Arm Holdings Stock Soars 210%, Price Target Raised to $360

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 3 days ago

0mins

Source: Fool

- Stock Surge: Driven by rampant enthusiasm for AI stocks, Arm Holdings has seen its stock price soar over 210% since the beginning of 2026, with a 13% increase today, reflecting strong market demand and investor confidence.

- Price Target Increase: Mizuho raised its price target for Arm stock from $290 to $360, based on expectations of strong demand for dynamic random access memory (DRAM) that is anticipated to persist through 2027, further propelling growth in the semiconductor sector.

- Market Potential: Mizuho also highlighted that the total addressable market for high bandwidth memory is expanding, which provides a favorable outlook for Arm's future, indicating that the company will continue to strengthen its competitive position in the semiconductor industry.

- Valuation Considerations: Despite Mizuho's bullish outlook on Arm stock, its current price-to-earnings ratio stands at a steep 356 times, leading investors to consider investing in AI ETFs that include Arm stock to mitigate risk while gaining market exposure.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ARM?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ARM

Wall Street analysts forecast ARM stock price to fall

24 Analyst Rating

19 Buy

4 Hold

1 Sell

Strong Buy

Current: 335.270

Low

120.00

Averages

160.58

High

201.00

Current: 335.270

Low

120.00

Averages

160.58

High

201.00

About ARM

Arm Holdings plc is a United Kingdom-based company. The Company is engaged in the design of central processing units (CPUs) and compute platforms for semiconductor chips. It develops and licenses CPU products and related technology. Its cloud and data center solutions include Arm AGI CPU and Arm Neoverse Compute Subsystems. The Arm Agentic Generalized Infrastructure (AGI) CPU is a production-ready system on a chip (SoC) for artificial intelligence (AI) data centers, delivering compute at scale. The Arm Neoverse Compute Subsystems (CSS) are pre-validated, performance-optimized compute platforms designed to accelerate infrastructure silicon development. The Company's primary markets include smartphone applications, processors and other chips used in mobile phones, consumer electronics, networking equipment, cloud and data center servers, automotive applications, Internet of Things (loT) and other embedded computing devices.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Arm Holdings Sees Significant Growth in CPU Market Share

- Market Share Increase: Arm Holdings has achieved approximately 50% market share in the data center CPU sector, driven by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, which is expected to further solidify its market position.

- Revenue Growth Potential: Arm anticipates that its first-party chip business will generate $15 billion in sales by 2031, potentially yielding $7.5 billion in gross profit, significantly surpassing its current royalty revenue model and demonstrating the success of its strategic transformation.

- Future Market Expectations: Arm projects that the data center CPU market will reach $100 billion by 2031, doubling from $50 billion in 2026, reflecting the rapid growth in AI compute demand, which is further driving the need for CPUs.

- Valuation Challenges: Despite Arm's stock tripling in value since the beginning of the year, the current price-to-earnings ratio of 159 presents a risk of overvaluation for investors, as management's 2031 earnings guidance indicates substantial future growth potential, but high valuations may limit further stock price increases.

See More

Earnings Reports and Tech Conferences This Week

- Earnings Reports: This week, Palo Alto Networks, CrowdStrike, and Broadcom are set to report earnings, with Palo Alto expected to post $0.80 per share on $2.94 billion in revenue, while CrowdStrike is projected to report $1.07 per share on $1.36 billion, highlighting strong market interest in cybersecurity.

- AI-Driven Market Rebound: As AI technology becomes more prevalent, both Palo Alto and CrowdStrike have seen their stock prices rebound to all-time highs, and despite facing high valuation pressures, market expectations for their future performance remain optimistic, making management's outlook a key focus for investors.

- Tech Conference Highlights: Nvidia, Arm, and Microsoft will discuss AI-related topics at tech conferences this week, with Nvidia CEO Jensen Huang scheduled to deliver a keynote on Monday, where he is expected to unveil a new product, potentially personal computers powered by its GPUs, further boosting its market share.

- Labor Market Data: The JOLTS report will be released this week, with expectations of 120,000 new private sector jobs added in May and an unemployment rate holding steady at 4.3%, reflecting economic resilience, and investors will closely monitor these figures for their potential impact on inflation and monetary policy.

See More

Arm Holdings' Surge in Data Center CPU Market

- Market Share Growth: Arm Holdings has achieved a 50% market share in the data center CPU market, driven by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, indicating a strong competitive position.

