Impinj Q4 Earnings Miss Expectations with $0.50 EPS

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 05 2026

0mins

Should l Buy PI?

Source: seekingalpha

- Earnings Performance: Impinj reported a Q4 non-GAAP EPS of $0.50, missing expectations by $0.01, indicating pressure on profitability that may affect investor confidence.

- Revenue Growth: The company achieved revenue of $92.8 million, reflecting a modest year-over-year increase of 1.3%, which, while in line with expectations, suggests challenges amid intensifying market competition.

- Cautious Outlook: For Q1 2026, revenue is projected between $71.0 million and $74.0 million, falling short of the consensus estimate of $90.47 million, indicating a conservative stance on short-term performance that could impact stock price.

- Net Loss Projections: GAAP net loss is expected to range from $16.6 million to $15.1 million, with diluted loss per share between $0.55 and $0.49, highlighting ongoing challenges in cost control and achieving profitability.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy PI?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on PI

Wall Street analysts forecast PI stock price to rise

8 Analyst Rating

7 Buy

1 Hold

0 Sell

Strong Buy

Current: 98.750

Low

200.00

Averages

240.50

High

273.00

Current: 98.750

Low

200.00

Averages

240.50

High

273.00

About PI

Impinj, Inc. (Impinj) is a RAIN radio frequency identification (RFID) and Internet of things provider. The Company helps businesses and people analyze, optimize, and innovate by wirelessly connecting billions of everyday things, such as apparel, automobile parts, luggage, and shipments to the Internet. The Impinj platform uses RAIN RFID to deliver timely data about these everyday things to business and consumer applications, enabling a boundless Internet of Things. It designs, sells or licenses, including silicon RAIN radios; manufacturing, test, encoding and reading systems, and software and cloud services that encapsulate its solutions know-how. The Company sells two types of silicon integrated circuit (IC), radios. The first are endpoint ICs that store a serialized number to wirelessly identify an item. The second are reader ICs that its partners use in finished readers to wirelessly discover, inventory and engage the endpoint ICs.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Impinj to Repurchase $40.2 Million of Convertible Notes

- Repurchase Agreement: Impinj has entered into agreements to repurchase approximately $40.2 million of its 1.125% convertible notes, with a total repurchase cost of about $47.2 million, indicating a proactive approach to debt management.

- Closing Timeline: The repurchases are expected to close on March 16, 2026, after which approximately $57.3 million of the notes will remain outstanding, reflecting the company's ongoing efforts to optimize its capital structure.

- Future Revenue Outlook: Impinj targets Q1 2026 revenue between $71 million and $74 million, driven by the rollout of custom chips and inventory transition, showcasing the company's strategic focus on new product development.

- Market Environment Challenges: Despite the positive outlook on repurchases and revenue targets, market analysts suggest that Impinj may continue to face lingering low growth pressures, necessitating close attention to its competitive position in the semiconductor industry.

See More

Impinj Inc. Announces $40.2 Million Convertible Note Repurchase

- Repurchase Agreement Details: Impinj has entered into agreements with certain holders to repurchase approximately $40.2 million of its 1.125% Convertible Notes, with a total repurchase cost of about $47.2 million, including accrued and unpaid interest, indicating proactive capital management by the company.

- Repurchase Timeline: The repurchases are expected to close on March 16, 2026, after which approximately $57.3 million of the Convertible Notes will remain outstanding, reflecting the company's ongoing efforts to optimize its debt structure.

- Market Impact Analysis: By reducing the outstanding amount of Convertible Notes, Impinj may enhance its earnings per share and boost investor confidence while lowering future interest burdens, thereby laying a foundation for the company's long-term financial health.

- Forward-Looking Statement Risks: The company notes that forward-looking statements are subject to market fluctuations and other uncertainties, urging investors to consider these risks for informed investment decisions.

See More

Aperture Investors Initiates Position in Impinj

- New Position Established: According to a February 17, 2026 SEC filing, Aperture Investors initiated a new position in Impinj during Q4 2025, acquiring 117,118 shares valued at $20.38 million, indicating confidence in the company's potential.

- AUM Proportion: This investment represents 2.33% of Aperture Investors' reportable AUM as of December 31, 2025, highlighting a strategic diversification within their investment portfolio.

- Stock Performance: As of Thursday, Impinj shares were priced at $91.62, reflecting a mere 0.4% increase over the past year, significantly underperforming the S&P 500's approximately 20% gain, which raises concerns about its future growth prospects.

- Financial Outlook: Impinj projects first-quarter revenues between $71 million and $74 million, with a net loss forecasted between $15.1 million and $16.6 million, leading to a sharp 25% decline in stock price following the announcement, indicating market skepticism regarding its profitability.

