Analysts Expect a 10% Increase for IYY

ETF Analysis: The iShares Dow Jones U.S. ETF (IYY) has an implied analyst target price of $178.58, indicating a potential upside of 9.53% from its current trading price of $163.04.

Notable Holdings: Key underlying holdings with significant upside potential include First Horizon Corp (10.63% upside), Exelixis Inc (10.12% upside), and Evercore Inc (10.06% upside) based on their respective analyst target prices.

Analyst Target Justification: The article raises questions about whether analysts' target prices are justified or overly optimistic, suggesting that high targets may lead to downgrades if they do not align with current market conditions.

Further Research Needed: Investors are encouraged to conduct additional research to assess the validity of the analysts' targets in light of recent developments in the companies and their industries.

Trade with 70% Backtested Accuracy

Analyst Views on EXEL

About EXEL

About the author

Exelixis Shares Drop After Zanzalintinib Trial Fails to Meet Statistical Significance

- Trial Results: Exelixis announced that its zanzalintinib failed to meet statistical significance in the phase 3 STELLAR-303 trial for metastatic colorectal cancer, leading to a drop in shares during Monday morning trading, indicating uncertainty in the drug's market potential.

- Survival Data: The median overall survival was 15.9 months for patients receiving the zanzalintinib and Roche's Tecentriq combination compared to 12.7 months for those on Bayer's Stivarga, showing a trend but lacking statistical significance, which may affect future market acceptance.

- Other Primary Endpoints: Despite the lack of statistical significance in a specific cohort, Exelixis reported that the combination achieved a statistically significant improvement in overall survival in the intent-to-treat population, providing some support for its upcoming FDA review.

- FDA Review Timeline: The FDA action date for the candidate is set for December 3, and Exelixis also announced a $750 million stock buyback authorization, reflecting the company's proactive capital management approach in the face of clinical challenges.

CABOMETYX Shows Significant Efficacy in Advanced NET Treatment

- Risk Reduction: CABOMETYX significantly reduced the risk of disease progression or death by 74% in non-functional and 60% in functional advanced neuroendocrine tumor (NET) patients, reinforcing its position as a critical treatment option.

- Progression-Free Survival Improvement: In the CABINET trial, the median progression-free survival (PFS) for CABOMETYX was 9.4 months in non-functional NET patients compared to just 3.1 months for placebo, highlighting its effectiveness in disease control.

- Clinical Results Presentation: The results will be presented at the 2026 American Society of Clinical Oncology Annual Meeting, emphasizing CABOMETYX's efficacy across different functional statuses of NET, which may influence future treatment decisions.

- Safety Profile Consistency: The safety profile of CABOMETYX remained consistent with known characteristics, with no new safety signals identified; in functional NET patients, the most common grade 3/4 adverse events were hypertension (21%), indicating its acceptable safety profile.

U.S.-Iran Interim Deal Boosts Stock Market to New Highs

- Market Highs: The stock market surged to new highs on Thursday following reports of an interim U.S.-Iran deal, reflecting investor optimism over reduced geopolitical risks, which positively impacted overall market performance.

- Dell's Strong Earnings: Dell Technologies saw its stock soar after reporting robust earnings, demonstrating the company's strong market performance and profitability, which further bolstered investor confidence in tech stocks.

- Improved Investor Sentiment: The positive market reaction to the U.S.-Iran agreement not only lifted stock indices but may also attract more capital into the market, fostering economic recovery and corporate investment.

- Geopolitical Impact: The interim deal between the U.S. and Iran could alleviate tensions in the Middle East, potentially bringing greater stability to global markets and enhancing investors' risk appetite.

Exelixis to Present New Therapies at ASCO Meeting

- New Drug Presentation: Exelixis will showcase its flagship product CABOMETYX® and investigational oral kinase inhibitor zanzalintinib at the 2026 ASCO Annual Meeting, highlighting ongoing progress in tumor treatment, which is expected to attract investor interest and boost market confidence.

- Clinical Trial Results: CABOMETYX has demonstrated significant efficacy in multiple clinical trials, including studies targeting renal cell carcinoma and neuroendocrine tumors, further solidifying its foundational role in patient care and potentially driving sales growth.

- Strategic Development: Dana T. Aftab, Exelixis' EVP of Research and Development, stated that the presented datasets affirm the company's commitment to improving cancer care standards, which may lay the groundwork for future product line expansions.

