Buffett's Investment Philosophy Lives On: The Appeal of Apple and Alphabet

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy AAPL?

Source: Fool

- Apple's Brand Strength: Apple continues to attract consumers with its strong brand influence and customer loyalty, as evidenced by its latest earnings report showing a 16% year-over-year revenue increase to $143.8 billion in Q1 2026, indicating its solid market position and long-term growth potential.

- Expansion of Service Ecosystem: Apple's services segment reached a new high for paid accounts in Q1 2026, and with the growing base of active devices, there are ample opportunities to further tap into revenue streams, enhancing the company's overall profitability.

- Google's Advertising Business: Google's core advertising business generated $113.8 billion in revenue in Q4 2026, an 18% year-over-year increase, showcasing its competitive edge in the search engine market and strong network effects that further solidify its market position.

- Growth Potential in Cloud and AI: Google's cloud segment achieved $17.7 billion in revenue in Q4, up 48% year-over-year, with a cloud backlog of $240 billion, indicating that the company's investments in cloud computing and artificial intelligence will provide robust growth momentum for the future.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AAPL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AAPL

Wall Street analysts forecast AAPL stock price to rise

27 Analyst Rating

17 Buy

9 Hold

1 Sell

Moderate Buy

Current: 260.830

Low

239.00

Averages

306.89

High

350.00

Current: 260.830

Low

239.00

Averages

306.89

High

350.00

About AAPL

Apple Inc. designs, manufactures and markets smartphones, personal computers, tablets, wearables and accessories, and sells a variety of related services. Its product categories include iPhone, Mac, iPad, and Wearables, Home and Accessories. Its software platforms include iOS, iPadOS, macOS, watchOS, visionOS, and tvOS. Its services include advertising, AppleCare, cloud services, digital content and payment services. The Company operates various platforms, including the App Store, that allow customers to discover and download applications and digital content, such as books, music, video, games and podcasts. It also offers digital content through subscription-based services, including Apple Arcade, Apple Fitness+, Apple Music, Apple News+, and Apple TV+. Its products include iPhone 16 Pro, iPhone 16, iPhone 15, iPhone 14, iPhone SE, MacBook Air, MacBook Pro, iMac, Mac mini, Mac Studio, Mac Pro, iPad Pro, iPad Air, AirPods, AirPods Pro, AirPods Max, Apple TV, Apple Vision Pro and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Apple's MacBook Neo Officially Launched

- Positive Market Reception: Apple's MacBook Neo officially launched on Wednesday, with expected shipments of 4.5 to 5 million units this year despite being in small-volume production, indicating strong market demand, particularly in the education sector.

- Significant Price Advantage: Starting at $599 (or $499 for education), the MacBook Neo effectively fills a gap in Apple's mid-range PC market, likely attracting more price-sensitive consumers and enhancing cross-device engagement within the Apple ecosystem.

- Changing Competitive Landscape: Analysts note that rising memory prices may lead other laptop models to increase prices starting in Q2 2026, making the MacBook Neo more competitive on price and further solidifying its market position.

- Market Share Growth: J.P. Morgan analysts believe the MacBook Neo will significantly increase Apple's computer market share, particularly against Chromebooks and Windows devices, leveraging the A18 Pro chip to ensure smooth product delivery.

