Markets Rise Amid Geopolitical Headlines

Markets are higher near noon as geopolitical headlines remain at the center of the tape. The conflict in the Middle East has entered its fifth day and while there have been reports Iran has made indirect contact about potential talks, feeding some risk appetite, uncertainty around the durability of any de-escalation continues to drive positioning. The energy complex continues to influence the broader market's direction as the easing in the recent oil price surge has provided a tailwind, but traders are still cautious amid the ongoing Iran conflict.Global equity markets outside the U.S. are showing stress, with Asian markets taking a particularly severe hit. South Korea's benchmark index experienced one of its largest historical selloffs and other major Asian indices like Japan's Nikkei and Taiwan's TAIEX traded materially lower as well.Get caught up quickly on the top news and calls moving stocks with these five Top Five lists.1. STOCK NEWS:Applecontinued a week of, with the latest being the MacBook Neo laptopA subsidiary of Roivant Sciencesand Arbutus Biopharmaentered into a COVID-19with Modernaworth up to $2.25BRoss Storesreported a, raised its quarterly dividend and approved a new two-year $2.55B stock repurchase planCoreWeaveannounced awith Perplexity to support its inference workloadsFordwere down 5.5% year-over-year in February to 149,962 vehicles2. WALL STREET CALLS:BofATeslaat Buy as the "leader" of the next era of mobilityTargetto Outperform at Telsey Advisory and to Market Perform at BernsteinPiper Sandlerto Outperform at NorthlandLegalZoomto Underweight at BarclaysFirst Solarto Hold at GLJ Research on weak guidance3. AROUND THE WEB:AmazonPublisher Services, which helps websites run ad auctions, is exploring offering technology to help other apps and sites sell ads in AI chatbots, The Information saysOpenAI is developing an alternative to Microsoft'sGitHub, The Information reportsMetais testing a shopping research feature for its AI chatbot that will allow requests for product suggestions, Bloomberg saysThe White House is debating if it will allow Tencentto maintain stakes in popular video game groups, FT reportsDraftKing'sstrategy to become a prediction market leader is to copy the formula it used to dominate the online sports betting industry, WSJ reports4. MOVERS:SCHMIDgains in New York afterthe first specialized InfinityLine H+ systemEvolushigher afterand providing guidance for FY26Babcock & Wilcoxincreases afterand announcing it has received full notice to proceed on a $2.4B design-build agreement with Base ElectronIndie Semiconductorfalls after filing to sell $150M ofGitLablower afterand authorizing a $400M share repurchase program5. EARNINGS/GUIDANCEAbercrombie & Fitchand provided guidance for Q1 and FY26Holleywith EPS missing consensusDycom, with CEO Dan Peyovich commenting, "Our strong fourth quarter performance closed a record year for Dycom"Bath & Body Works, with EPS and revenue beating consensusBayerand provided guidance for FY26INDEXES:Near midday, the Dow was up 0.68%, or 329.64, to 48,830.91, the Nasdaq was up 1.46%, or 329.81, to 22,846.51, and the S&P 500 was up 0.87%, or 59.51, to 6,876.14.

Trade with 70% Backtested Accuracy

Analyst Views on AMZN

About AMZN

About the author

Amazon's AI-Driven Growth Potential is Significant

- AI Chip Partnership: Amazon's collaboration with Meta Platforms, which will utilize Amazon's Graviton5 processors, not only opens new sales opportunities for Amazon's custom chip business but also strengthens its internal tech stack's competitiveness.

- Cloud Infrastructure Growth: Amazon Web Services (AWS) reported a 28% year-over-year revenue increase to $37.59 billion in Q1, surpassing Wall Street estimates, indicating that AI demand is driving higher utilization rates and promising future growth.

- E-commerce and Digital Advertising Integration: As the world's largest online retailer, Amazon's advertising revenue grew 24% year-over-year to $17.24 billion in Q1, with AI integration expected to enhance profitability and market share in both e-commerce and advertising sectors.

- Profit Driver: Although AWS accounted for only 20.7% of total sales in Q1, it generated the majority of profits, and with the cloud business accelerating, Amazon's earnings outlook is increasingly positive, boosting investor confidence.

Market Dynamics and Corporate Performance Analysis

- Dell's Quarter Performance: Dell reported a quarter that exceeded expectations, with shares rising over 30%, indicating strong performance across all business levels, particularly in data center servers, which is expected to boost overall market confidence.

- Costco Membership Renewal Rates Up: Costco's latest earnings report showed improved membership renewal rates in the U.S. and Canada; although market reaction was muted, record performance in its gas business is likely to enhance membership loyalty and solidify its market position.

