On Holding's 2026 Guidance Sparks Stock Volatility

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 05 2026

0mins

Should l Buy ONON?

Source: Fool

- Stock Price Fluctuation: On Holding's shares dipped following its 2026 guidance, and while Wall Street expressed disappointment over conservative revenue forecasts, long-term investors may view this as an opportunity, indicating a potential undervaluation of the brand's worth.

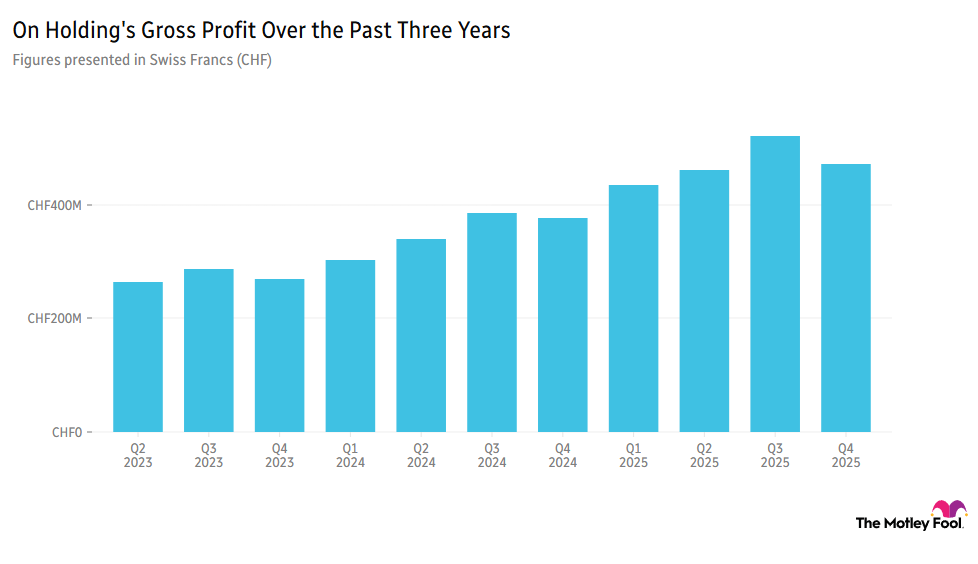

- Sustained Revenue Growth: The company continues to grow revenue at a rate exceeding 20%, showcasing its robust performance in the premium market, although external economic factors complicate the analysis of its business dynamics.

- Margins Exceed Expectations: On Holding's margins are higher than anticipated, which not only enhances its financial health but also instills greater confidence in future investors, indicating strong profitability in a competitive landscape.

- Brand Value Highlighted: As a premium brand, On Holding's fundamentals remain strong; despite short-term market sentiment impacts, its long-term growth potential is noteworthy, particularly in the high-end consumer goods sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy ONON?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on ONON

Wall Street analysts forecast ONON stock price to rise

21 Analyst Rating

18 Buy

2 Hold

1 Sell

Strong Buy

Current: 33.830

Low

30.00

Averages

60.79

High

85.00

Current: 33.830

Low

30.00

Averages

60.79

High

85.00

About ONON

On Holding AG is a Switzerland-based company active in athletic sports accesories industry. The Company provides footwear and sports apparel and is engaged in developing and distributing performance sports products, through independent retailers and global distributors. The Company sells its products trough the internet and its own stores.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

On Holding AG to Report Q1 Earnings on May 12

- Earnings Report Announcement: On Holding AG is set to report its Q1 earnings on May 12, with analysts projecting earnings of 27 cents per share, indicating market focus on the company's profitability.

- CEO Change: The announcement of a CEO change may significantly impact the company's strategic direction and market confidence, particularly at this critical juncture ahead of the earnings report.

- Stock Price Decline: Ahead of the earnings report, On Holding AG's stock fell by 3.4%, reflecting investor concerns regarding the upcoming earnings and leadership transition, which could affect short-term market performance.

- Market Reaction Analysis: Investor reactions to the forthcoming earnings report and management changes may influence the company's future stock price trajectory, especially given the heightened sensitivity to earnings expectations in the current economic climate.

See More

Significant Stock Movements for Vestis and Others

- Vestis Earnings Beat: Vestis surged over 30% after reporting fiscal Q2 results that exceeded expectations, along with an upward revision of its fiscal 2026 EBITDA outlook, indicating strong growth potential in the apparel sector.

- Zebra's Strong Performance: Zebra Technologies reported Q1 earnings of $4.75 per share, surpassing the $4.25 expected by analysts, with revenues of $1.5 billion, and Q2 guidance also exceeded estimates, highlighting ongoing growth in the automation sector.

