Key Takeaway

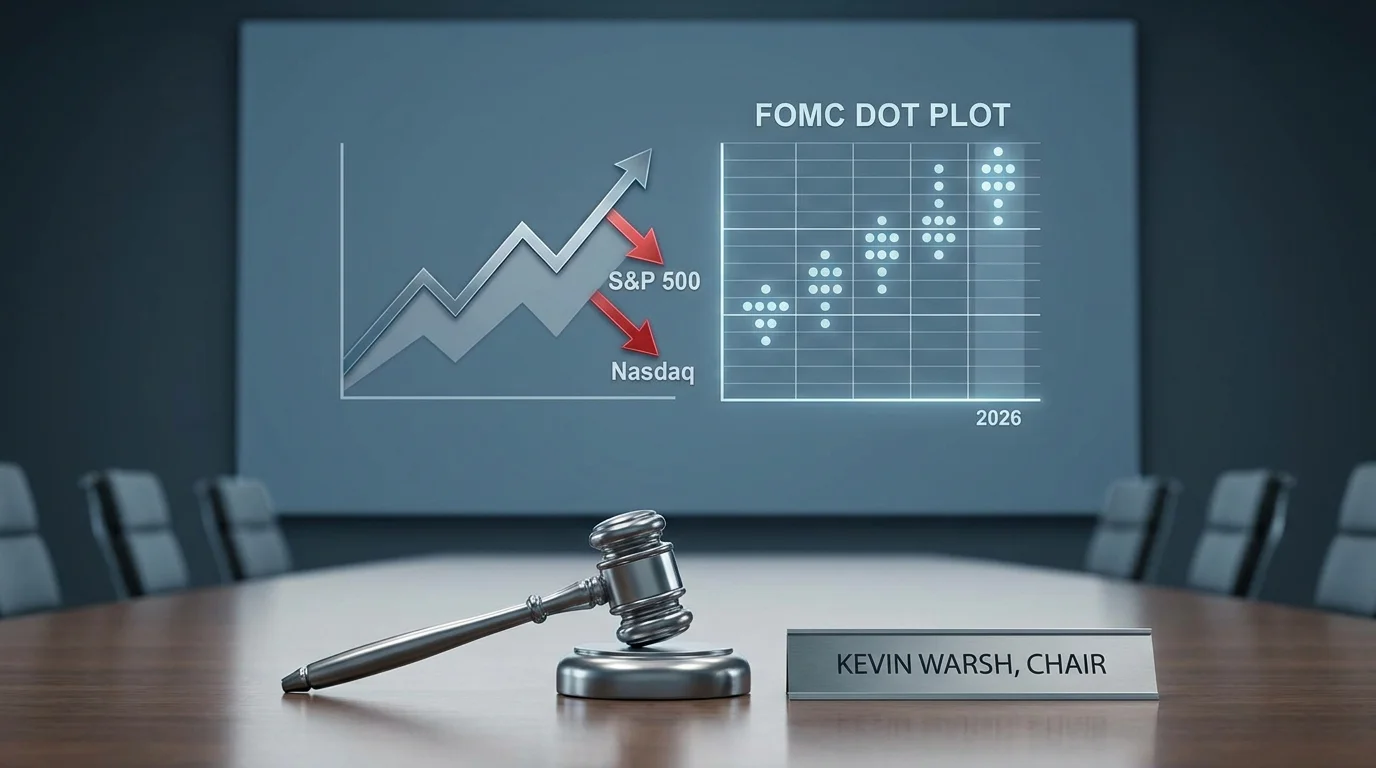

The Federal Reserve's June 2026 meeting delivered a seismic shift in monetary policy expectations that caught markets completely off guard. While the central bank maintained the federal funds rate at its current range of 3.50% to 3.75%, the closely-watched dot plot revealed a hawkish pivot that has fundamentally altered the interest rate outlook for the remainder of the year. Nine out of eighteen Federal Open Market Committee officials now project at least one rate hike before year-end, with six officials anticipating two or more increases—a dramatic reversal from March projections when no one expected hikes and twelve officials actually foresaw rate cuts.

