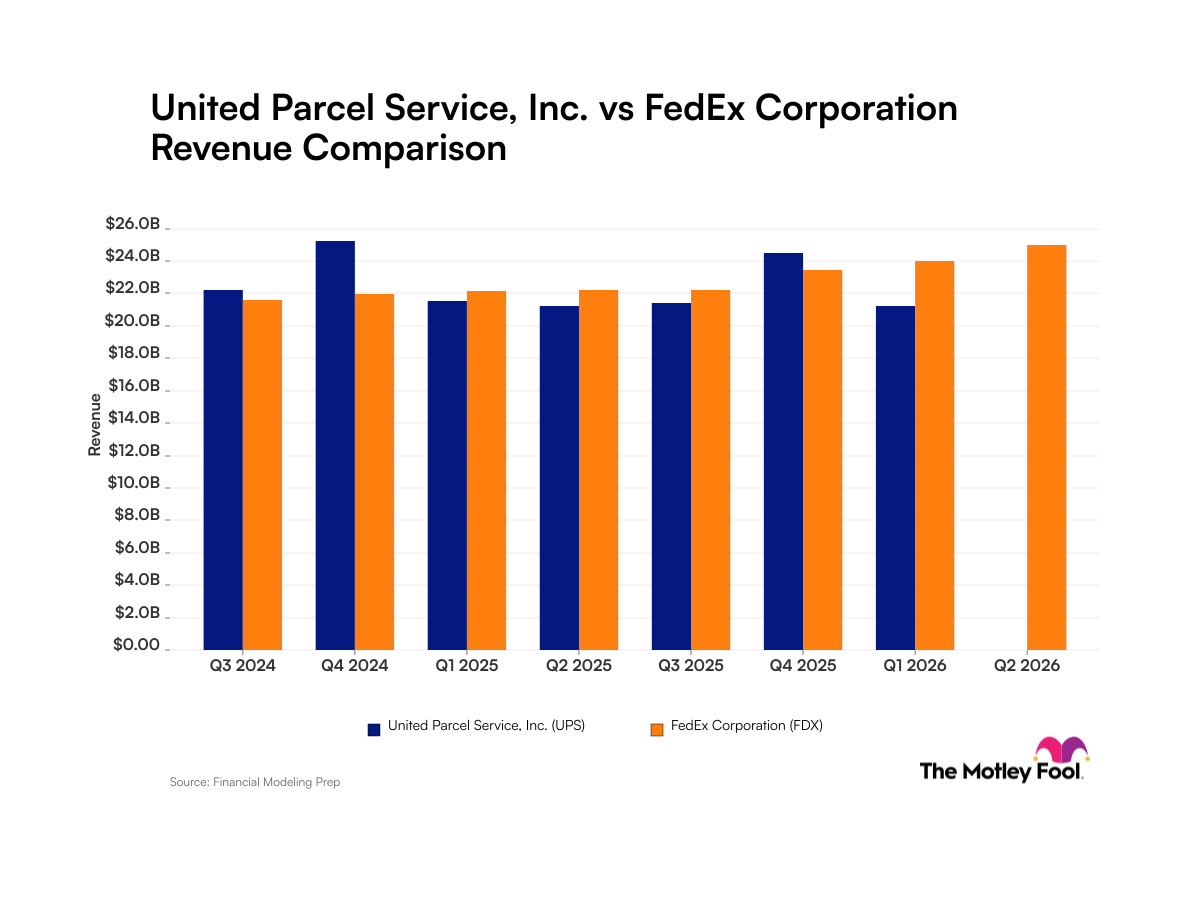

FedEx vs UPS: Revenue Trends Analysis

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 13 hours ago

0mins

Source: NASDAQ.COM

- Revenue Growth Comparison: FedEx has consistently achieved revenue growth over the past eight quarters, reporting $94.7 billion for fiscal year 2026, an 8% increase from $87.9 billion the previous year, demonstrating its stable business expansion capabilities.

- UPS Volatile Performance: In contrast, UPS experienced significant quarterly fluctuations during the same period, with a net income margin of 4% for Q1 2026, as it reduced its low-margin partnership with Amazon, leading to unstable revenue and impacting overall profitability.

- Strategic Market Differences: FedEx prioritizes volume growth, expecting approximately 11% year-over-year growth in the next fiscal year, while UPS focuses on margin protection due to higher union costs, limiting its revenue growth potential.

