Key Takeaway

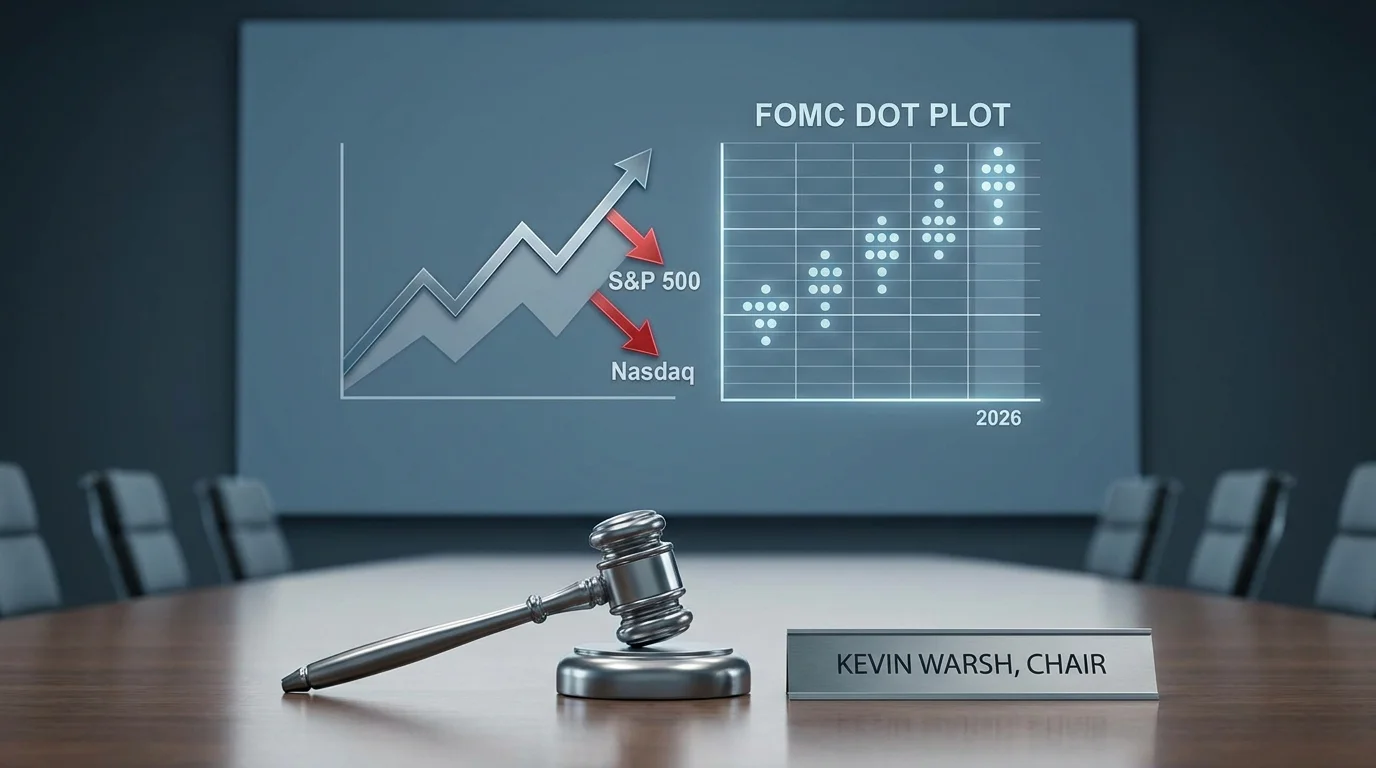

The Federal Reserve's June 2026 meeting delivered a seismic shock to financial markets as new Fed Chair Kevin Warsh presided over his first Federal Open Market Committee (FOMC) gathering, signaling a dramatic shift toward hawkish monetary policy that caught investors off guard. While the central bank maintained the federal funds rate at its current 3.50% to 3.75% range, the updated Summary of Economic Projections revealed that nine of eighteen Fed officials now anticipate at least one rate hike before year-end, with six of those policymakers expecting multiple increases.