Newly appointed Fed Chair Kevin Warsh presided over his first policy meeting with an unconventional approach that signals a new era of central bank communication. Warsh notably abstained from submitting his own rate projection for the dot plot and eliminated forward guidance language entirely from the post-meeting statement, characterizing the committee as evenly split between those favoring steady rates and those advocating for hikes. The median year-end federal funds rate projection jumped to 3.8% from 3.4% in March, implying at least one quarter-point increase if the outlook materializes. Markets reacted violently to the hawkish surprise, with the Dow Jones Industrial Average plunging 500 points and Treasury yields surging as traders recalibrated their expectations for borrowing costs.

The Hawkish Pivot: Understanding the Dot Plot Revolution

The Summary of Economic Projections released alongside the policy statement painted a starkly different picture of the Fed's rate trajectory than what markets had anticipated just three months ago. The median projection for the federal funds rate at the end of 2026 now stands at 3.8%, representing a 40 basis point increase from the 3.4% median forecast in March. This shift implies that the committee sees at least one quarter-point rate hike as the most likely outcome, a dramatic departure from earlier expectations that had priced in potential easing.

Of the eighteen FOMC members who submitted projections, nine now anticipate at least one rate increase before the conclusion of 2026. Perhaps more strikingly, six officials project two or more hikes, suggesting that a significant portion of the committee believes multiple tightening moves may be necessary to address lingering inflation concerns. This stands in stark contrast to the March meeting, where twelve of nineteen officials expected at least one rate cut and absolutely no one on the committee anticipated rate increases.

The distribution of the dots reveals a committee deeply divided about the appropriate path for monetary policy. Eight officials expect rates to remain steady at current levels through year-end, while only one member projects a rate cut—a lonely position that reflects the dramatic recalibration of inflation risks that has occurred over the past quarter. This dispersion of views suggests that future policy decisions will likely be highly data-dependent and could result in lively debates among committee members as the year progresses.

For investors seeking to navigate this uncertain rate environment, consider using Intellectia AI's stock screener to identify companies best positioned for higher interest rate scenarios. The AI-powered platform can help filter for businesses with strong balance sheets and pricing power that typically outperform during tightening cycles.

Kevin Warsh's Unconventional Debut: A New Era of Fed Communication

Kevin Warsh's first meeting as Federal Reserve Chair was marked by communication choices that departed significantly from his predecessors' approaches, signaling potential structural changes in how the central bank guides market expectations. In a highly unusual move, Warsh declined to submit his own interest rate projection for the dot plot, leaving markets without direct insight into the new chair's personal view on the appropriate policy path. This abstention makes interpreting the committee's collective outlook more challenging, as observers cannot distinguish between the chair's preferences and those of other voting members.

During his post-meeting press conference, Warsh characterized the rate-path projections as reflecting a committee evenly split between those who want to hold rates steady and those who feel hikes will be necessary to combat persistent inflationary pressures. This framing acknowledged the significant disagreement among policymakers while providing little steer about which camp the chair himself might favor. The deliberate ambiguity represents a notable departure from the more prescriptive communication style employed by previous Fed chairs, who typically used press conferences to nudge market expectations in their preferred direction.

Perhaps more consequential for market participants, Warsh eliminated forward guidance language entirely from the post-meeting policy statement, reducing the document to a terse 130 words that provided minimal insight into the committee's thinking. The statement described the U.S. economy as "expanding at a solid pace" and noted that "job gains have kept pace with the workforce," but offered no hints about the likely direction of future policy moves. This dramatic simplification of Fed communication removes a tool that previous chairs had used extensively to prepare markets for upcoming policy shifts.

Warsh also announced the launch of a comprehensive review of Fed communications practices, suggesting that Wednesday's changes may represent just the beginning of a broader overhaul of how the central bank interacts with financial markets. This reform-minded approach aligns with Warsh's prior criticisms of the Fed's overly communicative stance during his time as an outside observer, and could signal a return to a more mysterious central bank that allows its actions rather than its words to guide market expectations.

Inflation Concerns Drive the Hawkish Shift

The dramatic repricing of the Fed's interest rate outlook reflects growing concerns among policymakers that inflation has proven far stickier than previously anticipated. The updated Summary of Economic Projections revealed significant upward revisions to inflation forecasts, with the personal consumption expenditures price index—the Fed's preferred inflation gauge—now expected to reach 3.6% in 2026, up sharply from previous projections. Core PCE inflation, which excludes volatile food and energy prices, was revised to 3.3%, indicating that underlying price pressures remain elevated across the economy.

