AbbVie Partners with MLB for Multi-Year Deal

AbbVie announced a multi-year partnership with Major League Baseball, naming AbbVie the Official Pharmaceutical Partner of MLB beginning with the 2026 season. This partnership, a first-of-its-kind for the company, marks the national expansion of Striking Out Cancer - first introduced during the 2025 MLB season through AbbVie's collaboration with the Chicago Cubs, which enters its second year in the 2026 season. This new partnership extends Striking Out Cancer beyond AbbVie's hometown of Chicago to become a league-wide initiative. Throughout the MLB season, AbbVie will donate $20 for every strikeout, up to a maximum donation of $1M per season. This per-strikeout contribution reflects the 20% of the population worldwide who will be diagnosed with cancer before age 75, according to the World Health Organization's Global Cancer Observatory.

Trade with 70% Backtested Accuracy

Analyst Views on ABBV

About ABBV

About the author

AbbVie Advances Dermatology Research at AAD 2026

- Research Presentation: AbbVie will present 24 research abstracts at the 2026 American Academy of Dermatology Annual Meeting, including a significant late-breaking study that underscores the company's leadership in advancing treatment standards for immune-mediated skin diseases, which is expected to reshape future treatment paradigms.

- Long-Term Efficacy Data: The KEEPsAKE 1 Phase 3 trial shows that risankizumab maintains radiographic non-progression in patients with active psoriatic arthritis over five years, indicating its potential to significantly improve patient quality of life.

- Safety Studies: Long-term safety data for upadacitinib in moderate-to-severe atopic dermatitis from three Phase 3 studies reveal six years of results, further solidifying its application prospects and potentially enhancing market acceptance.

- Real-World Evidence: The AD-VISE study provides real-world effectiveness data for upadacitinib across different body regions, highlighting its importance in patient-reported outcomes, which may influence prescribing decisions and treatment choices among physicians.

Eli Lilly Faces Competitive Pressure but Maintains Optimistic Outlook

- Market Performance: Despite leading the weight-loss medicine market, Eli Lilly's shares have fallen 15% this year, raising concerns about intensified competition in its core niche that could erode pricing power and profits.

- Margin Improvement: Since 2020, Eli Lilly's gross and operating margins have significantly improved, with Q4 2025 margins surpassing those of peers, indicating that sales are growing much faster than expenses, reflecting enhanced manufacturing efficiency.

- Manufacturing Capacity Investment: Eli Lilly has invested $55 billion since 2020 to expand its manufacturing capacity, which may hurt profits and margins in the short term but is expected to lower costs and boost capacity, driving significant economies of scale in the long run.

- Artificial Intelligence Initiatives: Eli Lilly has built the largest supercomputer in the pharmaceutical industry with Nvidia's help, aiming to accelerate drug discovery and clinical trial design, with even a 5% reduction in time and costs potentially having a positive impact across the business.

Eli Lilly's Competitive Margin Analysis

- Margin Improvement: Since 2020, Eli Lilly has significantly improved its gross and operating margins, with Q4 2025 margins surpassing those of peers, indicating that sales are growing much faster than expenses, reflecting enhanced drug manufacturing efficiency.

- Competitive Market Pressure: Despite leading the weight-loss drug market, Eli Lilly's shares have fallen 15% this year, raising concerns about potential fierce competition that could erode pricing power and profits in the future.

- Manufacturing Capacity Investment: Eli Lilly has invested $55 billion in expanding its manufacturing capacity since 2020, which may hurt profits in the short term but is expected to lower costs and enhance economies of scale in the long run.

- Artificial Intelligence Applications: Eli Lilly has partnered with Nvidia to build the largest supercomputer in the pharmaceutical industry, aiming to accelerate drug discovery and clinical trial design, with even a 5% reduction in time and costs potentially benefiting the entire business.

AbbVie Increases Dividend by Over 330% Since 2013

- Significant Dividend Growth: AbbVie has increased its dividend by over 330% since 2013, which not only enhances investor income expectations but also boosts the company's market appeal, reflecting its stable cash flow and profitability.

