Evercore Highlights Potential Upside for Microsoft's Azure Revenue

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy MSFT?

Source: seekingalpha

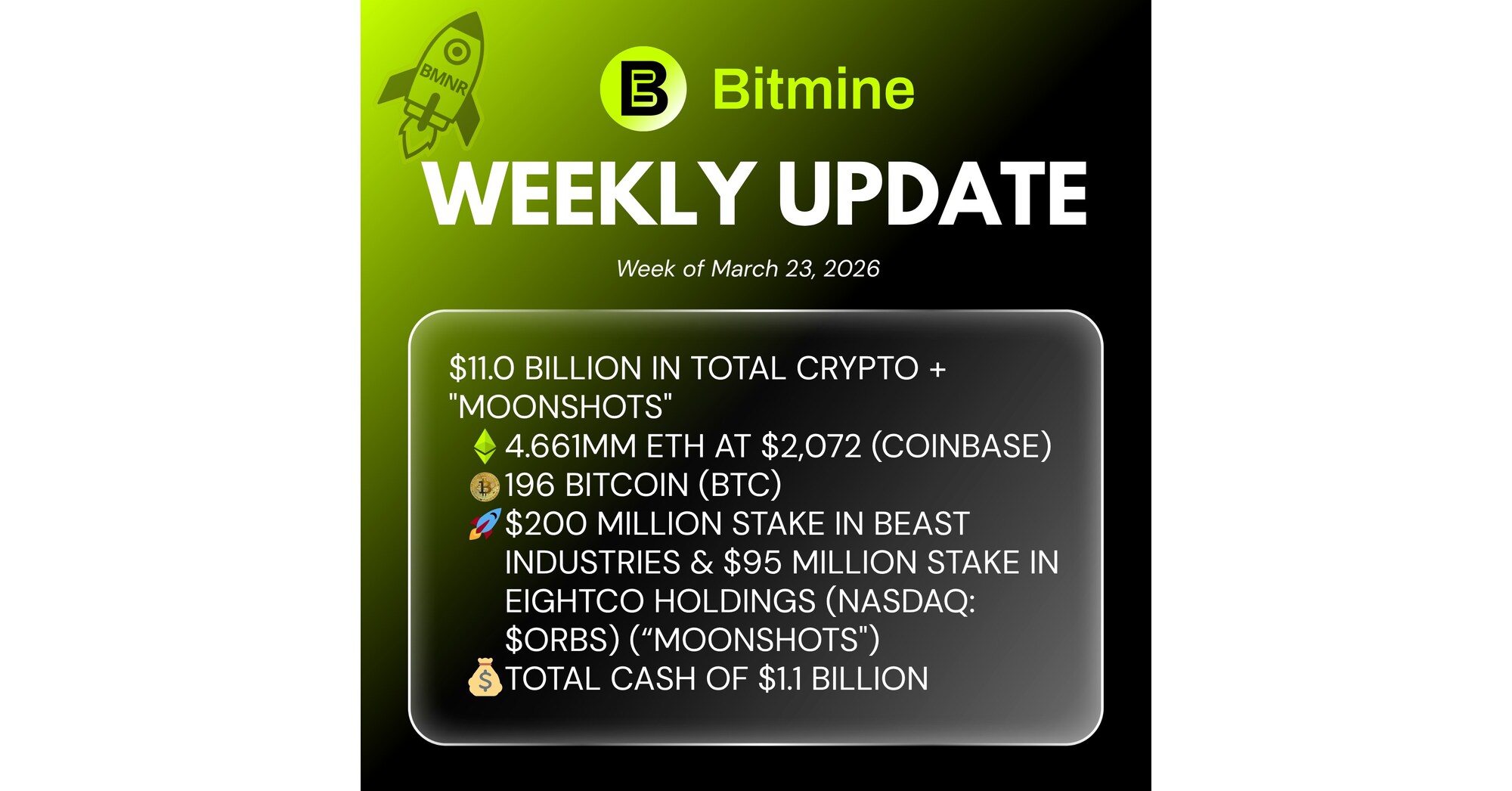

- Azure Revenue Upside: Evercore analysts project that if Microsoft's capital expenditures proceed as planned, Azure AI revenue could reach $25.7 billion in CY26, surpassing the previous estimate of $21.8 billion, indicating strong growth potential in the cloud computing sector.

