Investor Critiques Tesla's Stock Performance Amid Autonomous Driving Race

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 27 2026

0mins

Should l Buy TSLA?

Source: Benzinga

- Poor Stock Performance: Investor Gary Black criticized Tesla's stock for showing almost no growth over the past five years, with TSLA rising 81% compared to the Nasdaq 100's 94%, indicating a lack of market confidence despite significant advancements in its autonomous driving technology.

- Earnings Forecast Downgrade: Black noted that Tesla's earnings estimates for 2026-2028 have been sharply reduced, and the newly launched Cybertruck AWD trim is cannibalizing sales from mid-level trims, potentially impacting overall revenue performance.

- Investor Skepticism: Black questioned the optimism of Tesla's supporters who ignore financial data, asserting that stock prices should be driven by earnings and cash flows, and likening this attitude to asking Elon Musk to ignore the laws of physics.

- Cybercab Production Update: Tesla's Cybercab is set to ramp up production in April this year, with Musk stating it will be priced below $30,000, and a production-ready version has been unveiled at the Texas Gigafactory, showcasing Tesla's ongoing innovation in the electric mobility sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy TSLA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

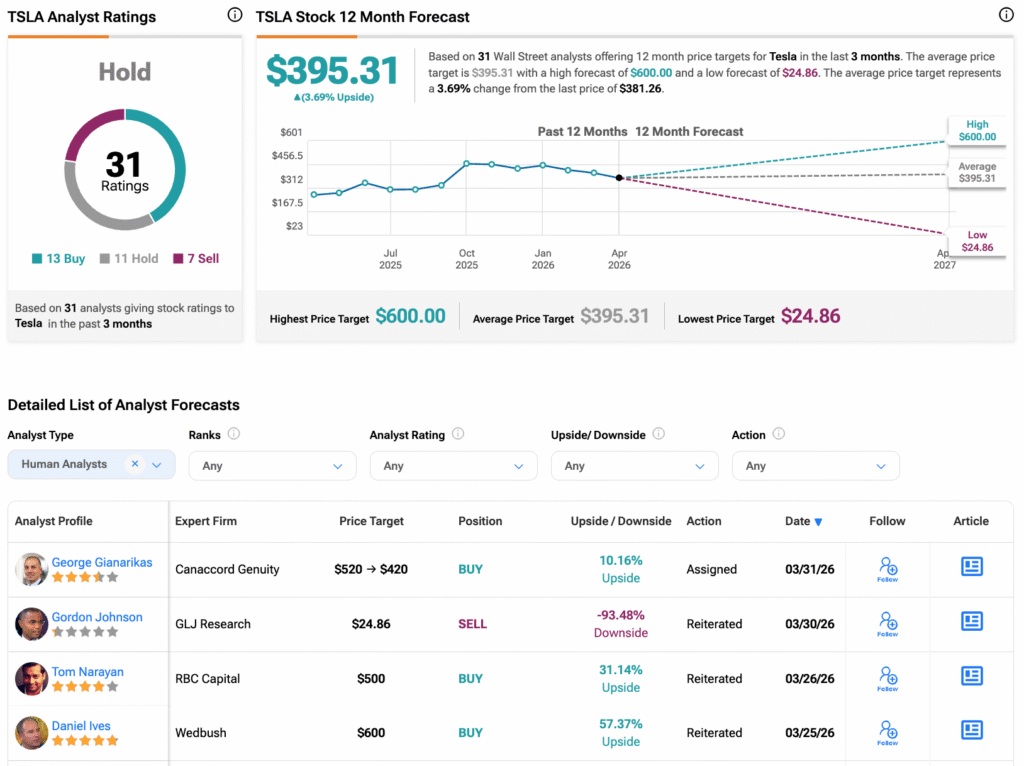

Analyst Views on TSLA

Wall Street analysts forecast TSLA stock price to rise

30 Analyst Rating

12 Buy

11 Hold

7 Sell

Hold

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

Current: 381.260

Low

25.28

Averages

401.93

High

600.00

About TSLA

Tesla, Inc. designs, develops, manufactures, sells and leases high-performance fully electric vehicles and energy generation and storage systems, and offers services related to its products. Its segments include automotive, and energy generation and storage. The automotive segment includes the design, development, manufacturing, sales and leasing of high-performance fully electric vehicles, and sales of automotive regulatory credits. It also includes sales of used vehicles, non-warranty maintenance services and collisions, part sales, paid supercharging, insurance services revenue and retail merchandise sales. The energy generation and storage segment include the design, manufacture, installation, sales and leasing of solar energy generation and energy storage products and related services and sales of solar energy systems incentives. Its consumer vehicles include the Model 3, Y, S, X and Cybertruck. Its lithium-ion battery energy storage products include Powerwall and Megapack.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Emerging Tech Stars in the Market

- TSMC's AI Potential: Taiwan Semiconductor Manufacturing (TSM), a global leader in chip manufacturing, holds a market cap of $1.8 trillion and is poised to benefit from broad market demand in AI chip production, particularly in smartphones and personal computers over the coming years.

