Key Takeaway

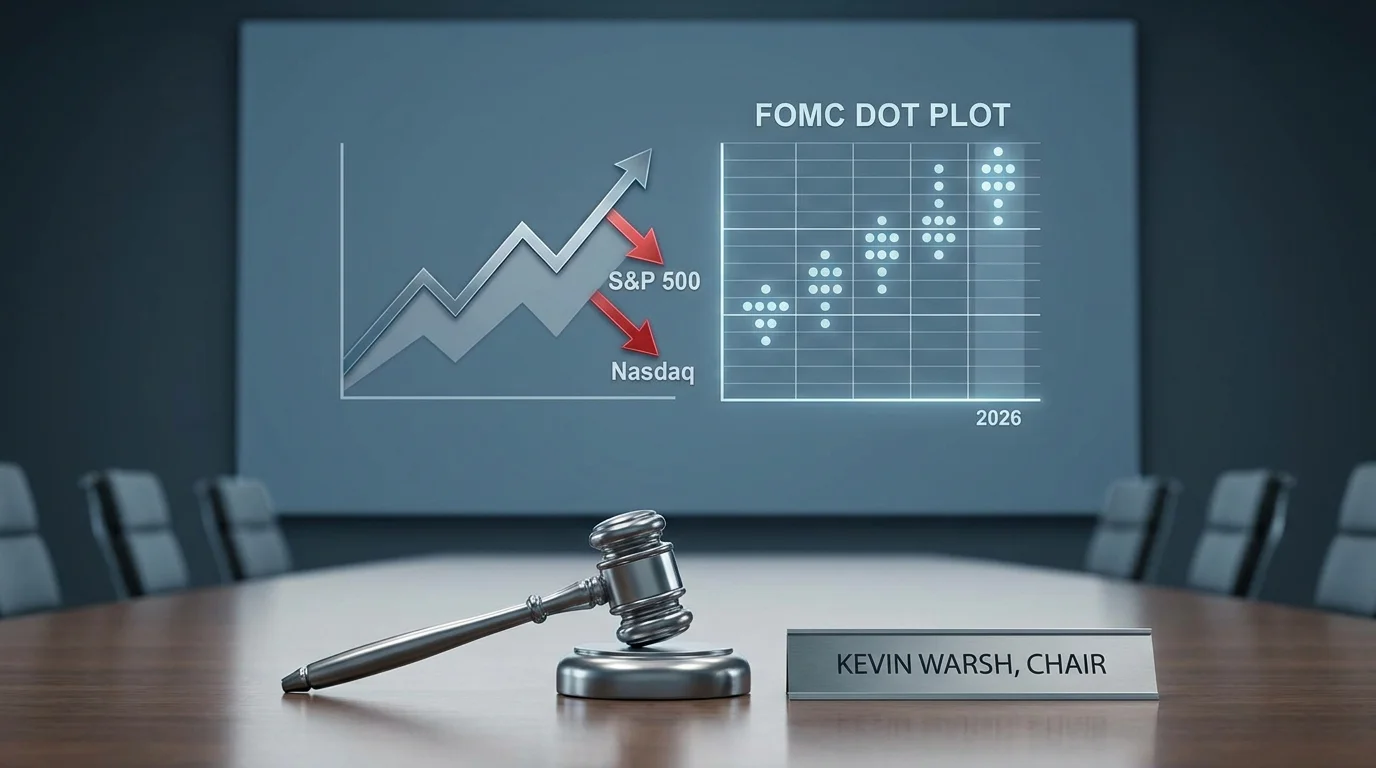

The Federal Reserve's June 2026 meeting, the first under newly appointed Chairman Kevin Warsh, delivered a seismic shift in monetary policy expectations that caught markets off guard. While the central bank held its benchmark rate steady at 3.5% to 3.75%, the real shock came from the Federal Open Market Committee's projections: nine of nineteen policymakers now anticipate at least one interest rate hike before year-end, a dramatic reversal from earlier expectations of multiple cuts.

This hawkish pivot reflects mounting concerns about inflation, which has climbed to a three-year high, partly fueled by geopolitical tensions and supply chain disruptions from the recent conflict with Iran. The dot plot projections reveal a committee increasingly divided on the path forward, with eight members expecting no change, one forecasting a cut, and the majority preparing for tightening. For investors who had positioned for an easing cycle, this recalibration demands a fundamental reassessment of portfolio strategy across asset classes.

For investors seeking to navigate this shifting monetary landscape, leveraging AI-powered stock screening tools can help identify companies best positioned to withstand higher interest rates and inflationary pressures.

Understanding the Fed's Dramatic Shift

The Federal Reserve's June 2026 meeting marks a pivotal moment in monetary policy, representing not just a change in leadership but a fundamental rethinking of the inflation outlook. Kevin Warsh, who assumed the chairmanship following Jerome Powell's departure, approached his inaugural FOMC meeting with characteristic caution—but the committee's collective wisdom pointed toward a more aggressive stance than markets had anticipated.