- Revenue Growth Expectations: Arm anticipates that its proprietary chip sales will reach $15 billion by 2031, potentially generating $7.5 billion in gross profit, showcasing significant growth potential compared to its total gross profit of $4.8 billion in 2025.

- Surge in CPU Demand: With the rise of agentic AI, the demand for CPUs is expected to shift from the current 1:4 CPU to GPU ratio to 1:1 in the future, further driving market demand for Arm's offerings and strengthening its business foundation.

- Valuation Challenges: Despite Arm's stock tripling in value since the beginning of the year, its current P/E ratio stands at 159, presenting a challenge for investors as the high valuation raises concerns about the feasibility of another tripling in stock price, even with substantial growth potential ahead.

See More

Arm Holdings' Rise in Data Center CPU Market

- Market Share Growth: Arm Holdings has captured approximately 50% of the data center CPU market, bolstered by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, indicating a significant shift in competitive dynamics.

- Revenue Growth Outlook: Arm anticipates that its direct chip sales will reach $15 billion by 2031, potentially generating $7.5 billion in gross profit, showcasing a remarkable growth trajectory compared to its gross profit of $4.8 billion in 2025, reflecting strong future demand.

- Surging CPU Demand: As agentic AI workloads increase, the CPU-to-GPU ratio may shift from 1:4 to 1:1, highlighting the value of Arm's designs in meeting this demand, which further enhances its market position.

- Valuation Concerns: Despite Arm's stock tripling in value since the beginning of the year, its current P/E ratio stands at 159, prompting investors to carefully evaluate whether this high valuation is justified, especially given the disparity between the company's growth potential and market expectations.

