Intel Stock Rises 3.3%, Speculation on Nvidia Partnership Fuels Market Interest

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 28 2026

0mins

Should l Buy INTC?

Source: stocktwits

- Stock Recovery: Intel's stock rose 3.3% on Tuesday, breaking a two-day losing streak and providing investors with some relief, indicating growing market interest in the company's future prospects.

- Optimistic Market Sentiment: Stocktwits sentiment has remained 'extremely bullish' over the past few days, despite disappointing fourth-quarter earnings, as retail investors increasingly view Intel's long-term outlook positively.

- Speculation on Partnership: Rumors suggest that Nvidia may utilize Intel's manufacturing capabilities for its next-gen AI and GPU platform, although neither company has confirmed this news, leading to positive market reactions.

- Increased Investor Attention: Intel's message volume on Stocktwits has remained 'extremely high' over the past two days, reflecting strong investor interest in the company's future developments and potential partnerships, despite ongoing challenges in its foundry business.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy INTC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on INTC

Wall Street analysts forecast INTC stock price to fall

29 Analyst Rating

5 Buy

19 Hold

5 Sell

Hold

Current: 48.030

Low

20.00

Averages

39.30

High

52.00

Current: 48.030

Low

20.00

Averages

39.30

High

52.00

About INTC

Intel Corporation is a global designer and manufacturer of semiconductor products. The Company operates through three segments: Intel Products, Intel Foundry, and All Other. Its Intel Products segment includes Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX). The CCG is bringing together the operating system, system architecture, hardware, and software application integration to enable PC experiences. DCAI delivers workload-optimized solutions to cloud service providers and enterprises, along with silicon devices for communications service providers, network and edge, and HPC customers. NEX helps networks and edge compute systems from fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Intel Foundry segment comprises technology development, manufacturing and foundry services. All Other segments include Altera, Mobileye, Other.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Intel to Report Q1 Financial Results on April 23, 2026

- Earnings Report Schedule: Intel has announced that it will release its Q1 financial results on April 23, 2026, after market close, reflecting the company's commitment to transparency and timely information for investors.

- Conference Call Timing: Following the earnings release, Intel will hold a conference call at 2 p.m. PT that day to discuss the results, enhancing investor interaction and potentially boosting market confidence.

- Webcast Availability: Investors can access a live webcast of the earnings conference call on Intel's Investor Relations website, ensuring broad dissemination of information and further enhancing company transparency and investor engagement.

- Company Background: Intel focuses on designing and manufacturing advanced semiconductors that drive modern computing, emphasizing its ongoing efforts in technological innovation and market leadership.

See More

Intel to Repurchase 49% Stake in Ireland Facility for $14.2 Billion

- Share Buyback Agreement: Intel has reached a deal to repurchase Apollo's 49% equity interest in the Fab 34 joint venture for $14.2 billion, which will provide the company with stronger capital support during its manufacturing expansion and is expected to enhance future profitability.

- Funding Strategy: Intel plans to finance the buyback with cash on hand and approximately $6.5 billion in new debt, a strategy that not only optimizes its capital structure but could also strengthen the company's credit rating in 2027 and beyond.

- Technological Production Capacity: The Fab 34 facility produces chips using Intel 4 and Intel 3 process technologies, including processors for AI-enabled systems, indicating the company's ongoing investment and innovation in high-growth sectors.

- Improved Financial Position: CFO David Zinsner noted that the company's balance sheet and business strategy have significantly improved since the original partnership was formed, indicating Intel's gradual recovery of its leadership position in the competitive semiconductor market.

See More

Muddy Waters Accuses SoFi of Financial Shenanigans

- Short-Selling Allegations: Short-seller Muddy Waters recently accused SoFi Technologies of engaging in financial shenanigans by inflating fair value gains in its portfolios, a claim that could undermine investor trust and lead to further stock price declines.

- Stock Price Volatility: SoFi's stock has dropped nearly 51% from recent highs, partly due to concerns raised by Muddy Waters, reflecting investor apprehension about the company's financial health and potentially impacting its future fundraising capabilities.