- Robust Financial Performance: Microsoft reported a 15% year-over-year revenue growth in Q2 FY2023 in constant currency, driven by a 38% increase in Azure revenue, demonstrating solid fundamentals despite facing capacity challenges.

- Copilot Strategic Challenges: While Microsoft unveiled the Microsoft 365 Copilot Wave 3 and E7 suite, analysts noted that Copilot has not yet captured user interest to the expected extent, indicating challenges in adoption within the enterprise market that require time to overcome.

- Investor Concerns: Analysts believe the lack of consumption data related to Copilot creates unease among investors, emphasizing that providing usage metrics would help illustrate Copilot's value, although Microsoft's extensive enterprise presence still offers growth opportunities.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 381.870

Low

500.00

Averages

631.36

High

678.00

Current: 381.870

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company that develops and supports software, services, devices, and solutions. Its Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services, spanning a variety of devices and platforms. It comprises Microsoft 365 Commercial products and cloud services; Microsoft 365 Consumer products and cloud services; LinkedIn, and Dynamics products and cloud services. The Intelligent Cloud segment consists of its public, private, and hybrid server products and cloud services. It comprises server products and cloud services, including Azure, and enterprise and partner services, including Enterprise Support Services. Its More Personal Computing segment primarily comprises Windows and Devices, including Windows OEM licensing; Gaming, including Xbox hardware and Xbox content; Search and news advertising, comprising Bing and Copilot, Microsoft News, and Microsoft Edge.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft Faces Multiple Challenges and Opportunities

- Lowest Valuation: Microsoft’s P/E ratio of 25 marks its lowest since the 2022 bear market, indicating that while the stock appears cheap, it does not guarantee a rebound, prompting investors to carefully consider buying opportunities.

- Capital Expenditure Pressure: Microsoft has already spent $49 billion on AI-related capital expenditures in the first half of fiscal 2026, with projections reaching $100 billion for the year; despite holding $89 billion in liquidity, the high spending raises market concerns.

- Strong Revenue Growth: In the first half of fiscal 2026, Microsoft reported revenues of $159 billion, an 18% year-over-year increase, with net income of $66 billion reflecting a 36% rise, demonstrating effective expense management.

- AI Market Outlook: Grand View Research forecasts a 31% CAGR for the AI industry, potentially reaching $3.5 trillion by 2033, suggesting that Microsoft’s substantial investments could yield significant long-term returns.

See More

OPENAI IN NEGOTIATIONS TO PURCHASE POWER FROM SAM ALTMAN-SUPPORTED FUSION COMPANY HELION ENERGY - AXIOS

OpenAI's Acquisition Talks: OpenAI is in advanced discussions to acquire Electric City, a startup backed by Sam Altman, focusing on fusion energy technology.

Fusion Energy Focus: The acquisition aims to enhance OpenAI's capabilities in the energy sector, particularly in developing sustainable fusion energy solutions.

See More

Microsoft Stock Undervalued, Investment Opportunity Emerges

- Rapid Cloud Growth: Microsoft's cloud computing segment, Azure, saw a 39% year-over-year revenue increase last quarter, indicating strong demand in the AI sector and solidifying Microsoft's leadership in the rapidly expanding AI market.

- Strong Overall Performance: With a 17% year-over-year revenue growth, Microsoft's fundamentals remain robust despite a low market valuation, suggesting potential for increased investor interest in the near future.

- Historically Undervalued Levels: Currently, Microsoft's stock is at a rarely seen low valuation over the past decade, with its operating price-to-earnings ratio highlighting its attractiveness, presenting a buying opportunity akin to early 2023.

- Ongoing AI Strategy: Microsoft's investments and neutral strategy in AI position it as the preferred platform for developers, expected to continue driving market share growth and enhancing the company's central role in global AI deployment.