The decision to hold rates steady while signaling future hikes reflects the delicate balancing act central bankers face. On one hand, economic growth has remained surprisingly resilient despite elevated borrowing costs. On the other, inflationary pressures have proven more persistent than the transitory narrative suggested, with core metrics climbing steadily throughout the first half of 2026. The war with Iran exacerbated these pressures through energy price volatility and supply chain disruptions, creating additional headwinds for price stability.

Warsh's approach to the meeting was notably unconventional—he declined to submit his own rate projection, an unusual move that may have been intended to signal a period of observation and assessment before steering the committee definitively. This departure from standard practice left markets parsing the dot plot with even greater scrutiny, as investors sought clues about the new chairman's ultimate policy preferences.

Market Reaction: Stocks Slide, Yields Surge

Financial markets responded swiftly and decisively to the Fed's hawkish messaging, with equity indices suffering sharp declines while Treasury yields climbed across the curve. The S&P 500 and Nasdaq plummeted in immediate reaction to the FOMC statement and subsequent press conference, as traders recalibrated their expectations for corporate earnings in a higher-for-longer interest rate environment.

The yield curve steepened notably, with short-dated Treasuries bearing the brunt of the selling pressure. Two-year yields climbed to their highest levels since early 2025, reflecting market pricing that now incorporates the possibility of multiple rate increases before year-end. This repricing has significant implications for everything from mortgage rates to corporate borrowing costs, potentially cooling sectors that had benefited from expectations of monetary easing.

Perhaps most telling was the reaction in fed funds futures markets. CME FedWatch data, which aggregates market expectations for future rate moves, now shows virtually no probability of rate cuts in 2026—a stark contrast to the beginning of the year when traders were pricing in at least two quarter-point reductions by December. This dramatic shift in forward guidance underscores how seriously markets are taking the Fed's new inflation-fighting resolve.

Inflation at Three-Year High: The Driving Force

The Fed's hawkish turn cannot be understood without examining the inflation dynamics that compelled this shift. Consumer price metrics have climbed steadily throughout 2026, reaching levels not seen since the post-pandemic surge of 2022-2023. While the headline numbers grab attention, it's the breadth and persistence of price pressures that have clearly alarmed policymakers.

Energy prices have played an outsized role in recent inflation readings, with the conflict involving Iran creating volatility in global oil markets. Though a recent peace agreement has brought some relief—with Brent crude falling to around $77 per barrel from higher levels seen during peak tensions—the pass-through effects of earlier price spikes continue to ripple through the economy. Transportation costs, manufacturing inputs, and agricultural commodities have all felt the impact.

Beyond energy, shelter costs remain elevated despite some moderation in housing market activity. The lagged nature of rent adjustments means that earlier increases in home prices and market rents continue feeding into inflation metrics. Meanwhile, services inflation has proven stickier than goods inflation, with wage growth in certain sectors sustaining price pressures even as supply chain disruptions have eased for physical products.

For investors looking to hedge against inflation while positioning for potential rate hikes, exploring AI-driven stock picking capabilities can help identify opportunities in sectors that historically outperform during tightening cycles.

The Dot Plot Divide: Reading Between the Lines

The quarterly Summary of Economic Projections, with its famous dot plot showing individual policymakers' rate expectations, revealed a committee far from unified in its outlook. This divergence of views offers valuable insight into the debates occurring behind closed doors and the uncertainty surrounding the economic trajectory.

Nine officials projecting at least one rate hike suggests a working majority convinced that current policy remains too accommodative given inflation realities. These policymakers likely view the natural rate of interest as having risen structurally, requiring a more restrictive stance to achieve price stability. Their projections imply confidence that the economy can withstand higher rates without tipping into recession—a sanguine view that not all committee members share.

Eight officials expecting no change may represent those concerned about financial stability risks or the potential for overtightening. They likely point to signs of cooling in certain sectors, tightness in credit markets, and the long lags through which monetary policy affects the economy as reasons for patience. The single official projecting a rate cut appears to hold a distinctly dovish view, perhaps anticipating that inflation will moderate naturally as base effects and supply improvements take hold.

Implications for Investors and Portfolios

The Fed's pivot toward potential rate hikes carries profound implications for investment strategy across asset classes. Portfolios constructed around the assumption of monetary easing may face headwinds, while those positioned for a higher-rate environment stand to benefit. Understanding these dynamics is essential for navigating the months ahead.

In equity markets, rate-sensitive sectors face particular pressure. Growth stocks, especially those with valuations dependent on distant future cash flows, typically suffer when discount rates rise. Real estate investment trusts and utilities, prized for their dividend yields, become less attractive when Treasury bonds offer competitive returns with lower risk. Conversely, financials may benefit from wider net interest margins, while energy and materials companies often outperform during inflationary periods.

