Wall Street Traders Anticipate Strong Potential for Year-End Stock Surge Fueled by FOMO

Market Trends: Traders on Wall Street suggest that stocks may rise towards the end of the year due to under-invested participants driven by fear of missing out (FOMO) and favorable market conditions related to artificial intelligence and deregulation.

Retail vs. Institutional Investors: Retail investors are currently the primary price setters in the market, actively buying, while institutional investors are seen as under-exposed.

Positive Market Indicators: Morgan Stanley highlights positive developments outside the AI sector, noting strength in global banking and a revival in the real economy, as evidenced by the performance of the Invesco KBW Bank ETF and the iShares Transportation Average ETF.

Retail Investor Activity: Recent data from JPMorgan indicates that retail investors have been consistently buying into the market, contributing to a strong overall market performance, with the S&P 500 up over 16% in 2025.

Trade with 70% Backtested Accuracy

Analyst Views on MS

About MS

About the author

Morgan Stanley Invests in 932 MW Power Project

- Investment Overview: Morgan Stanley Infrastructure Partners announces an investment in the 932-megawatt gas-fired combined cycle power generation project, Greenlight, located in Sturgeon County, Alberta, reflecting its strategic focus on North American electricity markets.

- Ownership Structure: Morgan Stanley and Pembina Pipeline Corporation will each hold a 47.5% stake in the Greenlight project, while Kineticor Asset Management retains the remaining 5%, facilitating effective project management and execution.

- Market Demand Response: The project is expected to provide long-term, reliable power to meet the growing electricity demand driven by artificial intelligence and data centers, further solidifying Morgan Stanley's position in critical infrastructure investments.

- Construction Management Advantage: Pembina will serve as the construction and operations manager, leveraging its local expertise in delivering large-scale infrastructure projects to ensure the efficient implementation and operation of the Greenlight project.

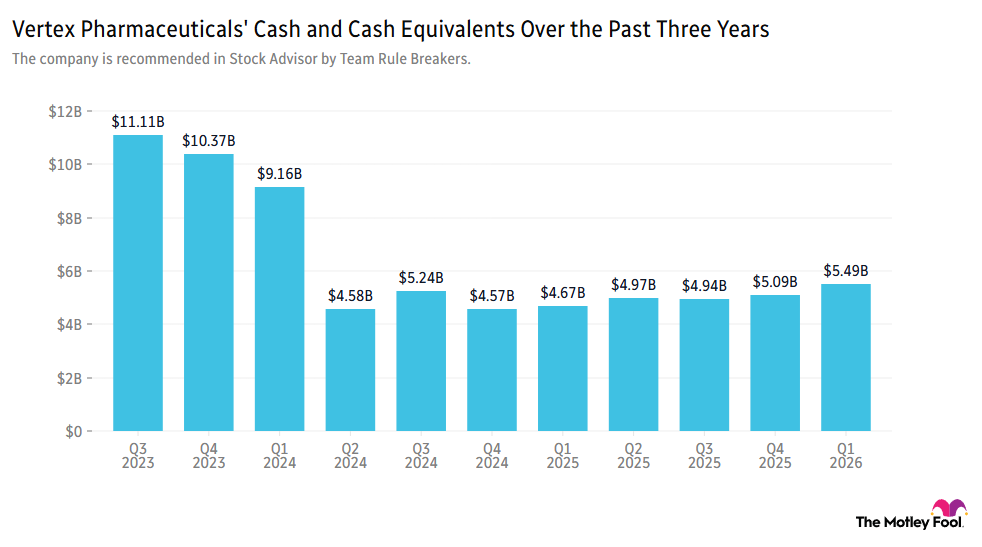

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Rocket Lab Acquires Iridium, Poised for Significant Growth

- Massive Market Potential: Morgan Stanley forecasts that the global space industry could exceed $1 trillion by 2040, positioning Rocket Lab as a promising player in this rapidly growing sector with significant revenue opportunities over the coming decades.

- Acquisition Fuels Growth: Rocket Lab's acquisition of Iridium Communications for $8 billion, which serves 2.55 million subscribers globally, enhances its competitive edge in satellite manufacturing and launch services, directly challenging SpaceX's Starlink business segment.

- Launch Capability Enhancement: The development of Rocket Lab's Neutron rocket, designed for larger payloads, is underway and expected to launch in 2026, with 70 missions already booked, indicating strong market demand and growth potential.

- Optimistic Financial Outlook: Rocket Lab is projected to generate approximately $1.8 billion in revenue by 2026, including Iridium's contributions, showcasing robust growth prospects in the space economy, despite its current market cap of $58 billion reflecting a high valuation that may impact short-term performance.

Rocket Lab's Iridium Acquisition Fuels Growth Potential

- Reusable Rocket Advantage: Rocket Lab's Neutron rocket positions the company to compete more effectively against SpaceX, enhancing its market share and strengthening its standing in the launch services sector.

- Revenue Growth Potential: The acquisition of Iridium Communications is expected to boost Rocket Lab's total revenue to approximately $1.8 billion in 2026, including Iridium's $871 million revenue, indicating strong growth prospects.

- Launch Mission Innovation: Rocket Lab has booked more launch missions in the first quarter of 2026 than in all of last year, with a current manifest of 70 missions, marking an all-time high and reflecting robust market demand.

- Market Valuation Challenges: Despite Rocket Lab's market cap of $58 billion, which is over 30 times its estimated 2026 revenue, the rapid growth of the space economy presents significant opportunities for the company, potentially yielding substantial returns for investors.

