Invesco Reports Q4 Earnings Beat Expectations with Strong Asset Growth

Invesco's stock fell 5.13% and hit a 5-day low amid broader market gains, with the Nasdaq-100 up 0.80% and the S&P 500 up 0.38%.

Invesco reported a Q4 non-GAAP EPS of $0.62, exceeding expectations by $0.04, which underscores the company's robust profitability and enhances market confidence. The company achieved $1.26 billion in revenue for Q4, reflecting an 8.6% year-over-year increase and surpassing market expectations by $10 million. Additionally, net long-term inflows reached $19.1 billion, primarily driven by ETFs and index funds, showcasing investor confidence in the company's offerings.

Despite the positive earnings report, Invesco's stock price declined, indicating a potential sector rotation as investors may be reallocating funds to other sectors amid the overall market strength.

Trade with 70% Backtested Accuracy

Analyst Views on IVZ

About IVZ

About the author

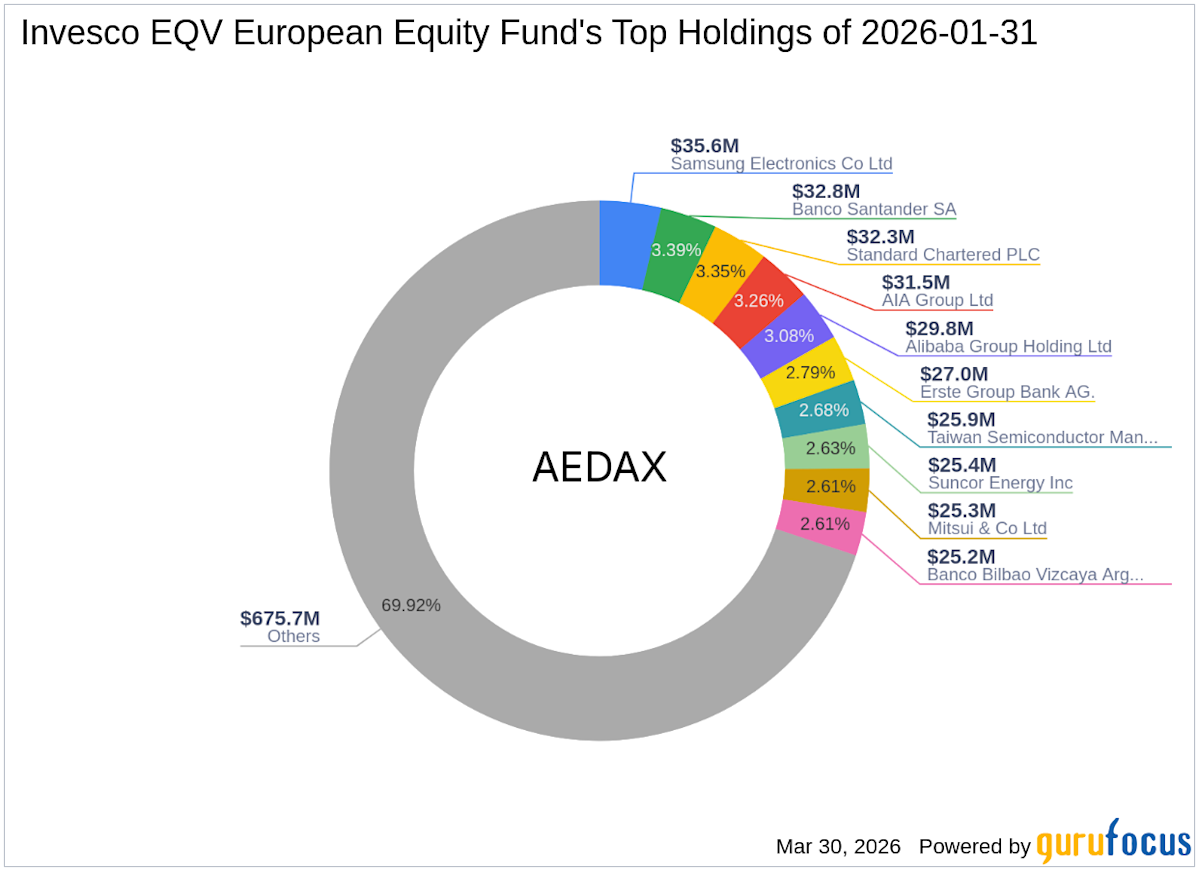

Invesco EQV European Equity Fund's Q1 2026 Portfolio Adjustments

- New Additions: In Q1 2026, Invesco EQV European Equity Fund added 11 stocks, with Taiwan Semiconductor Manufacturing Co Ltd (TPE:2330) being the largest at 469,000 shares, representing 2.68% of the portfolio and valued at NT$25.93 billion, indicating strong confidence in the semiconductor sector.