- Ralliant's Earnings Surprise: Ralliant's adjusted Q1 earnings of 57 cents per share exceeded both company guidance and FactSet consensus of 49 cents, leading to a 14% stock increase, reflecting robust demand in the high-precision instruments market.

- Hub Group Financial Restatement: Hub Group's shares fell over 10% after announcing a restatement of its year-end 2023 and 2024 results, which may negatively impact investor confidence.

See More

US Stocks Retreat as Cramer Analyzes Market Dynamics

- Market Pullback: On Tuesday, the S&P 500 retreated due to a hotter-than-expected April consumer price index and spikes in oil and bond yields, indicating market sensitivity to rising rates, with Jim Cramer noting this adjustment is necessary for AI-related stocks.

- Home Depot Outlook: Despite struggling in a high-interest-rate environment, Jim Cramer remains bullish on Home Depot, believing it will outperform Lowe's, with Citi rating Home Depot as a buy, reflecting confidence in its future earnings potential.

- Nvidia Price Fluctuation: Nvidia shares slipped from a fresh intraday high ahead of its earnings report, although Wells Fargo raised its price target to $325, Jim Cramer advises investors to hold onto the stock, emphasizing its critical role in the market.

- Rapid Recap: At the end of the video, Jim Cramer mentioned stocks including FedEx, On Holding, Under Armour, Lowe's, and eBay, highlighting his focus on a diversified investment portfolio.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

On Holding Reports Strong Q1 Results but Maintains Sales Guidance

- Strong Sales Performance: On Holding AG reported net sales of CHF 831.9 million (approximately $1.06 billion) for Q1, reflecting over 14% year-on-year growth; however, investor disappointment over unchanged FY26 sales guidance led to a stock decline.

- Margin Improvement: The company achieved a gross profit margin increase of 430 basis points to 64.2%, while net income margin rose by 460 basis points to 12.4%, indicating effective cost management alongside sales growth, enhancing profitability.

- Cautious Future Outlook: Despite On Holding's expectation for at least 23% growth in FY26 net sales to CHF 3.51 billion, management remains cautious due to significant headwinds from higher U.S. tariffs, impacting future confidence.

- EBITDA Guidance Upgrade: The adjusted EBITDA margin for FY26 is projected to be between 19.5% and 20%, up from the previous guidance of 18.5% to 19%, reflecting ongoing improvements in the company's profitability.

See More

ONON Shares Surge After Record Sales Drive Profitability

- Significant Sales Growth: On Holding (ONON) shares surged over 5% pre-market, driven by a remarkable 44.4% revenue growth in the APAC region, achieving record net sales and profitability, which enhances its full-year profit outlook and validates its premium brand strategy.

- Profitability Enhancement: Co-CEO Casper Coppetti emphasized that Q1 performance serves as strong evidence of their premium strategy's success, with projections indicating a gross profit margin of 64.5% by year-end, further solidifying the company's market position.

- Positive Market Reaction: Despite facing significant headwinds from spending and tariffs, TMF CIO Andy Cross noted that On Holding continues to demonstrate strong long-term performance, reflecting investor confidence in its business model and optimistic outlook for future growth.

- Favorable Industry Trends: As AI workloads shift towards inference, the CPU market is entering a growth 'super cycle,' presenting new opportunities for chipmakers like AMD and Intel, which are expected to be near-term winners, further driving stock price increases.

See More

On Holding AG to Report Q1 Earnings on May 12

- Earnings Report Announcement: On Holding AG is set to report its Q1 earnings on May 12, with analysts projecting earnings of 27 cents per share, indicating market focus on the company's profitability.

- CEO Change: The announcement of a CEO change may significantly impact the company's strategic direction and market confidence, particularly at this critical juncture ahead of the earnings report.

- Stock Price Decline: Ahead of the earnings report, On Holding AG's stock fell by 3.4%, reflecting investor concerns regarding the upcoming earnings and leadership transition, which could affect short-term market performance.

- Market Reaction Analysis: Investor reactions to the forthcoming earnings report and management changes may influence the company's future stock price trajectory, especially given the heightened sensitivity to earnings expectations in the current economic climate.

See More

Significant Stock Movements for Vestis and Others

- Vestis Earnings Beat: Vestis surged over 30% after reporting fiscal Q2 results that exceeded expectations, along with an upward revision of its fiscal 2026 EBITDA outlook, indicating strong growth potential in the apparel sector.