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

Analysis of Honeywell's Post-Split Performance

- Honeywell Stock Performance: Following its split, Honeywell's combined stock trades around $240, reflecting a 6% increase since late June, indicating market confidence in its future growth, particularly in the aerospace sector.

- Strong Aerospace Division: Honeywell Aerospace shares have surged 15% over the past three sessions, currently priced at approximately $220, with analysts setting a target of $285, highlighting its attractiveness for long-term growth.

- Tech Sector Rebound: As investors rotate back into AI themes, technology stocks, including semiconductors, are rebounding, boosting overall market sentiment against a backdrop of capital outflows from healthcare and consumer retail sectors.

- Goldman and Wells Fargo Performance: Goldman Sachs shares rose over 2%, ranking first in global M&A fees for the first half of 2026, while Wells Fargo's price target was raised, reflecting investor optimism about its trading revenues and upcoming earnings.

Morgan Stanley Invests in 932 MW Power Project

- Investment Overview: Morgan Stanley Infrastructure Partners announces an investment in the 932-megawatt gas-fired combined cycle power generation project, Greenlight, located in Sturgeon County, Alberta, reflecting its strategic focus on North American electricity markets.

- Ownership Structure: Morgan Stanley and Pembina Pipeline Corporation will each hold a 47.5% stake in the Greenlight project, while Kineticor Asset Management retains the remaining 5%, facilitating effective project management and execution.

- Market Demand Response: The project is expected to provide long-term, reliable power to meet the growing electricity demand driven by artificial intelligence and data centers, further solidifying Morgan Stanley's position in critical infrastructure investments.

- Construction Management Advantage: Pembina will serve as the construction and operations manager, leveraging its local expertise in delivering large-scale infrastructure projects to ensure the efficient implementation and operation of the Greenlight project.

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

Rocket Lab Acquires Iridium, Poised for Significant Growth

- Massive Market Potential: Morgan Stanley forecasts that the global space industry could exceed $1 trillion by 2040, positioning Rocket Lab as a promising player in this rapidly growing sector with significant revenue opportunities over the coming decades.

- Acquisition Fuels Growth: Rocket Lab's acquisition of Iridium Communications for $8 billion, which serves 2.55 million subscribers globally, enhances its competitive edge in satellite manufacturing and launch services, directly challenging SpaceX's Starlink business segment.

- Launch Capability Enhancement: The development of Rocket Lab's Neutron rocket, designed for larger payloads, is underway and expected to launch in 2026, with 70 missions already booked, indicating strong market demand and growth potential.

- Optimistic Financial Outlook: Rocket Lab is projected to generate approximately $1.8 billion in revenue by 2026, including Iridium's contributions, showcasing robust growth prospects in the space economy, despite its current market cap of $58 billion reflecting a high valuation that may impact short-term performance.

Rocket Lab's Iridium Acquisition Fuels Growth Potential

- Reusable Rocket Advantage: Rocket Lab's Neutron rocket positions the company to compete more effectively against SpaceX, enhancing its market share and strengthening its standing in the launch services sector.

- Revenue Growth Potential: The acquisition of Iridium Communications is expected to boost Rocket Lab's total revenue to approximately $1.8 billion in 2026, including Iridium's $871 million revenue, indicating strong growth prospects.

- Launch Mission Innovation: Rocket Lab has booked more launch missions in the first quarter of 2026 than in all of last year, with a current manifest of 70 missions, marking an all-time high and reflecting robust market demand.

- Market Valuation Challenges: Despite Rocket Lab's market cap of $58 billion, which is over 30 times its estimated 2026 revenue, the rapid growth of the space economy presents significant opportunities for the company, potentially yielding substantial returns for investors.

Market Update: SpaceX and Coca-Cola Reach New Highs

- SpaceX Joins Nasdaq: SpaceX was fast-tracked into the Nasdaq-100 on Tuesday, closing its first trading day at $160.95, approximately 30% below its June 16 high of $225.64, indicating strong market interest despite the decline.

- Financial Sector Surge: The S&P Financials sector surged 4.5% in the past week and 7.6% over the month, with 82 out of 85 stocks rising last week, led by Robinhood's impressive 43% increase over three months, reflecting renewed investor confidence in financial stocks.

- Coca-Cola Hits New High: Coca-Cola shares have risen 7.4% over the past three months, reaching a new high, while the S&P Staples sector remained flat, showcasing Coca-Cola's robust performance and stable consumer demand in a challenging market.

- Cybersecurity Stocks Reach All-Time Highs: CrowdStrike, Fortinet, and Palo Alto Networks all achieved record highs on Monday, with CrowdStrike up 100%, Fortinet up 97%, and Palo Alto Networks up 121% over three months, highlighting strong market interest and investment in cybersecurity solutions.

Analysis of Honeywell's Post-Split Performance

- Honeywell Stock Performance: Following its split, Honeywell's combined stock trades around $240, reflecting a 6% increase since late June, indicating market confidence in its future growth, particularly in the aerospace sector.

- Strong Aerospace Division: Honeywell Aerospace shares have surged 15% over the past three sessions, currently priced at approximately $220, with analysts setting a target of $285, highlighting its attractiveness for long-term growth.

- Tech Sector Rebound: As investors rotate back into AI themes, technology stocks, including semiconductors, are rebounding, boosting overall market sentiment against a backdrop of capital outflows from healthcare and consumer retail sectors.

- Goldman and Wells Fargo Performance: Goldman Sachs shares rose over 2%, ranking first in global M&A fees for the first half of 2026, while Wells Fargo's price target was raised, reflecting investor optimism about its trading revenues and upcoming earnings.