American Tower Q1 Earnings Exceed Expectations

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 6 hours ago

0mins

Should l Buy AMT?

Source: seekingalpha

- Strong Financial Performance: American Tower reported a Q1 FFO of $2.84, beating expectations by $0.41, indicating robust profitability and strong market demand for its services.

- Significant Revenue Growth: The company achieved total revenue of $2.74 billion, a 7.0% year-over-year increase, surpassing market expectations by $90 million, reflecting solid performance in the leasing market and an expanding customer base.

- Optimistic Future Outlook: For 2026, total property revenue is projected to range between $10.585 billion and $10.735 billion, with a growth rate of 3.4%, demonstrating the company's confidence in long-term growth prospects.

- Increased Adjusted EBITDA: Adjusted EBITDA is expected to be between $7.195 billion and $7.265 billion, with a year-over-year growth rate of 1.4%, indicating ongoing improvements in cost control and operational efficiency.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy AMT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on AMT

Wall Street analysts forecast AMT stock price to rise

11 Analyst Rating

7 Buy

4 Hold

0 Sell

Moderate Buy

Current: 175.300

Low

185.00

Averages

211.45

High

254.00

Current: 175.300

Low

185.00

Averages

211.45

High

254.00

About AMT

American Tower Corporation is a global real estate investment trust (REIT) and an independent owner, operator and developer of multitenant communications real estate with a portfolio of nearly 150,000 communications sites and a highly interconnected footprint of United States data center facilities. The Company's segments include U.S. & Canada property, Africa & APAC property, Europe property, Latin America property, Data Centers and Services. The Company’s primary business is leasing space on multitenant communications sites to wireless service providers, radio and television broadcast companies, wireless data providers, government agencies and municipalities and tenants in a number of other industries. The Company’s Data Centers segment relates to data center facilities and related assets that it owns and operates in the United States. Its Services segment offers tower-related services in the United States, including AZP, structural and mount analyses, and construction management.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

American Tower Set to Announce Q1 Earnings

- Earnings Announcement: American Tower is set to release its Q1 2023 earnings on April 28 before market open, with consensus estimates predicting a FFO of $2.43 per share and revenue of $2.65 billion, reflecting a 3.5% year-over-year growth, which will provide critical performance insights for investors.

- Tenant Default Impact: Recent tenant defaults have caused a temporary dip in stock price, leading analysts to suggest this presents a buying opportunity, particularly given the company's diversified prospects in 5G and AI, which may attract increased investor interest.

- Rating Upgrade: Mizuho has upgraded American Tower to an “Outperform” rating, primarily due to the undervaluation of its data center business, a move that could bolster market confidence in the company.

- Large-Cap REIT Rankings: Ahead of the Q1 earnings release, large-cap REITs have been ranked by quantitative ratings, indicating American Tower's competitive position within the industry, which may influence investor decisions.

See More

CoreSite Launches 100Gbps Ethernet Virtual Circuits for Enhanced Connectivity

- Bandwidth Expansion: CoreSite introduces 100Gbps Ethernet Virtual Circuits on its Open Cloud Exchange platform, significantly enhancing customers' capabilities for high-bandwidth cloud services and market access, thereby addressing escalating digital demands and strengthening competitive positioning.

- Rapid Service Activation: With OCX, customers can activate services in minutes to establish direct, secure, high-performance connections, enhancing support for critical workloads like AI and real-time analytics, further solidifying CoreSite's leadership in inter-market connectivity.

- Flexible Network Management: Customers can manage and dynamically scale network connections through a single secure self-service interface, avoiding complex manual reconfigurations and infrastructure changes, ensuring flexibility to respond to traffic fluctuations without long-term contracts.

- Government Customer Case: An existing government customer seamlessly interconnects its deployments across CoreSite's Silicon Valley, Northern Virginia, and Orlando data centers using 100G connectivity, simplifying the establishment of high-capacity private connections through OCX, which enhances business resilience and scalability.

See More

American Tower Raises 2026 Forecast After Strong Q1 Results

- Strong Performance: American Tower raised its full-year 2026 forecasts following robust first-quarter results, indicating sustained business performance driven by strong leasing demand from telecom firms and increasing mobile data consumption.

- Infrastructure Investment Surge: U.S. wireless operators are ramping up infrastructure investments to expand network capacity and meet the surging demand for high-speed internet services, providing strong support for American Tower's future growth.

- Cloud and AI Expansion: CEO Steve Vondran highlighted that the accelerating adoption of cloud services and rapid expansion of AI-driven workloads are enhancing the structural growth drivers of the business, signaling sustained investment in high-quality digital infrastructure.

- Optimistic Market Outlook: The company maintains an optimistic outlook for future market conditions, believing that rising mobile data consumption and the proliferation of cloud services will further drive business growth, ensuring its leading position in the digital infrastructure sector.

