Valaris Q4 Earnings Exceed Expectations with Strong Revenue Guidance

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 20 2026

0mins

Should l Buy VAL?

Source: seekingalpha

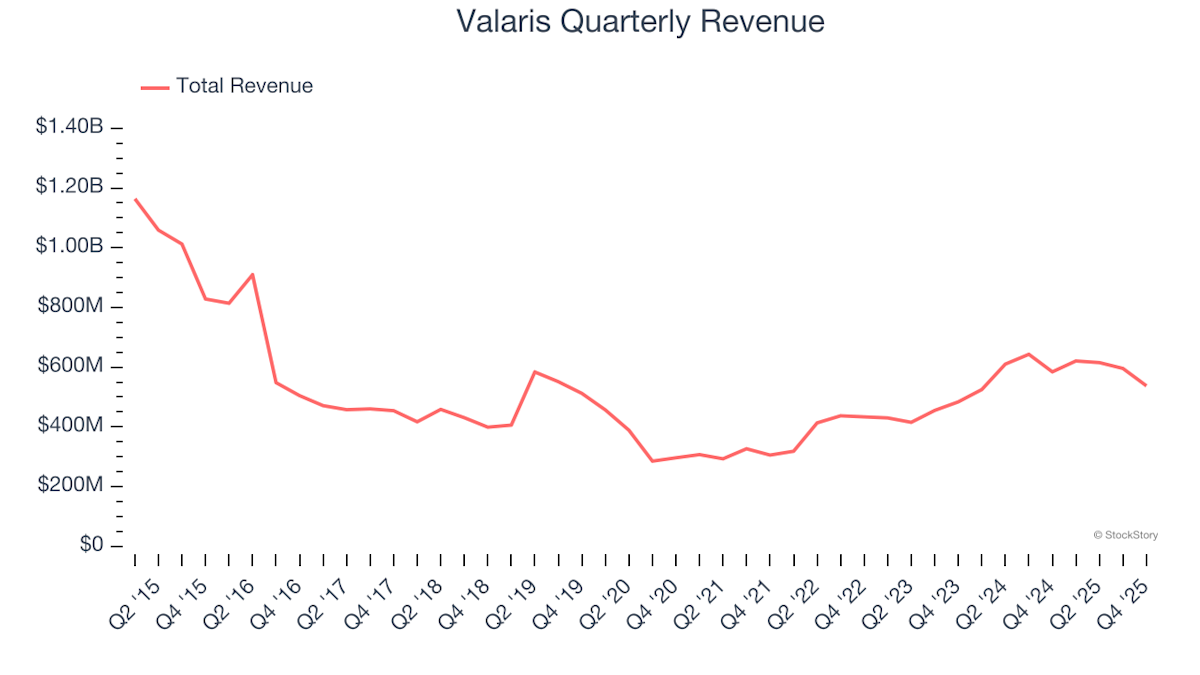

- Earnings Highlights: Valaris reported Q4 EPS of $10.26, significantly surpassing the consensus estimate of $0.84, indicating strong profitability despite an 8% year-over-year revenue decline to $537.4 million, which exceeded expectations by $42.99 million, showcasing the company's resilience in challenging conditions.

- 2026 Financial Guidance: The company projects total operating revenues for FY 2026 to be between $2.125 billion and $2.205 billion, slightly above the consensus of $2.12 billion, reflecting management's confidence in future growth, particularly in light of the pending merger with Transocean.

- Adjusted EBITDA Outlook: Valaris anticipates adjusted EBITDA for FY 2026 to range from $485 million to $565 million, excluding costs associated with the upcoming Transocean merger, indicating strong profitability potential post-merger.

