As Big Tech Dominates the News, Small-Cap Stocks Are Surging. Can This Momentum Continue?

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 16 2026

0mins

Source: Barron's

Tesla's Ambition: Elon Musk predicts that Optimus robots will become the best surgeons on Earth by the end of the decade.

Walmart's Drone Delivery Expansion: Walmart is collaborating with Alphabet to increase aerial drone delivery services to 40 million customers next year, a significant rise from the current two million.

Disney's Theme Park Update: Walt Disney is planning to retheme its Rock ‘n’ Roller Coaster at Hollywood Studios to feature The Muppets, showcasing the company's focus on innovative attractions.

Small-Cap Stocks Performance: There is a notable trend of small-cap stocks outperforming larger ones since mid-November, raising questions about whether this is a temporary phenomenon or the beginning of a longer-term recovery.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BAC?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BAC

Wall Street analysts forecast BAC stock price to rise

19 Analyst Rating

15 Buy

4 Hold

0 Sell

Strong Buy

Current: 58.730

Low

55.00

Averages

61.64

High

71.00

Current: 58.730

Low

55.00

Averages

61.64

High

71.00

About BAC

Bank of America Corporation is a bank holding company and a financial holding company. Its segments include Consumer Banking, Global Wealth & Investment Management (GWIM), Global Banking and Global Markets. Consumer Banking segment offers a range of credit, banking and investment products and services to consumers and small businesses. The GWIM includes two businesses: Merrill Wealth Management, which provides tailored solutions to meet clients' needs through a full set of investment management, brokerage, banking and retirement products and Bank of America Private Bank, which provides comprehensive wealth management solutions. Global Banking segment provides a range of lending-related products and services, integrated working capital management and treasury solutions, and underwriting and advisory services. Global Markets segment offers sales and trading services and research services to institutional clients across fixed-income, credit, currency, commodity, and equity businesses.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

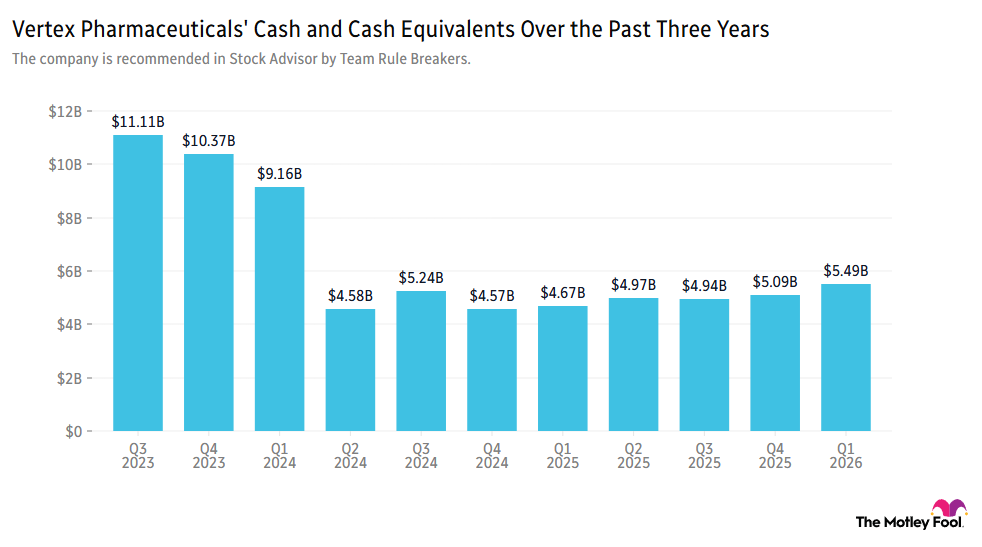

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Fiserv Discusses Sale of Payments Business with Major Banks

- Stock Surge: Fiserv shares rallied over 5% after The Wall Street Journal reported discussions with major banks like JPMorgan and Bank of America regarding the sale of its payments infrastructure business, potentially leading to strategic restructuring and enhanced market competitiveness.