- Broadcom's Custom Chip Advantage: Broadcom (AVGO) forecasts over $100 billion in AI chip revenue by 2027, successfully carving out a niche in the AI market with its custom chips designed for specific tasks, reflecting strong customer demand and market potential.

- Nebius Group's Rapid Growth: Nebius Group (NBIS) focuses on AI workloads, achieving annual recurring revenue of $1.25 billion in the recent year, with expectations to rise to $7 billion to $9 billion this year, showcasing its strong growth potential in the cloud computing sector.

- Market Environment Challenges: Despite concerns about the economy and geopolitical factors affecting the Magnificent Seven tech stocks, emerging companies like TSMC, Broadcom, and Nebius Group demonstrate robust growth potential, positioning themselves as future market leaders.

See More

Future Outlook for the Magnificent Seven Tech Stocks

- Tech Stock Performance Review: The remarkable growth of the S&P 500 over the past few years is partly attributed to the 'Magnificent Seven' tech stocks—Apple, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla—which have become household names due to their impressive growth.

- AI Market Concerns: Despite their strong past performance, these tech giants have recently faced stagnation or declines in stock prices amid concerns about the artificial intelligence (AI) revenue opportunities and uncertainties in the economic and geopolitical landscape, reflecting market caution regarding future growth.

- Potential Replacement Stocks: In light of the challenges facing the 'Magnificent Seven', Taiwan Semiconductor Manufacturing, Broadcom, and Nebius Group are seen as potential replacements, with TSMC playing a crucial role in AI chip manufacturing and Nebius focusing on AI workloads, indicating strong growth potential.

- Nebius Group Growth Expectations: Nebius Group's annual recurring revenue reached $1.25 billion in the recent year, with expectations to grow to between $7 billion and $9 billion in the coming year, highlighting its strong demand and growth prospects in the AI market.

See More

SpaceX Files for IPO with $2 Trillion Valuation Target

- IPO Filing: SpaceX confidentially filed for an IPO on April 1, aiming for a historic valuation of $2 trillion, which would surpass both Tesla and Meta, reflecting strong market confidence in its future growth potential.

- Merger and Valuation: The merger with Elon Musk's AI startup xAI, valued at $250 billion, boosts SpaceX's overall valuation to $1.25 trillion, further solidifying its position in the tech sector.

- Revenue and Profitability: For 2025, SpaceX reported revenues between $15 billion and $16 billion, with an EBITDA of around $8 billion; while its profitability remains unclear, the majority of its revenue is derived from Starlink, with NASA contributing only 5%.

- Market Competition and Risks: Despite SpaceX's dominance in the rocket launch market, the justification for its valuation is questioned, especially when compared to rapidly growing companies like Palantir, leading investors to approach its high price-to-sales ratio of 130 with caution.

See More

SpaceX Confidentially Files for IPO Targeting $2 Trillion Valuation

- IPO Potential: SpaceX confidentially filed for an IPO on Wednesday, aiming for a historic valuation of $2 trillion, which, if successful, would surpass Saudi Aramco's $75 billion fundraising record, reflecting high market expectations for its future growth.

- Financial Overview: As of 2025, SpaceX's revenue is projected between $15 billion and $16 billion, with an EBITDA of around $8 billion; while GAAP profitability remains unconfirmed, its revenue heavily relies on Starlink, with NASA contributing only 5%, indicating a lack of diversification in its revenue streams.

- Merger Supports IPO: In 2026, SpaceX acquired Elon Musk's AI startup xAI for a valuation of $1.25 trillion, a move that not only provides funding support for xAI but also paves the way for SpaceX's IPO, showcasing Musk's strategic vision in technology integration.

- Market Competition Risks: Despite SpaceX's dominance in the rocket launch market, its valuation appears less robust compared to the

See More

SpaceX Confidentially Files for IPO Targeting $2 Trillion Valuation

- IPO Filing: SpaceX confidentially filed for its IPO on Wednesday, aiming for a staggering $2 trillion valuation, which, if successful, would make it the largest IPO in history, surpassing Saudi Aramco's fundraising record.

- Financial Performance: According to Reuters, SpaceX is projected to generate between $15 billion and $16 billion in revenue for 2025, with an EBITDA of around $8 billion, although it remains unclear if the company is profitable on a GAAP basis, with most revenue stemming from Starlink.

- Market Competition: While SpaceX dominates the rocket launch market, its valuation appears weak compared to the

See More

SpaceX Files for IPO Targeting Over $1.75 Trillion Valuation

- IPO Overview: Billionaire Elon Musk's SpaceX has filed for an IPO with the U.S. SEC, targeting a valuation exceeding $1.75 trillion and aiming to raise up to $75 billion, potentially making it one of the largest public offerings in history if successful by June 2026.

- Tesla's Indirect Investment: Tesla has received government approval to convert its investment in Musk's xAI into a small stake in SpaceX, meaning Tesla shareholders will benefit indirectly from SpaceX's growth, with its value set to be publicly reflected in Tesla's assets post-IPO.