- Capital Expenditure Plans: The company plans to invest between $425 million and $475 million in capital expenditures for FY 2026, alongside expected upfront payments of approximately $110 million from customers for contract-specific upgrades, providing essential funding for future growth initiatives.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy VAL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on VAL

Wall Street analysts forecast VAL stock price to fall

6 Analyst Rating

1 Buy

4 Hold

1 Sell

Hold

Current: 94.540

Low

49.00

Averages

56.50

High

65.00

Current: 94.540

Low

49.00

Averages

56.50

High

65.00

About VAL

Valaris Limited is an offshore contract drilling company, which is engaged in providing offshore contract drilling services to the international oil and gas industry with operations on the offshore market on approximately six continents. The Company operates a rig fleet of ultra-deepwater drill ships, semisubmersibles, and shallow water jackups. The Company operates through four segments: Floaters, which includes its drill ships and semisubmersible rigs; Jackups; ARO, and Other, which consists of management services on rigs owned by third parties and the activities associated with its arrangements with ARO. Its customers include many of the offshore exploration and production companies, including integrated energy companies, national oil companies, and independent operators. The Company owns approximately 52 rigs, including 13 drill ships, four dynamically positioned semisubmersible rigs, one moored semisubmersible rig, and 34 jackup rigs.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Crude Oil Price Drop Triggers Stock Market Volatility

- Significant Oil Price Drop: Brent crude oil prices fell over 10% to below $90 per barrel, primarily due to a 10-day ceasefire between Israel and Lebanon and optimism surrounding U.S.-Iran negotiations, which alleviated market fears of supply disruptions and reduced the risk premium on oil prices.

- Oilfield Services Companies Impacted: Transocean's stock fell 6.1%, Valaris dropped 6%, and RPC decreased by 8.5%, as these companies typically face pressure to cut capital expenditures when oil prices decline, leading to canceled contracts and idle equipment that negatively affect short-term performance.

- Market Overreaction: The stock market's reaction to falling oil prices may be overly dramatic, and while there could be buying opportunities for high-quality stocks in the short term, the volatility in the oilfield services sector necessitates careful risk assessment by investors.

- RPC Stock Performance: RPC has risen 19.3% since the beginning of the year, yet at $6.60 per share, it remains 9.9% below its 52-week high of $7.32, indicating a cautious market sentiment regarding its future performance, prompting investors to monitor its long-term growth potential.

See More

Valaris Shareholders Enjoy Windfall Amid Stock Surge

- Stock Surge: Valaris's stock price has surged by 90.6% over the past six months, reaching $91.79 per share; however, analysts suggest that this might not be the best time to invest, potentially influencing investor decisions.

- Long-Term Revenue Growth: The company has achieved a 10.7% compounded annual growth rate over the last five years, slightly above the industry average, indicating a good fit with customer needs, but short-term performance in a cyclical industry may not guarantee long-term stability.

- Low Gross Margin Issue: With an average gross margin of 21% over the past five years, Valaris ranks at the bottom of its sector, suggesting weak competitiveness in high commodity price environments, which could impact future profitability.

- Cash Burn Concerns: Valaris's free cash flow margin averaged negative 5.7%, indicating a cash burn of $5.68 for every $100 in revenue, which limits its ability to return capital to investors and increases financial risk.

See More

Valaris to Release Q1 2026 Earnings After Market Close

- Earnings Release Schedule: Valaris plans to issue its Q1 2026 earnings report after the NYSE closes on May 4, 2026, reflecting the company's ongoing commitment to transparency and information disclosure.

- Business Combination Update: Following the announcement of its business combination with Transocean Ltd. on February 9, 2026, Valaris will not hold future earnings conference calls or provide forward-looking guidance, indicating a strategic shift during the integration process.

- Information Disclosure Channels: Valaris utilizes its website to disclose material information to investors, customers, and employees, ensuring timely access to company updates and enhancing communication efficiency with stakeholders.

- Industry Leadership Position: As a leader in offshore drilling services, Valaris operates a high-quality rig fleet across various water depths and geographies, demonstrating its unwavering commitment to safety, operational excellence, and customer satisfaction.

See More

Foreign Energy Stocks Shine in 2026 YTD Performance

- YTD Performance: Tenaz Energy Corp. leads with a remarkable 138.57% year-to-date gain, showcasing its strong position in the international energy market, which has attracted investor interest and boosted its market capitalization.