See More

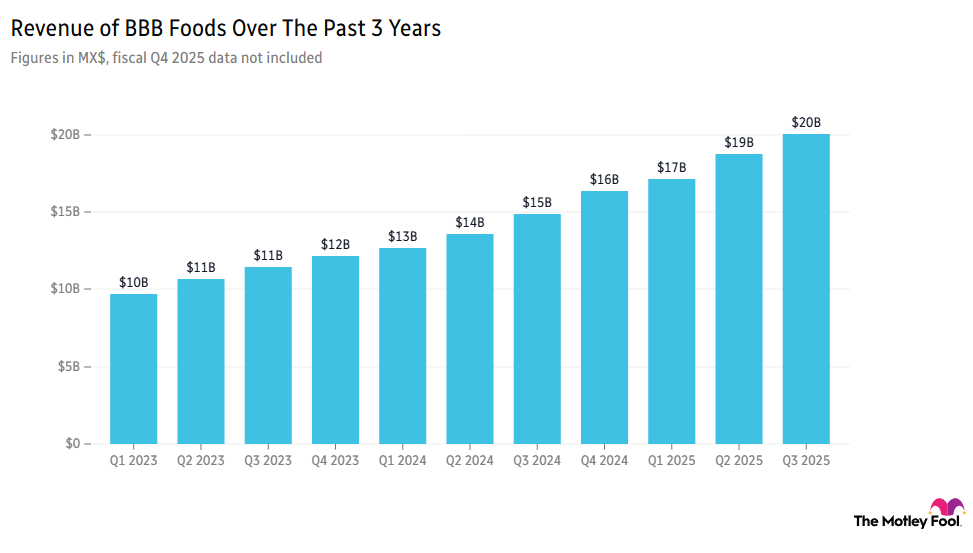

BBB Foods Prioritizes Growth Over Margins Amid Losses

- Net Loss Continues: BBB Foods (TBBB) fell over 2% ahead of the opening bell due to a higher-than-expected net loss, marking the fourth consecutive quarter of missing consensus earnings per share estimates, despite a 34.4% year-over-year revenue increase, indicating profitability challenges amid aggressive expansion.

- CEO Strategic Shift: CEO K. Anthony Hatoum emphasized that while EBITDA margin is important, the company does not manage to a specific profit target, focusing instead on successfully opening new stores, enhancing customer value, and improving operational efficiency, which may impact short-term profitability.

- Market Performance Outpaces Index: Since the July 2025 Rule Breakers recommendation, BBB Foods' stock has outperformed the S&P 500 by 17%, reflecting market recognition of its growth strategy despite ongoing losses.

- Consumer Behavior Changes: Analyst Dan Caplinger noted that shoppers have been visiting BBB Foods stores more frequently and spending more per visit, indicating positive progress in customer attraction and sales enhancement.

See More

India Plans New Smartphone Manufacturing Incentives

- Export-Linked Incentives: India is drafting a new smartphone manufacturing incentive scheme that ties government subsidies to exports and domestic parts usage, which is expected to benefit Apple, Samsung, and their suppliers, thereby boosting smartphone exports from India.

- Policy Shift: The new plan will replace the current Production-Linked Incentive program, explicitly linking benefits to exports and localization, aiming to enhance India's position in global supply chains and attract companies to use India as an export base.

- Localization Requirements: The new incentives will be tiered based on the level of domestic value addition in devices, with manufacturers receiving additional benefits for sourcing critical components from Indian suppliers, promoting local production of high-value parts.

- Market Outlook: As the current incentive program nears its end, companies are urgently seeking clarity on the new policy, which is expected to drive export plans for Apple and Samsung, further solidifying India's role as a global smartphone manufacturing hub.

See More

Buffett's Investment Philosophy Lives On: The Appeal of Apple and Alphabet

- Apple's Brand Strength: Apple continues to attract consumers with its strong brand influence and customer loyalty, as evidenced by its latest earnings report showing a 16% year-over-year revenue increase to $143.8 billion in Q1 2026, indicating its solid market position and long-term growth potential.

- Expansion of Service Ecosystem: Apple's services segment reached a new high for paid accounts in Q1 2026, and with the growing base of active devices, there are ample opportunities to further tap into revenue streams, enhancing the company's overall profitability.

- Google's Advertising Business: Google's core advertising business generated $113.8 billion in revenue in Q4 2026, an 18% year-over-year increase, showcasing its competitive edge in the search engine market and strong network effects that further solidify its market position.

