Kinsale Capital Q1 Performance Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 25 2026

0mins

Source: Yahoo Finance

- Revenue Growth Miss: Kinsale Capital reported Q1 revenue of $466.7 million, reflecting a 10.2% year-over-year increase, yet falling short of Wall Street's expectation of $471.6 million, indicating that despite growth, the company faces significant market pressures.

- Earnings Beat Expectations: The company’s adjusted EPS of $5.11 exceeded analyst estimates of $4.68, demonstrating Kinsale's ability to maintain profitability amidst challenging market conditions, which highlights the effectiveness of its strategy focused on smaller accounts.

- Intensified Market Competition: Management noted that increased competition and pricing pressures, particularly in the large commercial property insurance sector, have significantly impacted growth, with the CEO emphasizing the challenges faced in larger accounts, prompting a strategic shift towards more attractive smaller accounts.

- Technology-Driven Efficiency Gains: Kinsale continues to invest in technology and AI to enhance underwriting and claims processes, with expectations that these integrations will further bolster the company's cost advantages and profitability, even as competitive pressures persist.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy KNSL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on KNSL

Wall Street analysts forecast KNSL stock price to rise

11 Analyst Rating

3 Buy

8 Hold

0 Sell

Moderate Buy

Current: 308.850

Low

415.00

Averages

465.89

High

510.00

Current: 308.850

Low

415.00

Averages

465.89

High

510.00

About KNSL

Kinsale Capital Group, Inc. is a specialty insurance company that focuses on the excess and surplus lines (E&S) market in the United States. It writes E&S insurance on a non-admitted basis through its insurance subsidiary, Kinsale Insurance Company, which is authorized to write business in 50 states, the District of Columbia, the Commonwealth of Puerto Rico, and the United States Virgin Islands. It also markets certain products through its subsidiary, Aspera Insurance Services, Inc., an insurance broker. Its core client focus is small- to medium-sized accounts. Its commercial lines offerings include commercial property, excess casualty, general casualty, small business casualty, construction, allied health, entertainment, products liability, small business property, products liability, energy, environmental, management liability, inland marine, aviation, and all other commercial lines. Its personal lines offerings include high value homeowners and personal insurance.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Kinsale Capital Market Trends Analysis

- Market Trend Insights: In the latest Motley Fool Scoreboard episode, analysts delve into Kinsale Capital's market dynamics, offering unique insights into future investment opportunities that help investors gauge market pulse.

- Investment Opportunity Assessment: The episode highlights Kinsale Capital's potential in the insurance sector, particularly its innovative strategies for addressing climate change and natural disaster risks, which could lead to substantial growth for the company.

- Stock Price Reference: The stock price mentioned in the episode is from April 29, 2026, reflecting market expectations for Kinsale Capital's future performance, prompting investors to monitor stock price fluctuations in relation to market trends.

- Video Release Information: This video was published on June 11, 2026, aiming to provide timely market analysis and investment advice to enhance investor decision-making capabilities.

See More

Kinsale Capital Investment Insights from Motley Fool

- Market Trend Analysis: In the latest Motley Fool video, analysts discuss market trends surrounding Kinsale Capital, noting that while the company did not make the list of the top 10 recommended stocks, it still provides valuable investment insights for understanding market dynamics.

- Return Comparison: The average return of Stock Advisor stands at 926%, significantly outperforming the S&P 500's 203%, indicating that even though Kinsale Capital is not recommended, investors should still monitor its potential market performance for informed decision-making.

- AI and Future Investments: The video highlights the potential for AI to create the world's first trillionaire, suggesting that investors should focus on unique opportunities in the tech sector, particularly those related to giants like Nvidia and Intel, to capture future growth potential.

- Investor Community Building: Motley Fool encourages investors to join its community to share and gain investment advice; although Kinsale Capital is not on the recommended list, participants can still access information on other high-potential stocks through the community.

See More

KINSALE CAPITAL GROUP INC: TRUIST SECURITIES LOWERS TARGET PRICE FROM $450 TO $405

Company Announcement: Kinsale Capital Group Inc. has announced a reduction in the target price for Truist Securities.

New Target Price: The target price has been cut from $450 to $405.

See More

Kinsale Capital Q1 Performance Analysis

- Revenue Growth Miss: Kinsale Capital reported Q1 revenue of $466.7 million, reflecting a 10.2% year-over-year increase, yet falling short of Wall Street's expectation of $471.6 million, indicating that despite growth, the company faces significant market pressures.

- Earnings Beat Expectations: The company’s adjusted EPS of $5.11 exceeded analyst estimates of $4.68, demonstrating Kinsale's ability to maintain profitability amidst challenging market conditions, which highlights the effectiveness of its strategy focused on smaller accounts.

