Key Takeaway

The Federal Reserve's June 17, 2026 meeting marked a watershed moment for financial markets as Kevin Warsh chaired his first Federal Open Market Committee session, delivering a decisively hawkish surprise that caught many investors off guard. While the central bank held its benchmark interest rate steady at the widely expected range of 3.50% to 3.75%, the devil was in the details of the quarterly Summary of Economic Projections and the controversial dot plot that revealed a significant shift in policymakers' thinking.

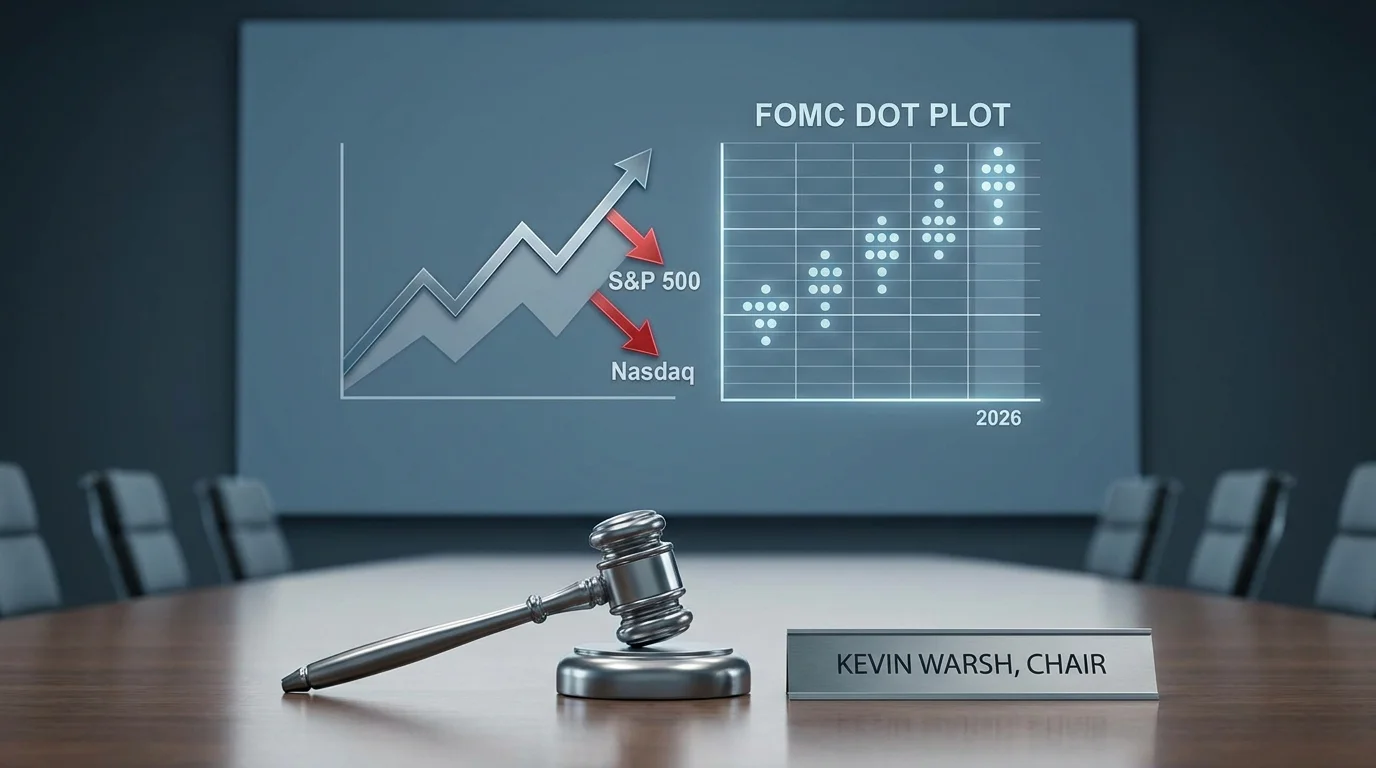

Nine of the eighteen voting FOMC members now project at least one interest rate increase before the end of 2026, with six officials penciling in two quarter-point hikes. This marks a dramatic departure from the March projections, where the consensus pointed toward rate cuts rather than increases. Perhaps even more telling was Chair Warsh's unprecedented decision to abstain from submitting his own rate projection, breaking with decades of tradition and signaling a potential overhaul of how the Fed communicates with markets.