See More

Evercore Highlights Potential Upside for Microsoft's Azure Revenue

- Azure Revenue Upside: Evercore analysts project that if Microsoft's capital expenditures proceed as planned, Azure AI revenue could reach $25.7 billion in CY26, surpassing the previous estimate of $21.8 billion, indicating strong growth potential in the cloud computing sector.

- Robust Financial Performance: Microsoft reported a 15% year-over-year revenue growth in Q2 FY2023 in constant currency, driven by a 38% increase in Azure revenue, demonstrating solid fundamentals despite facing capacity challenges.

- Copilot Strategic Challenges: While Microsoft unveiled the Microsoft 365 Copilot Wave 3 and E7 suite, analysts noted that Copilot has not yet captured user interest to the expected extent, indicating challenges in adoption within the enterprise market that require time to overcome.

- Investor Concerns: Analysts believe the lack of consumption data related to Copilot creates unease among investors, emphasizing that providing usage metrics would help illustrate Copilot's value, although Microsoft's extensive enterprise presence still offers growth opportunities.

See More

Micron Technology Options Volume Surges

- Surge in Options Volume: Micron Technology (MU) sees an options trading volume of 381,326 contracts today, equating to approximately 38.1 million shares, which is about 99% of its average daily trading volume over the past month.

- High-Frequency Trading Insight: The $400 strike put option stands out with 21,756 contracts traded today, representing around 2.2 million shares of MU, indicating market expectations for potential price declines.

- Microsoft Options Activity: Concurrently, Microsoft (MSFT) experiences an options volume of 332,121 contracts, translating to approximately 33.2 million shares, which is about 97.2% of its average daily trading volume over the past month, reflecting investor interest in its future performance.

- Market Trend Observation: The $387.50 strike call option for MSFT shows significant activity with 16,022 contracts traded today, representing about 1.6 million shares, suggesting a bullish sentiment regarding Microsoft's stock price appreciation.

See More

Oil Price Plunge Boosts Stock Market Gains

- Market Surge: The S&P 500 rose by 2.10%, the Dow Jones by 2.30%, and the Nasdaq 100 by 2.19%, indicating a strong market response to the sharp drop in oil prices, which is expected to enhance corporate profitability.

- Oil Price Drop: Crude oil prices plummeted over 10% after President Trump postponed strikes on Iranian energy infrastructure, which will lower fuel costs for airlines and cruise lines, thereby boosting their profit margins.

- Bond Yields Decline: The 10-year Treasury yield fell from an 8-month high of 4.44% to 4.34%, reflecting reduced market concerns about inflationary pressures, which supports further stock market gains.

- International Tensions: Productive talks between Trump and Iran may lead to an end to the Middle East conflict, with the International Energy Agency reporting severe damage to over 40 energy sites across nine countries, potentially causing long-term disruptions to global supply chains.

See More

Microsoft Faces Multiple Challenges and Opportunities

- Lowest Valuation: Microsoft’s P/E ratio of 25 marks its lowest since the 2022 bear market, indicating that while the stock appears cheap, it does not guarantee a rebound, prompting investors to carefully consider buying opportunities.

- Capital Expenditure Pressure: Microsoft has already spent $49 billion on AI-related capital expenditures in the first half of fiscal 2026, with projections reaching $100 billion for the year; despite holding $89 billion in liquidity, the high spending raises market concerns.

- Strong Revenue Growth: In the first half of fiscal 2026, Microsoft reported revenues of $159 billion, an 18% year-over-year increase, with net income of $66 billion reflecting a 36% rise, demonstrating effective expense management.

- AI Market Outlook: Grand View Research forecasts a 31% CAGR for the AI industry, potentially reaching $3.5 trillion by 2033, suggesting that Microsoft’s substantial investments could yield significant long-term returns.

See More

OPENAI IN NEGOTIATIONS TO PURCHASE POWER FROM SAM ALTMAN-SUPPORTED FUSION COMPANY HELION ENERGY - AXIOS

OpenAI's Acquisition Talks: OpenAI is in advanced discussions to acquire Electric City, a startup backed by Sam Altman, focusing on fusion energy technology.