- FDA Application Progress: The FDA has accepted the New Drug Application for zanzalintinib, with a target action date of December 3, 2026; if approved, this could open new market opportunities for the company and enhance its competitiveness in cancer treatment.

Exelixis Poised for Doubling Growth Over Next Five Years

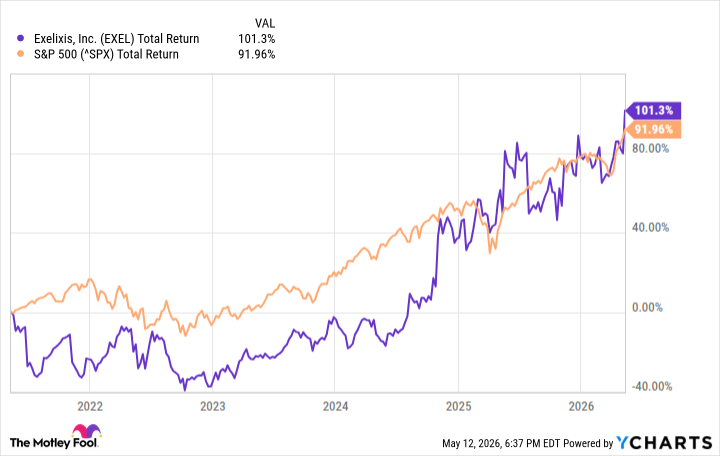

- Strong Stock Performance: Exelixis has seen its stock price rise by 101% over the past five years, outperforming the S&P 500, indicating robust performance in the biotech sector, with potential for another doubling in the next five years attracting investor interest.

- Cabometyx Growth: The company's flagship product, Cabometyx, generated $610.8 million in revenue in Q1 2023, a 10% year-over-year increase, with projected revenue of $2.58 billion for fiscal year 2026, underscoring its strong market position in liver and kidney cancers.

- Next-Gen Drug Potential: Exelixis is developing zanzalintinib, which has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, addressing a significant unmet need with projected peak sales of $5 billion, enhancing the company's growth prospects.

- Diverse Pipeline Strategy: Beyond Cabometyx, Exelixis is testing zanzalintinib for various cancers, including renal cell carcinoma, and successful indications could provide substantial financial support, ensuring continued growth in the competitive oncology market.

Exelixis Shows Significant Future Growth Potential

- Strong Stock Performance: Exelixis shares have risen 101% over the past five years, slightly outperforming the S&P 500, indicating robust performance and investment appeal in the biotech sector.

- Cabometyx Drives Growth: As Exelixis' flagship product, Cabometyx saw a 10% year-over-year revenue increase to $610.8 million in Q1, with projected midpoint revenue of $2.58 billion for FY 2026, reflecting sustained demand and strong sales capabilities in the cancer treatment market.

- New Drug Development Progress: The investigational drug zanzalintinib has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, with potential peak sales of $5 billion, showcasing the company's strategic focus on addressing unmet medical needs.

- Optimistic Future Outlook: Despite the impending patent cliff for Cabometyx, Exelixis has several early-stage pipeline candidates expected to drive financial growth in the coming years, suggesting a bright medium-term outlook with potential for stock doubling by 2031.

Exelixis Shares Drop After Zanzalintinib Trial Fails to Meet Statistical Significance

- Trial Results: Exelixis announced that its zanzalintinib failed to meet statistical significance in the phase 3 STELLAR-303 trial for metastatic colorectal cancer, leading to a drop in shares during Monday morning trading, indicating uncertainty in the drug's market potential.

- Survival Data: The median overall survival was 15.9 months for patients receiving the zanzalintinib and Roche's Tecentriq combination compared to 12.7 months for those on Bayer's Stivarga, showing a trend but lacking statistical significance, which may affect future market acceptance.

- Other Primary Endpoints: Despite the lack of statistical significance in a specific cohort, Exelixis reported that the combination achieved a statistically significant improvement in overall survival in the intent-to-treat population, providing some support for its upcoming FDA review.

- FDA Review Timeline: The FDA action date for the candidate is set for December 3, and Exelixis also announced a $750 million stock buyback authorization, reflecting the company's proactive capital management approach in the face of clinical challenges.

CABOMETYX Shows Significant Efficacy in Advanced NET Treatment

- Risk Reduction: CABOMETYX significantly reduced the risk of disease progression or death by 74% in non-functional and 60% in functional advanced neuroendocrine tumor (NET) patients, reinforcing its position as a critical treatment option.