- Anthropic Surpasses OpenAI: Anthropic raised $65 billion at a $965 billion valuation, becoming the most valuable AI startup, a significant increase from $380 billion in February, showcasing explosive revenue growth and wealth creation potential in the AI sector.

- Cybersecurity Market Volatility: Okta beat expectations in its earnings report, with shares rising over 8%, while Zscaler's stock fell due to disappointing guidance, highlighting a divergence in the cybersecurity industry that affected the performance of other companies, including CrowdStrike.

Major Wall Street Rating Changes Overview

- Dell Upgrade: Susquehanna upgraded Dell from neutral to positive, citing increased confidence in a sustainable 8-10% operating margin and a 6% free cash flow margin, which supports a potential rerating of its EV/sales multiple to 3x, indicating strong market potential.

- Viper Energy Initiation: RBC initiated coverage of Viper Energy with an Outperform rating and a $58 price target, highlighting its advantages in scale and core Permian focus, positioning it as a best-in-class mineral and royalty company.

- SentinelOne Buy Rating: Bank of America upgraded SentinelOne from neutral to buy, viewing its solid quarterly performance as a strong entry point after an 18% decline in after-hours trading, reflecting confidence in its future growth prospects.

- XPeng Upgrade: Macquarie upgraded XPeng from neutral to outperform, noting its volume growth in the Chinese EV market, while future investments in humanoids and robotaxis provide additional upside potential for its stock.

SpaceX IPO Outlook and AI Investment Risks

- IPO Anticipation: SpaceX's planned IPO on June 12 is one of the most awaited public debuts in years, drawing significant investor interest in its future growth potential.

- AI Investment Scale: The company allocated $12.7 billion to artificial intelligence, significantly exceeding the $3.8 billion spent on its space segment, indicating a strategic pivot towards AI despite the associated high risks.

- Operating Loss Comparison: SpaceX's operating loss in AI reached $6.3 billion, far surpassing the $657 million loss from its space operations, raising concerns about the financial implications of such an imbalance for potential investors.

- Market Outlook and Risks: While SpaceX estimates a total addressable market of $26.5 trillion for AI, the uncertainty surrounding its massive expenditures and the ability to capture a significant market share necessitates careful risk assessment by investors considering the IPO.

SpaceX's AI Investments and IPO Outlook Analysis

- AI Investment Scale: SpaceX's investment in artificial intelligence reached $12.7 billion in 2025, significantly exceeding its $3.8 billion in space program spending, indicating the company's strong focus and expectations for future AI potential.

- Operating Loss Comparison: The operating loss in AI soared to $6.3 billion, far surpassing the $657 million loss from its space segment, highlighting the financial pressure and risks associated with its AI expenditures.

- Data Center Construction: The company is building Colossus and Colossus II data centers to support the training of next-generation AI models, and despite challenges related to energy consumption and public backlash, SpaceX plans to relocate data centers to space to address these issues.

- Market Outlook Assessment: SpaceX estimates its total addressable market for AI to be $26.5 trillion, and while facing high expenditures and uncertainties, investors must weigh the risks against potential rewards.

