No relevant news for Maplebear Inc.

Maplebear Inc. experienced a decline of 4.21% and hit a 20-day low during regular trading.

Despite the positive performance of the Nasdaq-100 and S&P 500, Maplebear's stock fell, indicating a potential sector rotation as investors shift focus to other opportunities in the market. The broader market strength did not translate into gains for Maplebear, suggesting specific challenges or investor sentiment affecting the company.

This decline may raise concerns among investors regarding Maplebear's current market position and future prospects, especially in light of the competitive landscape in the online grocery sector.

Trade with 70% Backtested Accuracy

Analyst Views on CART

About CART

About the author

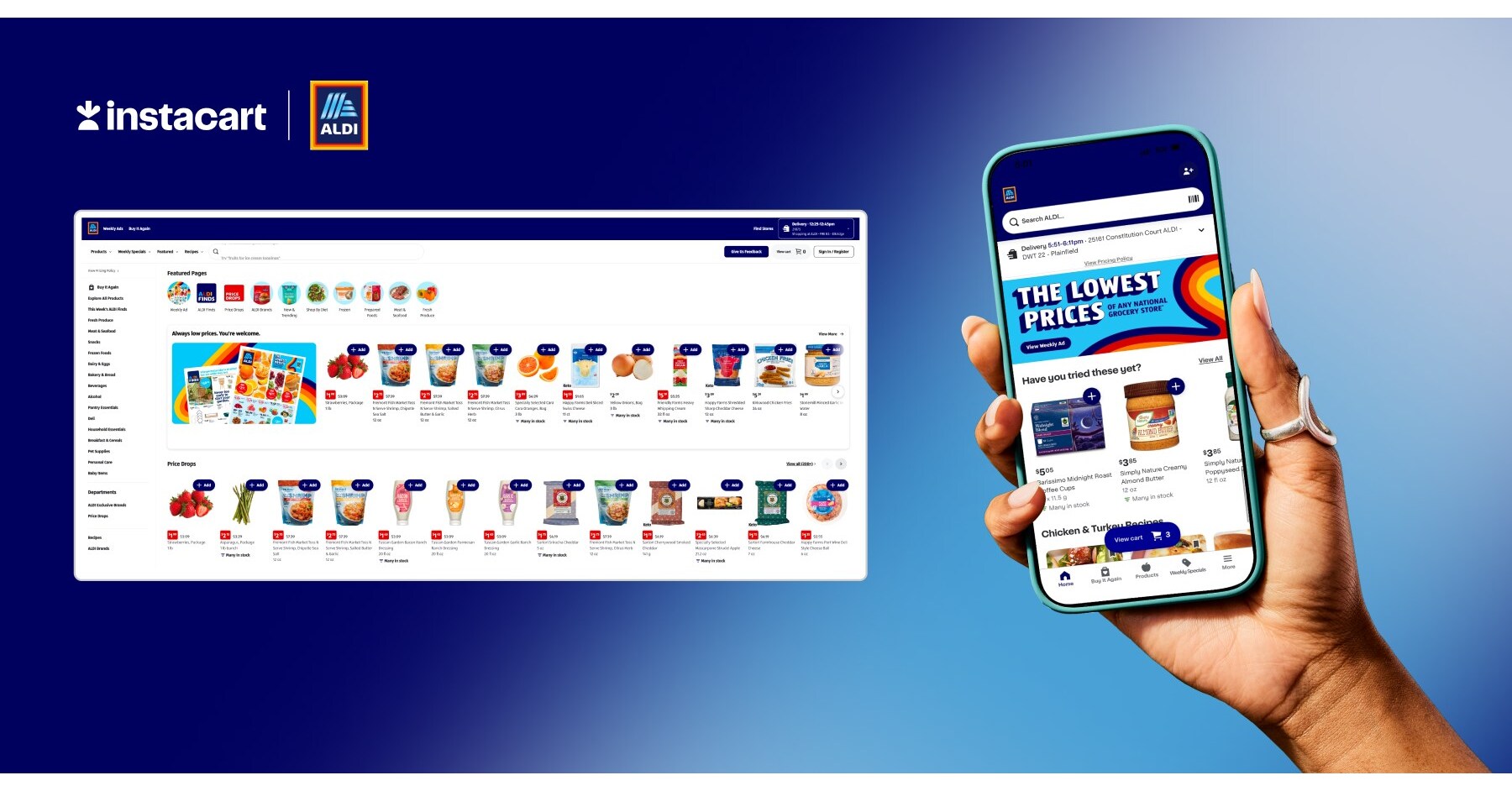

ALDI Partners with Instacart to Enhance Online Shopping Experience

- Partnership Deepening: Instacart's collaboration with ALDI, which began in 2017, has now evolved into an exclusive fulfillment partnership, leveraging the Storefront Pro platform to enhance the online shopping experience and is expected to further drive ALDI's market expansion in the U.S.

