Shopify Expands Share Buyback Program Amid Market Weakness

Shopify Inc. has seen its stock price decline by 5.02%, hitting a 5-day low, as the broader market experiences significant downturns with the Nasdaq-100 down 2.69% and the S&P 500 down 1.36%.

The company's Board has authorized an additional $3 billion for share repurchases, raising the total authorization to $5 billion. This move reflects Shopify's confidence in its future business prospects, particularly during market volatility. The repurchase program is expected to enhance earnings per share and provide flexibility for future investments, despite the current market challenges.

This buyback initiative is likely to bolster investor confidence in Shopify's long-term growth potential, even as the stock faces pressure from broader market conditions. The company's ability to maintain stable cash flow and execute a flexible buyback strategy may position it favorably once market conditions improve.

Trade with 70% Backtested Accuracy

Analyst Views on SHOP

About SHOP

About the author

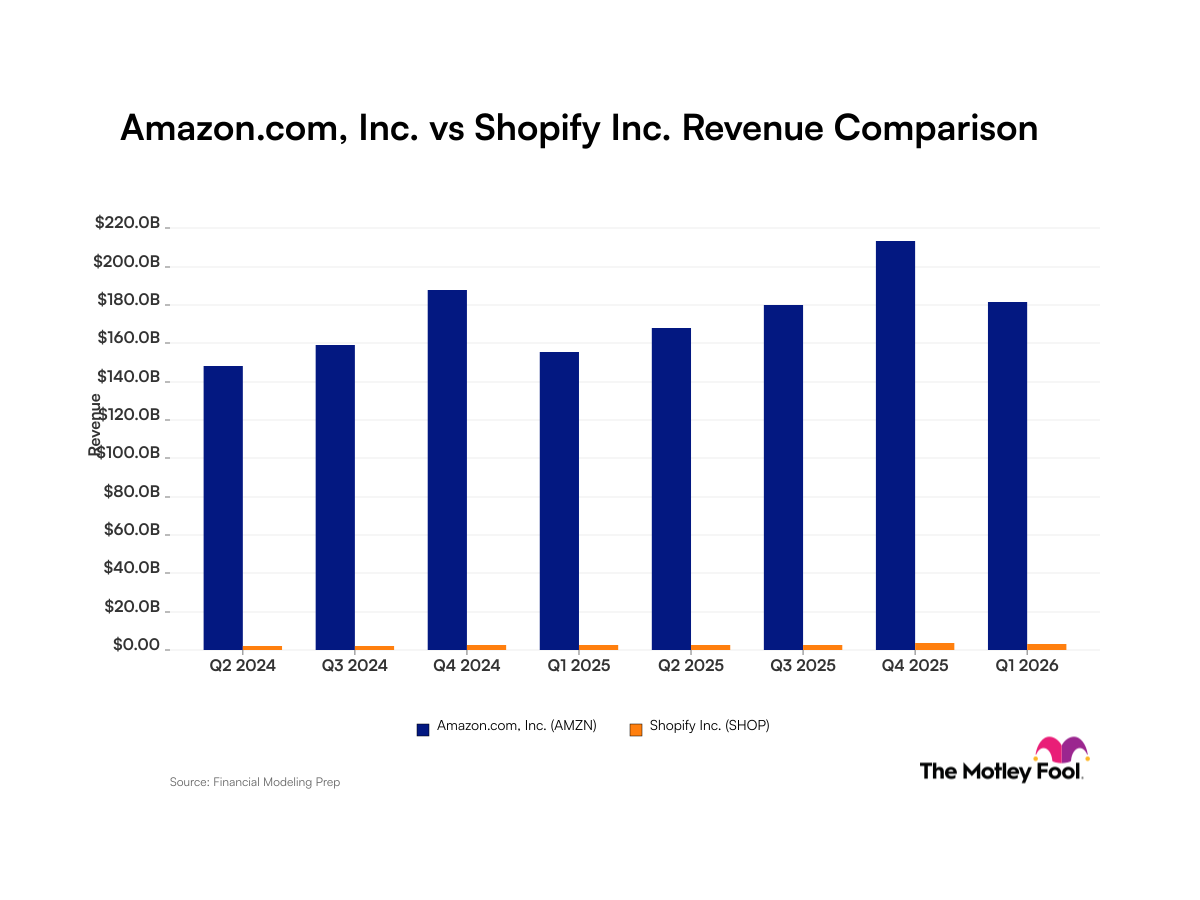

Amazon and Shopify Revenue Comparison

- Amazon Revenue Performance: As of March 31, 2026, Amazon reported a net income margin of 17%, indicating strong performance in the global e-commerce and cloud computing sectors; despite regulatory scrutiny, its revenue scale continues to far exceed Shopify's, suggesting sustained market leadership.