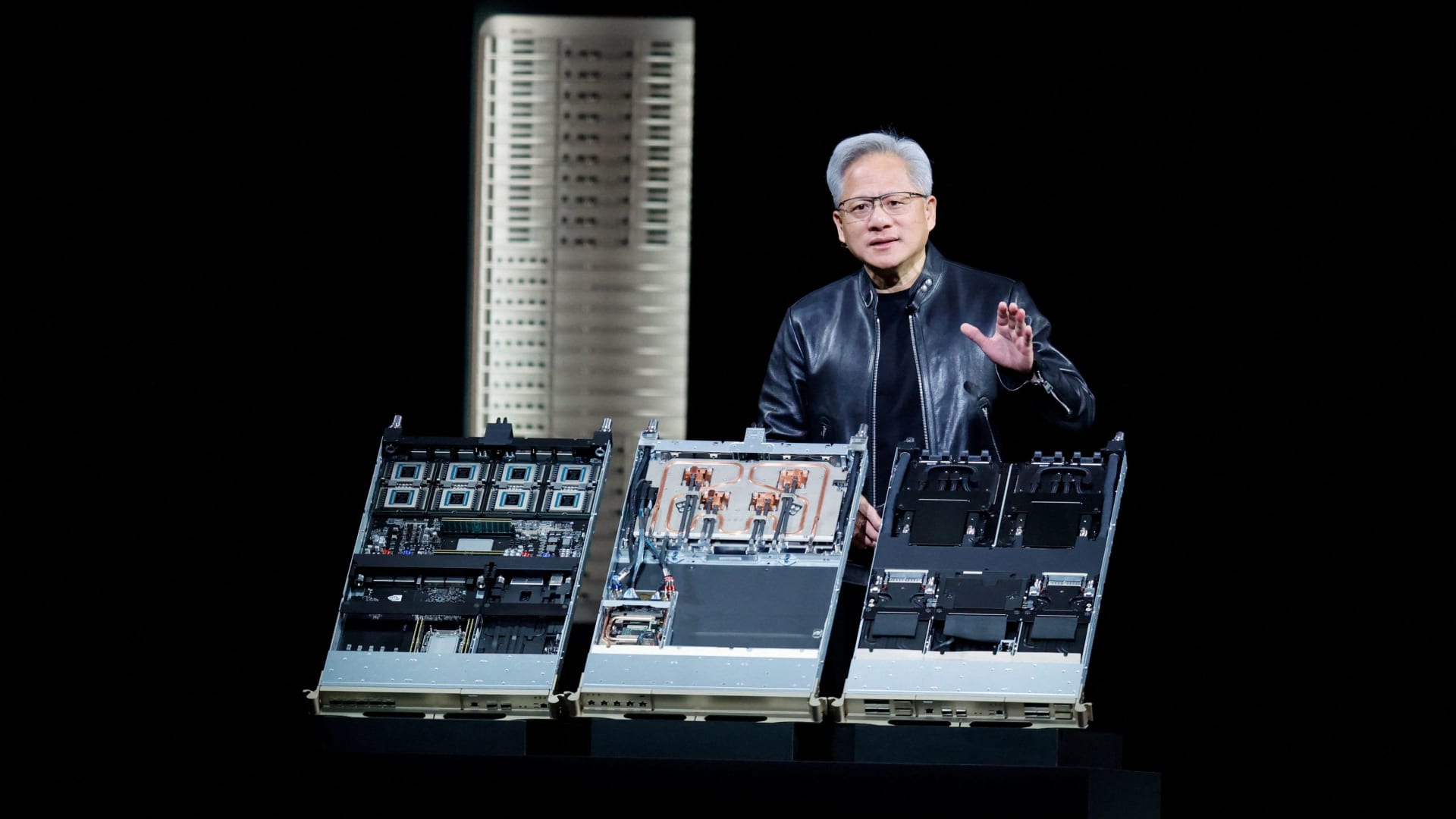

NVIDIA Increases Investment in Photonics Technology

- Photonics Investment: Since March, NVIDIA has invested $2 billion in companies like Lumentum, Coherent, and Marvell to advance photonics technology, aiming to enhance AI infrastructure performance and efficiency, thereby maintaining a competitive edge in a rapidly evolving market.

- Silicon Photonics Expansion: CEO Jensen Huang announced at the GTC conference that NVIDIA is scaling its silicon photonics capacity, indicating that significantly higher technological capabilities will be required to meet market demands, which will greatly enhance the computational power and response speed of its products.

- Manufacturing Challenges: Analysts from 650 Group highlight that the rapid growth of photonics technology will face challenges in supply chain and manufacturing capabilities, especially with surging demand, potentially requiring one to two product generations to adapt to the new technology.

- AI System Adaptation: Analyst Gil Luria noted that existing AI systems will need significant redesign to incorporate optical components, a process that may extend product update cycles, but successful implementation will significantly improve the performance and efficiency of AI models.

Amazon's AI-Driven Growth Potential is Significant

- AI Chip Partnership: Amazon's collaboration with Meta Platforms, which will utilize Amazon's Graviton5 processors, not only opens new sales opportunities for Amazon's custom chip business but also strengthens its internal tech stack's competitiveness.

- Cloud Infrastructure Growth: Amazon Web Services (AWS) reported a 28% year-over-year revenue increase to $37.59 billion in Q1, surpassing Wall Street estimates, indicating that AI demand is driving higher utilization rates and promising future growth.

- E-commerce and Digital Advertising Integration: As the world's largest online retailer, Amazon's advertising revenue grew 24% year-over-year to $17.24 billion in Q1, with AI integration expected to enhance profitability and market share in both e-commerce and advertising sectors.

- Profit Driver: Although AWS accounted for only 20.7% of total sales in Q1, it generated the majority of profits, and with the cloud business accelerating, Amazon's earnings outlook is increasingly positive, boosting investor confidence.