- Investor Considerations: Analysts advise investors to consider the impact of UPS's reduced collaboration with Amazon on its revenue before investing, while FedEx's spin-off of its freight business may further enhance its market share.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy UPS?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on UPS

Wall Street analysts forecast UPS stock price to fall

19 Analyst Rating

9 Buy

9 Hold

1 Sell

Moderate Buy

Current: 111.960

Low

80.00

Averages

107.06

High

126.00

Current: 111.960

Low

80.00

Averages

107.06

High

126.00

About UPS

United Parcel Service, Inc. is a global package delivery and logistics provider. Its U.S. Domestic Package segment offers a full spectrum of air and ground package transportation services. Its air portfolio offers time-definite, same-day, next-day, two-day and three-day delivery alternatives as well as air cargo services. Its ground network enables customers to ship using its day-definite ground service. Ground Saver provides residential ground service for customers with non-urgent, lightweight residential shipments. Its International Package segment consists of small package operations in Europe, Middle East and Africa, Canada and Latin America and Asia. It offers a selection of guaranteed day and time-definite international transportation services supported by its brokerage capabilities that facilitate cross-border clearance for international shipments. Its supply chain solutions consist of customized third-party logistics and specialized cold chain transportation solutions.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

UPS Stock Shows Signs of Turnaround

- Short-Term Rebound: UPS has rebounded strongly from its May lows, rallying back to the $110 area and forming a clear bullish cup-and-handle pattern; a breakout above the upper resistance line could target $128, surpassing its highest level in 2026, indicating potential upward momentum.

- Risk Management Strategy: A stop loss near $104 is recommended, as it is close to the handle of the formation, reflecting a risk management approach typical in pattern-based trade recommendations, ensuring capital protection amid volatility.

- Long-Term Trend Improvement: The weekly chart suggests the potential for a larger rounding bottom; if UPS can break above its 2026 high, it would create a broad basing structure encompassing approximately 18 months of price action, signaling future growth opportunities.

- Relative Performance Recovery: The relative performance chart against the S&P 500 highlights significant underperformance from 2023 to 2025, but recent signs of reversal are emerging, with the monthly relative strength index (RSI) rising after reaching oversold levels, indicating that downside momentum may be fading and long-term improvements are becoming evident.

See More

Analysis of Revenue Fluctuations for UPS and FedEx

- UPS Revenue Fluctuations: UPS reported a 4% net income margin for Q1 2026 while planning to close additional distribution centers; despite significant revenue from Amazon, the partnership was cut due to low margins, leading to increased quarterly revenue volatility and impacting overall profitability.

- FedEx Growth Momentum: FedEx achieved $94.7 billion in revenue for the fiscal year ending May 31, 2026, a notable increase from $87.9 billion the previous year, with an expected year-over-year growth of approximately 11% in the next fiscal year, indicating strong competitive positioning and expansion potential.

- Industry Comparison: UPS focuses on margin protection due to higher union costs, limiting revenue growth, while FedEx prioritizes volume growth to expand sales, highlighting significant strategic differences between the two companies.

- Market Dynamics Impact: UPS's revenue fluctuations are closely tied to its strategy of cutting low-margin business, while FedEx's spin-off of its freight division may further drive revenue growth, reflecting differing strategies in responding to market changes.

See More

FedEx vs UPS: Revenue Trends Analysis

- Revenue Growth Comparison: FedEx has consistently achieved revenue growth over the past eight quarters, reporting $94.7 billion for fiscal year 2026, an 8% increase from $87.9 billion the previous year, demonstrating its stable business expansion capabilities.

- UPS Volatile Performance: In contrast, UPS experienced significant quarterly fluctuations during the same period, with a net income margin of 4% for Q1 2026, as it reduced its low-margin partnership with Amazon, leading to unstable revenue and impacting overall profitability.

- Strategic Market Differences: FedEx prioritizes volume growth, expecting approximately 11% year-over-year growth in the next fiscal year, while UPS focuses on margin protection due to higher union costs, limiting its revenue growth potential.

- Investor Considerations: Analysts advise investors to consider the impact of UPS's reduced collaboration with Amazon on its revenue before investing, while FedEx's spin-off of its freight business may further enhance its market share.