- Shopify Growth Challenges: Shopify's net income margin was -18% in Q1 2026, and while it experienced a 34% year-over-year sales increase, it faced challenges from a copyright lawsuit and temporary system outages, impacting its market competitiveness and investor confidence.

- AI Investment Strategy: Amazon recently issued $25 billion in bonds to fund its AI expansion, a costly move that aims to develop a proprietary AI model, which is expected to provide a competitive edge and further solidify its market position in the future.

- Valuation Discrepancy: Amazon's price-to-sales ratio stands at 4, while Shopify's is at 13, highlighting Amazon's relative value in the current market; Shopify's high valuation has contributed to its stock price falling to a 52-week low of $94 in May, reflecting investor concerns about its future growth prospects.

Key Wall Street Rating Updates on Tuesday

- Deutsche Bank Upgrade: Deutsche Bank upgraded First Solar from hold to buy, citing its compelling fundamentals and strong balance sheet, making it an attractive option for investors in the U.S. panel production sector.

- TD Cowen Initiations: TD Cowen initiated coverage on US Foods, Chefs' Warehouse, and Performance Foods with buy ratings, projecting USFD to achieve 5% revenue growth and 20% EPS growth in the medium term, highlighting its diversified exposure to high-margin subsegments.

- Morgan Stanley on Kingsoft Cloud: Morgan Stanley initiated Kingsoft Cloud as overweight, noting its successful transition from a mid-tier cloud player to an AI cloud provider, with accelerating revenue and improving profitability supported by Xiaomi and Kingsoft Group's ecosystem.

- Goldman Sachs on Rentokil: Goldman Sachs upgraded Rentokil from neutral to buy, expecting steady improvement in organic growth in pest services, aiming for mid-single-digit organic growth by 2027 as the company's growth strategy takes effect.

OUSD Stablecoin Poses Existential Threat to Circle

- Launch of New Stablecoin: A coalition of over 140 financial, tech, and retail giants, including Visa, Mastercard, and Coinbase, has backed the new stablecoin Open USD (OUSD), which poses a direct threat to Circle's USD Coin (USDC), causing Circle's stock to drop by 7.21%.

- Revenue Model Disruption: OUSD challenges Circle's traditional revenue model, which relies on cash and U.S. Treasury holdings, by sharing reserve income with ecosystem partners, potentially leading to a significant decline in Circle's market share and revenue.

- Decentralized Governance Advantage: Unlike USDC, which is managed solely by Circle, OUSD is governed by an independent board, making it more appealing to companies that prefer not to be controlled by a single entity, which could accelerate the loss of USDC users.

- Critical Role of Coinbase: Coinbase's partnership with OUSD raises concerns as it may not renew its revenue-sharing agreement with Circle, further weakening Circle's income sources, prompting investors to closely monitor its future performance.

OUSD Stablecoin Challenges USDC Market Dynamics

- New Stablecoin Launch: A coalition of over 140 financial, tech, and retail giants, including Visa, Mastercard, and BlackRock, has launched the OUSD stablecoin, aiming to challenge Circle's USDC by offering shared yields and zero-cost minting, which could significantly impact USDC's market share.

- Decentralized Governance Advantage: Unlike USDC, which is solely managed by Circle, OUSD is governed by an independent board of partners, appealing to companies that prefer not to be dominated by a single entity, potentially reshaping the stablecoin market landscape.

- Potential Revenue Sharing Risk: Coinbase's partnership with OUSD raises concerns as it may choose not to renew its revenue-sharing agreement with Circle after August 18, which could lead to a substantial decline in Circle's revenue and further impact its stock performance.