Market Dynamics and Corporate Performance Analysis

- Dell's Quarter Performance: Dell reported a quarter that exceeded expectations, with shares rising over 30%, indicating strong performance across all business levels, particularly in data center servers, which is expected to boost overall market confidence.

- Costco Membership Renewal Rates Up: Costco's latest earnings report showed improved membership renewal rates in the U.S. and Canada; although market reaction was muted, record performance in its gas business is likely to enhance membership loyalty and solidify its market position.

- Anthropic Surpasses OpenAI: Anthropic raised $65 billion at a $965 billion valuation, becoming the most valuable AI startup, a significant increase from $380 billion in February, showcasing explosive revenue growth and wealth creation potential in the AI sector.

- Cybersecurity Market Volatility: Okta beat expectations in its earnings report, with shares rising over 8%, while Zscaler's stock fell due to disappointing guidance, highlighting a divergence in the cybersecurity industry that affected the performance of other companies, including CrowdStrike.

Major Wall Street Rating Changes Overview

- Dell Upgrade: Susquehanna upgraded Dell from neutral to positive, citing increased confidence in a sustainable 8-10% operating margin and a 6% free cash flow margin, which supports a potential rerating of its EV/sales multiple to 3x, indicating strong market potential.

- Viper Energy Initiation: RBC initiated coverage of Viper Energy with an Outperform rating and a $58 price target, highlighting its advantages in scale and core Permian focus, positioning it as a best-in-class mineral and royalty company.

- SentinelOne Buy Rating: Bank of America upgraded SentinelOne from neutral to buy, viewing its solid quarterly performance as a strong entry point after an 18% decline in after-hours trading, reflecting confidence in its future growth prospects.

- XPeng Upgrade: Macquarie upgraded XPeng from neutral to outperform, noting its volume growth in the Chinese EV market, while future investments in humanoids and robotaxis provide additional upside potential for its stock.

SpaceX IPO Outlook and AI Investment Risks

- IPO Anticipation: SpaceX's planned IPO on June 12 is one of the most awaited public debuts in years, drawing significant investor interest in its future growth potential.

- AI Investment Scale: The company allocated $12.7 billion to artificial intelligence, significantly exceeding the $3.8 billion spent on its space segment, indicating a strategic pivot towards AI despite the associated high risks.

- Operating Loss Comparison: SpaceX's operating loss in AI reached $6.3 billion, far surpassing the $657 million loss from its space operations, raising concerns about the financial implications of such an imbalance for potential investors.

- Market Outlook and Risks: While SpaceX estimates a total addressable market of $26.5 trillion for AI, the uncertainty surrounding its massive expenditures and the ability to capture a significant market share necessitates careful risk assessment by investors considering the IPO.

SpaceX's AI Investments and IPO Outlook Analysis

- AI Investment Scale: SpaceX's investment in artificial intelligence reached $12.7 billion in 2025, significantly exceeding its $3.8 billion in space program spending, indicating the company's strong focus and expectations for future AI potential.

- Operating Loss Comparison: The operating loss in AI soared to $6.3 billion, far surpassing the $657 million loss from its space segment, highlighting the financial pressure and risks associated with its AI expenditures.

- Data Center Construction: The company is building Colossus and Colossus II data centers to support the training of next-generation AI models, and despite challenges related to energy consumption and public backlash, SpaceX plans to relocate data centers to space to address these issues.

- Market Outlook Assessment: SpaceX estimates its total addressable market for AI to be $26.5 trillion, and while facing high expenditures and uncertainties, investors must weigh the risks against potential rewards.

NVIDIA Increases Investment in Photonics Technology

- Photonics Investment: Since March, NVIDIA has invested $2 billion in companies like Lumentum, Coherent, and Marvell to advance photonics technology, aiming to enhance AI infrastructure performance and efficiency, thereby maintaining a competitive edge in a rapidly evolving market.

- Silicon Photonics Expansion: CEO Jensen Huang announced at the GTC conference that NVIDIA is scaling its silicon photonics capacity, indicating that significantly higher technological capabilities will be required to meet market demands, which will greatly enhance the computational power and response speed of its products.

- Manufacturing Challenges: Analysts from 650 Group highlight that the rapid growth of photonics technology will face challenges in supply chain and manufacturing capabilities, especially with surging demand, potentially requiring one to two product generations to adapt to the new technology.

- AI System Adaptation: Analyst Gil Luria noted that existing AI systems will need significant redesign to incorporate optical components, a process that may extend product update cycles, but successful implementation will significantly improve the performance and efficiency of AI models.