Nvidia's Stock Price Potential Soars in 2026

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 10 2026

0mins

Should l Buy NVDA?

Source: Fool

- Significant Revenue Growth: Nvidia's fiscal Q4 2026 revenue surged 73% year-over-year to $68 billion, with full-year revenue increasing 65% to $216 billion, reflecting strong market demand and the company's leadership in the AI sector.

- Chip Platform Success: Nvidia's Blackwell and Rubin chip platforms have gained tremendous traction among customers, with projected revenues of up to $1 trillion in 2026 and 2027, significantly exceeding previous expectations and indicating strong market appeal.

- Data Center Business Expansion: Nvidia recorded a record $193.7 billion in data center revenue for fiscal 2026, up 68% from the previous year, with expectations for substantial growth in the coming years, enhancing the company's overall profitability.

- Stock Price Potential: Despite the current stock pullback, Nvidia's forward P/E ratio stands at 21 times, and given its earnings growth is expected to outpace the S&P 500's average, analysts project the stock could double to $348, making it a compelling buy opportunity.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 219.440

Low

200.00

Averages

264.97

High

352.00

Current: 219.440

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia's Q1 Revenue Expected to Exceed Estimates by $1.4B

- Revenue Surge Expected: According to Citi, Nvidia's Q1 FY2027 revenue is projected to reach $80B, exceeding the consensus estimate of $78.6B by $1.4B, driven by a robust ramp of the B300 product line.

- Continued Growth Trend: The company anticipates an 11% quarter-over-quarter sales increase in Q2 FY2027, reaching $89B, primarily due to the ongoing ramp of B300 and faster-than-expected shipments of 1.6 trillion transceivers, solidifying its market position.

- Strong GPU Demand: Nvidia has only missed consensus estimates by more than $1B three times in the past 12 quarters, with CEO Jensen Huang describing the demand for their GPUs as “insane,” highlighting the company's strong appeal in high-performance computing.

- Sales Forecast Revision: Citi has raised Nvidia's FY2027 sales forecast to $284B, reflecting a 79% year-over-year increase, with AI GPUs expected to account for 70% to 80% of total data center sales, showcasing the company's strategic advantage in AI and data processing.

See More

Nvidia's Dominance in AI Market Continues to Strengthen

- Market Share Advantage: Nvidia holds a 92% share of the GPU data center market, and with global AI infrastructure spending projected to reach $7 trillion by 2030, this will further solidify its market leadership and drive sustained growth for the company.

- Future Revenue Expectations: Nvidia anticipates first-quarter revenue of $78 billion for fiscal Q4 2026, with total revenue expected to reach $922 billion over the next seven quarters, indicating strong growth potential and market confidence.

- Stock Price Forecast: Should Nvidia achieve $621 billion in revenue by 2027, its stock price could surge by 252% to $640, resulting in a market cap of approximately $15.5 trillion, reflecting optimistic market expectations for its future performance.

- Accelerated Innovation Cycle: By shortening its GPU update cycle to 12-18 months compared to competitors' 3-5 years, Nvidia's rapid innovation capability will help maintain its lead in the AI sector, further boosting investor confidence.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