- Market Comparison: In contrast to the volatility faced by domestic energy stocks, foreign energy companies have excelled due to rising commodity prices and favorable geopolitical conditions, indicating a growing investor confidence in international markets.

- Diverse Sectors: The top ten foreign energy stocks include companies from Canada, Brazil, and Norway across various subsectors, such as oil and gas exploration and offshore drilling services, highlighting the diversity and potential of the global energy market.

- Strong Growth: Companies like Valaris, Equinor ASA, and Spartan Delta have achieved over 74% year-to-date gains, reflecting their competitiveness and profitability in the current market environment.

See More

Valaris and Halliburton Partner with Petronas for Suriname Offshore Development

- Strategic Collaboration: Valaris (VAL) and Halliburton (HAL) have entered into a strategic collaboration agreement with Petronas to leverage Valaris' offshore drilling expertise, Petronas' project stewardship, and Halliburton's digital solutions for the development of Suriname's offshore assets, enhancing competitive positioning in the region.

- Resource Integration Advantage: This partnership aims to capitalize on the rich resources of the Guyana-Suriname Basin, which continues to experience strong exploration success and development activity, potentially providing long-term business opportunities for operators and service providers, thereby driving industry growth.

- Contract Extension: Valaris (VAL) secured a 1,064-day contract extension with Petrobras (PBR) for the Valaris DS-4 drillship starting November 2027, adding approximately $447 million to its contract backlog, which strengthens the company's financial stability.

- Optimistic Market Outlook: With rising oil prices, Halliburton (HAL) is likely to revise its earnings estimates upward, and combined with Valaris' expansion plans, this could attract more investor interest and further drive stock price appreciation.

See More

Valiant Gold Successfully Lists on ASX

- Successful IPO: Valiant Gold lists on the ASX, raising $75 million by issuing 300 million shares at $0.25 each, reflecting strong market confidence in its prospects and solidifying its position as an independent gold company.

- Oversubscribed Priority Offer: The $20 million priority offer to eligible Westgold shareholders was oversubscribed, indicating high investor recognition of Valiant's future growth potential and strengthening its capital base.

- Resource Advantage: Valiant holds approximately 1.2 million ounces of JORC-compliant mineral resources in Western Australia's Murchison region, ensuring competitiveness in the gold mining sector and providing a solid foundation for future production.

- Strategic Cooperation Agreement: The ore purchase agreement with Westgold offers Valiant a pathway to potential early cash flow while supplying incremental ore to Westgold's strategic processing hubs, enhancing synergies between the two companies.

See More

Crude Oil Price Drop Triggers Stock Market Volatility

- Significant Oil Price Drop: Brent crude oil prices fell over 10% to below $90 per barrel, primarily due to a 10-day ceasefire between Israel and Lebanon and optimism surrounding U.S.-Iran negotiations, which alleviated market fears of supply disruptions and reduced the risk premium on oil prices.

- Oilfield Services Companies Impacted: Transocean's stock fell 6.1%, Valaris dropped 6%, and RPC decreased by 8.5%, as these companies typically face pressure to cut capital expenditures when oil prices decline, leading to canceled contracts and idle equipment that negatively affect short-term performance.

- Market Overreaction: The stock market's reaction to falling oil prices may be overly dramatic, and while there could be buying opportunities for high-quality stocks in the short term, the volatility in the oilfield services sector necessitates careful risk assessment by investors.

- RPC Stock Performance: RPC has risen 19.3% since the beginning of the year, yet at $6.60 per share, it remains 9.9% below its 52-week high of $7.32, indicating a cautious market sentiment regarding its future performance, prompting investors to monitor its long-term growth potential.

See More

Valaris Shareholders Enjoy Windfall Amid Stock Surge

- Stock Surge: Valaris's stock price has surged by 90.6% over the past six months, reaching $91.79 per share; however, analysts suggest that this might not be the best time to invest, potentially influencing investor decisions.

- Long-Term Revenue Growth: The company has achieved a 10.7% compounded annual growth rate over the last five years, slightly above the industry average, indicating a good fit with customer needs, but short-term performance in a cyclical industry may not guarantee long-term stability.