- Growth Potential in Cloud and AI: Google's cloud segment achieved $17.7 billion in revenue in Q4, up 48% year-over-year, with a cloud backlog of $240 billion, indicating that the company's investments in cloud computing and artificial intelligence will provide robust growth momentum for the future.

See More

Apple's AI Strategy Sparks Market Interest

- Market Position Recovery: Apple's stock has surged nearly 30% over the past few months, potentially allowing it to reclaim its market-leading status, despite its overall business experiencing sluggish growth with revenues fluctuating in the mid-single digits, leading investors to remain cautious about its future performance.

- Low AI Spending Attracts Investors: Apple's conservative approach to AI spending makes it more appealing in the current market, especially as the AI sector faces challenges; investors are increasingly favoring stable companies like Apple over those aggressively transforming into AI-first operations.

- Increased Competitive Pressure: While Apple enjoys high customer loyalty, the introduction of AI features by competitors poses a threat to its market share, and there is a risk that a game-changing feature could emerge, leading to potential user attrition and impacting Apple's ecosystem.

- Strategic Risks Emerge: Although Apple's cautious AI investment strategy has garnered market favor in the short term, if generative AI does not develop as expected, Apple may need to rely on external companies for computing capacity, which could challenge its future market position.

See More

Apple's AI Investment Strategy Raises Concerns

- Market Recovery: Apple's (NASDAQ: AAPL) stock has surged nearly 30% over the past few months, indicating investor preference for its relatively low-risk investment strategy, despite significantly lower AI spending compared to peers.

- Increased Competitive Pressure: While Apple remains the most popular tech brand in the U.S., the introduction of AI features by competitors poses a challenge to user loyalty, which could impact its market share in the future.

- Investor Sentiment Shift: In contrast to Nvidia's (NASDAQ: NVDA) mere 5.5% gain since August, Apple's performance suggests that investors are gravitating towards companies that maintain a low profile in AI spending, reflecting a cautious approach to market volatility.

- Strategic Risk Assessment: Although Apple's conservative AI investment strategy may attract investors in the short term, failing to keep pace with industry changes could necessitate reliance on external computing capacity for its AI models, increasing future uncertainty.

See More

Apple's MacBook Neo Officially Launched

- Positive Market Reception: Apple's MacBook Neo officially launched on Wednesday, with expected shipments of 4.5 to 5 million units this year despite being in small-volume production, indicating strong market demand, particularly in the education sector.

- Significant Price Advantage: Starting at $599 (or $499 for education), the MacBook Neo effectively fills a gap in Apple's mid-range PC market, likely attracting more price-sensitive consumers and enhancing cross-device engagement within the Apple ecosystem.

- Changing Competitive Landscape: Analysts note that rising memory prices may lead other laptop models to increase prices starting in Q2 2026, making the MacBook Neo more competitive on price and further solidifying its market position.

- Market Share Growth: J.P. Morgan analysts believe the MacBook Neo will significantly increase Apple's computer market share, particularly against Chromebooks and Windows devices, leveraging the A18 Pro chip to ensure smooth product delivery.

See More

BBB Foods Prioritizes Growth Over Margins Amid Losses

- Net Loss Continues: BBB Foods (TBBB) fell over 2% ahead of the opening bell due to a higher-than-expected net loss, marking the fourth consecutive quarter of missing consensus earnings per share estimates, despite a 34.4% year-over-year revenue increase, indicating profitability challenges amid aggressive expansion.

- CEO Strategic Shift: CEO K. Anthony Hatoum emphasized that while EBITDA margin is important, the company does not manage to a specific profit target, focusing instead on successfully opening new stores, enhancing customer value, and improving operational efficiency, which may impact short-term profitability.

- Market Performance Outpaces Index: Since the July 2025 Rule Breakers recommendation, BBB Foods' stock has outperformed the S&P 500 by 17%, reflecting market recognition of its growth strategy despite ongoing losses.

- Consumer Behavior Changes: Analyst Dan Caplinger noted that shoppers have been visiting BBB Foods stores more frequently and spending more per visit, indicating positive progress in customer attraction and sales enhancement.