- Market Performance: Despite SoFi averaging annual gains of 38% over the past three years, the current negative news may affect its market position among younger consumers, especially as it aims to transform into a one-stop financial services platform.

- Management Confidence: In spite of the allegations, SoFi CEO Anthony Noto recently purchased shares, indicating confidence in the company's future; however, investors should exercise caution and wait for more information to assess the risks before making decisions.

See More

Investment Risk Alert: Etsy, Nike, Tesla

- Etsy Sales Decline: Etsy's gross merchandise sales fell by 5.3% year-over-year in 2025, and while there was a slight recovery in Q4 excluding Reverb sales, the overall decrease in active buyers and sellers alongside a drop in net income indicates a weakening market position.

- Nike's Weak Performance: In its Q3 fiscal 2026 report, Nike showed flat year-over-year revenue despite a 5% increase in wholesale revenue, as direct sales declined by 4%, highlighting ongoing market share losses, particularly with a 7% drop in sales in China.

- Tesla's Growth Obstacles: Despite exceeding a $1 trillion market cap, Tesla's revenue dipped by 3% year-over-year in 2025, with a 10% decline in automobile sales and a 46% drop in GAAP net income, indicating significant challenges in sustaining growth in the electric vehicle market.

- Investor Confidence Shaken: With the declining performance of Etsy, Nike, and Tesla, investor confidence in these once high-flying stocks is waning, prompting analysts to suggest considering divestment ahead of upcoming earnings reports to avoid potential larger losses.

See More

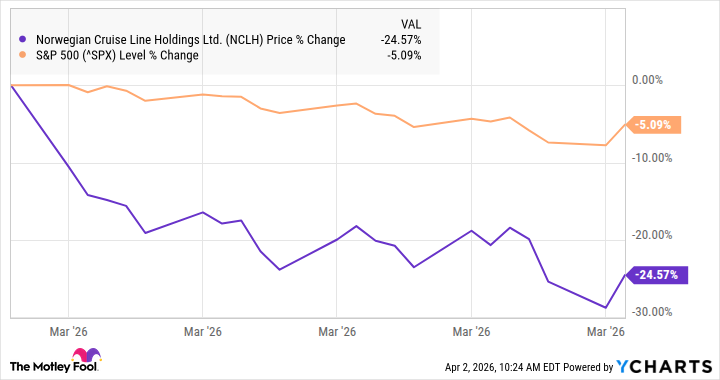

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

American Express Stock Pullback Reveals Growth Potential

- Strong Earnings Growth: American Express reported a 10% revenue increase for 2025, reaching $72.2 billion, with adjusted earnings per share at $15.38, reflecting resilience and profitability amid macroeconomic pressures.

- Increased Shareholder Returns: The board approved a 16% increase in the quarterly dividend to $0.95 per share in March, resulting in a 1.3% dividend yield, indicating strong cash flow that supports future dividend growth.

- Aggressive Buyback Program: In 2025, American Express returned $7.6 billion to shareholders, with approximately $5.3 billion allocated for share repurchases, reducing the share count by about 2%, which directly boosts per-share earnings.

- Strong Pricing Power: By raising the annual fee of its flagship Platinum Card by nearly 30% and enhancing lifestyle benefits, the company successfully attracts younger consumers, demonstrating its pricing power and potential for future growth.

See More

Intel to Report Q1 Financial Results on April 23, 2026

- Earnings Report Schedule: Intel has announced that it will release its Q1 financial results on April 23, 2026, after market close, reflecting the company's commitment to transparency and timely information for investors.

- Conference Call Timing: Following the earnings release, Intel will hold a conference call at 2 p.m. PT that day to discuss the results, enhancing investor interaction and potentially boosting market confidence.

- Webcast Availability: Investors can access a live webcast of the earnings conference call on Intel's Investor Relations website, ensuring broad dissemination of information and further enhancing company transparency and investor engagement.