- Market Expectations and Valuation Pressure: Analysts project Circle's revenue to nearly double from 2025 to 2028, but the introduction of OUSD may force them to lower growth expectations for Circle, making its current valuation appear overstretched, prompting investors to carefully assess their timing for investment.

Opendoor Stock Drops 21% Amid Housing Market Pressures

- Significant Stock Decline: Opendoor Technologies' stock dropped 21% in the first half of the year according to S&P Global Market Intelligence, indicating a gradual decline after last year's surge driven by social media and retail investors, amidst ongoing pressures in the housing market.

- New CEO's Strategic Shift: Under new CEO Kaz Nejatian, the company has integrated more artificial intelligence to enhance efficiency and introduced a 'cash now, more later' product, which accounted for one-third of acquisition contracts in Q1, showcasing diversification in customer options.

- Increased Home Purchases: In Q1 2026, Opendoor purchased 45% more homes sequentially, with 5,000 under contract, doubling the fourth-quarter figure and marking the highest level since 2022, indicating promising initial results from its strategic overhaul.

- Market Environment Challenges: Despite improvements in contribution margins and faster sales, Opendoor faces the reality of unprofitability and a challenging environment due to high interest rates and ongoing housing market pressures, preventing the stock from reflecting its recovery potential.

Opendoor's New CEO Drives Transformation Progress

- New CEO Appointment: Kaz Nejatian has taken over as CEO of Opendoor, driving the company's transformation amidst a challenging market environment, with the stock dropping 21% in the first half of the year, reflecting investor concerns about future performance.

- Strategy Shift in Home Buying: The new strategy focuses on purchasing quality homes and accelerating sales, with a 45% increase in home purchases in Q1 compared to the previous quarter, reaching 5,000 contracts, the highest since 2022, indicating the company's adaptability under market pressure.

- Improved Market Performance: The percentage of homes on the market for over 120 days decreased from 33% in the previous quarter to 10%, below the market average, demonstrating the company's effectiveness in enhancing sales efficiency, although overall profitability remains a concern.

- Investor Confidence Lacking: Despite initial progress in the transformation, ongoing high interest rates and an unfavorable housing market lead to cautious sentiment from the market regarding Opendoor's future, preventing it from making the list of recommended top stocks for investors.

Amazon and Shopify Revenue Comparison

- Amazon Revenue Performance: As of March 31, 2026, Amazon reported a net income margin of 17%, indicating strong performance in the global e-commerce and cloud computing sectors; despite regulatory scrutiny, its revenue scale continues to far exceed Shopify's, suggesting sustained market leadership.

- Shopify Growth Challenges: Shopify's net income margin was -18% in Q1 2026, and while it experienced a 34% year-over-year sales increase, it faced challenges from a copyright lawsuit and temporary system outages, impacting its market competitiveness and investor confidence.

- AI Investment Strategy: Amazon recently issued $25 billion in bonds to fund its AI expansion, a costly move that aims to develop a proprietary AI model, which is expected to provide a competitive edge and further solidify its market position in the future.

- Valuation Discrepancy: Amazon's price-to-sales ratio stands at 4, while Shopify's is at 13, highlighting Amazon's relative value in the current market; Shopify's high valuation has contributed to its stock price falling to a 52-week low of $94 in May, reflecting investor concerns about its future growth prospects.

Key Wall Street Rating Updates on Tuesday

- Deutsche Bank Upgrade: Deutsche Bank upgraded First Solar from hold to buy, citing its compelling fundamentals and strong balance sheet, making it an attractive option for investors in the U.S. panel production sector.

- TD Cowen Initiations: TD Cowen initiated coverage on US Foods, Chefs' Warehouse, and Performance Foods with buy ratings, projecting USFD to achieve 5% revenue growth and 20% EPS growth in the medium term, highlighting its diversified exposure to high-margin subsegments.

- Morgan Stanley on Kingsoft Cloud: Morgan Stanley initiated Kingsoft Cloud as overweight, noting its successful transition from a mid-tier cloud player to an AI cloud provider, with accelerating revenue and improving profitability supported by Xiaomi and Kingsoft Group's ecosystem.