See More

American Tower: Tenant Default Creates Dip-Buying Opportunity

- Strong Financial Performance: American Tower Corporation (AMT) exceeded market expectations in its latest earnings report, with both revenue and profit surpassing analyst forecasts, showcasing robust growth potential in the 5G and AI sectors, which boosts investor confidence.

- Updated Outlook: The company revised its fiscal year 2026 outlook, anticipating continued growth, reflecting strategic investments in its data center business that will support future revenue increases and further solidify its market position.

- Rating Upgrade: Mizuho upgraded American Tower's rating to Outperform, primarily based on the undervalued potential of its data center business, indicating a positive market sentiment towards its future performance, which may attract more investor interest.

- Tenant Default Impact: Despite facing challenges from tenant defaults, this situation is viewed as a buying opportunity, allowing investors to increase their positions during price dips, thereby benefiting from the company's diversified prospects in 5G and AI over the long term.

See More

American Tower Surpasses Earnings Expectations, Stock Rises

- Earnings Beat: American Tower (AMT) saw a 1.8% premarket stock rise after reporting Q1 adjusted AFFO per share of $2.84, exceeding the $2.75 consensus and up from $2.63 in Q3 and $2.75 in Q4 2024, indicating strong operational performance.

- 2026 Guidance Raised: The company increased its 2026 adjusted FFO per share guidance to $10.90-$11.07 (midpoint $10.99), surpassing the Visible Alpha consensus of $10.98, reflecting positive foreign currency impacts and accelerating revenue growth in Latin America.

- Strong Revenue Growth: Total operating revenue reached $2.74 billion, exceeding the $2.65 billion consensus, remaining flat from the previous quarter but showing significant growth from $2.56 billion a year ago, highlighting robust demand for communication infrastructure.

- Cost Control Improvement: Total operating expenses were $1.50 billion, below the Visible Alpha estimate of $1.46 billion, increasing from $1.31 billion in Q1 2025 but decreasing from $1.58 billion in Q4, demonstrating ongoing efforts in cost management.

See More

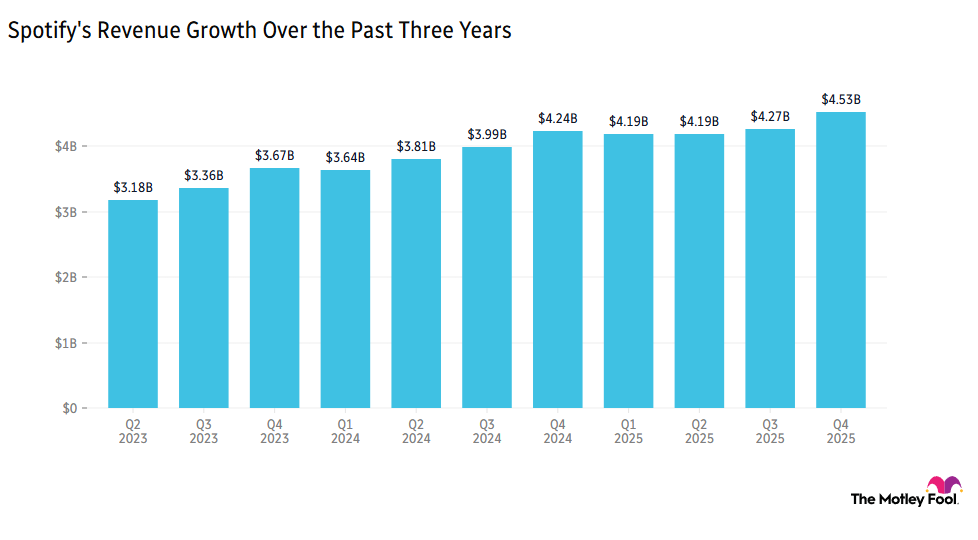

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More

American Tower Set to Announce Q1 Earnings

- Earnings Announcement: American Tower is set to release its Q1 2023 earnings on April 28 before market open, with consensus estimates predicting a FFO of $2.43 per share and revenue of $2.65 billion, reflecting a 3.5% year-over-year growth, which will provide critical performance insights for investors.

- Tenant Default Impact: Recent tenant defaults have caused a temporary dip in stock price, leading analysts to suggest this presents a buying opportunity, particularly given the company's diversified prospects in 5G and AI, which may attract increased investor interest.

- Rating Upgrade: Mizuho has upgraded American Tower to an “Outperform” rating, primarily due to the undervaluation of its data center business, a move that could bolster market confidence in the company.

- Large-Cap REIT Rankings: Ahead of the Q1 earnings release, large-cap REITs have been ranked by quantitative ratings, indicating American Tower's competitive position within the industry, which may influence investor decisions.