- Technology Upgrade: The new website and mobile app provide personalized product recommendations and enhanced product discovery through Instacart's enterprise-grade solutions, allowing customers to enjoy a more convenient shopping experience across ALDI's 2,600+ stores, thereby improving customer satisfaction.

- Rapid Delivery Capability: Since 2019, Instacart's fulfillment solutions have enabled ALDI customers to receive high-quality delivery and curbside pickup in as fast as one hour, ensuring time and cost efficiency for shoppers.

- Market Leadership: According to the 2026 dunnhumby Retailer Preference Index report, ALDI is recognized as the number one in

Instacart Shares Rise 5% Following Jefferies Upgrade to 'Buy'

Stock Performance: Shares of Instacart have increased by 5% following a positive upgrade from Jeffries, which changed its rating to 'Buy'.

Market Reaction: The upgrade reflects a favorable outlook on Instacart's business prospects, influencing investor sentiment and stock valuation.

Analyst Insights: Jeffries' analysts provided insights into the company's potential growth, contributing to the decision to upgrade the stock rating.

Investment Implications: The upgrade may attract more investors to Instacart, potentially leading to further increases in share price and market interest.

Latest Wall Street Rating Updates

- UBS Upgrade: UBS upgrades Adecoagro from Neutral to Buy, raising the price target from $8 to $16.2, indicating the company is poised to benefit from the ongoing Middle East conflict, which is expected to enhance its financial performance.

- HSBC Bullish on Carnival: HSBC upgrades Carnival from Hold to Buy, asserting that the current share price undervalues the resilience of experience-led demand, which is likely to improve the company's market performance in the near future.

- Morgan Stanley Reiterates Meta: Morgan Stanley lowers its price target for Meta from $825 to $775 but maintains it as a top investment idea, suggesting that market sentiment has bottomed out, making it an opportune time to buy.

- Deutsche Bank Upgrades Colgate: Deutsche Bank upgrades Colgate-Palmolive from Hold to Buy, highlighting the company's core business as having long-term investment value and the ability to weather current market volatility effectively.

MAPLEBEAR INC: JEFFERIES UPGRADES TO BUY FROM HOLD; INCREASES TARGET PRICE TO $45 FROM $38

- Company Update: Maple Bear has raised its target price to $45 from $38.

- Investment Strategy: Jeffries is set to buy from Hold, indicating a shift in investment stance.

New NYC Grocery Delivery Laws Impact Instacart Operations

- Regulatory Changes: New York City's law mandates third-party apps to pay a minimum of $21.44 per hour for delivery workers, prompting Instacart to introduce a $5.99 regulatory response fee, which may affect consumer payment willingness and usage frequency.

- Operational Adjustments: Instacart stated that the new law necessitates fundamental changes in its operations, particularly limiting the number of online shoppers to avoid paying for significant idle time, which could impact service efficiency and user experience on the platform.

- Acceptance Rate Metric: To comply with the new regulations, Instacart has implemented a new acceptance rate metric and restricted shoppers to accepting orders one at a time, which may lead to longer delivery times and increased order rejection rates.

- Market Reaction: Following the implementation of the new regulations, Instacart's stock price slid in the final hour of trading, reflecting market concerns about the company's future profitability, especially as consumers may face higher fees and longer delivery times.

OpenAI Launches New Shopping Experience in ChatGPT

- Shopping Experience Upgrade: OpenAI has launched a new shopping experience within ChatGPT, aimed at simplifying product search and comparison by allowing users to upload images or describe items, thereby enhancing user convenience and satisfaction.

- Instant Checkout Withdrawal: Following the failure of the previous Instant Checkout feature, OpenAI has decided to allow merchants to use their own checkout experiences, a shift that will enable greater flexibility in managing transaction processes while focusing on product discovery.

- Merchant Integration Support: OpenAI now allows merchants to share product feeds and promotions, ensuring their products are fully represented within ChatGPT, with retailers like Target, Sephora, and Nordstrom already supporting this new experience, thus enhancing the platform's product coverage.

- App Integration: OpenAI introduced custom app functionality at its annual developer conference, enabling merchants to better control customer experiences and transaction processes through these apps, further enhancing the personalization and convenience of the shopping experience.