See More

Top Rule Breakers Seek Innovation

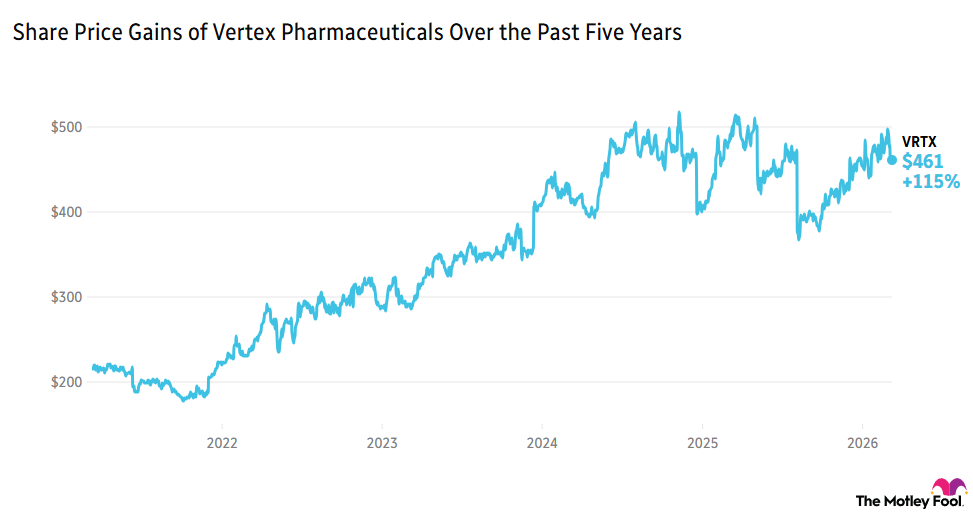

- Vertex Drug Trial Success: Vertex Pharmaceuticals (VRTX) rose over 5% after the closing bell due to positive trial data from Povetacicept, enhancing the likelihood of a potential accelerated FDA approval filing, which is expected to further boost the company's stock performance, surpassing a 33% increase over the S&P 500 since February 2022.

- Hewlett Packard's Strong Earnings: Hewlett Packard (HPE) gained over 1% thanks to a 380% surge in Data Center Networking sales and an upgraded group revenue forecast, indicating robust growth potential in the market that may attract more investor interest.

- Casey's and Vail Resorts Earnings Pressure: Casey's General Stores (CASY) dropped about 2% ahead of the opening bell due to only a 0.5% revenue increase, while Vail Resorts (MTN) fell after reporting a 5% quarterly revenue drop, with the CEO citing weather impacts, highlighting challenges faced by the industry.

- BioNTech Faces Losses: BioNTech (BNTX) fell over 14% ahead of the opening bell as it reported an annual net loss nearly double that of the previous year and announced plans for co-founders to create an independent company focusing on next-generation mRNA innovations, which may affect its future market performance.

See More

Meta Partners with AMD for Massive Chip Investment

- Massive Investment Plan: Meta Platforms announced plans to invest tens of billions in Advanced Micro Devices (AMD) chips and gear to support its data centers and AI operations, which is expected to drive growth in the semiconductor industry.

- Low-Rated Stocks: According to Seeking Alpha's Quant Ratings, Impinj (PI) ranks lowest with a score of 1.20, followed closely by Datavault AI (DVLT) at 1.23, indicating a lack of market confidence in these companies.

- Negative Returns: Impinj and Rigetti Computing have year-to-date returns of -31.62% and -27.67%, respectively, reflecting poor performance of these low-rated stocks in the market, which may influence investor decisions.

- Rating System Overview: Seeking Alpha's Quant system ranks stocks based on critical metrics such as valuation, growth, stock momentum, and profitability, with ratings from 1 to 5, where above 3.5 indicates bullish sentiment and below 2.5 indicates bearish outlook.

See More

Impinj Misses Q4 Estimates, Shares Plunge

- Flat Revenue Growth: Impinj's Q4 revenue increased by only 1.4% to $92.8 million, matching analyst expectations but failing to boost market confidence, resulting in a 21.4% drop in stock price.

- Profitability Pressure: Adjusted EBITDA rose from $15 million to $16.4 million, yet the earnings per share of $0.50 fell short of the $0.51 consensus, indicating ongoing profitability challenges.

- Pessimistic Outlook: The company forecasts Q1 revenue between $71 million and $74 million, implying a 2% decline at the midpoint, significantly below the $90.5 million consensus, reflecting weak demand from apparel retailers.

- Market Reaction: Although analysts maintained positive ratings on Impinj, the stock was heavily impacted by the expected GAAP net loss of $15.1 million to $16.6 million, intensifying concerns over its premium valuation amidst ongoing headwinds.

See More

Impinj to Repurchase $40.2 Million of Convertible Notes

- Repurchase Agreement: Impinj has entered into agreements to repurchase approximately $40.2 million of its 1.125% convertible notes, with a total repurchase cost of about $47.2 million, indicating a proactive approach to debt management.

- Closing Timeline: The repurchases are expected to close on March 16, 2026, after which approximately $57.3 million of the notes will remain outstanding, reflecting the company's ongoing efforts to optimize its capital structure.

- Future Revenue Outlook: Impinj targets Q1 2026 revenue between $71 million and $74 million, driven by the rollout of custom chips and inventory transition, showcasing the company's strategic focus on new product development.