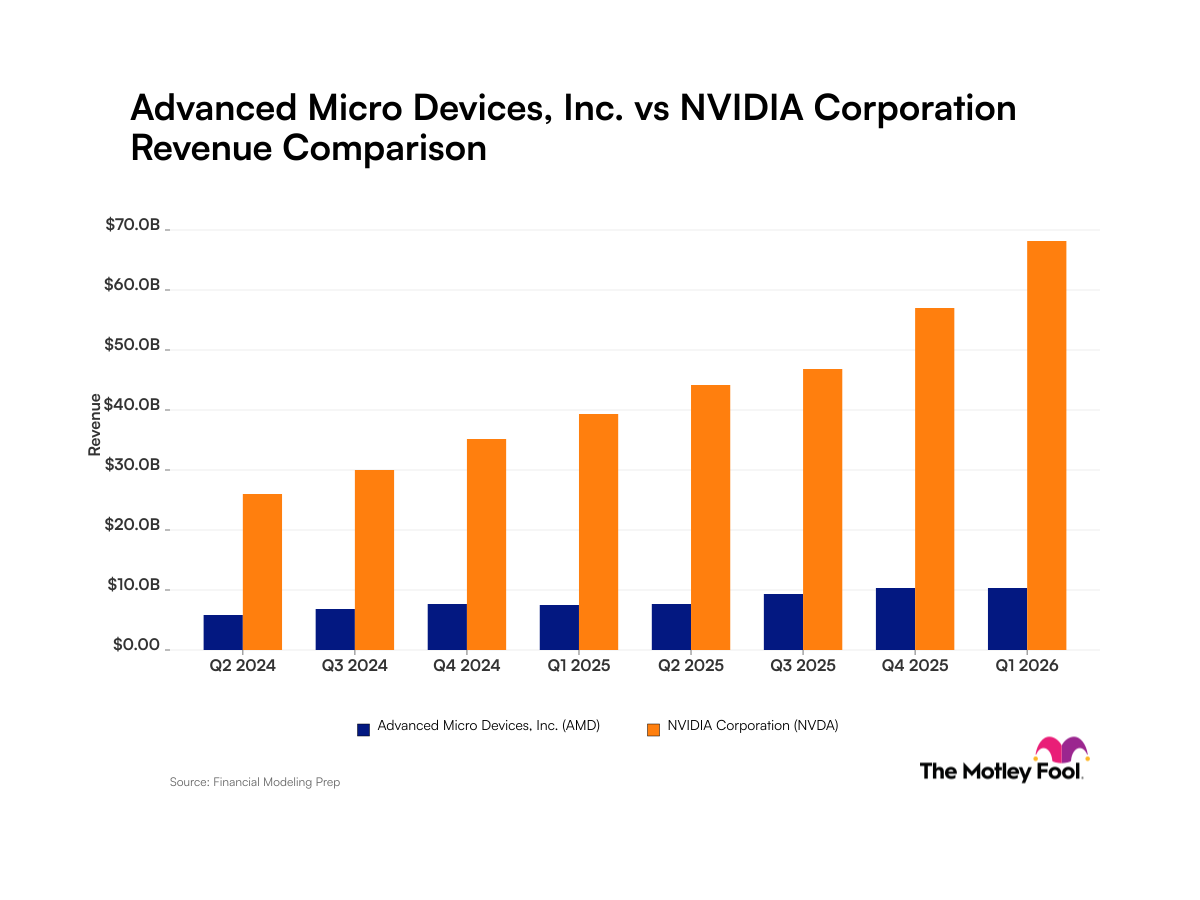

Analysis of Revenue Growth for AMD and Nvidia

- AMD Revenue Growth: AMD reported a revenue of $10.3 billion in Q1 2026 with a net income margin of approximately 13%, indicating stable growth in consumer and enterprise computing markets, although it still lags behind Nvidia.

- Nvidia Market Dominance: Nvidia achieved a revenue of $68.1 billion in Q1 2026 with a net income margin of around 63%, and its consistent quarter-over-quarter growth underscores its leadership position in the AI sector, surpassing AMD's market performance.

- Surge in AI Demand: The rise of artificial intelligence has led to a skyrocketing demand for high-performance computing components from both AMD and Nvidia, particularly as Nvidia leverages its CUDA software and the Vera Rubin platform to further solidify its market advantage, putting AMD under greater competitive pressure.

- Quarterly Revenue Comparison: In Q2 2024, AMD's revenue was $5.8 billion compared to Nvidia's $26.0 billion, highlighting the significant revenue disparity between the two companies and reflecting Nvidia's robust performance and market share in the semiconductor industry.