ALDI Partners with Instacart to Enhance Online Shopping Experience

- Partnership Deepening: Instacart's collaboration with ALDI, which began in 2017, has now evolved into an exclusive fulfillment partnership, leveraging the Storefront Pro platform to enhance the online shopping experience and is expected to further drive ALDI's market expansion in the U.S.

- Technology Upgrade: The new website and mobile app provide personalized product recommendations and enhanced product discovery through Instacart's enterprise-grade solutions, allowing customers to enjoy a more convenient shopping experience across ALDI's 2,600+ stores, thereby improving customer satisfaction.

- Rapid Delivery Capability: Since 2019, Instacart's fulfillment solutions have enabled ALDI customers to receive high-quality delivery and curbside pickup in as fast as one hour, ensuring time and cost efficiency for shoppers.

- Market Leadership: According to the 2026 dunnhumby Retailer Preference Index report, ALDI is recognized as the number one in

Instacart Shares Rise 5% Following Jefferies Upgrade to 'Buy'

Stock Performance: Shares of Instacart have increased by 5% following a positive upgrade from Jeffries, which changed its rating to 'Buy'.

Market Reaction: The upgrade reflects a favorable outlook on Instacart's business prospects, influencing investor sentiment and stock valuation.

Analyst Insights: Jeffries' analysts provided insights into the company's potential growth, contributing to the decision to upgrade the stock rating.

Investment Implications: The upgrade may attract more investors to Instacart, potentially leading to further increases in share price and market interest.

Latest Wall Street Rating Updates

- UBS Upgrade: UBS upgrades Adecoagro from Neutral to Buy, raising the price target from $8 to $16.2, indicating the company is poised to benefit from the ongoing Middle East conflict, which is expected to enhance its financial performance.

- HSBC Bullish on Carnival: HSBC upgrades Carnival from Hold to Buy, asserting that the current share price undervalues the resilience of experience-led demand, which is likely to improve the company's market performance in the near future.

- Morgan Stanley Reiterates Meta: Morgan Stanley lowers its price target for Meta from $825 to $775 but maintains it as a top investment idea, suggesting that market sentiment has bottomed out, making it an opportune time to buy.

- Deutsche Bank Upgrades Colgate: Deutsche Bank upgrades Colgate-Palmolive from Hold to Buy, highlighting the company's core business as having long-term investment value and the ability to weather current market volatility effectively.

MAPLEBEAR INC: JEFFERIES UPGRADES TO BUY FROM HOLD; INCREASES TARGET PRICE TO $45 FROM $38

- Company Update: Maple Bear has raised its target price to $45 from $38.

- Investment Strategy: Jeffries is set to buy from Hold, indicating a shift in investment stance.

New NYC Grocery Delivery Laws Impact Instacart Operations

- Regulatory Changes: New York City's law mandates third-party apps to pay a minimum of $21.44 per hour for delivery workers, prompting Instacart to introduce a $5.99 regulatory response fee, which may affect consumer payment willingness and usage frequency.

- Operational Adjustments: Instacart stated that the new law necessitates fundamental changes in its operations, particularly limiting the number of online shoppers to avoid paying for significant idle time, which could impact service efficiency and user experience on the platform.

- Acceptance Rate Metric: To comply with the new regulations, Instacart has implemented a new acceptance rate metric and restricted shoppers to accepting orders one at a time, which may lead to longer delivery times and increased order rejection rates.

- Market Reaction: Following the implementation of the new regulations, Instacart's stock price slid in the final hour of trading, reflecting market concerns about the company's future profitability, especially as consumers may face higher fees and longer delivery times.

OpenAI Launches New Shopping Experience in ChatGPT

- Shopping Experience Upgrade: OpenAI has launched a new shopping experience within ChatGPT, aimed at simplifying product search and comparison by allowing users to upload images or describe items, thereby enhancing user convenience and satisfaction.

- Instant Checkout Withdrawal: Following the failure of the previous Instant Checkout feature, OpenAI has decided to allow merchants to use their own checkout experiences, a shift that will enable greater flexibility in managing transaction processes while focusing on product discovery.

- Merchant Integration Support: OpenAI now allows merchants to share product feeds and promotions, ensuring their products are fully represented within ChatGPT, with retailers like Target, Sephora, and Nordstrom already supporting this new experience, thus enhancing the platform's product coverage.

- App Integration: OpenAI introduced custom app functionality at its annual developer conference, enabling merchants to better control customer experiences and transaction processes through these apps, further enhancing the personalization and convenience of the shopping experience.