- Strong Revenue Growth: Despite losing patent protection for Humira, AbbVie reported an 8.6% year-over-year revenue increase in 2025, indicating the resilience of its product portfolio and sustained market demand, further solidifying its position in the pharmaceutical industry.

- Robust R&D Pipeline: With over 90 drugs currently in development, AbbVie's extensive pipeline not only secures future revenue growth but also demonstrates the company's ongoing commitment to innovation and strategic planning in drug development.

- Reasonable Valuation Levels: AbbVie’s forward-looking P/E ratio stands at 14, slightly above the five-year average of 13, suggesting that the market's growth expectations are reasonable while providing investors with a relatively attractive entry point.

AbbVie: A Reliable Source of Dividend Income

- Dividend Yield Advantage: AbbVie boasts a dividend yield of 3.38%, significantly higher than the S&P 500 average of 1.1%, making it an ideal choice for income-seeking investors looking to cover living expenses or reinvest.

- Dividend Payment Capability: With a recent dividend of $1.73 per share, translating to an annual payout of $6.92, investors aiming for $10,000 in annual dividends would need to purchase 1,445 shares, costing approximately $296,225, highlighting its reliable dividend payment.

- Consistent Dividend Growth: AbbVie has increased its dividend by over 330% since 2013, and when combined with Abbott's history, it has achieved annual dividend growth for over 25 years, showcasing its appeal as a long-term investment.

- Strong Growth Potential: Despite losing patent protection for its blockbuster drug Humira, AbbVie’s 2025 revenue still grew by 8.6% year-over-year, and its pipeline of over 90 drugs in development indicates promising future growth, further enhancing its investment value.