See More

Multiple Companies Face Dividend Cut Risks

- Dividend Cut Risks: According to Wolfe Research, several companies are at risk of cutting dividends, particularly those with high debt levels and payout ratios exceeding 80%, which could directly impact income investors' cash flow.

- Whirlpool's Dividend Suspension: Whirlpool announced in May that it would suspend its dividend to pay down debt and navigate what it termed a 'recession-level industry decline,' reflecting the company's strategy under financial pressure, which may affect shareholder confidence.

- PepsiCo's Dividend Increase: Despite increasing its dividend in June, PepsiCo, with a 4.14% yield, appeared on Wolfe's screen, and its second-quarter earnings report is expected this Thursday, with analysts maintaining an optimistic outlook, indicating market confidence in its stability.

- UPS's Turnaround Plan: United Parcel Service (UPS) currently has a 5.95% dividend yield and aims for $3 billion in annual cost savings by 2026; despite challenges, its stock has risen 11% year-to-date, reflecting market recognition of its turnaround efforts.

See More

UPS Invests $48 Million to Upgrade Facilities

- Strategic Investment: UPS plans to invest $48 million in 27 temperature-controlled facilities to meet the growing demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, highlighting the company's strategic focus on the healthcare sector.

- Business Transformation: Despite a 50% drop in stock price from its 2022 peak, UPS is undergoing a massive business overhaul aimed at enhancing operational efficiency through modernization, although this may lead to short-term revenue declines and increased costs.

- Customer Focus: UPS is shifting from low-margin customers to high-margin ones, particularly in the healthcare sector, which is expected to yield higher profit margins and growth opportunities, reflecting the company's emphasis on future profitability.

- Market Reaction: Although investors remain cautious about UPS's turnaround, resulting in a high 6% dividend yield, the $48 million investment indicates a long-term strategic effort towards growth, potentially leading to a business inflection point in the second half of 2026.

See More

UPS Invests $48 Million in Temperature-Controlled Facilities

- Business Transformation Investment: UPS has announced a $48 million investment in 27 temperature-controlled facilities to meet the rising demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, thereby enhancing its market share and profit margins in the healthcare sector.

- Customer Focus Strategy: The company is shifting from low-margin high-volume customers to high-margin clients, which has led to a decline in overall revenue; however, revenue per package is increasing, indicating early signs of success, with management projecting a turnaround inflection point in the second half of 2026.

- Market Reaction and Dividends: Despite UPS's stock price dropping 50% from its 2022 peak, its 6% dividend yield reflects investor concerns about the turnaround, while also indicating market expectations for future growth potential.

- Long-term Strategic Significance: By investing in temperature-controlled facilities, UPS is not only enhancing service quality but also laying the groundwork for future growth, particularly in high-margin opportunities within the healthcare sector, signaling a potential shift from business contraction to expansion.

See More

UPS Stock Shows Signs of Turnaround

- Short-Term Rebound: UPS has rebounded strongly from its May lows, rallying back to the $110 area and forming a clear bullish cup-and-handle pattern; a breakout above the upper resistance line could target $128, surpassing its highest level in 2026, indicating potential upward momentum.

- Risk Management Strategy: A stop loss near $104 is recommended, as it is close to the handle of the formation, reflecting a risk management approach typical in pattern-based trade recommendations, ensuring capital protection amid volatility.

- Long-Term Trend Improvement: The weekly chart suggests the potential for a larger rounding bottom; if UPS can break above its 2026 high, it would create a broad basing structure encompassing approximately 18 months of price action, signaling future growth opportunities.

- Relative Performance Recovery: The relative performance chart against the S&P 500 highlights significant underperformance from 2023 to 2025, but recent signs of reversal are emerging, with the monthly relative strength index (RSI) rising after reaching oversold levels, indicating that downside momentum may be fading and long-term improvements are becoming evident.

See More

Analysis of Revenue Fluctuations for UPS and FedEx

- UPS Revenue Fluctuations: UPS reported a 4% net income margin for Q1 2026 while planning to close additional distribution centers; despite significant revenue from Amazon, the partnership was cut due to low margins, leading to increased quarterly revenue volatility and impacting overall profitability.

- FedEx Growth Momentum: FedEx achieved $94.7 billion in revenue for the fiscal year ending May 31, 2026, a notable increase from $87.9 billion the previous year, with an expected year-over-year growth of approximately 11% in the next fiscal year, indicating strong competitive positioning and expansion potential.