- Key Position Increases: The fund increased stakes in 9 stocks, notably in Contemporary Amperex Technology Co Ltd (HKSE:03750) by 89,000 shares, a 45.66% increase impacting the portfolio by 0.57%, valued at HK$17.71 million, reflecting a focus on battery technology.

- Complete Exits: In Q1 2026, the fund completely exited 9 holdings, including Prosus NV (XAMS:PRX) and Sumitomo Forestry Co Ltd (TSE:1911), resulting in -2.26% and -1.66% impacts on the portfolio respectively, showcasing a cautious stance on these investments.

- Position Reductions: The fund reduced positions in 35 stocks, with Alibaba Group Holding Ltd (HKSE:09988) seeing a reduction of 386,600 shares, a 21.64% decrease impacting the portfolio by -0.9%, reflecting a strategic response to market volatility.

Victory Capital Withdraws Bid for Janus Henderson Amid Market Dynamics

- Acquisition Dynamics: Victory Capital's withdrawal from the bid for Janus Henderson has led to its acquisition by General Catalyst and Trian, indicating a critical price discovery moment in the asset management industry, with the deal priced at a modest 11.6x forward earnings estimates.

- Fee Pressure: Asset management fees are trending lower, with ETFs providing a compelling low-cost alternative for many investors; however, the bidding war for Janus Henderson suggests that some asset management firms may be undervalued, capturing market attention.

- Invesco's Market Position: As a heavyweight in the industry, Invesco manages $2.26 trillion in assets, with its QQQ Trust essentially acting as a money-printing machine, and its current trading price is significantly below what a private equity firm would pay to build the business from scratch, highlighting its strong competitive moat.

- Options Trading Strategy: By structuring options trades to offset the dividend one would forgo by not purchasing the stock, investors can effectively acquire IVZ shares at about a 9% discount if the stock falls below $22, while also positioning for a maximum payout of $2 if the stock benefits from the JHG deal, showcasing a flexible investment strategy.

Invesco Partners with Superstate to Manage USTB Fund

- Collaboration Background: Invesco has partnered with Superstate to become the investment manager of the Superstate Short Duration US Treasury Fund (USTB), marking the first time an independent asset manager has leveraged Superstate's tokenization infrastructure, which is expected to enhance market acceptance of digital asset products.

- Asset Scale: USTB currently manages over $967 million in assets, ranking among the top five tokenized U.S. treasury funds globally, with Invesco's Global Liquidity team taking over day-to-day management, thereby strengthening its market position.

- Market Impact: Since its launch in early 2024, USTB has onboarded over 150 institutional investors and processed billions of dollars in transactions, demonstrating market validation of its institutional-grade infrastructure, and Invesco's involvement will expand its market reach.

- Future Outlook: Following the expected transition of management in Q2 2026, USTB will be renamed Invesco Short Duration US Government Securities Fund while retaining the same ticker and smart contracts, further promoting the adoption and efficiency of tokenized products.

Federal Reserve's Rate Pause Attracts Short-Duration Asset Investments

- Attraction of Short-Term Assets: The Federal Reserve's decision to maintain the federal funds rate between 3.5% and 3.75% and the expectation of one rate cut this year keeps yields on short-term Treasuries and high-quality bonds at levels not seen in many years, drawing investor interest towards short-duration assets.

- Surge in Bond ETF Inflows: Ultra-short bond ETFs have seen $85 billion in inflows over the past 12 months, making them the leading category for new investments among fixed-income ETFs, indicating a strong market appetite for short-term debt instruments.

- Popularity of Bank Loans: Bank loans, also known as senior loans, have gained traction among retail investors due to their high yields and increased ETF issuance, with the T. Rowe Price Floating Rate ETF offering a 30-day SEC yield of 6.51%, showcasing their appeal.