- Zebra's Strong Performance: Zebra Technologies reported Q1 earnings of $4.75 per share, surpassing the $4.25 expected by analysts, with revenues of $1.5 billion, and Q2 guidance also exceeded estimates, highlighting ongoing growth in the automation sector.

- Ralliant's Earnings Surprise: Ralliant's adjusted Q1 earnings of 57 cents per share exceeded both company guidance and FactSet consensus of 49 cents, leading to a 14% stock increase, reflecting robust demand in the high-precision instruments market.

- Hub Group Financial Restatement: Hub Group's shares fell over 10% after announcing a restatement of its year-end 2023 and 2024 results, which may negatively impact investor confidence.

See More

US Stocks Retreat as Cramer Analyzes Market Dynamics

- Market Pullback: On Tuesday, the S&P 500 retreated due to a hotter-than-expected April consumer price index and spikes in oil and bond yields, indicating market sensitivity to rising rates, with Jim Cramer noting this adjustment is necessary for AI-related stocks.

- Home Depot Outlook: Despite struggling in a high-interest-rate environment, Jim Cramer remains bullish on Home Depot, believing it will outperform Lowe's, with Citi rating Home Depot as a buy, reflecting confidence in its future earnings potential.

- Nvidia Price Fluctuation: Nvidia shares slipped from a fresh intraday high ahead of its earnings report, although Wells Fargo raised its price target to $325, Jim Cramer advises investors to hold onto the stock, emphasizing its critical role in the market.

- Rapid Recap: At the end of the video, Jim Cramer mentioned stocks including FedEx, On Holding, Under Armour, Lowe's, and eBay, highlighting his focus on a diversified investment portfolio.

See More

GameStop's $56B eBay Bid Rejected as Unviable

- Acquisition Proposal Rejected: eBay has officially rejected GameStop's unsolicited $56 billion acquisition bid, labeling it as 'neither credible nor attractive,' with concerns over a significant funding gap and high debt load, which could undermine GameStop's market confidence.

- Financing Challenges Emerge: Despite CEO Ryan Cohen's commitment to provide $20 billion in financing, analysts warn that GameStop's $10 billion market cap makes acquiring a $48 billion giant nearly impossible without extreme equity dilution, highlighting the fragility of its financing capabilities.

- Market Reaction Tepid: Following eBay's rejection, GameStop's stock fell 2.37% in pre-market trading, indicating investor concerns about its acquisition ability, which may impact its future stock performance and market positioning.

- Unclear Strategic Direction: eBay's board reiterated its focus on luxury goods and trading cards, believing this will yield superior shareholder returns, while GameStop's acquisition intentions could distract from its core resources and strategic focus.

See More

On Holding Reports Strong Q1 Results but Maintains Sales Guidance

- Strong Sales Performance: On Holding AG reported net sales of CHF 831.9 million (approximately $1.06 billion) for Q1, reflecting over 14% year-on-year growth; however, investor disappointment over unchanged FY26 sales guidance led to a stock decline.

- Margin Improvement: The company achieved a gross profit margin increase of 430 basis points to 64.2%, while net income margin rose by 460 basis points to 12.4%, indicating effective cost management alongside sales growth, enhancing profitability.

- Cautious Future Outlook: Despite On Holding's expectation for at least 23% growth in FY26 net sales to CHF 3.51 billion, management remains cautious due to significant headwinds from higher U.S. tariffs, impacting future confidence.

- EBITDA Guidance Upgrade: The adjusted EBITDA margin for FY26 is projected to be between 19.5% and 20%, up from the previous guidance of 18.5% to 19%, reflecting ongoing improvements in the company's profitability.

See More

ONON Shares Surge After Record Sales Drive Profitability

- Significant Sales Growth: On Holding (ONON) shares surged over 5% pre-market, driven by a remarkable 44.4% revenue growth in the APAC region, achieving record net sales and profitability, which enhances its full-year profit outlook and validates its premium brand strategy.

- Profitability Enhancement: Co-CEO Casper Coppetti emphasized that Q1 performance serves as strong evidence of their premium strategy's success, with projections indicating a gross profit margin of 64.5% by year-end, further solidifying the company's market position.

- Positive Market Reaction: Despite facing significant headwinds from spending and tariffs, TMF CIO Andy Cross noted that On Holding continues to demonstrate strong long-term performance, reflecting investor confidence in its business model and optimistic outlook for future growth.

- Favorable Industry Trends: As AI workloads shift towards inference, the CPU market is entering a growth 'super cycle,' presenting new opportunities for chipmakers like AMD and Intel, which are expected to be near-term winners, further driving stock price increases.

See More