PRI Overview

-

$

0.000

0.000(0.000%)

At close0.000(0.000%)Aft-market

ET

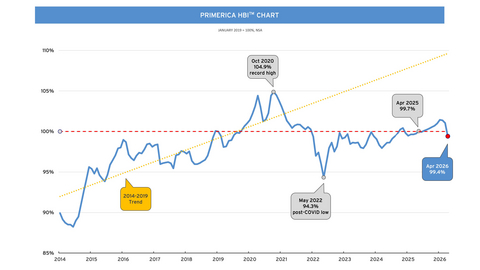

Loading chart...

The current price of PRI is 302.55 USD — it has increased 1.13

Primerica, Inc. is a provider of financial products and services to middle-income households in North America. The Company's segments include Term Life Insurance, Investment and Savings Products, and Corporate and Other Distributed Products. The Company, through its three life insurance subsidiaries, Primerica Life Insurance Company, National Benefit Life Insurance Company and Primerica Life Insurance Company of Canada (Primerica Life Canada), offers term life insurance to clients in the United States, its territories, and Canada. The Company, through Primerica Financial Services, LLC; PFS Investments Inc.; Primerica Life Canada; PFSL Investments Canada Ltd., and licensed independent sales representatives, distributes and sells to its clients a range of investment products such as mutual funds; managed investments; variable, index-linked, fixed and fixed indexed annuities, and segregated funds. It distributes other products, including prepaid legal services and mortgage loan referrals.

Wall Street analysts forecast PRI stock price to rise over the next 12 months. According to Wall Street analysts, the average 1-year price target for PRI is303.50 USD with a low forecast of 267.00 USD and a high forecast of 340.00 USD. However, analyst price targets are subjective and often lag stock prices, so investors should focus on the objective reasons behind analyst rating changes, which better reflect the company's fundamentals.

Primerica Inc revenue for the last quarter amounts to 872.69M USD, increased 8.43

Primerica Inc. EPS for the last quarter amounts to 5.97 USD, increased 18.22

Primerica Inc (PRI) has 2301 emplpoyees as of July 08 2026.

Today PRI has the market capitalization of 9.43B USD.