- Stable Cash Asset Yields: Although the annual percentage rates for money market funds have fallen below 4%, they still provide relatively stable income, with the Crane 100 list showing an annualized seven-day yield of 3.47%, offering investors a safe income option.

Invesco Supports Tax-Advantaged Child Savings Accounts

- Employee Benefit Enhancement: Invesco announces its commitment to match the U.S. government's $1,000 contribution for eligible newborns, effectively doubling the initial account size and enhancing financial resilience for employees' families, reflecting the company's focus on employee welfare.

- Long-Term Savings Advocacy: By supporting the newly established Section 530A Accounts, Invesco aims to encourage employees and their families to cultivate saving and investing habits from an early age, promoting future financial wellness in line with the company's mission to help people invest for a better future.

- Financial Education Support: Invesco has long been committed to promoting financial education and responsible investing, believing that early exposure to saving and investing can significantly improve financial outcomes, especially when paired with diversified investment solutions and strong investor education.

- Global Asset Management Strength: As of the end of 2025, Invesco manages $2.2 trillion in assets, and with its broad range of investment capabilities and global scale, the company is well-positioned to help retail and institutional investors navigate challenges and discover new possibilities for success.

Invesco Supports Tax-Advantaged Child Savings Accounts

- Employee Benefit Enhancement: Invesco commits to match the U.S. government's $1,000 contribution to child savings accounts for eligible newborns of its employees, effectively doubling the initial account size and enhancing financial resilience for families.

- Long-Term Investment Habits: By supporting these child savings accounts, Invesco aims to foster long-term saving and investment habits from an early age, encouraging the next generation's participation in capital markets and improving future financial health.

- Advocacy for Financial Education: Invesco has long supported financial education and responsible investing, believing that early exposure to saving and investing can significantly improve financial outcomes, especially when paired with diversified investment solutions and robust investor education.

- Global Asset Management Strength: As of the end of 2025, Invesco manages $2.2 trillion in assets, and with its broad investment capabilities and global scale, the firm is well-positioned to help retail and institutional investors navigate challenges and discover new opportunities for success.

Invesco EQV European Equity Fund's Q1 2026 Portfolio Adjustments

- New Additions: In Q1 2026, Invesco EQV European Equity Fund added 11 stocks, with Taiwan Semiconductor Manufacturing Co Ltd (TPE:2330) being the largest at 469,000 shares, representing 2.68% of the portfolio and valued at NT$25.93 billion, indicating strong confidence in the semiconductor sector.

- Key Position Increases: The fund increased stakes in 9 stocks, notably in Contemporary Amperex Technology Co Ltd (HKSE:03750) by 89,000 shares, a 45.66% increase impacting the portfolio by 0.57%, valued at HK$17.71 million, reflecting a focus on battery technology.

- Complete Exits: In Q1 2026, the fund completely exited 9 holdings, including Prosus NV (XAMS:PRX) and Sumitomo Forestry Co Ltd (TSE:1911), resulting in -2.26% and -1.66% impacts on the portfolio respectively, showcasing a cautious stance on these investments.

- Position Reductions: The fund reduced positions in 35 stocks, with Alibaba Group Holding Ltd (HKSE:09988) seeing a reduction of 386,600 shares, a 21.64% decrease impacting the portfolio by -0.9%, reflecting a strategic response to market volatility.

Victory Capital Withdraws Bid for Janus Henderson Amid Market Dynamics

- Acquisition Dynamics: Victory Capital's withdrawal from the bid for Janus Henderson has led to its acquisition by General Catalyst and Trian, indicating a critical price discovery moment in the asset management industry, with the deal priced at a modest 11.6x forward earnings estimates.

- Fee Pressure: Asset management fees are trending lower, with ETFs providing a compelling low-cost alternative for many investors; however, the bidding war for Janus Henderson suggests that some asset management firms may be undervalued, capturing market attention.

- Invesco's Market Position: As a heavyweight in the industry, Invesco manages $2.26 trillion in assets, with its QQQ Trust essentially acting as a money-printing machine, and its current trading price is significantly below what a private equity firm would pay to build the business from scratch, highlighting its strong competitive moat.