See More

India Plans New Smartphone Manufacturing Incentives

- Export-Linked Incentives: India is drafting a new smartphone manufacturing incentive scheme that ties government subsidies to exports and domestic parts usage, which is expected to benefit Apple, Samsung, and their suppliers, thereby boosting smartphone exports from India.

- Policy Shift: The new plan will replace the current Production-Linked Incentive program, explicitly linking benefits to exports and localization, aiming to enhance India's position in global supply chains and attract companies to use India as an export base.

- Localization Requirements: The new incentives will be tiered based on the level of domestic value addition in devices, with manufacturers receiving additional benefits for sourcing critical components from Indian suppliers, promoting local production of high-value parts.

- Market Outlook: As the current incentive program nears its end, companies are urgently seeking clarity on the new policy, which is expected to drive export plans for Apple and Samsung, further solidifying India's role as a global smartphone manufacturing hub.

See More

Buffett's Investment Philosophy Lives On: The Appeal of Apple and Alphabet

- Apple's Brand Strength: Apple continues to attract consumers with its strong brand influence and customer loyalty, as evidenced by its latest earnings report showing a 16% year-over-year revenue increase to $143.8 billion in Q1 2026, indicating its solid market position and long-term growth potential.

- Expansion of Service Ecosystem: Apple's services segment reached a new high for paid accounts in Q1 2026, and with the growing base of active devices, there are ample opportunities to further tap into revenue streams, enhancing the company's overall profitability.

- Google's Advertising Business: Google's core advertising business generated $113.8 billion in revenue in Q4 2026, an 18% year-over-year increase, showcasing its competitive edge in the search engine market and strong network effects that further solidify its market position.

- Growth Potential in Cloud and AI: Google's cloud segment achieved $17.7 billion in revenue in Q4, up 48% year-over-year, with a cloud backlog of $240 billion, indicating that the company's investments in cloud computing and artificial intelligence will provide robust growth momentum for the future.

See More

Apple's AI Strategy Sparks Market Interest

- Market Position Recovery: Apple's stock has surged nearly 30% over the past few months, potentially allowing it to reclaim its market-leading status, despite its overall business experiencing sluggish growth with revenues fluctuating in the mid-single digits, leading investors to remain cautious about its future performance.

- Low AI Spending Attracts Investors: Apple's conservative approach to AI spending makes it more appealing in the current market, especially as the AI sector faces challenges; investors are increasingly favoring stable companies like Apple over those aggressively transforming into AI-first operations.

- Increased Competitive Pressure: While Apple enjoys high customer loyalty, the introduction of AI features by competitors poses a threat to its market share, and there is a risk that a game-changing feature could emerge, leading to potential user attrition and impacting Apple's ecosystem.

- Strategic Risks Emerge: Although Apple's cautious AI investment strategy has garnered market favor in the short term, if generative AI does not develop as expected, Apple may need to rely on external companies for computing capacity, which could challenge its future market position.

See More

Apple's AI Investment Strategy Raises Concerns

- Market Recovery: Apple's (NASDAQ: AAPL) stock has surged nearly 30% over the past few months, indicating investor preference for its relatively low-risk investment strategy, despite significantly lower AI spending compared to peers.

- Increased Competitive Pressure: While Apple remains the most popular tech brand in the U.S., the introduction of AI features by competitors poses a challenge to user loyalty, which could impact its market share in the future.

- Investor Sentiment Shift: In contrast to Nvidia's (NASDAQ: NVDA) mere 5.5% gain since August, Apple's performance suggests that investors are gravitating towards companies that maintain a low profile in AI spending, reflecting a cautious approach to market volatility.

- Strategic Risk Assessment: Although Apple's conservative AI investment strategy may attract investors in the short term, failing to keep pace with industry changes could necessitate reliance on external computing capacity for its AI models, increasing future uncertainty.

See More