This unexpected pivot triggered immediate and severe market reactions, with the S&P 500 plummeting 1.2% to close at 7,420.72, the tech-heavy Nasdaq Composite shedding 1.4% to finish at 26,021.66, and the Dow Jones Industrial Average declining 1% to settle at 51,493.16. Treasury yields surged as traders rapidly repriced their expectations for monetary policy, reflecting growing concern that the Fed may prioritize taming inflation over supporting asset prices. The meeting marks a significant departure from the dovish stance markets had grown accustomed to, potentially ushering in a new era of tighter financial conditions that could reshape investment strategies across all asset classes.

For investors navigating this shifting landscape, understanding the nuances of the Fed's evolving stance and its implications for portfolio positioning has become paramount. The combination of persistent inflation pressures, now at a three-year high with May CPI registering 4.2% year-over-year, and the central bank's renewed commitment to price stability suggests that volatility may remain elevated as markets adjust to this new paradigm.

The Hawkish Pivot: Understanding the Fed's June 2026 Decision

A New Era Under Kevin Warsh

Kevin Warsh's inaugural FOMC meeting as Federal Reserve Chairman represented more than a routine policy decision—it signaled a potential transformation in how the world's most influential central bank approaches monetary policy. Warsh, who assumed leadership of the Fed amid mounting inflationary pressures and growing concerns about asset bubbles, wasted little time distinguishing his approach from that of his predecessors. In a striking departure from tradition, Warsh announced that the Fed has "dropped" its forward guidance entirely, declaring during his post-meeting press conference that he "can't give you any guidance on what we're going to do next."

This elimination of forward guidance represents a fundamental break from the communication strategy that has defined Fed policy for over a decade. By removing the predictive framework that markets had relied upon to anticipate policy moves, Warsh has effectively introduced a new era of uncertainty that demands investors pay closer attention to incoming economic data rather than central bank rhetoric. The approach aligns with Warsh's reputation as a more hawkish policymaker who has historically expressed concerns about the unintended consequences of prolonged monetary accommodation.

The market's reaction to this communication shift was immediate and unambiguous. Equity futures, which had traded relatively flat ahead of the decision, sold off sharply as traders digested the implications of a Fed that may be less predictable and more reactive to inflation data than in recent years. This uncertainty premium manifested across asset classes, with the CBOE Volatility Index (VIX) spiking as investors scrambled to adjust their positioning for a potentially more volatile monetary policy environment.

The Dot Plot Revelation

Perhaps the most consequential element of the June meeting was the updated dot plot, which provides individual policymakers' projections for the appropriate federal funds rate path. The median projection now indicates expectations for 0.25% of rate hikes in 2026, followed by an equivalent amount of cuts in 2027. While this may appear modest at first glance, the distribution of views among committee members tells a more compelling story.

Nine of eighteen Fed officials—exactly half the committee—now anticipate at least one rate increase this year, with six of those policymakers projecting multiple hikes. This represents a dramatic shift from the previous dot plot, which had suggested a baseline scenario of steady rates through 2026. The implications are profound: the Fed is no longer merely considering the possibility of tighter policy but is actively positioning for a scenario in which borrowing costs rise further from already elevated levels.

The divergence of views among committee members also merits attention. While nine officials anticipate hikes, the remaining nine expect rates to remain steady or even decline slightly. This split reflects the genuine uncertainty surrounding the economic outlook, with policymakers weighing competing signals about inflation persistence against concerns about economic growth momentum. The Fed also modestly reduced its economic growth projections, trimming expectations from 2.4% to 2.2%, suggesting that policymakers are acknowledging the trade-off between fighting inflation and supporting expansion.

Market Impact: Sectors Hit Hardest by Rate Hike Fears

Tech Stocks Lead the Decline

The technology sector bore the brunt of the market's negative reaction to the Fed's hawkish pivot, with high-growth stocks experiencing particularly severe drawdowns as investors recalibrated their valuations for a higher interest rate environment. The Nasdaq Composite's 1.4% decline masked even more dramatic individual stock movements, as the market's most beloved technology names faced relentless selling pressure.

Nvidia (NVDA), which had been riding a wave of artificial intelligence enthusiasm, slid 2.4% as investors questioned whether the stock's lofty valuation could be sustained in an environment of rising discount rates. Advanced Micro Devices (AMD) fared even worse, plummeting 7.3% as concerns about semiconductor demand intersected with broader fears about tech sector profitability in a higher-rate world. Other chip stocks suffered similar fates, with Broadcom declining 4.4% and Micron Technology dropping 6.2%.