- Low Gross Margin Issue: With an average gross margin of 21% over the past five years, Valaris ranks at the bottom of its sector, suggesting weak competitiveness in high commodity price environments, which could impact future profitability.

- Cash Burn Concerns: Valaris's free cash flow margin averaged negative 5.7%, indicating a cash burn of $5.68 for every $100 in revenue, which limits its ability to return capital to investors and increases financial risk.

See More

Valaris to Release Q1 2026 Earnings After Market Close

- Earnings Release Schedule: Valaris plans to issue its Q1 2026 earnings report after the NYSE closes on May 4, 2026, reflecting the company's ongoing commitment to transparency and information disclosure.

- Business Combination Update: Following the announcement of its business combination with Transocean Ltd. on February 9, 2026, Valaris will not hold future earnings conference calls or provide forward-looking guidance, indicating a strategic shift during the integration process.

- Information Disclosure Channels: Valaris utilizes its website to disclose material information to investors, customers, and employees, ensuring timely access to company updates and enhancing communication efficiency with stakeholders.

- Industry Leadership Position: As a leader in offshore drilling services, Valaris operates a high-quality rig fleet across various water depths and geographies, demonstrating its unwavering commitment to safety, operational excellence, and customer satisfaction.

See More

Foreign Energy Stocks Shine in 2026 YTD Performance

- YTD Performance: Tenaz Energy Corp. leads with a remarkable 138.57% year-to-date gain, showcasing its strong position in the international energy market, which has attracted investor interest and boosted its market capitalization.

- Market Comparison: In contrast to the volatility faced by domestic energy stocks, foreign energy companies have excelled due to rising commodity prices and favorable geopolitical conditions, indicating a growing investor confidence in international markets.

- Diverse Sectors: The top ten foreign energy stocks include companies from Canada, Brazil, and Norway across various subsectors, such as oil and gas exploration and offshore drilling services, highlighting the diversity and potential of the global energy market.

- Strong Growth: Companies like Valaris, Equinor ASA, and Spartan Delta have achieved over 74% year-to-date gains, reflecting their competitiveness and profitability in the current market environment.

See More

Valaris and Halliburton Partner with Petronas for Suriname Offshore Development

- Strategic Collaboration: Valaris (VAL) and Halliburton (HAL) have entered into a strategic collaboration agreement with Petronas to leverage Valaris' offshore drilling expertise, Petronas' project stewardship, and Halliburton's digital solutions for the development of Suriname's offshore assets, enhancing competitive positioning in the region.

- Resource Integration Advantage: This partnership aims to capitalize on the rich resources of the Guyana-Suriname Basin, which continues to experience strong exploration success and development activity, potentially providing long-term business opportunities for operators and service providers, thereby driving industry growth.

- Contract Extension: Valaris (VAL) secured a 1,064-day contract extension with Petrobras (PBR) for the Valaris DS-4 drillship starting November 2027, adding approximately $447 million to its contract backlog, which strengthens the company's financial stability.

- Optimistic Market Outlook: With rising oil prices, Halliburton (HAL) is likely to revise its earnings estimates upward, and combined with Valaris' expansion plans, this could attract more investor interest and further drive stock price appreciation.

See More

Valiant Gold Successfully Lists on ASX

- Successful IPO: Valiant Gold lists on the ASX, raising $75 million by issuing 300 million shares at $0.25 each, reflecting strong market confidence in its prospects and solidifying its position as an independent gold company.

- Oversubscribed Priority Offer: The $20 million priority offer to eligible Westgold shareholders was oversubscribed, indicating high investor recognition of Valiant's future growth potential and strengthening its capital base.

- Resource Advantage: Valiant holds approximately 1.2 million ounces of JORC-compliant mineral resources in Western Australia's Murchison region, ensuring competitiveness in the gold mining sector and providing a solid foundation for future production.

- Strategic Cooperation Agreement: The ore purchase agreement with Westgold offers Valiant a pathway to potential early cash flow while supplying incremental ore to Westgold's strategic processing hubs, enhancing synergies between the two companies.

See More