- Options Trading Strategy: By structuring options trades to offset the dividend one would forgo by not purchasing the stock, investors can effectively acquire IVZ shares at about a 9% discount if the stock falls below $22, while also positioning for a maximum payout of $2 if the stock benefits from the JHG deal, showcasing a flexible investment strategy.

Invesco Partners with Superstate to Manage USTB Fund

- Collaboration Background: Invesco has partnered with Superstate to become the investment manager of the Superstate Short Duration US Treasury Fund (USTB), marking the first time an independent asset manager has leveraged Superstate's tokenization infrastructure, which is expected to enhance market acceptance of digital asset products.

- Asset Scale: USTB currently manages over $967 million in assets, ranking among the top five tokenized U.S. treasury funds globally, with Invesco's Global Liquidity team taking over day-to-day management, thereby strengthening its market position.

- Market Impact: Since its launch in early 2024, USTB has onboarded over 150 institutional investors and processed billions of dollars in transactions, demonstrating market validation of its institutional-grade infrastructure, and Invesco's involvement will expand its market reach.

- Future Outlook: Following the expected transition of management in Q2 2026, USTB will be renamed Invesco Short Duration US Government Securities Fund while retaining the same ticker and smart contracts, further promoting the adoption and efficiency of tokenized products.

Federal Reserve's Rate Pause Attracts Short-Duration Asset Investments

- Attraction of Short-Term Assets: The Federal Reserve's decision to maintain the federal funds rate between 3.5% and 3.75% and the expectation of one rate cut this year keeps yields on short-term Treasuries and high-quality bonds at levels not seen in many years, drawing investor interest towards short-duration assets.

- Surge in Bond ETF Inflows: Ultra-short bond ETFs have seen $85 billion in inflows over the past 12 months, making them the leading category for new investments among fixed-income ETFs, indicating a strong market appetite for short-term debt instruments.

- Popularity of Bank Loans: Bank loans, also known as senior loans, have gained traction among retail investors due to their high yields and increased ETF issuance, with the T. Rowe Price Floating Rate ETF offering a 30-day SEC yield of 6.51%, showcasing their appeal.

- Stable Cash Asset Yields: Although the annual percentage rates for money market funds have fallen below 4%, they still provide relatively stable income, with the Crane 100 list showing an annualized seven-day yield of 3.47%, offering investors a safe income option.

Invesco Supports Tax-Advantaged Child Savings Accounts

- Employee Benefit Enhancement: Invesco announces its commitment to match the U.S. government's $1,000 contribution for eligible newborns, effectively doubling the initial account size and enhancing financial resilience for employees' families, reflecting the company's focus on employee welfare.

- Long-Term Savings Advocacy: By supporting the newly established Section 530A Accounts, Invesco aims to encourage employees and their families to cultivate saving and investing habits from an early age, promoting future financial wellness in line with the company's mission to help people invest for a better future.

- Financial Education Support: Invesco has long been committed to promoting financial education and responsible investing, believing that early exposure to saving and investing can significantly improve financial outcomes, especially when paired with diversified investment solutions and strong investor education.

- Global Asset Management Strength: As of the end of 2025, Invesco manages $2.2 trillion in assets, and with its broad range of investment capabilities and global scale, the company is well-positioned to help retail and institutional investors navigate challenges and discover new possibilities for success.

Invesco Supports Tax-Advantaged Child Savings Accounts

- Employee Benefit Enhancement: Invesco commits to match the U.S. government's $1,000 contribution to child savings accounts for eligible newborns of its employees, effectively doubling the initial account size and enhancing financial resilience for families.

- Long-Term Investment Habits: By supporting these child savings accounts, Invesco aims to foster long-term saving and investment habits from an early age, encouraging the next generation's participation in capital markets and improving future financial health.

- Advocacy for Financial Education: Invesco has long supported financial education and responsible investing, believing that early exposure to saving and investing can significantly improve financial outcomes, especially when paired with diversified investment solutions and robust investor education.

- Global Asset Management Strength: As of the end of 2025, Invesco manages $2.2 trillion in assets, and with its broad investment capabilities and global scale, the firm is well-positioned to help retail and institutional investors navigate challenges and discover new opportunities for success.