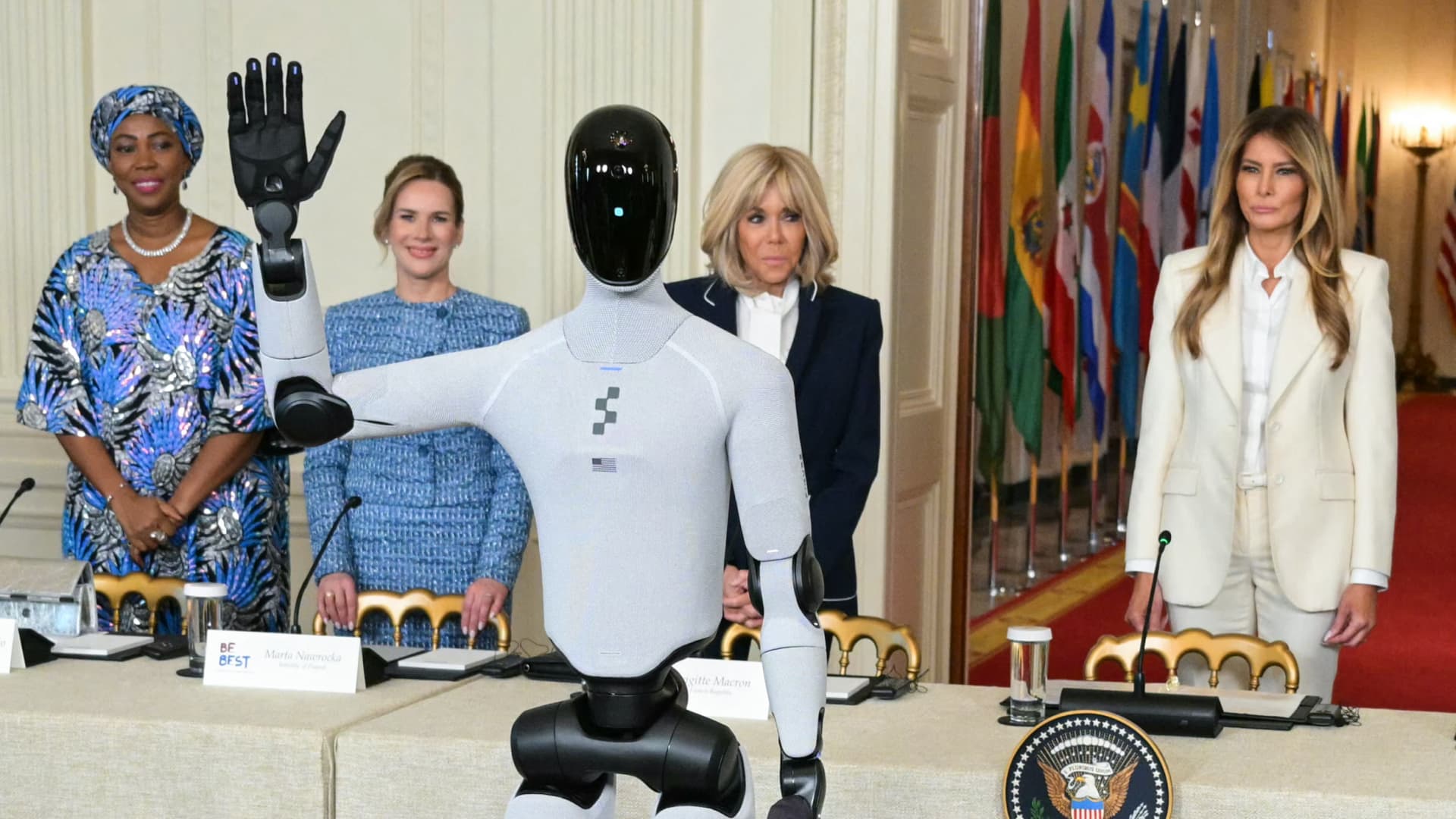

White House Hosts First Humanoid Robot Guest

- High-Profile Showcase: The White House hosted its first humanoid robot, Figure 3, during the Global Coalition Summit, showcasing advancements in U.S. humanoid robotics and highlighting the technology's significance in global tech competition, likely boosting brand recognition for Figure AI.

- Educational Potential: Melania Trump promoted the use of the robot for AI in children's education, suggesting that such robots could become interactive educators at home, which could significantly enhance the technological aspect of family education and its societal implications.

- Funding and Valuation: Figure AI raised over $1 billion in its Series C funding round in September, achieving a post-money valuation of $39 billion, with plans to deploy thousands of robots in homes and logistics, reflecting strong investor enthusiasm for physical AI.

- Legal Risk Awareness: The ongoing lawsuit against Figure AI may be reexamined due to Melania's endorsement, as a former safety head alleged safety concerns regarding the robots, emphasizing the need for safety standards in humanoid robotics development, which could impact the company's reputation and future growth.

AbbVie Advances Dermatology Research at AAD 2026

- Research Presentation: AbbVie will present 24 research abstracts at the 2026 American Academy of Dermatology Annual Meeting, including a significant late-breaking study that underscores the company's leadership in advancing treatment standards for immune-mediated skin diseases, which is expected to reshape future treatment paradigms.

- Long-Term Efficacy Data: The KEEPsAKE 1 Phase 3 trial shows that risankizumab maintains radiographic non-progression in patients with active psoriatic arthritis over five years, indicating its potential to significantly improve patient quality of life.

- Safety Studies: Long-term safety data for upadacitinib in moderate-to-severe atopic dermatitis from three Phase 3 studies reveal six years of results, further solidifying its application prospects and potentially enhancing market acceptance.

- Real-World Evidence: The AD-VISE study provides real-world effectiveness data for upadacitinib across different body regions, highlighting its importance in patient-reported outcomes, which may influence prescribing decisions and treatment choices among physicians.

Eli Lilly Faces Competitive Pressure but Maintains Optimistic Outlook

- Market Performance: Despite leading the weight-loss medicine market, Eli Lilly's shares have fallen 15% this year, raising concerns about intensified competition in its core niche that could erode pricing power and profits.

- Margin Improvement: Since 2020, Eli Lilly's gross and operating margins have significantly improved, with Q4 2025 margins surpassing those of peers, indicating that sales are growing much faster than expenses, reflecting enhanced manufacturing efficiency.

- Manufacturing Capacity Investment: Eli Lilly has invested $55 billion since 2020 to expand its manufacturing capacity, which may hurt profits and margins in the short term but is expected to lower costs and boost capacity, driving significant economies of scale in the long run.