See More

Institutional and Retail Traders Bullish on Stocks

- Surge in Market Participation: RBC Capital Markets' Amy Wu-Silverman highlights that both institutional and retail traders are actively buying call options, indicating widespread enthusiasm and confidence in the stock market's future.

- Historic Call Buying Activity: Silverman describes the recent surge in call option purchases as 'historic,' reflecting an intensifying bullish sentiment among investors, particularly as the S&P 500 recently surpassed 7,400 points.

- Nvidia Earnings Outlook: Nvidia is set to report earnings next week, and as the most valuable company in the S&P 500 with a market cap of $5.33 trillion, accounting for about 8% of the index, its report could significantly impact market dynamics.

- Market Rebound Momentum: Despite ongoing tensions between the U.S. and Iran, the S&P 500 has rebounded strongly to all-time highs, demonstrating market confidence in economic recovery and expectations for future growth.

See More

Market Outlook: Inflation Pressures and Tech Stock Dynamics

- Inflation Data Surprises: April's Consumer Price Index (CPI) rose 3.8% year-over-year, exceeding the 3.7% expectation, while core CPI also slightly surpassed forecasts at 2.8%, putting pressure on Fed rate cut hopes and potentially affecting market sentiment.

- Nvidia's Earnings Outlook Positive: Despite Nvidia's stock hitting a record high with a 16% gain over the past month, analysts maintain a bullish stance, believing the stock, trading at under 20 times 2028 earnings estimates, is worth buying, with price targets raised from $265 to $315.

- AMD and Super Micro Price Target Increases: Mizuho raised AMD's price target from $414 to $515, citing agentic AI driving server demand, while Super Micro's target was increased to $36 due to strong AI server demand, although concerns linger about the company's ties to China.

- Qnity Electronics Strong Performance: Qnity Electronics reported better-than-expected earnings with a 17% organic sales growth driven by the AI boom, leading to a more than 3% stock increase, indicating strong market demand and future growth potential.

See More

Nvidia's Q1 Revenue Expected to Exceed Estimates by $1.4B

- Revenue Surge Expected: According to Citi, Nvidia's Q1 FY2027 revenue is projected to reach $80B, exceeding the consensus estimate of $78.6B by $1.4B, driven by a robust ramp of the B300 product line.

- Continued Growth Trend: The company anticipates an 11% quarter-over-quarter sales increase in Q2 FY2027, reaching $89B, primarily due to the ongoing ramp of B300 and faster-than-expected shipments of 1.6 trillion transceivers, solidifying its market position.

- Strong GPU Demand: Nvidia has only missed consensus estimates by more than $1B three times in the past 12 quarters, with CEO Jensen Huang describing the demand for their GPUs as “insane,” highlighting the company's strong appeal in high-performance computing.

- Sales Forecast Revision: Citi has raised Nvidia's FY2027 sales forecast to $284B, reflecting a 79% year-over-year increase, with AI GPUs expected to account for 70% to 80% of total data center sales, showcasing the company's strategic advantage in AI and data processing.

See More

Nvidia's Dominance in AI Market Continues to Strengthen

- Market Share Advantage: Nvidia holds a 92% share of the GPU data center market, and with global AI infrastructure spending projected to reach $7 trillion by 2030, this will further solidify its market leadership and drive sustained growth for the company.

- Future Revenue Expectations: Nvidia anticipates first-quarter revenue of $78 billion for fiscal Q4 2026, with total revenue expected to reach $922 billion over the next seven quarters, indicating strong growth potential and market confidence.

- Stock Price Forecast: Should Nvidia achieve $621 billion in revenue by 2027, its stock price could surge by 252% to $640, resulting in a market cap of approximately $15.5 trillion, reflecting optimistic market expectations for its future performance.

- Accelerated Innovation Cycle: By shortening its GPU update cycle to 12-18 months compared to competitors' 3-5 years, Nvidia's rapid innovation capability will help maintain its lead in the AI sector, further boosting investor confidence.