For investors, the implications are profound. Treasury yields surged immediately following the announcement, with the 2-year yield jumping more than 16 basis points to 4.216%, while major equity indices reversed earlier gains to close lower. The SPDR S and P 500 ETF (SPY) slipped 1%, the Invesco QQQ Trust (QQQ) declined approximately 0.5%, and the SPDR Dow Jones Industrial Average ETF Trust (DIA) fell 1%, erasing what had been record intraday highs for the Dow. This market reaction underscores the genuine uncertainty now surrounding monetary policy trajectories and the potential for tighter financial conditions ahead.

The Warsh Era Begins: A New Chapter for Federal Reserve Policy

Kevin Warsh's ascension to the Federal Reserve Chairmanship represents more than just a personnel change; it signals a potential philosophical transformation in how the central bank approaches monetary policy and market communication. Warsh, who previously served as a Fed Governor from 2006 to 2011, has long been critical of the Fed's quantitative easing programs and has advocated for a more rules-based approach to interest rate setting.

Breaking Tradition: The Missing Dot

In a move that sent ripples through financial markets, Chair Warsh chose not to submit his own interest rate projection for the quarterly dot plot, making the committee's outlook harder for investors to interpret. This decision breaks with decades of tradition where the Fed Chair has always participated in the projections, effectively serving as a lodestar for the committee's collective thinking.

Analysts at Goldman Sachs and JPMorgan Chase characterized this FOMC meeting as significantly more hawkish than markets had anticipated, with particular emphasis on the fact that half of the voting members now support rate hikes this year. The abstention raises important questions about Warsh's strategic vision: Is this a one-time occurrence as the new Chair finds his footing, or does it presage a more fundamental restructuring of how the Fed communicates policy intentions?

Task Forces for Operational Overhaul

Beyond the immediate rate decision, Warsh announced the formation of task forces to overhaul major Federal Reserve operations, suggesting that changes to the central bank's communication framework may be just the beginning. These task forces will examine everything from the Fed's balance sheet management to its inflation targeting regime, potentially setting the stage for more substantial reforms in the months ahead.

Reading the Dot Plot: Nine Hawks vs. Nine Doves

The quarterly dot plot has always been one of the most closely scrutinized elements of any FOMC meeting, and the June 2026 edition did not disappoint. The distribution of projections revealed a committee genuinely split about the appropriate path for monetary policy, with profound implications for asset prices across markets.

The Shift in Policy Trajectory

The most striking aspect of the new dot plot is the dramatic shift from March projections. Where previously the median expectation pointed toward rate cuts, the June projections show a clear bias toward tightening. Nine officials now see rates ending 2026 higher than the current 3.50% to 3.75% range, while the remaining nine project rates to remain unchanged or see only modest adjustments.

This division reflects genuine uncertainty about the economic outlook and the persistence of inflationary pressures. The six officials projecting two 25-basis-point hikes by year-end appear to be responding to the Fed's upgraded inflation forecasts, which now see headline inflation at 3.6% and core inflation at 3.3% by the end of 2026, significantly above the previous projections of 2.7%.

Market Pricing Adjusts

Futures markets had entered the June meeting pricing a 97% probability of no rate change, but the post-meeting pricing tells a different story for the remainder of the year. Current market pricing now suggests rates could reach 3.8% by September 2026 and approach 4% by year-end, implying at least one rate increase is now considered likely.