See More

Comparative Growth Analysis of Qualcomm and Arm

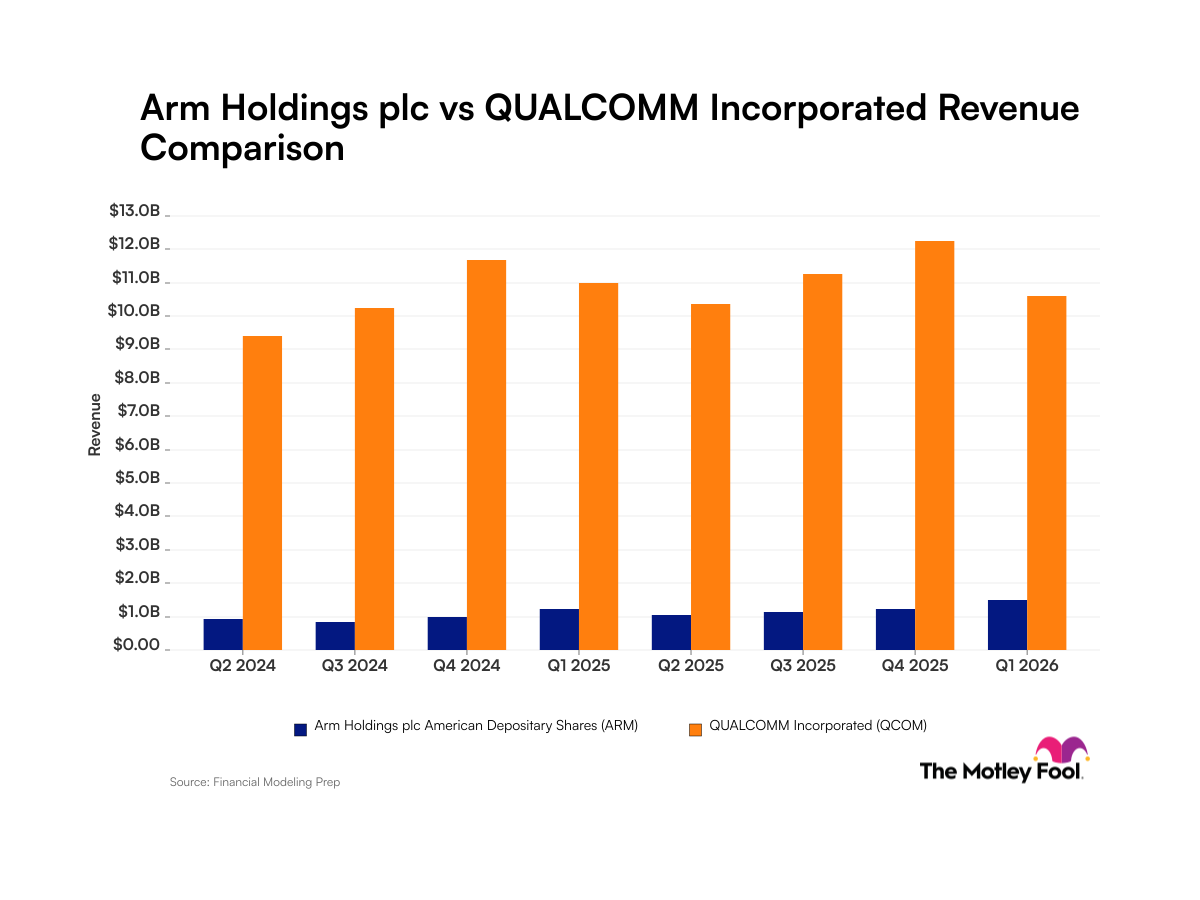

- Revenue Growth Comparison: Arm achieved a 20% year-over-year growth in Q1 2026, while Qualcomm's revenue fell by 3.5%, indicating Arm's stronger growth potential in the market, which may attract investor interest in its future performance.

- Profitability Analysis: Arm's net income margin stands at 21%, while Qualcomm boasts nearly 70%, indicating Qualcomm's strong profitability; however, its slowing revenue growth may impact long-term investment appeal.

- Market Transformation Strategy: Qualcomm is shifting focus from the handset market to sectors like automotive, IoT, and data centers, and if its AI strategy is successfully implemented, it could accelerate revenue growth and narrow the gap with Arm.

- Investor Focus: Despite Arm's stock rising nearly 600% over the past three years, Qualcomm's growth is also noteworthy, especially during its transformation, prompting investors to closely monitor its performance in AI and consumer devices.

See More

AI Drives Growth Opportunities for Arm and Qualcomm

- Arm Revenue Growth: In Q1 2026, Arm's revenue grew 20% year-over-year to $1.5 billion, driven by its licensing and royalty-based business model, resulting in a healthy 21% net income margin, indicating strong market demand and profitability.

- Qualcomm Revenue Fluctuations: Despite Qualcomm's net income margin nearing 70% in Q1, its revenue fell 3.5% year-over-year, reflecting challenges in its strategic shift from the handset market to automotive, IoT, and data center segments, necessitating close monitoring of future growth potential.

- Market Competition Analysis: Over the past three years, Arm's stock has surged nearly 600%, compared to Qualcomm's approximately 123% return, highlighting Arm's increasing competitiveness in the semiconductor industry, particularly in automotive and AI applications.

- Future Outlook: As Qualcomm adjusts its product lineup to seize opportunities in data centers and AI-driven consumer devices, it will be crucial to observe whether it can accelerate revenue growth in the coming years while Arm continues to expand its market share.

See More

Arm Holdings Sees Significant Growth in CPU Market Share

- Market Share Increase: Arm Holdings has achieved approximately 50% market share in the data center CPU sector, driven by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, which is expected to further solidify its market position.

- Revenue Growth Potential: Arm anticipates that its first-party chip business will generate $15 billion in sales by 2031, potentially yielding $7.5 billion in gross profit, significantly surpassing its current royalty revenue model and demonstrating the success of its strategic transformation.

- Future Market Expectations: Arm projects that the data center CPU market will reach $100 billion by 2031, doubling from $50 billion in 2026, reflecting the rapid growth in AI compute demand, which is further driving the need for CPUs.

- Valuation Challenges: Despite Arm's stock tripling in value since the beginning of the year, the current price-to-earnings ratio of 159 presents a risk of overvaluation for investors, as management's 2031 earnings guidance indicates substantial future growth potential, but high valuations may limit further stock price increases.

See More

Earnings Reports and Tech Conferences This Week

- Earnings Reports: This week, Palo Alto Networks, CrowdStrike, and Broadcom are set to report earnings, with Palo Alto expected to post $0.80 per share on $2.94 billion in revenue, while CrowdStrike is projected to report $1.07 per share on $1.36 billion, highlighting strong market interest in cybersecurity.

- AI-Driven Market Rebound: As AI technology becomes more prevalent, both Palo Alto and CrowdStrike have seen their stock prices rebound to all-time highs, and despite facing high valuation pressures, market expectations for their future performance remain optimistic, making management's outlook a key focus for investors.

