Ford Reshapes Battery Strategy, Acquires Kentucky Plants

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 5 days ago

0mins

Source: stocktwits

- Strategic Restructuring: Ford announced its exit from the BlueOval SK joint venture, reshaping its battery strategy while acquiring two Kentucky battery plants, which is expected to reduce future capital contributions by approximately $6.6 billion over the next five years, thereby optimizing capital efficiency.

- Loan Obligations: Ford will assume a $3.805 billion Department of Energy loan linked to one of the plants, with an annual interest rate of 4.814% and quarterly interest payments required until January 2030, demonstrating the company's long-term commitment to battery production.

- Job Creation: The new plants are projected to create 7,500 operational jobs and provided over 5,000 construction jobs during the building phase, further driving local economic development and enhancing Ford's market position in battery manufacturing.

- Market Sentiment: Although Ford's stock price has remained flat this year, retail investor sentiment on Stocktwits remains 'bullish', indicating confidence in Ford's future battery strategy despite a decrease in message volume.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy F?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on F

Wall Street analysts forecast F stock price to fall

14 Analyst Rating

3 Buy

10 Hold

1 Sell

Hold

Current: 14.930

Low

11.00

Averages

13.65

High

16.00

Current: 14.930

Low

11.00

Averages

13.65

High

16.00

About F

Ford Motor Company develops and delivers Ford trucks, sport utility vehicles, commercial vans and cars, and Lincoln luxury vehicles, along with connected services, including BlueCruise (ADAS) and security. The Company's segments include Ford Blue, Ford Model e, Ford Pro, and Ford Credit. The Ford Blue segment primarily includes the sale of Ford and Lincoln internal combustion engine (ICE) and hybrid vehicles, service parts, accessories, and digital services for retail customers. The Ford Model e segment primarily includes the sale of its electric vehicles, service parts, accessories, and digital services for retail customers. The Ford Pro segment primarily includes the sale of Ford and Lincoln vehicles, service parts, accessories, and services for commercial, government, and rental customers. The Ford Credit segment consists of the Ford Credit business on a consolidated basis, which is primarily vehicle-related financing and leasing activities. Its vehicle brands are Ford and Lincoln.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Hindalco Projects Novelis to Earn $500 per Tonne by Fiscal 2027

- Earnings Outlook: Hindalco anticipates its subsidiary Novelis will achieve earnings of approximately $500 per tonne by fiscal 2027, reflecting confidence in future profitability amid strong demand in its Indian aluminium and copper sectors.

- Financial Impact: The fire-related disruptions at Novelis' Oswego plant resulted in a one-time charge of ₹41.71 billion (approximately $437.59 million) for fiscal 2026, impacting Hindalco's earnings; however, management asserts that “the worst is over.”

- Market Dynamics: Hindalco's U.S. operations contribute about 60% of revenue, reporting adjusted EBITDA of $462 per tonne for fiscal 2026, despite rising input costs due to the Middle East conflict affecting overall profitability.

- Growth Prospects: The company expects high double-digit growth in its domestic aluminium downstream business this fiscal year, driven by the ramp-up of its new rolling facility, Aditya FRP, and expansion into higher-value products such as EV components and construction materials.

See More

Ford Stock Soars 24% in May, Attracting Investor Interest

- Valuation Appeal: Ford's price-to-earnings ratio stands at 11.3, representing a 37% discount compared to its 10-year average, making its stock particularly attractive in the current market environment and likely to draw interest from value-focused investors.

- Attractive Dividend Yield: With a dividend yield of 4.02%, Ford not only appeals to dividend-seeking investors but also enhances its stock's attractiveness, especially in a low-interest-rate environment where income generation is crucial.

- Growth Potential from New Segment: Ford plans to launch battery energy storage systems in 2027, leveraging its electric vehicle infrastructure, which is expected to introduce a new growth engine and enhance its competitive position in the market.

- Profitability Challenges: Despite achieving an 11.4% operating margin in Q1, Ford's overall operating margin has averaged only 1.6% over the past decade, indicating ongoing challenges in profitability and economies of scale that may undermine long-term investor confidence.