This repricing has significant implications across asset classes. Higher interest rates for longer generally favor financial stocks and value-oriented sectors while placing pressure on growth stocks and long-duration assets. The sharp reaction in Treasury yields, particularly at the front end of the curve, reflects this fundamental reassessment of monetary policy expectations.

Inflation Concerns Take Center Stage

The Fed's upgraded inflation projections represent perhaps the most concerning development from the June meeting for both policymakers and investors. After years of forecasting that inflation would return to the 2% target, the central bank appears to be acknowledging that price pressures may prove more persistent than previously assumed.

Headline vs. Core Dynamics

The divergence between headline and core inflation projections is particularly noteworthy. Headline inflation is now expected to reach 3.6% by year-end, up sharply from the 2.7% projected in March, while core inflation (excluding food and energy) is seen at 3.3%. This gap suggests that the Fed believes energy price volatility and supply chain disruptions will continue to exert upward pressure on consumer prices.

The US-Iran peace agreement, announced just days before the FOMC meeting, may provide some relief on the energy front by reopening trade through the Strait of Hormuz and potentially lowering oil prices. However, Fed officials appear to be looking through this temporary factor, focusing instead on underlying inflation dynamics that show little sign of abating.

Long-Run Rate Expectations

Despite the near-term hawkish shift, Fed officials maintained their long-run expectation for the federal funds rate at 3.1%, suggesting that the current tightening bias is viewed as a cyclical adjustment rather than a permanent shift to higher rate levels. This long-run anchor provides some comfort to investors concerned about a return to the ultra-low rate environment of the 2010s, while also suggesting that rates are unlikely to reach the heights of previous hiking cycles.

Market Impact: Stocks Slide, Yields Surge

The immediate market reaction to the June FOMC decision was swift and unambiguous, with risk assets selling off and fixed income markets repricing sharply higher in yield terms. This reaction reflects the genuine uncertainty now surrounding the policy path and the potential for tighter financial conditions to weigh on economic growth.

Equity Market Response

All three major U.S. equity indices reversed earlier gains to close lower following the Fed announcement. The Dow Jones Industrial Average, which had reached a fresh all-time intraday record above 52,000 on optimism about the Iran peace deal, closed down 0.98% at 51,492.55. Financial stocks, which had been buoyed by the prospect of improved capital markets activity, gave up significant portions of their earlier gains.

JPMorgan Chase, which had surged 3.69% to $331.18 in the session's early trading, finished well off its highs despite still posting gains for the day. Goldman Sachs and Morgan Stanley similarly retreated from intraday records, though all three major banks maintained positive closes. This price action suggests that while higher rates benefit bank net interest margins, the potential for slower economic growth and reduced deal flow presents offsetting headwinds.

Fixed Income Repricing

The Treasury market experienced its most significant repricing in months, with yields rising sharply across the curve. The 2-year yield's 16-basis-point jump to 4.216% was particularly notable, as this maturity is most sensitive to near-term Fed policy expectations. The iShares 20+ Year Treasury Bond ETF (TLT) also faced selling pressure as investors reassessed the outlook for longer-duration assets.

This yield curve steepening has important implications for borrowing costs across the economy, from mortgage rates to corporate bond yields. If sustained, higher long-term rates could begin to dampen housing market activity and corporate capital expenditure plans, potentially achieving some of the Fed's desired tightening through financial conditions rather than direct policy rate increases.

Sector Winners and Losers

Not all sectors responded equally to the Fed's hawkish pivot, creating both opportunities and risks for active investors. Understanding these differential impacts is crucial for portfolio positioning in the months ahead.

Financials: Mixed Blessing

The financial sector presents perhaps the most complex investment case in a rising rate environment. On one hand, higher interest rates directly improve bank net interest margins and profitability. JPMorgan, Goldman Sachs, and Visa all benefited from this dynamic in the immediate aftermath of the Fed decision, with Visa climbing 2.92% to $333.26 alongside the broader financial rally.