- Market Environment Challenges: Despite the positive outlook on repurchases and revenue targets, market analysts suggest that Impinj may continue to face lingering low growth pressures, necessitating close attention to its competitive position in the semiconductor industry.

See More

Impinj Inc. Announces $40.2 Million Convertible Note Repurchase

- Repurchase Agreement Details: Impinj has entered into agreements with certain holders to repurchase approximately $40.2 million of its 1.125% Convertible Notes, with a total repurchase cost of about $47.2 million, including accrued and unpaid interest, indicating proactive capital management by the company.

- Repurchase Timeline: The repurchases are expected to close on March 16, 2026, after which approximately $57.3 million of the Convertible Notes will remain outstanding, reflecting the company's ongoing efforts to optimize its debt structure.

- Market Impact Analysis: By reducing the outstanding amount of Convertible Notes, Impinj may enhance its earnings per share and boost investor confidence while lowering future interest burdens, thereby laying a foundation for the company's long-term financial health.

- Forward-Looking Statement Risks: The company notes that forward-looking statements are subject to market fluctuations and other uncertainties, urging investors to consider these risks for informed investment decisions.

See More

Aperture Investors Initiates Position in Impinj

- New Position Established: According to a February 17, 2026 SEC filing, Aperture Investors initiated a new position in Impinj during Q4 2025, acquiring 117,118 shares valued at $20.38 million, indicating confidence in the company's potential.

- AUM Proportion: This investment represents 2.33% of Aperture Investors' reportable AUM as of December 31, 2025, highlighting a strategic diversification within their investment portfolio.

- Stock Performance: As of Thursday, Impinj shares were priced at $91.62, reflecting a mere 0.4% increase over the past year, significantly underperforming the S&P 500's approximately 20% gain, which raises concerns about its future growth prospects.

- Financial Outlook: Impinj projects first-quarter revenues between $71 million and $74 million, with a net loss forecasted between $15.1 million and $16.6 million, leading to a sharp 25% decline in stock price following the announcement, indicating market skepticism regarding its profitability.

See More

Top Rule Breakers Seek Innovation

- Vertex Drug Trial Success: Vertex Pharmaceuticals (VRTX) rose over 5% after the closing bell due to positive trial data from Povetacicept, enhancing the likelihood of a potential accelerated FDA approval filing, which is expected to further boost the company's stock performance, surpassing a 33% increase over the S&P 500 since February 2022.

- Hewlett Packard's Strong Earnings: Hewlett Packard (HPE) gained over 1% thanks to a 380% surge in Data Center Networking sales and an upgraded group revenue forecast, indicating robust growth potential in the market that may attract more investor interest.

- Casey's and Vail Resorts Earnings Pressure: Casey's General Stores (CASY) dropped about 2% ahead of the opening bell due to only a 0.5% revenue increase, while Vail Resorts (MTN) fell after reporting a 5% quarterly revenue drop, with the CEO citing weather impacts, highlighting challenges faced by the industry.

- BioNTech Faces Losses: BioNTech (BNTX) fell over 14% ahead of the opening bell as it reported an annual net loss nearly double that of the previous year and announced plans for co-founders to create an independent company focusing on next-generation mRNA innovations, which may affect its future market performance.

See More

Meta Partners with AMD for Massive Chip Investment

- Massive Investment Plan: Meta Platforms announced plans to invest tens of billions in Advanced Micro Devices (AMD) chips and gear to support its data centers and AI operations, which is expected to drive growth in the semiconductor industry.

- Low-Rated Stocks: According to Seeking Alpha's Quant Ratings, Impinj (PI) ranks lowest with a score of 1.20, followed closely by Datavault AI (DVLT) at 1.23, indicating a lack of market confidence in these companies.

- Negative Returns: Impinj and Rigetti Computing have year-to-date returns of -31.62% and -27.67%, respectively, reflecting poor performance of these low-rated stocks in the market, which may influence investor decisions.

- Rating System Overview: Seeking Alpha's Quant system ranks stocks based on critical metrics such as valuation, growth, stock momentum, and profitability, with ratings from 1 to 5, where above 3.5 indicates bullish sentiment and below 2.5 indicates bearish outlook.

See More

Impinj Misses Q4 Estimates, Shares Plunge

- Flat Revenue Growth: Impinj's Q4 revenue increased by only 1.4% to $92.8 million, matching analyst expectations but failing to boost market confidence, resulting in a 21.4% drop in stock price.

- Profitability Pressure: Adjusted EBITDA rose from $15 million to $16.4 million, yet the earnings per share of $0.50 fell short of the $0.51 consensus, indicating ongoing profitability challenges.

- Pessimistic Outlook: The company forecasts Q1 revenue between $71 million and $74 million, implying a 2% decline at the midpoint, significantly below the $90.5 million consensus, reflecting weak demand from apparel retailers.

- Market Reaction: Although analysts maintained positive ratings on Impinj, the stock was heavily impacted by the expected GAAP net loss of $15.1 million to $16.6 million, intensifying concerns over its premium valuation amidst ongoing headwinds.

See More