See More

Ford's Stock Surge and Profitability Outlook Analysis

- Stock Performance: Ford's stock surged 24% in May, significantly outperforming the S&P 500 index, attracting market participants seeking investment opportunities, although its price-to-earnings ratio of 11.3 still indicates a relatively cheap valuation.

- Dividend Appeal: With a dividend yield exceeding 4%, Ford has become a focal point for value investors, particularly in the current market environment, drawing attention from those seeking stable income.

- Growth Potential: Ford's pro segment achieved an 11.4% operating margin in Q1, with paid software subscriptions growing 30% year-over-year, indicating growth potential in commercial and government sectors that could support future profitability.

- Long-term Investment Risks: Despite strong short-term stock performance, Ford's long-term financial results are disappointing, with a total return of only 92% over the past decade, significantly trailing the S&P 500's 331%, indicating insufficient appeal as a long-term investment.

See More

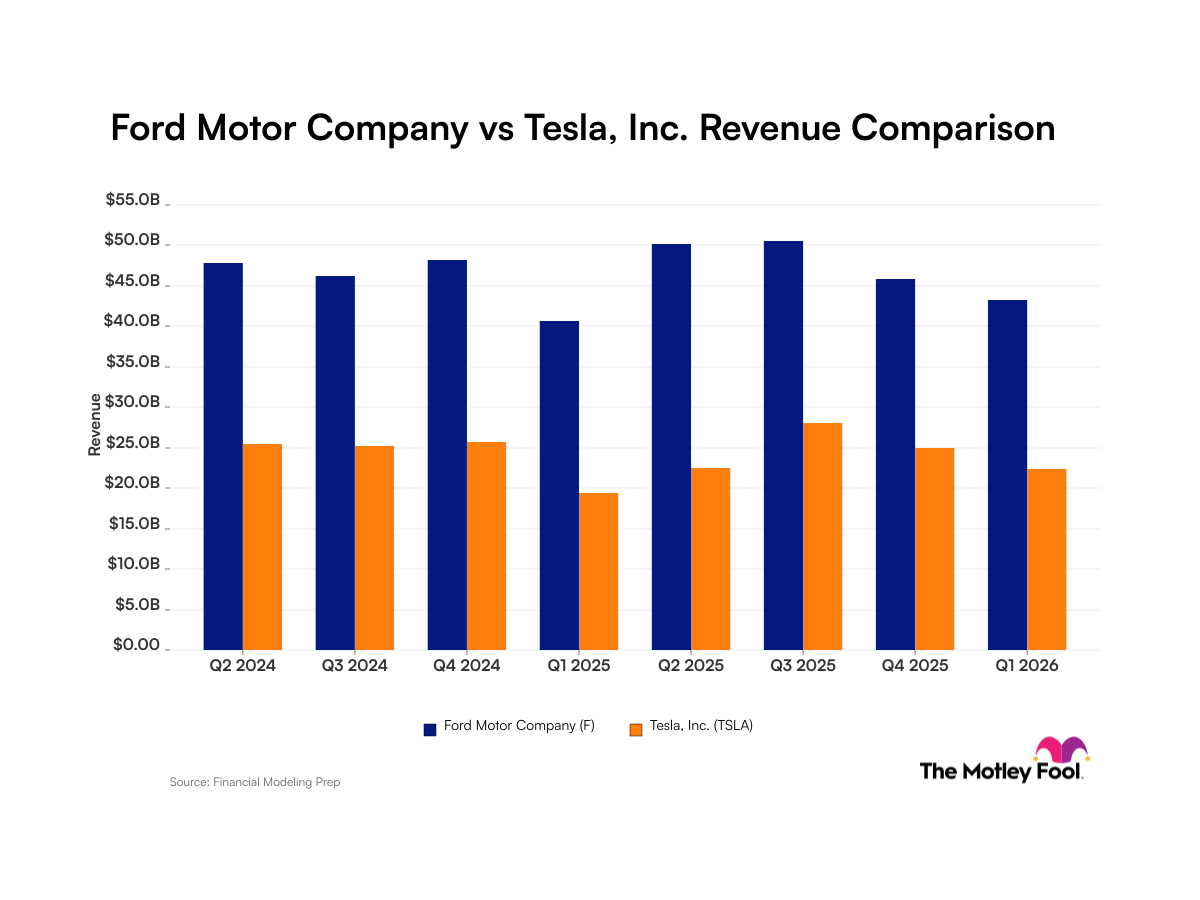

Analysis of Revenue Gap Between Ford and Tesla

- Revenue Gap Persistence: Ford consistently generates higher revenue than Tesla across all observed periods, with Ford's revenue showing a 6% year-over-year increase in Q1 2026, while Tesla's revenue grew by 16%, indicating a widening gap.