Fixed income investors face a challenging landscape. Bond prices move inversely to yields, meaning that even the prospect of rate hikes puts downward pressure on existing holdings. The yield curve's steepening suggests that short-duration bonds may offer better risk-adjusted returns than their longer-maturity counterparts. For those seeking income, floating-rate instruments and Treasury Inflation-Protected Securities provide mechanisms to benefit from rising rates rather than suffering from them.

For investors seeking professional-grade tools to analyze these market dynamics, consider upgrading to Intellectia AI's premium features for advanced screening and analytics capabilities.

Global Central Bank Coordination and Divergence

The Fed's hawkish turn occurs against a backdrop of varying approaches from other major central banks, creating interesting dynamics in global currency and capital markets. While the European Central Bank and Bank of England have maintained relatively dovish stances, the Bank of Japan has continued its ultra-loose policy, and several emerging market central banks have already been tightening to defend their currencies.

This divergence in monetary policy trajectories has significant implications for exchange rates. A more hawkish Fed typically strengthens the dollar, which can create headwinds for U.S. multinationals while providing relief to emerging markets that had been struggling with dollar-denominated debt servicing. Commodity prices, typically denominated in dollars, may face additional pressure from a stronger greenback.

The coordination question becomes particularly relevant given ongoing geopolitical uncertainties. The recent U.S.-Iran peace agreement, while welcome for stability, has created its own set of economic adjustments as oil markets recalibrate and sanctions regimes are modified. Central banks globally are watching to see how these developments affect inflation dynamics and whether they validate or undermine their current policy stances.

Historical Context: How Previous Hike Cycles Played Out

Understanding how markets have historically responded to Fed tightening cycles provides valuable context for the current environment. While history never repeats exactly, it often rhymes, and previous episodes of rate increases offer insights into potential scenarios ahead.

The most recent tightening cycle, which saw the Fed raise rates from near-zero to over 5% between 2022 and 2023, demonstrated both the resilience and vulnerabilities of markets under restrictive policy. Equities initially declined sharply but recovered as inflation moderated and the economy proved more durable than feared. The vaunted "soft landing"—taming inflation without triggering recession—was ultimately achieved, though not without significant volatility along the way.

Earlier cycles tell more cautionary tales. The rate hikes of the late 1990s preceded the dot-com bust, while the increases leading up to 2007 contributed to the housing market collapse that triggered the global financial crisis. The key variable in each case was not merely the level of rates but the speed of adjustment and the underlying vulnerabilities in financial markets and the real economy. Today's banking sector appears better capitalized, and household balance sheets are generally stronger, suggesting greater resilience—but complacency remains dangerous.

Looking Ahead: What to Watch in Coming Months

As markets digest the implications of the Fed's June meeting, several key data points and events will shape the narrative around monetary policy through the remainder of 2026. Investors should maintain focus on these catalysts while avoiding overreaction to any single data point.

Inflation reports, particularly the Consumer Price Index and Personal Consumption Expenditures price index, will carry heightened importance as the Fed seeks validation that its policy stance is appropriately calibrated. Any acceleration in price pressures would likely cement the case for hikes, while sustained moderation might allow the committee to maintain its current stance. Employment data remains crucial as well, with the Fed monitoring for signs that tight monetary policy is translating into labor market weakness.

Beyond domestic indicators, geopolitical developments and their impact on commodity markets will influence the inflation outlook. The implementation of the U.S.-Iran peace agreement, including the reopening of the Strait of Hormuz and potential return of Iranian oil to global markets, could provide meaningful relief to energy prices. However, any setbacks in diplomatic progress or new sources of supply disruption could quickly reverse these gains and complicate the Fed's calculus.

For those ready to take their investment analysis to the next level, sign up for Intellectia AI today and access powerful tools for navigating volatile markets.

Conclusion

The Federal Reserve's June 2026 meeting will be remembered as a turning point in monetary policy expectations, marking the moment when markets fully absorbed the reality that the easing cycle many had anticipated would not materialize. Under Kevin Warsh's leadership, the central bank has signaled a renewed commitment to price stability, even at the cost of near-term market volatility.

For investors, the path forward requires recalibrating expectations and portfolios alike. The era of ultra-low interest rates that defined the post-financial crisis period appears definitively over, replaced by a regime where central banks remain vigilant against inflationary pressures. Companies and investment strategies that thrived in the old environment may struggle in the new one, while opportunities will emerge for those positioned to benefit from higher rates and the economic dynamics they create.

The divergence within the FOMC itself—reflected in the split dot plot projections—suggests that policy uncertainty will persist, creating both risks and opportunities for active investors. Rather than attempting to predict the precise path of rates, prudent portfolio construction should account for multiple scenarios, maintaining flexibility to adapt as the economic picture clarifies. In this environment, discipline, diversification, and a focus on fundamentals will serve investors better than speculation about central bank timing.

Ready to navigate these complex market conditions with confidence? Start your journey with Intellectia AI's comprehensive platform and unlock the tools you need to make informed investment decisions in any monetary policy environment.