The selloff in mega-cap technology names was equally pronounced. Microsoft (MSFT) fell 1.44% to $393.99, while Tesla (TSLA) dropped 1.55% as investors grew wary of the company's sensitivity to consumer financing costs. Even Meta Platforms (META), which had shown resilience earlier in the week, succumbed to selling pressure as the session progressed. The rotation out of high-multiple growth stocks and into more defensive sectors accelerated, reflecting a fundamental repricing of risk assets for a tighter monetary policy regime.

Financials and Defensives Show Resilience

While technology stocks cratered, the market's reaction was far from uniform. Financial stocks demonstrated notable resilience, with the sector benefiting from expectations that higher rates would improve net interest margins for banks and other lenders. The divergence between the Dow Jones Industrial Average, which had hit record highs earlier in the week, and the Nasdaq Composite highlighted the rotational nature of the market's response to the Fed's messaging.

Traditional value sectors including utilities, consumer staples, and healthcare outperformed as investors sought shelter from the volatility engulfing growth stocks. This defensive rotation represents a classic response to tightening monetary policy, as investors gravitate toward companies with stable cash flows and pricing power that can weather economic uncertainty. The yield curve steepening that accompanied the Fed's announcement also provided some support for financial stocks, as the spread between short-term borrowing costs and long-term lending rates widened.

SpaceX, which had been trading like a "$2 trillion meme stock" following its record IPO, saw its winning streak snapped as the broader market turmoil affected even the most speculative corners of the equity market. The company's shares, which had advanced 4.8% earlier in the week, gave back some of those gains as risk appetite diminished across the investment landscape.

Treasury Yields Surge: The Bond Market's Verdict

The Yield Curve Response

The fixed income market delivered its own emphatic verdict on the Fed's hawkish turn, with Treasury yields surging across the curve as traders rapidly repriced their expectations for the path of monetary policy. The yield on the benchmark 10-year Treasury note climbed sharply, reflecting both inflation expectations and term premiums associated with greater policy uncertainty.

This yield surge has significant implications for asset allocation decisions. Higher Treasury yields increase the attractiveness of risk-free government debt relative to equities, potentially drawing capital away from stocks and into bonds. For income-focused investors, the improved yields offer a more compelling alternative to dividend-paying stocks, particularly in sectors where payout ratios have become stretched.

The yield curve's shape also warrants attention. Steepening at the long end suggests that markets are pricing in either higher inflation expectations or increased uncertainty about the Fed's ultimate terminal rate. This environment can be challenging for borrowers, particularly those with floating-rate debt or upcoming refinancing needs, while benefiting savers and fixed-income investors who have endured years of near-zero yields.

Corporate Credit Spreads Widen

As Treasury yields climbed, spreads on corporate bonds widened modestly, reflecting growing concerns about credit risk in a higher-rate environment. Companies with significant debt loads or those facing near-term maturities may face higher refinancing costs, potentially squeezing profit margins and limiting financial flexibility.

For investors in corporate credit, this spread widening creates both challenges and opportunities. While existing bondholders may experience mark-to-market losses, the higher yields now available offer improved compensation for assuming credit risk. Selective opportunities may emerge in sectors with strong balance sheets and stable cash flows, particularly if spread widening becomes overdone in certain market segments.

Investment Strategies for the New Fed Regime

Reassessing Growth vs. Value

The Fed's hawkish pivot demands a fundamental reassessment of portfolio positioning, particularly regarding the growth versus value debate that has dominated equity markets for years. The prospect of higher rates and increased volatility challenges the valuation assumptions that have supported premium multiples for high-growth technology stocks, while potentially benefiting more attractively valued cyclical and defensive sectors.

Investors may want to consider rebalancing toward value-oriented strategies that have historically outperformed during periods of tightening monetary policy. Sectors such as financials, energy, and industrials often demonstrate resilience in rising rate environments, benefiting from improved pricing power, better net interest margins, and stronger economic activity. The valuation gap between growth and value stocks, which had narrowed significantly in recent years, may begin to widen again as discount rates rise.