- Progression-Free Survival Improvement: In the CABINET trial, the median progression-free survival (PFS) for CABOMETYX was 9.4 months in non-functional NET patients compared to just 3.1 months for placebo, highlighting its effectiveness in disease control.

- Clinical Results Presentation: The results will be presented at the 2026 American Society of Clinical Oncology Annual Meeting, emphasizing CABOMETYX's efficacy across different functional statuses of NET, which may influence future treatment decisions.

- Safety Profile Consistency: The safety profile of CABOMETYX remained consistent with known characteristics, with no new safety signals identified; in functional NET patients, the most common grade 3/4 adverse events were hypertension (21%), indicating its acceptable safety profile.

U.S.-Iran Interim Deal Boosts Stock Market to New Highs

- Market Highs: The stock market surged to new highs on Thursday following reports of an interim U.S.-Iran deal, reflecting investor optimism over reduced geopolitical risks, which positively impacted overall market performance.

- Dell's Strong Earnings: Dell Technologies saw its stock soar after reporting robust earnings, demonstrating the company's strong market performance and profitability, which further bolstered investor confidence in tech stocks.

- Improved Investor Sentiment: The positive market reaction to the U.S.-Iran agreement not only lifted stock indices but may also attract more capital into the market, fostering economic recovery and corporate investment.

- Geopolitical Impact: The interim deal between the U.S. and Iran could alleviate tensions in the Middle East, potentially bringing greater stability to global markets and enhancing investors' risk appetite.

Exelixis to Present New Therapies at ASCO Meeting

- New Drug Presentation: Exelixis will showcase its flagship product CABOMETYX® and investigational oral kinase inhibitor zanzalintinib at the 2026 ASCO Annual Meeting, highlighting ongoing progress in tumor treatment, which is expected to attract investor interest and boost market confidence.

- Clinical Trial Results: CABOMETYX has demonstrated significant efficacy in multiple clinical trials, including studies targeting renal cell carcinoma and neuroendocrine tumors, further solidifying its foundational role in patient care and potentially driving sales growth.

- Strategic Development: Dana T. Aftab, Exelixis' EVP of Research and Development, stated that the presented datasets affirm the company's commitment to improving cancer care standards, which may lay the groundwork for future product line expansions.

- FDA Application Progress: The FDA has accepted the New Drug Application for zanzalintinib, with a target action date of December 3, 2026; if approved, this could open new market opportunities for the company and enhance its competitiveness in cancer treatment.

Exelixis Poised for Doubling Growth Over Next Five Years

- Strong Stock Performance: Exelixis has seen its stock price rise by 101% over the past five years, outperforming the S&P 500, indicating robust performance in the biotech sector, with potential for another doubling in the next five years attracting investor interest.

- Cabometyx Growth: The company's flagship product, Cabometyx, generated $610.8 million in revenue in Q1 2023, a 10% year-over-year increase, with projected revenue of $2.58 billion for fiscal year 2026, underscoring its strong market position in liver and kidney cancers.

- Next-Gen Drug Potential: Exelixis is developing zanzalintinib, which has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, addressing a significant unmet need with projected peak sales of $5 billion, enhancing the company's growth prospects.

- Diverse Pipeline Strategy: Beyond Cabometyx, Exelixis is testing zanzalintinib for various cancers, including renal cell carcinoma, and successful indications could provide substantial financial support, ensuring continued growth in the competitive oncology market.

Exelixis Shows Significant Future Growth Potential

- Strong Stock Performance: Exelixis shares have risen 101% over the past five years, slightly outperforming the S&P 500, indicating robust performance and investment appeal in the biotech sector.

- Cabometyx Drives Growth: As Exelixis' flagship product, Cabometyx saw a 10% year-over-year revenue increase to $610.8 million in Q1, with projected midpoint revenue of $2.58 billion for FY 2026, reflecting sustained demand and strong sales capabilities in the cancer treatment market.

- New Drug Development Progress: The investigational drug zanzalintinib has completed phase 3 trials and is awaiting regulatory approval for metastatic colorectal cancer, with potential peak sales of $5 billion, showcasing the company's strategic focus on addressing unmet medical needs.

- Optimistic Future Outlook: Despite the impending patent cliff for Cabometyx, Exelixis has several early-stage pipeline candidates expected to drive financial growth in the coming years, suggesting a bright medium-term outlook with potential for stock doubling by 2031.