- Retail Investor Opportunities: SpaceX plans to allocate up to 30% of shares to retail investors, tripling the typical IPO norm, allowing Tesla's loyal retail investor base direct access from day one, enhancing their investment opportunities.

- Potential Merger Outlook: Wedbush analyst Dan Ives predicts a possible merger between Tesla and SpaceX as early as 2027, referring to this combination as the “holy grail” that could connect both disruptive tech companies within a single AI-driven ecosystem, showcasing significant strategic potential.

See More

Emerging Tech Stars in the Market

- TSMC's AI Potential: Taiwan Semiconductor Manufacturing (TSM), a global leader in chip manufacturing, holds a market cap of $1.8 trillion and is poised to benefit from broad market demand in AI chip production, particularly in smartphones and personal computers over the coming years.

- Broadcom's Custom Chip Advantage: Broadcom (AVGO) forecasts over $100 billion in AI chip revenue by 2027, successfully carving out a niche in the AI market with its custom chips designed for specific tasks, reflecting strong customer demand and market potential.

- Nebius Group's Rapid Growth: Nebius Group (NBIS) focuses on AI workloads, achieving annual recurring revenue of $1.25 billion in the recent year, with expectations to rise to $7 billion to $9 billion this year, showcasing its strong growth potential in the cloud computing sector.

- Market Environment Challenges: Despite concerns about the economy and geopolitical factors affecting the Magnificent Seven tech stocks, emerging companies like TSMC, Broadcom, and Nebius Group demonstrate robust growth potential, positioning themselves as future market leaders.

See More

Future Outlook for the Magnificent Seven Tech Stocks

- Tech Stock Performance Review: The remarkable growth of the S&P 500 over the past few years is partly attributed to the 'Magnificent Seven' tech stocks—Apple, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla—which have become household names due to their impressive growth.

- AI Market Concerns: Despite their strong past performance, these tech giants have recently faced stagnation or declines in stock prices amid concerns about the artificial intelligence (AI) revenue opportunities and uncertainties in the economic and geopolitical landscape, reflecting market caution regarding future growth.

- Potential Replacement Stocks: In light of the challenges facing the 'Magnificent Seven', Taiwan Semiconductor Manufacturing, Broadcom, and Nebius Group are seen as potential replacements, with TSMC playing a crucial role in AI chip manufacturing and Nebius focusing on AI workloads, indicating strong growth potential.

- Nebius Group Growth Expectations: Nebius Group's annual recurring revenue reached $1.25 billion in the recent year, with expectations to grow to between $7 billion and $9 billion in the coming year, highlighting its strong demand and growth prospects in the AI market.

See More

SpaceX Files for IPO with $2 Trillion Valuation Target

- IPO Filing: SpaceX confidentially filed for an IPO on April 1, aiming for a historic valuation of $2 trillion, which would surpass both Tesla and Meta, reflecting strong market confidence in its future growth potential.

- Merger and Valuation: The merger with Elon Musk's AI startup xAI, valued at $250 billion, boosts SpaceX's overall valuation to $1.25 trillion, further solidifying its position in the tech sector.

- Revenue and Profitability: For 2025, SpaceX reported revenues between $15 billion and $16 billion, with an EBITDA of around $8 billion; while its profitability remains unclear, the majority of its revenue is derived from Starlink, with NASA contributing only 5%.

- Market Competition and Risks: Despite SpaceX's dominance in the rocket launch market, the justification for its valuation is questioned, especially when compared to rapidly growing companies like Palantir, leading investors to approach its high price-to-sales ratio of 130 with caution.

See More

SpaceX Confidentially Files for IPO Targeting $2 Trillion Valuation

- IPO Potential: SpaceX confidentially filed for an IPO on Wednesday, aiming for a historic valuation of $2 trillion, which, if successful, would surpass Saudi Aramco's $75 billion fundraising record, reflecting high market expectations for its future growth.

- Financial Overview: As of 2025, SpaceX's revenue is projected between $15 billion and $16 billion, with an EBITDA of around $8 billion; while GAAP profitability remains unconfirmed, its revenue heavily relies on Starlink, with NASA contributing only 5%, indicating a lack of diversification in its revenue streams.

- Merger Supports IPO: In 2026, SpaceX acquired Elon Musk's AI startup xAI for a valuation of $1.25 trillion, a move that not only provides funding support for xAI but also paves the way for SpaceX's IPO, showcasing Musk's strategic vision in technology integration.

- Market Competition Risks: Despite SpaceX's dominance in the rocket launch market, its valuation appears less robust compared to the

See More

SpaceX Confidentially Files for IPO Targeting $2 Trillion Valuation

- IPO Filing: SpaceX confidentially filed for its IPO on Wednesday, aiming for a staggering $2 trillion valuation, which, if successful, would make it the largest IPO in history, surpassing Saudi Aramco's fundraising record.

- Financial Performance: According to Reuters, SpaceX is projected to generate between $15 billion and $16 billion in revenue for 2025, with an EBITDA of around $8 billion, although it remains unclear if the company is profitable on a GAAP basis, with most revenue stemming from Starlink.

- Market Competition: While SpaceX dominates the rocket launch market, its valuation appears weak compared to the

See More