- Acquisition Deal: Vertex Pharmaceuticals announced a $10 billion acquisition of Crinetics Pharmaceuticals to expand its product line in rare hormonal disease treatments, although Vertex shares dipped nearly 1%, this deal is expected to strengthen its market position.

- Stock Upgrade: First Solar's stock rose nearly 3% after Deutsche Bank upgraded its rating from neutral to buy, with analysts citing potential trade policy shifts as a reason for investors to buy the dip, boosting market confidence.

- EV Stock Decline: Rivian shares tumbled 9% despite revenue and delivery guidance exceeding market expectations, as the company announced a plan to sell 75 million new shares for a significant capital raise, negatively impacting investor sentiment.

See More

Major Banks Explore Acquisition of Fiserv's Debit Card Network

- Acquisition Talks Initiated: Major banks including JPMorgan Chase, Bank of America, Wells Fargo, and PNC Financial Services Group are in early discussions to acquire Fiserv's debit card network, which could significantly enhance their payment processing capabilities while bypassing federal caps on debit card transaction fees if successful.

- Regulatory Impact Analysis: The Durbin Amendment of the 2010 Dodd-Frank Act caps interchange fees for institutions with over $10 billion in assets, but banks owning the underlying network infrastructure can legally avoid these limits, potentially restoring lost revenue streams.

- Fiserv Stock Volatility: Following acquisition rumors, Fiserv's stock rose 4% in after-hours trading; however, it has plummeted approximately 70% from its 2025 highs, reflecting ongoing pressures from intensified competition and frequent executive turnover in the payments sector.

- Market Sentiment Shift: While retail sentiment on Stocktwits remains bearish regarding Fiserv's stock, discussions have surged over 1,000% from last week, indicating increased interest in the usage of its Clover payment system, which may influence future investment decisions.

See More

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

See More

SK Hynix Launches $28 Billion U.S. Listing Amid Chip Demand Surge

- U.S. Listing Initiative: SK Hynix is set to raise approximately $28 billion through its U.S. listing, with plans to issue 17.79 million ADRs representing a tenth of a common share, enabling the company to attract American investors eager for memory chips and semiconductors, thereby enhancing its market competitiveness.

- Competing with Micron: This listing allows SK Hynix to trade alongside rival Micron Technology, which recently announced a $9.3 billion expansion plan on July 4 to increase advanced memory capacity for AI workloads, expected to begin equipment shipments in 2028, intensifying market competition.

- Positive Market Reaction: Following the announcement of SK Hynix's listing, Micron's stock rose about 2% in pre-market trading, indicating optimistic market sentiment towards the semiconductor sector and reflecting investor expectations for SK Hynix's future performance.

- Optimistic Industry Outlook: With the rapid advancement of AI technologies, the demand for memory chips continues to rise, and SK Hynix's listing not only provides financial backing but could significantly enhance its market share and profitability in the coming years, further solidifying its position in the global semiconductor market.

See More

Intel Shares Surge on Potential Apple Partnership

- Stock Surge: Intel Corporation (INTC) shares soared by 21.8% in June, according to S&P Global Market Intelligence, reflecting market confidence in its long-term growth potential, particularly amid rumors of a partnership with Apple.

- Partnership Impact: Although neither Apple nor Intel has confirmed an agreement, President Trump hinted in mid-June that the two companies might collaborate on chip design and manufacturing in the U.S., which would bolster Intel's foundry business and enhance its competitiveness against market leader Taiwan Semiconductor.

- Core Business Prospects: Intel's central processing unit (CPU) business is gaining attention in AI infrastructure development, as the demand for CPUs is expected to rise significantly with the increasing importance of inference, despite graphics processing units (GPUs) currently dominating large language model training.

- Increased Market Recognition: As the market increasingly acknowledges the significance of inference AI spending, Intel's role in CPU manufacturing is likely to be better recognized, and confirmation of a partnership with Apple could further drive stock price appreciation.

See More

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Fiserv Discusses Sale of Payments Business with Major Banks

- Stock Surge: Fiserv shares rallied over 5% after The Wall Street Journal reported discussions with major banks like JPMorgan and Bank of America regarding the sale of its payments infrastructure business, potentially leading to strategic restructuring and enhanced market competitiveness.