- Intensified Market Competition: Management noted that increased competition and pricing pressures, particularly in the large commercial property insurance sector, have significantly impacted growth, with the CEO emphasizing the challenges faced in larger accounts, prompting a strategic shift towards more attractive smaller accounts.

- Technology-Driven Efficiency Gains: Kinsale continues to invest in technology and AI to enhance underwriting and claims processes, with expectations that these integrations will further bolster the company's cost advantages and profitability, even as competitive pressures persist.

See More

Kinsale Capital Group Q1 2026 Earnings Call Insights

- Profitability Improvement: Kinsale Capital Group reported diluted operating earnings per share of $5.11 in Q1 2026, a 37.7% increase from $3.71 in Q1 2025, indicating strong profitability amidst a competitive market environment.

- Premium Growth Dynamics: While gross written premiums decreased by 0.5%, net written premiums grew by 5.6%, reflecting successful adaptation to smaller transactions, particularly as the large commercial property sector faces intense competition.

- Expense Ratio Changes: The expense ratio for Q1 was 21.1%, up from 20% last year, primarily due to an increase in the net commission ratio resulting from higher reinsurance retentions, which may impact future profitability and cost management strategies.

- Intensified Market Competition: Management highlighted increased competition in the commercial property sector leading to price declines, although favorable underwriting conditions in small business property and multiple casualty divisions remain, necessitating vigilance on overall market sustainability.

See More

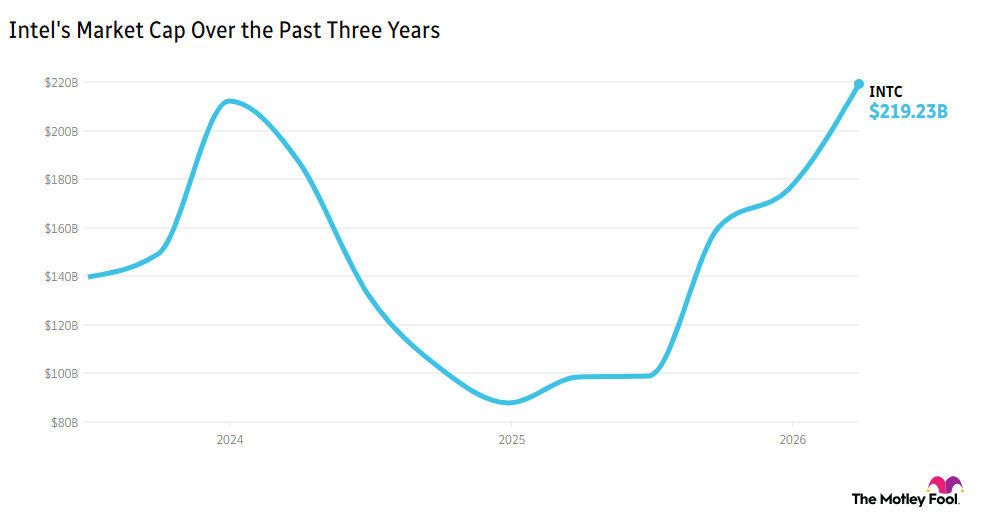

Intel CEO Tan Highlights Promising AI Future

- AI Business Growth: Intel (INTC) shares surged over 25% ahead of market open as CEO Lip-Bu Tan highlighted the company's pivot to AI, with financial outlook upgraded, projecting next quarter's revenue to rise from $13 billion to between $13.8 billion and $14.8 billion, indicating strong market demand and successful strategic transformation.

- Capacity Enhancement Plans: CFO David Zinsner stated that in response to soaring demand for data center processors, Intel is focused on rapidly increasing capacity to meet customer needs and avoid supply shortages, thereby enhancing its competitive position in the market.

- Strengthening Industry Position: Tan emphasized that as AI systems become more complex, Intel's CPUs remain the backbone of AI computing architecture, a trend that will further drive the company's market share and revenue growth in the future, showcasing its leadership in technological innovation.

- Positive Market Reaction: The market reacted enthusiastically to Intel's positive outlook and strong performance, reflecting investor confidence in the company's future development and further solidifying Intel's position in the tech industry.

See More

Kinsale Capital Market Trends Analysis

- Market Trend Insights: In the latest Motley Fool Scoreboard episode, analysts delve into Kinsale Capital's market dynamics, offering unique insights into future investment opportunities that help investors gauge market pulse.

- Investment Opportunity Assessment: The episode highlights Kinsale Capital's potential in the insurance sector, particularly its innovative strategies for addressing climate change and natural disaster risks, which could lead to substantial growth for the company.