- Tech Conference Highlights: Nvidia, Arm, and Microsoft will discuss AI-related topics at tech conferences this week, with Nvidia CEO Jensen Huang scheduled to deliver a keynote on Monday, where he is expected to unveil a new product, potentially personal computers powered by its GPUs, further boosting its market share.

- Labor Market Data: The JOLTS report will be released this week, with expectations of 120,000 new private sector jobs added in May and an unemployment rate holding steady at 4.3%, reflecting economic resilience, and investors will closely monitor these figures for their potential impact on inflation and monetary policy.

See More

Arm Holdings' Surge in Data Center CPU Market

- Market Share Growth: Arm Holdings has achieved a 50% market share in the data center CPU market, driven by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, indicating a strong competitive position.

- Revenue Growth Expectations: Arm anticipates that its proprietary chip sales will reach $15 billion by 2031, potentially generating $7.5 billion in gross profit, showcasing significant growth potential compared to its total gross profit of $4.8 billion in 2025.

- Surge in CPU Demand: With the rise of agentic AI, the demand for CPUs is expected to shift from the current 1:4 CPU to GPU ratio to 1:1 in the future, further driving market demand for Arm's offerings and strengthening its business foundation.

- Valuation Challenges: Despite Arm's stock tripling in value since the beginning of the year, its current P/E ratio stands at 159, presenting a challenge for investors as the high valuation raises concerns about the feasibility of another tripling in stock price, even with substantial growth potential ahead.

See More

Arm Holdings' Rise in Data Center CPU Market

- Market Share Growth: Arm Holdings has captured approximately 50% of the data center CPU market, bolstered by the widespread adoption of its efficient Arm architecture by top hyperscalers like Nvidia and Amazon, indicating a significant shift in competitive dynamics.

- Revenue Growth Outlook: Arm anticipates that its direct chip sales will reach $15 billion by 2031, potentially generating $7.5 billion in gross profit, showcasing a remarkable growth trajectory compared to its gross profit of $4.8 billion in 2025, reflecting strong future demand.

- Surging CPU Demand: As agentic AI workloads increase, the CPU-to-GPU ratio may shift from 1:4 to 1:1, highlighting the value of Arm's designs in meeting this demand, which further enhances its market position.

- Valuation Concerns: Despite Arm's stock tripling in value since the beginning of the year, its current P/E ratio stands at 159, prompting investors to carefully evaluate whether this high valuation is justified, especially given the disparity between the company's growth potential and market expectations.

See More

Comparative Growth Analysis of Qualcomm and Arm

- Revenue Growth Comparison: Arm achieved a 20% year-over-year growth in Q1 2026, while Qualcomm's revenue fell by 3.5%, indicating Arm's stronger growth potential in the market, which may attract investor interest in its future performance.

- Profitability Analysis: Arm's net income margin stands at 21%, while Qualcomm boasts nearly 70%, indicating Qualcomm's strong profitability; however, its slowing revenue growth may impact long-term investment appeal.

- Market Transformation Strategy: Qualcomm is shifting focus from the handset market to sectors like automotive, IoT, and data centers, and if its AI strategy is successfully implemented, it could accelerate revenue growth and narrow the gap with Arm.

- Investor Focus: Despite Arm's stock rising nearly 600% over the past three years, Qualcomm's growth is also noteworthy, especially during its transformation, prompting investors to closely monitor its performance in AI and consumer devices.

See More

AI Drives Growth Opportunities for Arm and Qualcomm

- Arm Revenue Growth: In Q1 2026, Arm's revenue grew 20% year-over-year to $1.5 billion, driven by its licensing and royalty-based business model, resulting in a healthy 21% net income margin, indicating strong market demand and profitability.

- Qualcomm Revenue Fluctuations: Despite Qualcomm's net income margin nearing 70% in Q1, its revenue fell 3.5% year-over-year, reflecting challenges in its strategic shift from the handset market to automotive, IoT, and data center segments, necessitating close monitoring of future growth potential.

- Market Competition Analysis: Over the past three years, Arm's stock has surged nearly 600%, compared to Qualcomm's approximately 123% return, highlighting Arm's increasing competitiveness in the semiconductor industry, particularly in automotive and AI applications.

- Future Outlook: As Qualcomm adjusts its product lineup to seize opportunities in data centers and AI-driven consumer devices, it will be crucial to observe whether it can accelerate revenue growth in the coming years while Arm continues to expand its market share.

See More