- Acquisition Deal: Vertex Pharmaceuticals announced a $10 billion acquisition of Crinetics Pharmaceuticals to expand its product line in rare hormonal disease treatments, although Vertex shares dipped nearly 1%, this deal is expected to strengthen its market position.

- Stock Upgrade: First Solar's stock rose nearly 3% after Deutsche Bank upgraded its rating from neutral to buy, with analysts citing potential trade policy shifts as a reason for investors to buy the dip, boosting market confidence.

- EV Stock Decline: Rivian shares tumbled 9% despite revenue and delivery guidance exceeding market expectations, as the company announced a plan to sell 75 million new shares for a significant capital raise, negatively impacting investor sentiment.

See More

Major Banks Explore Acquisition of Fiserv's Debit Card Network

- Acquisition Talks Initiated: Major banks including JPMorgan Chase, Bank of America, Wells Fargo, and PNC Financial Services Group are in early discussions to acquire Fiserv's debit card network, which could significantly enhance their payment processing capabilities while bypassing federal caps on debit card transaction fees if successful.

- Regulatory Impact Analysis: The Durbin Amendment of the 2010 Dodd-Frank Act caps interchange fees for institutions with over $10 billion in assets, but banks owning the underlying network infrastructure can legally avoid these limits, potentially restoring lost revenue streams.

- Fiserv Stock Volatility: Following acquisition rumors, Fiserv's stock rose 4% in after-hours trading; however, it has plummeted approximately 70% from its 2025 highs, reflecting ongoing pressures from intensified competition and frequent executive turnover in the payments sector.

- Market Sentiment Shift: While retail sentiment on Stocktwits remains bearish regarding Fiserv's stock, discussions have surged over 1,000% from last week, indicating increased interest in the usage of its Clover payment system, which may influence future investment decisions.

See More

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

See More

SK Hynix Launches $28 Billion U.S. Listing Amid Chip Demand Surge

- U.S. Listing Initiative: SK Hynix is set to raise approximately $28 billion through its U.S. listing, with plans to issue 17.79 million ADRs representing a tenth of a common share, enabling the company to attract American investors eager for memory chips and semiconductors, thereby enhancing its market competitiveness.

- Competing with Micron: This listing allows SK Hynix to trade alongside rival Micron Technology, which recently announced a $9.3 billion expansion plan on July 4 to increase advanced memory capacity for AI workloads, expected to begin equipment shipments in 2028, intensifying market competition.

- Positive Market Reaction: Following the announcement of SK Hynix's listing, Micron's stock rose about 2% in pre-market trading, indicating optimistic market sentiment towards the semiconductor sector and reflecting investor expectations for SK Hynix's future performance.

- Optimistic Industry Outlook: With the rapid advancement of AI technologies, the demand for memory chips continues to rise, and SK Hynix's listing not only provides financial backing but could significantly enhance its market share and profitability in the coming years, further solidifying its position in the global semiconductor market.

See More

Intel Shares Surge on Potential Apple Partnership

- Stock Surge: Intel Corporation (INTC) shares soared by 21.8% in June, according to S&P Global Market Intelligence, reflecting market confidence in its long-term growth potential, particularly amid rumors of a partnership with Apple.

- Partnership Impact: Although neither Apple nor Intel has confirmed an agreement, President Trump hinted in mid-June that the two companies might collaborate on chip design and manufacturing in the U.S., which would bolster Intel's foundry business and enhance its competitiveness against market leader Taiwan Semiconductor.

- Core Business Prospects: Intel's central processing unit (CPU) business is gaining attention in AI infrastructure development, as the demand for CPUs is expected to rise significantly with the increasing importance of inference, despite graphics processing units (GPUs) currently dominating large language model training.

- Increased Market Recognition: As the market increasingly acknowledges the significance of inference AI spending, Intel's role in CPU manufacturing is likely to be better recognized, and confirmation of a partnership with Apple could further drive stock price appreciation.

See More