- Profitability Comparison: Ford reported a net income margin of approximately 6% for Q1 2026, compared to Tesla's 2%, highlighting Ford's superior profitability despite Tesla's faster revenue growth.

- Market Reaction Discrepancy: Ford's stock reached a 52-week high of $14.95 on May 22, while Tesla's stock exceeded $400, illustrating that revenue alone does not necessarily drive stock prices, as Tesla's rapid growth attracts more investor interest.

- Strategic Transformation and Challenges: Ford's newly established energy division aims to provide battery storage solutions, presenting a transformative opportunity, though associated costs may erode profits, while Tesla expands revenue through its ride-hailing service, minimizing operational costs.

See More

Financial Dynamics Analysis of Ford and Tesla

- Ford's Revenue Stability: Ford reported approximately $43.3 billion in revenue for Q1 2026, with a modest year-over-year growth of 6%, yet the establishment of a new product development organization is expected to enhance future innovation and market competitiveness.

- Tesla's Revenue Fluctuations: Tesla's revenue for Q1 2026 was $22.4 billion, reflecting a robust 16% year-over-year growth, despite challenges from workforce reductions and a transition to a subscription model for its Full Self-Driving software.

- Market Performance Comparison: While Ford's sales significantly exceed Tesla's, Ford's stock peaked at $14.95 over the past year, compared to Tesla's stock exceeding $400, indicating a market perception of Tesla's higher growth potential.

- Strategic Transformation Impact: Ford's newly established energy division aims to provide battery storage solutions, which may increase operational costs but also opens new revenue opportunities, while Tesla continues to enhance revenue through its autonomous ride-hailing service, maintaining its market leadership.

See More

Ford vs Tesla Revenue Comparison

- Ford's Stable Revenue: Ford reported approximately $43.3 billion in revenue for Q1 2026, with a modest 6% year-over-year growth; however, the establishment of a new product development organization is expected to enhance future product innovation and market competitiveness.

- Tesla's Revenue Fluctuations: Tesla's revenue for Q1 2026 was $22.4 billion, reflecting a 16% year-over-year increase, and despite facing workforce reductions and transition challenges, the subscription model for its Full Self-Driving software may enhance long-term revenue stability.

- Market Performance Discrepancy: While Ford's revenue significantly exceeds Tesla's, Ford's stock reached a 52-week high of $14.95, compared to Tesla's stock exceeding $400, indicating a market expectation for Tesla's future growth potential that is higher than Ford's.

- Strategic Transformation Impact: Ford's newly established energy division will provide battery storage solutions, which may increase short-term costs, but in the long run, it is expected to bolster the company's competitiveness in the battery market, particularly against Tesla's already established presence.

See More

Hindalco Projects Novelis to Earn $500 per Tonne by Fiscal 2027

- Earnings Outlook: Hindalco anticipates its subsidiary Novelis will achieve earnings of approximately $500 per tonne by fiscal 2027, reflecting confidence in future profitability amid strong demand in its Indian aluminium and copper sectors.

- Financial Impact: The fire-related disruptions at Novelis' Oswego plant resulted in a one-time charge of ₹41.71 billion (approximately $437.59 million) for fiscal 2026, impacting Hindalco's earnings; however, management asserts that “the worst is over.”

- Market Dynamics: Hindalco's U.S. operations contribute about 60% of revenue, reporting adjusted EBITDA of $462 per tonne for fiscal 2026, despite rising input costs due to the Middle East conflict affecting overall profitability.

- Growth Prospects: The company expects high double-digit growth in its domestic aluminium downstream business this fiscal year, driven by the ramp-up of its new rolling facility, Aditya FRP, and expansion into higher-value products such as EV components and construction materials.