- Goldman Sachs on Rentokil: Goldman Sachs upgraded Rentokil from neutral to buy, expecting steady improvement in organic growth in pest services, aiming for mid-single-digit organic growth by 2027 as the company's growth strategy takes effect.

OUSD Stablecoin Poses Existential Threat to Circle

- Launch of New Stablecoin: A coalition of over 140 financial, tech, and retail giants, including Visa, Mastercard, and Coinbase, has backed the new stablecoin Open USD (OUSD), which poses a direct threat to Circle's USD Coin (USDC), causing Circle's stock to drop by 7.21%.

- Revenue Model Disruption: OUSD challenges Circle's traditional revenue model, which relies on cash and U.S. Treasury holdings, by sharing reserve income with ecosystem partners, potentially leading to a significant decline in Circle's market share and revenue.

- Decentralized Governance Advantage: Unlike USDC, which is managed solely by Circle, OUSD is governed by an independent board, making it more appealing to companies that prefer not to be controlled by a single entity, which could accelerate the loss of USDC users.

- Critical Role of Coinbase: Coinbase's partnership with OUSD raises concerns as it may not renew its revenue-sharing agreement with Circle, further weakening Circle's income sources, prompting investors to closely monitor its future performance.

OUSD Stablecoin Challenges USDC Market Dynamics

- New Stablecoin Launch: A coalition of over 140 financial, tech, and retail giants, including Visa, Mastercard, and BlackRock, has launched the OUSD stablecoin, aiming to challenge Circle's USDC by offering shared yields and zero-cost minting, which could significantly impact USDC's market share.

- Decentralized Governance Advantage: Unlike USDC, which is solely managed by Circle, OUSD is governed by an independent board of partners, appealing to companies that prefer not to be dominated by a single entity, potentially reshaping the stablecoin market landscape.

- Potential Revenue Sharing Risk: Coinbase's partnership with OUSD raises concerns as it may choose not to renew its revenue-sharing agreement with Circle after August 18, which could lead to a substantial decline in Circle's revenue and further impact its stock performance.

- Market Expectations and Valuation Pressure: Analysts project Circle's revenue to nearly double from 2025 to 2028, but the introduction of OUSD may force them to lower growth expectations for Circle, making its current valuation appear overstretched, prompting investors to carefully assess their timing for investment.

Opendoor Stock Drops 21% Amid Housing Market Pressures

- Significant Stock Decline: Opendoor Technologies' stock dropped 21% in the first half of the year according to S&P Global Market Intelligence, indicating a gradual decline after last year's surge driven by social media and retail investors, amidst ongoing pressures in the housing market.

- New CEO's Strategic Shift: Under new CEO Kaz Nejatian, the company has integrated more artificial intelligence to enhance efficiency and introduced a 'cash now, more later' product, which accounted for one-third of acquisition contracts in Q1, showcasing diversification in customer options.

- Increased Home Purchases: In Q1 2026, Opendoor purchased 45% more homes sequentially, with 5,000 under contract, doubling the fourth-quarter figure and marking the highest level since 2022, indicating promising initial results from its strategic overhaul.

- Market Environment Challenges: Despite improvements in contribution margins and faster sales, Opendoor faces the reality of unprofitability and a challenging environment due to high interest rates and ongoing housing market pressures, preventing the stock from reflecting its recovery potential.

Opendoor's New CEO Drives Transformation Progress

- New CEO Appointment: Kaz Nejatian has taken over as CEO of Opendoor, driving the company's transformation amidst a challenging market environment, with the stock dropping 21% in the first half of the year, reflecting investor concerns about future performance.

- Strategy Shift in Home Buying: The new strategy focuses on purchasing quality homes and accelerating sales, with a 45% increase in home purchases in Q1 compared to the previous quarter, reaching 5,000 contracts, the highest since 2022, indicating the company's adaptability under market pressure.

- Improved Market Performance: The percentage of homes on the market for over 120 days decreased from 33% in the previous quarter to 10%, below the market average, demonstrating the company's effectiveness in enhancing sales efficiency, although overall profitability remains a concern.

- Investor Confidence Lacking: Despite initial progress in the transformation, ongoing high interest rates and an unfavorable housing market lead to cautious sentiment from the market regarding Opendoor's future, preventing it from making the list of recommended top stocks for investors.