However, the prospect of higher rates for longer also raises concerns about credit quality and loan demand. If the Fed's tightening ultimately slows economic growth, banks could face higher loan loss provisions and reduced investment banking activity. This tension explains why financial stocks, despite opening sharply higher, finished well off their best levels of the session.

Technology and Growth Stocks

Growth-oriented sectors, particularly technology, faced the most pressure from the Fed's hawkish shift. The Nasdaq 100's underperformance relative to the broader market reflects the sector's sensitivity to discount rate changes, as the present value of future earnings declines when rates rise.

Companies with minimal current profitability but strong growth expectations are most vulnerable to this dynamic, as their valuations depend heavily on earnings projections far into the future. Investors in these names should be prepared for continued volatility as markets digest the implications of potentially higher rates through 2026 and beyond.

Investment Implications and Portfolio Strategy

The June 2026 FOMC meeting marks a potential inflection point for investment strategy, requiring investors to reassess assumptions about monetary policy, inflation, and asset class performance. Several key themes emerge from the Fed's hawkish pivot that should inform portfolio positioning.

Duration Risk Management

The sharp repricing in Treasury yields serves as a reminder of the risks inherent in long-duration fixed income positions. Investors holding significant allocations to long-term bonds should consider whether their duration exposure remains appropriate given the changed policy outlook. Shorter-duration fixed income instruments or floating-rate securities may offer better risk-adjusted returns in the current environment.

For investors seeking income with less interest rate sensitivity, the AI Screener can help identify dividend-paying stocks with strong balance sheets and pricing power that can withstand higher borrowing costs.

Equity Sector Rotation

The market's reaction to the Fed decision reinforces the case for sector rotation toward value-oriented and economically sensitive names. Financials, energy, and industrials may outperform in a higher rate environment, while growth stocks and long-duration assets face headwinds. Within sectors, companies with pricing power and strong cash flow generation should command premium valuations.

The AI Stock Picker provides data-driven analysis of sector trends and individual stock selection, helping investors navigate the rotation from growth to value that typically accompanies rising interest rates.

Inflation Protection

With the Fed acknowledging that inflation may prove more persistent than previously expected, investors should consider whether their portfolios provide adequate inflation protection. Real assets, commodities, and Treasury Inflation-Protected Securities (TIPS) may warrant increased allocations for investors concerned about purchasing power erosion.

Companies with strong pricing power and the ability to pass cost increases to consumers also serve as implicit inflation hedges. The market's reaction to the Fed's upgraded inflation forecasts suggests that investors are beginning to price in a higher inflation regime, making these considerations increasingly urgent.

Conclusion

The June 2026 Federal Reserve meeting will be remembered as the moment when Kevin Warsh's Chairmanship truly began to reshape market expectations for monetary policy. The hawkish pivot revealed in the dot plot, combined with upgraded inflation forecasts and Warsh's unconventional decision to abstain from the projections, has created genuine uncertainty about the path of interest rates through the remainder of the year.

For investors, the key takeaway is that the era of predictable, accommodative monetary policy may be drawing to a close. The Fed's willingness to consider rate hikes despite ongoing economic uncertainties signals a renewed commitment to price stability, even at the potential cost of slower growth. Portfolio positioning should reflect this changed environment, with careful attention to duration risk, sector allocation, and inflation protection.

As markets digest the implications of the June FOMC meeting, volatility is likely to remain elevated. However, for disciplined investors willing to look through short-term noise, the current environment also presents opportunities. Quality companies with strong balance sheets, pricing power, and sustainable competitive advantages should continue to compound value regardless of the precise trajectory of interest rates.

Ready to navigate the new monetary policy landscape? Sign up for Intellectia today to access AI-powered analysis of Fed policy impacts, sector rotation opportunities, and personalized investment insights. Our platform helps you stay ahead of market-moving events like FOMC meetings with real-time analysis and actionable recommendations.