- Industry Comparison: UPS focuses on margin protection due to higher union costs, limiting revenue growth, while FedEx prioritizes volume growth to expand sales, highlighting significant strategic differences between the two companies.

- Market Dynamics Impact: UPS's revenue fluctuations are closely tied to its strategy of cutting low-margin business, while FedEx's spin-off of its freight division may further drive revenue growth, reflecting differing strategies in responding to market changes.

See More

FedEx vs UPS: Revenue Trends Analysis

- Revenue Growth Comparison: FedEx has consistently achieved revenue growth over the past eight quarters, reporting $94.7 billion for fiscal year 2026, an 8% increase from $87.9 billion the previous year, demonstrating its stable business expansion capabilities.

- UPS Volatile Performance: In contrast, UPS experienced significant quarterly fluctuations during the same period, with a net income margin of 4% for Q1 2026, as it reduced its low-margin partnership with Amazon, leading to unstable revenue and impacting overall profitability.

- Strategic Market Differences: FedEx prioritizes volume growth, expecting approximately 11% year-over-year growth in the next fiscal year, while UPS focuses on margin protection due to higher union costs, limiting its revenue growth potential.

- Investor Considerations: Analysts advise investors to consider the impact of UPS's reduced collaboration with Amazon on its revenue before investing, while FedEx's spin-off of its freight business may further enhance its market share.

See More

Multiple Companies Face Dividend Cut Risks

- Dividend Cut Risks: According to Wolfe Research, several companies are at risk of cutting dividends, particularly those with high debt levels and payout ratios exceeding 80%, which could directly impact income investors' cash flow.

- Whirlpool's Dividend Suspension: Whirlpool announced in May that it would suspend its dividend to pay down debt and navigate what it termed a 'recession-level industry decline,' reflecting the company's strategy under financial pressure, which may affect shareholder confidence.

- PepsiCo's Dividend Increase: Despite increasing its dividend in June, PepsiCo, with a 4.14% yield, appeared on Wolfe's screen, and its second-quarter earnings report is expected this Thursday, with analysts maintaining an optimistic outlook, indicating market confidence in its stability.

- UPS's Turnaround Plan: United Parcel Service (UPS) currently has a 5.95% dividend yield and aims for $3 billion in annual cost savings by 2026; despite challenges, its stock has risen 11% year-to-date, reflecting market recognition of its turnaround efforts.

See More

UPS Invests $48 Million to Upgrade Facilities

- Strategic Investment: UPS plans to invest $48 million in 27 temperature-controlled facilities to meet the growing demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, highlighting the company's strategic focus on the healthcare sector.

- Business Transformation: Despite a 50% drop in stock price from its 2022 peak, UPS is undergoing a massive business overhaul aimed at enhancing operational efficiency through modernization, although this may lead to short-term revenue declines and increased costs.

- Customer Focus: UPS is shifting from low-margin customers to high-margin ones, particularly in the healthcare sector, which is expected to yield higher profit margins and growth opportunities, reflecting the company's emphasis on future profitability.

- Market Reaction: Although investors remain cautious about UPS's turnaround, resulting in a high 6% dividend yield, the $48 million investment indicates a long-term strategic effort towards growth, potentially leading to a business inflection point in the second half of 2026.

See More

UPS Invests $48 Million in Temperature-Controlled Facilities

- Business Transformation Investment: UPS has announced a $48 million investment in 27 temperature-controlled facilities to meet the rising demand for low-temperature medication transport, particularly GLP-1 weight-loss drugs, thereby enhancing its market share and profit margins in the healthcare sector.

- Customer Focus Strategy: The company is shifting from low-margin high-volume customers to high-margin clients, which has led to a decline in overall revenue; however, revenue per package is increasing, indicating early signs of success, with management projecting a turnaround inflection point in the second half of 2026.

- Market Reaction and Dividends: Despite UPS's stock price dropping 50% from its 2022 peak, its 6% dividend yield reflects investor concerns about the turnaround, while also indicating market expectations for future growth potential.

- Long-term Strategic Significance: By investing in temperature-controlled facilities, UPS is not only enhancing service quality but also laying the groundwork for future growth, particularly in high-margin opportunities within the healthcare sector, signaling a potential shift from business contraction to expansion.

See More