See More

Ford Stock Soars 24% in May, Attracting Investor Interest

- Valuation Appeal: Ford's price-to-earnings ratio stands at 11.3, representing a 37% discount compared to its 10-year average, making its stock particularly attractive in the current market environment and likely to draw interest from value-focused investors.

- Attractive Dividend Yield: With a dividend yield of 4.02%, Ford not only appeals to dividend-seeking investors but also enhances its stock's attractiveness, especially in a low-interest-rate environment where income generation is crucial.

- Growth Potential from New Segment: Ford plans to launch battery energy storage systems in 2027, leveraging its electric vehicle infrastructure, which is expected to introduce a new growth engine and enhance its competitive position in the market.

- Profitability Challenges: Despite achieving an 11.4% operating margin in Q1, Ford's overall operating margin has averaged only 1.6% over the past decade, indicating ongoing challenges in profitability and economies of scale that may undermine long-term investor confidence.

See More

Ford's Stock Surge and Profitability Outlook Analysis

- Stock Performance: Ford's stock surged 24% in May, significantly outperforming the S&P 500 index, attracting market participants seeking investment opportunities, although its price-to-earnings ratio of 11.3 still indicates a relatively cheap valuation.

- Dividend Appeal: With a dividend yield exceeding 4%, Ford has become a focal point for value investors, particularly in the current market environment, drawing attention from those seeking stable income.

- Growth Potential: Ford's pro segment achieved an 11.4% operating margin in Q1, with paid software subscriptions growing 30% year-over-year, indicating growth potential in commercial and government sectors that could support future profitability.

- Long-term Investment Risks: Despite strong short-term stock performance, Ford's long-term financial results are disappointing, with a total return of only 92% over the past decade, significantly trailing the S&P 500's 331%, indicating insufficient appeal as a long-term investment.