Fusion Energy Focus: The acquisition aims to enhance OpenAI's capabilities in the energy sector, particularly in developing sustainable fusion energy solutions.

See More

Microsoft Stock Undervalued, Investment Opportunity Emerges

- Rapid Cloud Growth: Microsoft's cloud computing segment, Azure, saw a 39% year-over-year revenue increase last quarter, indicating strong demand in the AI sector and solidifying Microsoft's leadership in the rapidly expanding AI market.

- Strong Overall Performance: With a 17% year-over-year revenue growth, Microsoft's fundamentals remain robust despite a low market valuation, suggesting potential for increased investor interest in the near future.

- Historically Undervalued Levels: Currently, Microsoft's stock is at a rarely seen low valuation over the past decade, with its operating price-to-earnings ratio highlighting its attractiveness, presenting a buying opportunity akin to early 2023.

- Ongoing AI Strategy: Microsoft's investments and neutral strategy in AI position it as the preferred platform for developers, expected to continue driving market share growth and enhancing the company's central role in global AI deployment.

See More

Evercore Highlights Potential Upside for Microsoft's Azure Revenue

- Azure Revenue Upside: Evercore analysts project that if Microsoft's capital expenditures proceed as planned, Azure AI revenue could reach $25.7 billion in CY26, surpassing the previous estimate of $21.8 billion, indicating strong growth potential in the cloud computing sector.

- Robust Financial Performance: Microsoft reported a 15% year-over-year revenue growth in Q2 FY2023 in constant currency, driven by a 38% increase in Azure revenue, demonstrating solid fundamentals despite facing capacity challenges.

- Copilot Strategic Challenges: While Microsoft unveiled the Microsoft 365 Copilot Wave 3 and E7 suite, analysts noted that Copilot has not yet captured user interest to the expected extent, indicating challenges in adoption within the enterprise market that require time to overcome.

- Investor Concerns: Analysts believe the lack of consumption data related to Copilot creates unease among investors, emphasizing that providing usage metrics would help illustrate Copilot's value, although Microsoft's extensive enterprise presence still offers growth opportunities.

See More

Micron Technology Options Volume Surges

- Surge in Options Volume: Micron Technology (MU) sees an options trading volume of 381,326 contracts today, equating to approximately 38.1 million shares, which is about 99% of its average daily trading volume over the past month.

- High-Frequency Trading Insight: The $400 strike put option stands out with 21,756 contracts traded today, representing around 2.2 million shares of MU, indicating market expectations for potential price declines.

- Microsoft Options Activity: Concurrently, Microsoft (MSFT) experiences an options volume of 332,121 contracts, translating to approximately 33.2 million shares, which is about 97.2% of its average daily trading volume over the past month, reflecting investor interest in its future performance.

- Market Trend Observation: The $387.50 strike call option for MSFT shows significant activity with 16,022 contracts traded today, representing about 1.6 million shares, suggesting a bullish sentiment regarding Microsoft's stock price appreciation.

See More

Oil Price Plunge Boosts Stock Market Gains

- Market Surge: The S&P 500 rose by 2.10%, the Dow Jones by 2.30%, and the Nasdaq 100 by 2.19%, indicating a strong market response to the sharp drop in oil prices, which is expected to enhance corporate profitability.

- Oil Price Drop: Crude oil prices plummeted over 10% after President Trump postponed strikes on Iranian energy infrastructure, which will lower fuel costs for airlines and cruise lines, thereby boosting their profit margins.

- Bond Yields Decline: The 10-year Treasury yield fell from an 8-month high of 4.44% to 4.34%, reflecting reduced market concerns about inflationary pressures, which supports further stock market gains.

- International Tensions: Productive talks between Trump and Iran may lead to an end to the Middle East conflict, with the International Energy Agency reporting severe damage to over 40 energy sites across nine countries, potentially causing long-term disruptions to global supply chains.

See More