- Stock Price Reference: The stock price mentioned in the episode is from April 29, 2026, reflecting market expectations for Kinsale Capital's future performance, prompting investors to monitor stock price fluctuations in relation to market trends.

- Video Release Information: This video was published on June 11, 2026, aiming to provide timely market analysis and investment advice to enhance investor decision-making capabilities.

See More

Kinsale Capital Investment Insights from Motley Fool

- Market Trend Analysis: In the latest Motley Fool video, analysts discuss market trends surrounding Kinsale Capital, noting that while the company did not make the list of the top 10 recommended stocks, it still provides valuable investment insights for understanding market dynamics.

- Return Comparison: The average return of Stock Advisor stands at 926%, significantly outperforming the S&P 500's 203%, indicating that even though Kinsale Capital is not recommended, investors should still monitor its potential market performance for informed decision-making.

- AI and Future Investments: The video highlights the potential for AI to create the world's first trillionaire, suggesting that investors should focus on unique opportunities in the tech sector, particularly those related to giants like Nvidia and Intel, to capture future growth potential.

- Investor Community Building: Motley Fool encourages investors to join its community to share and gain investment advice; although Kinsale Capital is not on the recommended list, participants can still access information on other high-potential stocks through the community.

See More

KINSALE CAPITAL GROUP INC: TRUIST SECURITIES LOWERS TARGET PRICE FROM $450 TO $405

Company Announcement: Kinsale Capital Group Inc. has announced a reduction in the target price for Truist Securities.

New Target Price: The target price has been cut from $450 to $405.

See More

Kinsale Capital Q1 Performance Analysis

- Revenue Growth Miss: Kinsale Capital reported Q1 revenue of $466.7 million, reflecting a 10.2% year-over-year increase, yet falling short of Wall Street's expectation of $471.6 million, indicating that despite growth, the company faces significant market pressures.

- Earnings Beat Expectations: The company’s adjusted EPS of $5.11 exceeded analyst estimates of $4.68, demonstrating Kinsale's ability to maintain profitability amidst challenging market conditions, which highlights the effectiveness of its strategy focused on smaller accounts.

- Intensified Market Competition: Management noted that increased competition and pricing pressures, particularly in the large commercial property insurance sector, have significantly impacted growth, with the CEO emphasizing the challenges faced in larger accounts, prompting a strategic shift towards more attractive smaller accounts.

- Technology-Driven Efficiency Gains: Kinsale continues to invest in technology and AI to enhance underwriting and claims processes, with expectations that these integrations will further bolster the company's cost advantages and profitability, even as competitive pressures persist.

See More

Kinsale Capital Group Q1 2026 Earnings Call Insights

- Profitability Improvement: Kinsale Capital Group reported diluted operating earnings per share of $5.11 in Q1 2026, a 37.7% increase from $3.71 in Q1 2025, indicating strong profitability amidst a competitive market environment.

- Premium Growth Dynamics: While gross written premiums decreased by 0.5%, net written premiums grew by 5.6%, reflecting successful adaptation to smaller transactions, particularly as the large commercial property sector faces intense competition.

- Expense Ratio Changes: The expense ratio for Q1 was 21.1%, up from 20% last year, primarily due to an increase in the net commission ratio resulting from higher reinsurance retentions, which may impact future profitability and cost management strategies.

- Intensified Market Competition: Management highlighted increased competition in the commercial property sector leading to price declines, although favorable underwriting conditions in small business property and multiple casualty divisions remain, necessitating vigilance on overall market sustainability.

See More

Intel CEO Tan Highlights Promising AI Future

- AI Business Growth: Intel (INTC) shares surged over 25% ahead of market open as CEO Lip-Bu Tan highlighted the company's pivot to AI, with financial outlook upgraded, projecting next quarter's revenue to rise from $13 billion to between $13.8 billion and $14.8 billion, indicating strong market demand and successful strategic transformation.

- Capacity Enhancement Plans: CFO David Zinsner stated that in response to soaring demand for data center processors, Intel is focused on rapidly increasing capacity to meet customer needs and avoid supply shortages, thereby enhancing its competitive position in the market.

- Strengthening Industry Position: Tan emphasized that as AI systems become more complex, Intel's CPUs remain the backbone of AI computing architecture, a trend that will further drive the company's market share and revenue growth in the future, showcasing its leadership in technological innovation.

- Positive Market Reaction: The market reacted enthusiastically to Intel's positive outlook and strong performance, reflecting investor confidence in the company's future development and further solidifying Intel's position in the tech industry.

See More