These inflation projections place the Fed well above its long-run target of 2%, explaining why a majority of committee members now believe additional tightening may be necessary to restore price stability. The persistence of inflation above target has clearly frustrated policymakers who had hoped that the previous cycle of rate increases would have cooled price pressures more effectively by this stage of the economic cycle. Instead, the combination of a resilient labor market and continued consumer spending has allowed businesses to maintain pricing power even in the face of higher borrowing costs.

The inflation forecast revisions appear particularly significant given that they come despite the Fed maintaining interest rates at relatively elevated levels for an extended period. If inflation remains stubbornly high even with the federal funds rate at 3.50% to 3.75%, policymakers may conclude that even higher rates are necessary to achieve their mandate. This logic likely underpins the hawkish shift in the dot plot, as committee members grapple with the reality that the neutral rate of interest—the level that neither stimulates nor restrains the economy—may be higher than previously assumed.

Geopolitical factors have also contributed to the inflation outlook, with the ongoing conflict in the Middle East creating uncertainty about energy prices and global supply chains. Several Fed officials have cited the war with Iran as a contributing factor to higher-than-expected inflation, as energy price volatility and supply disruptions have added upward pressure to input costs across multiple sectors of the economy. This external source of inflation complicates the Fed's task, as monetary policy has limited ability to address supply-side price shocks.

For traders looking to capitalize on market movements driven by Fed policy shifts, Intellectia AI's stock picker provides AI-powered recommendations based on macroeconomic trends and interest rate scenarios. The platform analyzes thousands of data points to identify stocks likely to benefit from or be resilient to tightening monetary conditions.

Market Reaction: Stocks Plunge and Yields Surge

Financial markets responded violently to the hawkish surprise delivered by the June FOMC meeting, with equity indices plunging and Treasury yields surging as traders raced to recalibrate their expectations for monetary policy. The Dow Jones Industrial Average closed approximately 500 points lower, wiping out recent gains and reversing what had been a positive start to the week. The technology-heavy Nasdaq Composite also sold off sharply, as higher interest rate expectations particularly impacted growth stocks whose valuations depend heavily on distant future cash flows.

The bond market reaction was even more dramatic, with Treasury yields rising significantly across the curve as investors priced in the possibility of additional rate hikes. The yield on the benchmark 10-year Treasury note jumped to its highest level in months, reflecting both expectations of tighter monetary policy and concerns about persistent inflation. The yield curve, which had been showing signs of normalization, steepened as traders abandoned bets on imminent rate cuts that had prevailed earlier in the year.

Small-cap stocks, which are generally more sensitive to borrowing costs and domestic economic conditions, underperformed their large-cap counterparts during the selloff. The Russell 2000 index declined more than the broader market, reflecting concerns that smaller companies with less pricing power and more floating-rate debt exposure would face greater headwinds if the Fed follows through with additional rate increases. This divergence between large and small caps suggests that investors are becoming more selective about positioning in an environment where financial conditions may tighten further.

The market's reaction underscores how dramatically the Fed's communication shifted expectations. Entering the meeting, futures markets had been pricing in a high probability of rate cuts later in 2026, with many investors anticipating that slowing economic growth would prompt the Fed to begin easing. The dot plot revelation that the committee now leans toward hikes rather than cuts forced a rapid repricing of assets across the board, with interest-rate-sensitive sectors like real estate and utilities experiencing particularly sharp declines.

Economic Outlook: Solid Growth Meets Persistent Inflation

Despite the hawkish pivot in interest rate projections, the Fed's assessment of the broader economy remained relatively optimistic. The post-meeting statement described economic activity as "expanding at a solid pace," a characterization that suggests policymakers do not see an imminent recession on the horizon. This positive view of the growth outlook provides the Fed with the confidence to potentially raise rates further without fear of tipping the economy into contraction.

The labor market continues to support the case for potential rate hikes, with the Fed noting that "job gains have kept pace with the workforce." This formulation indicates that the central bank sees employment growth as roughly in line with sustainable long-run trends, suggesting that the economy is operating near full employment without generating excessive inflationary pressure through an overheated job market. The balanced description of labor market conditions implies that the Fed does not see unemployment as a pressing concern that would prevent additional tightening.