For those seeking to navigate this rotation systematically, Intellectia AI's AI stock screener provides sophisticated filtering capabilities to identify value opportunities across sectors and market capitalizations. By leveraging AI-powered analysis, investors can quickly surface attractively valued stocks with strong fundamentals that may be well-positioned for the new monetary policy environment.

Fixed Income Repositioning

The surge in Treasury yields creates opportunities for fixed income investors who have been starved for income in the ultra-low rate environment of recent years. However, duration management becomes critical in a rising rate environment, as longer-maturity bonds face the greatest price sensitivity to yield movements.

Strategies to consider include shortening portfolio duration to reduce interest rate risk, exploring floating-rate securities that benefit from rising benchmark rates, and selectively adding credit exposure where spreads offer adequate compensation for default risk. For investors with longer time horizons, the current yield levels may represent an attractive entry point for building income-generating positions that can provide stable cash flows regardless of near-term price volatility.

Alternative Assets and Diversification

The increased uncertainty surrounding Fed policy reinforces the importance of diversification across asset classes. Alternative investments including real estate, commodities, and infrastructure may offer portfolio benefits as traditional stock-bond correlations shift in response to changing monetary policy dynamics.

Commodities, in particular, may benefit from the inflationary pressures that appear to be motivating the Fed's hawkish turn. While the central bank is attempting to contain price increases through tighter policy, the lag between policy implementation and economic impact means inflation may remain elevated for some time, potentially supporting commodity prices.

What's Next: The Path Forward for Fed Policy

Data Dependency Takes Center Stage

With forward guidance effectively abandoned, incoming economic data will assume even greater importance in shaping market expectations for Fed policy. Employment reports, inflation readings, and consumer spending data will be scrutinized for clues about the committee's likely next moves, with each release potentially triggering significant market volatility.

The July and September inflation reports will be particularly consequential, as they will provide the first post-meeting readings on price pressures that could either validate or challenge the Fed's hawkish pivot. Should inflation remain stubbornly above the Fed's 2% target, pressure for additional tightening will intensify. Conversely, signs of cooling price pressures could prompt a reassessment of the rate hike trajectory.

Global Central Bank Coordination

The Fed's shift toward tighter policy occurs against a backdrop of diverging global monetary policy stances. While the European Central Bank and Bank of Japan have maintained more accommodative postures, the Fed's hawkish turn may create pressure for other central banks to follow suit to prevent currency depreciation and imported inflation.

This potential for coordinated global tightening raises the risk of synchronized economic slowing, as major economies simultaneously withdraw monetary stimulus. Investors should monitor developments from other central banks closely, as policy divergence or convergence will have significant implications for currency markets, international equity performance, and global growth prospects.

For investors seeking to stay ahead of these complex dynamics, Intellectia AI's AI stock picker offers intelligent recommendations based on real-time analysis of market conditions, central bank communications, and economic data releases. This proactive approach to portfolio management can help identify opportunities and risks as the monetary policy landscape evolves.

Conclusion

The Federal Reserve's June 2026 meeting marked a watershed moment for financial markets, as Kevin Warsh's first FOMC gathering as Chair signaled a decisive shift toward hawkish monetary policy that caught many investors unprepared. The combination of eliminated forward guidance, an unexpectedly hawkish dot plot, and renewed emphasis on price stability has created a new investment environment characterized by higher volatility, rising yields, and sector rotation away from growth stocks toward value and defensive sectors.

For investors, the implications are clear: the era of predictable, dovish central banking that supported ever-rising asset prices appears to be giving way to a more challenging environment where monetary policy uncertainty and inflation fighting take precedence. Portfolio strategies that thrived in the low-rate, high-liquidity conditions of recent years may require significant adjustment to navigate successfully the terrain ahead.

The path forward demands vigilance, flexibility, and a willingness to challenge assumptions that may no longer be valid in this evolving monetary policy regime. By staying informed about Fed communications, monitoring incoming economic data closely, and maintaining diversified exposure across asset classes and sectors, investors can position themselves to weather the volatility while capitalizing on opportunities that emerge during periods of market dislocation.

To enhance your investment research capabilities and make more informed decisions in this complex environment, consider signing up for Intellectia AI today. Our AI-powered platform provides the sophisticated analysis tools and real-time insights necessary to navigate changing market conditions and identify opportunities across all market environments.