See More

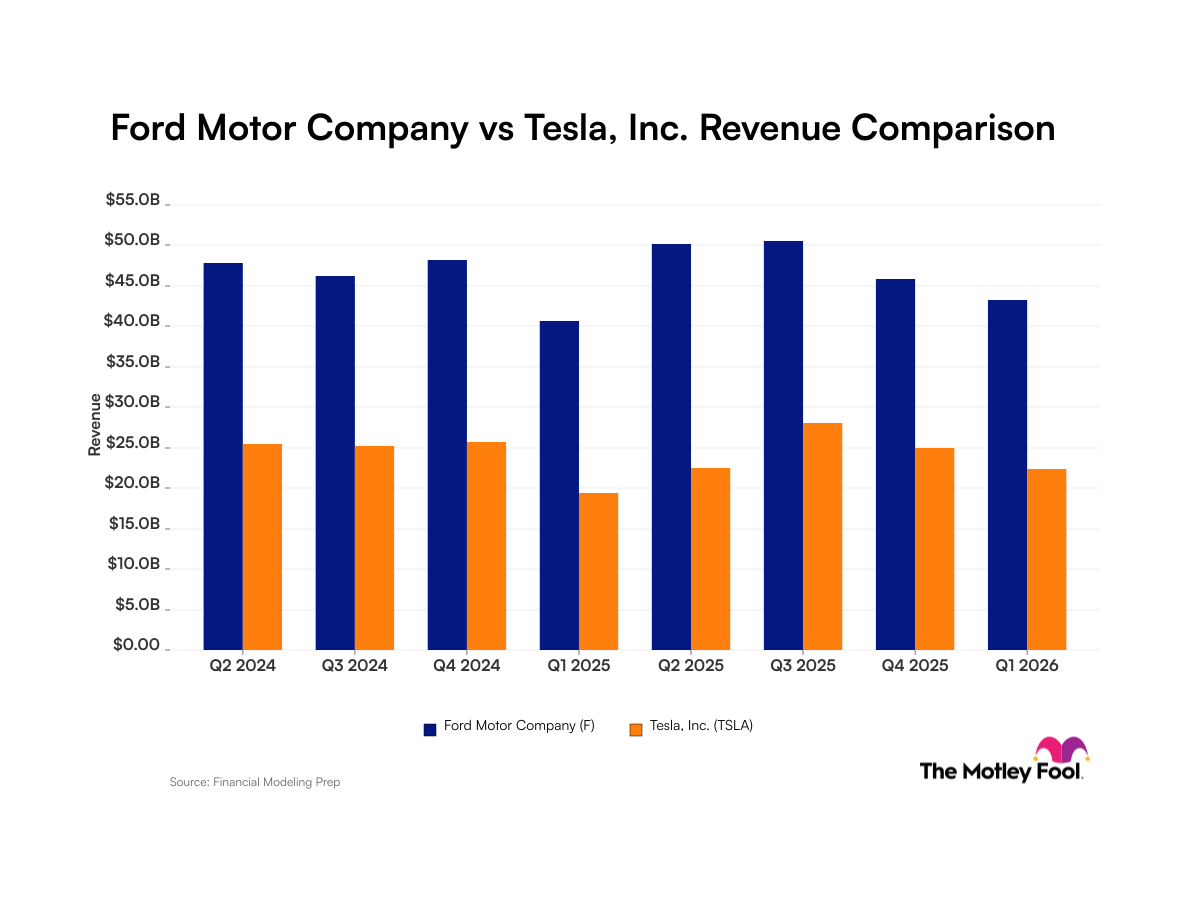

Analysis of Revenue Gap Between Ford and Tesla

- Revenue Gap Persistence: Ford consistently generates higher revenue than Tesla across all observed periods, with Ford's revenue showing a 6% year-over-year increase in Q1 2026, while Tesla's revenue grew by 16%, indicating a widening gap.

- Profitability Comparison: Ford reported a net income margin of approximately 6% for Q1 2026, compared to Tesla's 2%, highlighting Ford's superior profitability despite Tesla's faster revenue growth.

- Market Reaction Discrepancy: Ford's stock reached a 52-week high of $14.95 on May 22, while Tesla's stock exceeded $400, illustrating that revenue alone does not necessarily drive stock prices, as Tesla's rapid growth attracts more investor interest.

- Strategic Transformation and Challenges: Ford's newly established energy division aims to provide battery storage solutions, presenting a transformative opportunity, though associated costs may erode profits, while Tesla expands revenue through its ride-hailing service, minimizing operational costs.

See More

Financial Dynamics Analysis of Ford and Tesla

- Ford's Revenue Stability: Ford reported approximately $43.3 billion in revenue for Q1 2026, with a modest year-over-year growth of 6%, yet the establishment of a new product development organization is expected to enhance future innovation and market competitiveness.

- Tesla's Revenue Fluctuations: Tesla's revenue for Q1 2026 was $22.4 billion, reflecting a robust 16% year-over-year growth, despite challenges from workforce reductions and a transition to a subscription model for its Full Self-Driving software.

- Market Performance Comparison: While Ford's sales significantly exceed Tesla's, Ford's stock peaked at $14.95 over the past year, compared to Tesla's stock exceeding $400, indicating a market perception of Tesla's higher growth potential.

- Strategic Transformation Impact: Ford's newly established energy division aims to provide battery storage solutions, which may increase operational costs but also opens new revenue opportunities, while Tesla continues to enhance revenue through its autonomous ride-hailing service, maintaining its market leadership.

See More

Ford vs Tesla Revenue Comparison

- Ford's Stable Revenue: Ford reported approximately $43.3 billion in revenue for Q1 2026, with a modest 6% year-over-year growth; however, the establishment of a new product development organization is expected to enhance future product innovation and market competitiveness.

- Tesla's Revenue Fluctuations: Tesla's revenue for Q1 2026 was $22.4 billion, reflecting a 16% year-over-year increase, and despite facing workforce reductions and transition challenges, the subscription model for its Full Self-Driving software may enhance long-term revenue stability.

- Market Performance Discrepancy: While Ford's revenue significantly exceeds Tesla's, Ford's stock reached a 52-week high of $14.95, compared to Tesla's stock exceeding $400, indicating a market expectation for Tesla's future growth potential that is higher than Ford's.

- Strategic Transformation Impact: Ford's newly established energy division will provide battery storage solutions, which may increase short-term costs, but in the long run, it is expected to bolster the company's competitiveness in the battery market, particularly against Tesla's already established presence.

See More