See More

AI Drives Semiconductor Industry Growth

- Surging Market Demand: McKinsey predicts that by 2030, AI inference will account for over 50% of computing power in data centers, reflecting the urgent demand from enterprises and consumers for AI integration, thereby driving sustained growth in the semiconductor industry.

- Arm's Market Potential: Arm Holdings anticipates over $2 billion in customer demand for its AGI CPU in fiscal years 2027 and 2028, indicating strong competitiveness in the AI inference market and the potential to generate $15 billion in annual revenue over the next five years.

- Technological Innovation and Partnerships: Arm's collaboration with Meta Platforms on the AGI CPU promises to save up to $10 billion in data center capital expenditures while delivering double the computing performance of AMD and Intel's x86 processors, further solidifying its market position.

- Optimistic Financial Outlook: Arm's revenue increased by 23% to $4.92 billion in fiscal 2026, with expectations of reaching $25 billion by fiscal 2031, indicating robust growth potential, and projected earnings per share rising to $9.00, suggesting a 51% upside in stock price.

See More

Analysis of Revenue Growth for AMD and Nvidia

- AMD Revenue Growth: AMD reported a revenue of $10.3 billion in Q1 2026 with a net income margin of approximately 13%, indicating stable growth in consumer and enterprise computing markets, although it still lags behind Nvidia.

- Nvidia Market Dominance: Nvidia achieved a revenue of $68.1 billion in Q1 2026 with a net income margin of around 63%, and its consistent quarter-over-quarter growth underscores its leadership position in the AI sector, surpassing AMD's market performance.

- Surge in AI Demand: The rise of artificial intelligence has led to a skyrocketing demand for high-performance computing components from both AMD and Nvidia, particularly as Nvidia leverages its CUDA software and the Vera Rubin platform to further solidify its market advantage, putting AMD under greater competitive pressure.

- Quarterly Revenue Comparison: In Q2 2024, AMD's revenue was $5.8 billion compared to Nvidia's $26.0 billion, highlighting the significant revenue disparity between the two companies and reflecting Nvidia's robust performance and market share in the semiconductor industry.

See More

Institutional and Retail Traders Bullish on Stocks

- Surge in Market Participation: RBC Capital Markets' Amy Wu-Silverman highlights that both institutional and retail traders are actively buying call options, indicating widespread enthusiasm and confidence in the stock market's future.

- Historic Call Buying Activity: Silverman describes the recent surge in call option purchases as 'historic,' reflecting an intensifying bullish sentiment among investors, particularly as the S&P 500 recently surpassed 7,400 points.

- Nvidia Earnings Outlook: Nvidia is set to report earnings next week, and as the most valuable company in the S&P 500 with a market cap of $5.33 trillion, accounting for about 8% of the index, its report could significantly impact market dynamics.

- Market Rebound Momentum: Despite ongoing tensions between the U.S. and Iran, the S&P 500 has rebounded strongly to all-time highs, demonstrating market confidence in economic recovery and expectations for future growth.

See More

Market Outlook: Inflation Pressures and Tech Stock Dynamics

- Inflation Data Surprises: April's Consumer Price Index (CPI) rose 3.8% year-over-year, exceeding the 3.7% expectation, while core CPI also slightly surpassed forecasts at 2.8%, putting pressure on Fed rate cut hopes and potentially affecting market sentiment.

- Nvidia's Earnings Outlook Positive: Despite Nvidia's stock hitting a record high with a 16% gain over the past month, analysts maintain a bullish stance, believing the stock, trading at under 20 times 2028 earnings estimates, is worth buying, with price targets raised from $265 to $315.

- AMD and Super Micro Price Target Increases: Mizuho raised AMD's price target from $414 to $515, citing agentic AI driving server demand, while Super Micro's target was increased to $36 due to strong AI server demand, although concerns linger about the company's ties to China.

- Qnity Electronics Strong Performance: Qnity Electronics reported better-than-expected earnings with a 17% organic sales growth driven by the AI boom, leading to a more than 3% stock increase, indicating strong market demand and future growth potential.

See More