See More

CoreSite Launches 100Gbps Ethernet Virtual Circuits for Enhanced Connectivity

- Bandwidth Expansion: CoreSite introduces 100Gbps Ethernet Virtual Circuits on its Open Cloud Exchange platform, significantly enhancing customers' capabilities for high-bandwidth cloud services and market access, thereby addressing escalating digital demands and strengthening competitive positioning.

- Rapid Service Activation: With OCX, customers can activate services in minutes to establish direct, secure, high-performance connections, enhancing support for critical workloads like AI and real-time analytics, further solidifying CoreSite's leadership in inter-market connectivity.

- Flexible Network Management: Customers can manage and dynamically scale network connections through a single secure self-service interface, avoiding complex manual reconfigurations and infrastructure changes, ensuring flexibility to respond to traffic fluctuations without long-term contracts.

- Government Customer Case: An existing government customer seamlessly interconnects its deployments across CoreSite's Silicon Valley, Northern Virginia, and Orlando data centers using 100G connectivity, simplifying the establishment of high-capacity private connections through OCX, which enhances business resilience and scalability.

See More

American Tower Raises 2026 Forecast After Strong Q1 Results

- Strong Performance: American Tower raised its full-year 2026 forecasts following robust first-quarter results, indicating sustained business performance driven by strong leasing demand from telecom firms and increasing mobile data consumption.

- Infrastructure Investment Surge: U.S. wireless operators are ramping up infrastructure investments to expand network capacity and meet the surging demand for high-speed internet services, providing strong support for American Tower's future growth.

- Cloud and AI Expansion: CEO Steve Vondran highlighted that the accelerating adoption of cloud services and rapid expansion of AI-driven workloads are enhancing the structural growth drivers of the business, signaling sustained investment in high-quality digital infrastructure.

- Optimistic Market Outlook: The company maintains an optimistic outlook for future market conditions, believing that rising mobile data consumption and the proliferation of cloud services will further drive business growth, ensuring its leading position in the digital infrastructure sector.

See More

American Tower: Tenant Default Creates Dip-Buying Opportunity

- Strong Financial Performance: American Tower Corporation (AMT) exceeded market expectations in its latest earnings report, with both revenue and profit surpassing analyst forecasts, showcasing robust growth potential in the 5G and AI sectors, which boosts investor confidence.

- Updated Outlook: The company revised its fiscal year 2026 outlook, anticipating continued growth, reflecting strategic investments in its data center business that will support future revenue increases and further solidify its market position.

- Rating Upgrade: Mizuho upgraded American Tower's rating to Outperform, primarily based on the undervalued potential of its data center business, indicating a positive market sentiment towards its future performance, which may attract more investor interest.

- Tenant Default Impact: Despite facing challenges from tenant defaults, this situation is viewed as a buying opportunity, allowing investors to increase their positions during price dips, thereby benefiting from the company's diversified prospects in 5G and AI over the long term.

See More

American Tower Surpasses Earnings Expectations, Stock Rises

- Earnings Beat: American Tower (AMT) saw a 1.8% premarket stock rise after reporting Q1 adjusted AFFO per share of $2.84, exceeding the $2.75 consensus and up from $2.63 in Q3 and $2.75 in Q4 2024, indicating strong operational performance.

- 2026 Guidance Raised: The company increased its 2026 adjusted FFO per share guidance to $10.90-$11.07 (midpoint $10.99), surpassing the Visible Alpha consensus of $10.98, reflecting positive foreign currency impacts and accelerating revenue growth in Latin America.

- Strong Revenue Growth: Total operating revenue reached $2.74 billion, exceeding the $2.65 billion consensus, remaining flat from the previous quarter but showing significant growth from $2.56 billion a year ago, highlighting robust demand for communication infrastructure.

- Cost Control Improvement: Total operating expenses were $1.50 billion, below the Visible Alpha estimate of $1.46 billion, increasing from $1.31 billion in Q1 2025 but decreasing from $1.58 billion in Q4, demonstrating ongoing efforts in cost management.

See More

Spotify's Profit Forecast Falls Short of Expectations

- Ad Revenue Decline: Spotify's ad-supported revenue fell by 5% year-over-year, causing the stock to drop over 9% ahead of market open, reflecting concerns about growth, particularly in major markets like the U.S.

- Disappointing Profit Guidance: While overall revenue grew by 10%, the outlook for operating income and premium subscriber growth for the upcoming quarter disappointed investors, indicating challenges in major markets.

- User Growth Drivers: All key performance indicators met or exceeded expectations, with advanced AI-powered personalization tools and enhancements to the mobile free tier driving accelerated user growth, despite a weak overall growth outlook.

- Strong Market Performance: Since January 2022, Spotify's stock has outperformed the S&P 500 by 78%, demonstrating robust performance under specific market conditions, even as current profit forecasts raise investor concerns.

See More