- Company Background: Intel focuses on designing and manufacturing advanced semiconductors that drive modern computing, emphasizing its ongoing efforts in technological innovation and market leadership.

See More

Intel to Repurchase 49% Stake in Ireland Facility for $14.2 Billion

- Share Buyback Agreement: Intel has reached a deal to repurchase Apollo's 49% equity interest in the Fab 34 joint venture for $14.2 billion, which will provide the company with stronger capital support during its manufacturing expansion and is expected to enhance future profitability.

- Funding Strategy: Intel plans to finance the buyback with cash on hand and approximately $6.5 billion in new debt, a strategy that not only optimizes its capital structure but could also strengthen the company's credit rating in 2027 and beyond.

- Technological Production Capacity: The Fab 34 facility produces chips using Intel 4 and Intel 3 process technologies, including processors for AI-enabled systems, indicating the company's ongoing investment and innovation in high-growth sectors.

- Improved Financial Position: CFO David Zinsner noted that the company's balance sheet and business strategy have significantly improved since the original partnership was formed, indicating Intel's gradual recovery of its leadership position in the competitive semiconductor market.

See More

Muddy Waters Accuses SoFi of Financial Shenanigans

- Short-Selling Allegations: Short-seller Muddy Waters recently accused SoFi Technologies of engaging in financial shenanigans by inflating fair value gains in its portfolios, a claim that could undermine investor trust and lead to further stock price declines.

- Stock Price Volatility: SoFi's stock has dropped nearly 51% from recent highs, partly due to concerns raised by Muddy Waters, reflecting investor apprehension about the company's financial health and potentially impacting its future fundraising capabilities.

- Market Performance: Despite SoFi averaging annual gains of 38% over the past three years, the current negative news may affect its market position among younger consumers, especially as it aims to transform into a one-stop financial services platform.

- Management Confidence: In spite of the allegations, SoFi CEO Anthony Noto recently purchased shares, indicating confidence in the company's future; however, investors should exercise caution and wait for more information to assess the risks before making decisions.

See More

Investment Risk Alert: Etsy, Nike, Tesla

- Etsy Sales Decline: Etsy's gross merchandise sales fell by 5.3% year-over-year in 2025, and while there was a slight recovery in Q4 excluding Reverb sales, the overall decrease in active buyers and sellers alongside a drop in net income indicates a weakening market position.

- Nike's Weak Performance: In its Q3 fiscal 2026 report, Nike showed flat year-over-year revenue despite a 5% increase in wholesale revenue, as direct sales declined by 4%, highlighting ongoing market share losses, particularly with a 7% drop in sales in China.

- Tesla's Growth Obstacles: Despite exceeding a $1 trillion market cap, Tesla's revenue dipped by 3% year-over-year in 2025, with a 10% decline in automobile sales and a 46% drop in GAAP net income, indicating significant challenges in sustaining growth in the electric vehicle market.

- Investor Confidence Shaken: With the declining performance of Etsy, Nike, and Tesla, investor confidence in these once high-flying stocks is waning, prompting analysts to suggest considering divestment ahead of upcoming earnings reports to avoid potential larger losses.

See More

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

American Express Stock Pullback Reveals Growth Potential

- Strong Earnings Growth: American Express reported a 10% revenue increase for 2025, reaching $72.2 billion, with adjusted earnings per share at $15.38, reflecting resilience and profitability amid macroeconomic pressures.

- Increased Shareholder Returns: The board approved a 16% increase in the quarterly dividend to $0.95 per share in March, resulting in a 1.3% dividend yield, indicating strong cash flow that supports future dividend growth.

- Aggressive Buyback Program: In 2025, American Express returned $7.6 billion to shareholders, with approximately $5.3 billion allocated for share repurchases, reducing the share count by about 2%, which directly boosts per-share earnings.

- Strong Pricing Power: By raising the annual fee of its flagship Platinum Card by nearly 30% and enhancing lifestyle benefits, the company successfully attracts younger consumers, demonstrating its pricing power and potential for future growth.

See More