However, the combination of solid growth and persistent inflation creates a challenging policy dilemma for the Fed. If the economy remains resilient even as inflation stays above target, the central bank may feel compelled to raise rates further to fulfill its price stability mandate, even at the risk of eventually triggering a slowdown. This is the scenario that appears to be increasingly occupying the minds of the nine FOMC members who now project rate hikes, as they weigh the costs of allowing inflation to remain elevated against the risks of overtightening.

The Fed's economic projections also likely reflect uncertainty about the lagged effects of previous rate increases. Monetary policy operates with long and variable lags, meaning that the full impact of the tightening cycle that brought rates to their current levels may not yet be fully felt in the economy. Some committee members may be projecting rate hikes based on the assumption that the economy will prove more resilient than historically typical, while others may simply be reacting to the clear evidence that inflation has not declined as quickly as hoped.

What Investors Should Watch Next

The June FOMC meeting has set the stage for a data-dependent second half of 2026, with each incoming economic report likely to be scrutinized for clues about whether the Fed will follow through on the hawkish signals embedded in the dot plot. Investors should pay particularly close attention to monthly inflation readings, as these will be the primary determinant of whether the nine officials projecting rate hikes maintain their views or whether the committee coalesces around a more dovish consensus. The personal consumption expenditures price index, released monthly, will be especially significant given its status as the Fed's preferred inflation gauge.

Labor market data will also take on heightened importance in the wake of the June meeting. While the Fed currently characterizes job gains as keeping pace with the workforce, any signs of significant weakening in employment could shift the committee's calculus away from rate hikes and potentially back toward steady rates or even cuts. Weekly initial jobless claims, monthly nonfarm payrolls reports, and the unemployment rate will all be market-moving data points as traders attempt to anticipate the Fed's next move.

Fed Chair Warsh's future communications will be closely watched for additional insight into his thinking about the appropriate policy path. While his first press conference maintained deliberate ambiguity, future speeches and testimony before Congress may provide clearer signals about whether the new chair leans toward the hawkish camp or favors holding rates steady. Warsh's approach to guiding market expectations will be particularly important given his decision to eliminate forward guidance from policy statements, leaving his spoken words as the primary vehicle for communicating the Fed's outlook.

Investors should also monitor speeches and interviews from other FOMC members, as the apparent disagreement within the committee suggests that individual policymakers may actively campaign for their preferred policy paths. In an environment where the committee is genuinely divided, public statements from voting members can provide valuable advance signals about how policy debates are likely to unfold at future meetings. The regional Fed presidents in particular often use public appearances to preview their positions before formal votes.

For comprehensive market analysis and real-time insights on Fed policy impacts, consider signing up for Intellectia AI's platform. The AI-powered tools help investors navigate complex macroeconomic environments by analyzing market data, earnings reports, and central bank communications to identify opportunities and risks.

Conclusion

The Federal Reserve's June 2026 meeting represented a watershed moment for monetary policy expectations, as the dot plot revealed a committee that has fundamentally shifted its view on the likely direction of interest rates. With nine of eighteen officials now projecting at least one rate hike before year-end—a dramatic reversal from March when no one anticipated increases—the Fed has signaled that the battle against inflation remains far from won. The median year-end rate projection of 3.8% implies that borrowing costs may rise further even as the economy continues to expand at a solid pace.

New Fed Chair Kevin Warsh's unconventional approach to his first meeting, including his decision to abstain from the dot plot and eliminate forward guidance, suggests that central bank communications may be entering a new era of deliberate ambiguity. While this approach reduces the Fed's ability to steer market expectations through verbal guidance, it may also provide policymakers with greater flexibility to respond to incoming data without fear of contradicting earlier statements. Markets will need to adapt to an environment where the Fed's actions speak louder than its words.

For investors, the path forward requires careful attention to the economic data that will ultimately determine whether the hawkish members of the FOMC prevail in their push for additional tightening. Inflation readings, labor market reports, and signs of economic momentum will all be critical inputs into the policy debate that unfolds over the coming months. In this uncertain environment, maintaining portfolio diversification and focusing on companies with strong fundamentals and pricing power remains the most prudent strategy.

Ready to stay ahead of Fed policy shifts and market movements? Sign up for Intellectia AI today to access AI-powered stock analysis, real-time market insights, and intelligent screening tools that help you make informed investment decisions in any interest rate environment. Start your free trial and discover how AI can enhance your investment research process.