren has secured over 4.5 gigawatts of power and signed a $9.7 billion contract with Microsoft, expecting to generate $3.4 billion in annualized revenue by 2026, showcasing its strong execution capabilities and market opportunities in data center construction.

- Long-Term Investment Outlook: While Nvidia's valuation reflects strong growth, its projected earnings growth of 38% over the next five years, combined with Iren's untapped market potential, suggests both companies remain compelling investment opportunities amid the AI boom.

See More

Digital Rights Management Market on Rapid Growth Trajectory

- Market Size Growth: The digital rights management market is projected to grow from $3.97 billion in 2025 to $4.75 billion in 2026, reflecting a 19.1% CAGR, driven by the proliferation of digital media channels and video-on-demand platforms.

- Surge in OTT Consumption: The OTT audience in India reached over 481 million in 2023, marking a 13.5% increase from 2022, significantly fueling the demand for digital rights management to protect content from unauthorized duplication.

- Strengthened Strategic Collaborations: CDNetworks' partnership with Irdeto integrates DRM capabilities into its media delivery platform, expected to enhance content protection, while Vobile Group Inc.'s acquisition of Pex Inc. aims to solidify its leadership through advanced content identification technologies.

- Diverse Market Participants: Key players include Google, Microsoft, and Apple, with North America being the largest market in 2025, highlighting the region's significance in the digital rights management landscape and reflecting broad global participation.

See More

Institutional Concentration in Tech Stocks Persists

- High Concentration: According to a Bank of America report, Microsoft (MSFT) and Amazon (AMZN) are among the most overweight positions held by institutional investors, indicating their significant importance in portfolios and reflecting market confidence in their continued growth potential.

- AI Infrastructure Role: Nvidia (NVDA) and Alphabet's Google (GOOGL, GOOG) also maintain overweight positions, underscoring their central roles in artificial intelligence and cloud ecosystems, which further solidifies their market leadership.

- Meta's Relative Strength: Meta Platforms (META) shows significant overweight relative to its S&P 500 weight, indicating that institutional investors are optimistic about its future growth prospects, as evidenced by the high allocation levels.

- Apple and Tesla Divergence: While Apple (AAPL) is widely held, its overweight positioning is more moderate, suggesting stability as a core holding, whereas Tesla (TSLA) is closer to benchmark weight, reflecting a more cautious stance among institutional investors.

See More