- Artificial Intelligence Initiatives: Eli Lilly has built the largest supercomputer in the pharmaceutical industry with Nvidia's help, aiming to accelerate drug discovery and clinical trial design, with even a 5% reduction in time and costs potentially having a positive impact across the business.

Eli Lilly's Competitive Margin Analysis

- Margin Improvement: Since 2020, Eli Lilly has significantly improved its gross and operating margins, with Q4 2025 margins surpassing those of peers, indicating that sales are growing much faster than expenses, reflecting enhanced drug manufacturing efficiency.

- Competitive Market Pressure: Despite leading the weight-loss drug market, Eli Lilly's shares have fallen 15% this year, raising concerns about potential fierce competition that could erode pricing power and profits in the future.

- Manufacturing Capacity Investment: Eli Lilly has invested $55 billion in expanding its manufacturing capacity since 2020, which may hurt profits in the short term but is expected to lower costs and enhance economies of scale in the long run.

- Artificial Intelligence Applications: Eli Lilly has partnered with Nvidia to build the largest supercomputer in the pharmaceutical industry, aiming to accelerate drug discovery and clinical trial design, with even a 5% reduction in time and costs potentially benefiting the entire business.

AbbVie Increases Dividend by Over 330% Since 2013

- Significant Dividend Growth: AbbVie has increased its dividend by over 330% since 2013, which not only enhances investor income expectations but also boosts the company's market appeal, reflecting its stable cash flow and profitability.

- Strong Revenue Growth: Despite losing patent protection for Humira, AbbVie reported an 8.6% year-over-year revenue increase in 2025, indicating the resilience of its product portfolio and sustained market demand, further solidifying its position in the pharmaceutical industry.

- Robust R&D Pipeline: With over 90 drugs currently in development, AbbVie's extensive pipeline not only secures future revenue growth but also demonstrates the company's ongoing commitment to innovation and strategic planning in drug development.

- Reasonable Valuation Levels: AbbVie’s forward-looking P/E ratio stands at 14, slightly above the five-year average of 13, suggesting that the market's growth expectations are reasonable while providing investors with a relatively attractive entry point.

AbbVie: A Reliable Source of Dividend Income

- Dividend Yield Advantage: AbbVie boasts a dividend yield of 3.38%, significantly higher than the S&P 500 average of 1.1%, making it an ideal choice for income-seeking investors looking to cover living expenses or reinvest.

- Dividend Payment Capability: With a recent dividend of $1.73 per share, translating to an annual payout of $6.92, investors aiming for $10,000 in annual dividends would need to purchase 1,445 shares, costing approximately $296,225, highlighting its reliable dividend payment.

- Consistent Dividend Growth: AbbVie has increased its dividend by over 330% since 2013, and when combined with Abbott's history, it has achieved annual dividend growth for over 25 years, showcasing its appeal as a long-term investment.

- Strong Growth Potential: Despite losing patent protection for its blockbuster drug Humira, AbbVie’s 2025 revenue still grew by 8.6% year-over-year, and its pipeline of over 90 drugs in development indicates promising future growth, further enhancing its investment value.

White House Hosts First Humanoid Robot Guest

- High-Profile Showcase: The White House hosted its first humanoid robot, Figure 3, during the Global Coalition Summit, showcasing advancements in U.S. humanoid robotics and highlighting the technology's significance in global tech competition, likely boosting brand recognition for Figure AI.

- Educational Potential: Melania Trump promoted the use of the robot for AI in children's education, suggesting that such robots could become interactive educators at home, which could significantly enhance the technological aspect of family education and its societal implications.

- Funding and Valuation: Figure AI raised over $1 billion in its Series C funding round in September, achieving a post-money valuation of $39 billion, with plans to deploy thousands of robots in homes and logistics, reflecting strong investor enthusiasm for physical AI.

- Legal Risk Awareness: The ongoing lawsuit against Figure AI may be reexamined due to Melania's endorsement, as a former safety head alleged safety concerns regarding the robots, emphasizing the need for safety standards in humanoid robotics development, which could impact the company's reputation and future growth.