Vertex Pharmaceuticals Stock Performance Strong

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 18 2026

0mins

Should l Buy VRTX?

Source: CNBC

- Investment Recommendation: Jim Cramer highlighted Vertex Pharmaceuticals' strong stock performance, suggesting that buying early was a good decision, reflecting market confidence in its future growth and potentially attracting more investor interest.

- Industry Challenges: Oddity Tech's performance fell short of expectations, with Cramer admitting he underestimated the industry's complexities, indicating that market confidence in the company may be waning, prompting investors to carefully assess its future potential.

- Risk Assessment: ImmunityBio faces uncertainty, with Cramer emphasizing the need to observe how it resolves current issues, which could impact its stock price trajectory, necessitating vigilance from investors to navigate potential risks.

- Buying Opportunity: Copart is viewed as undervalued, with Cramer suggesting it represents a good buying opportunity, likely attracting investors looking for undervalued stocks and enhancing market interest in the company.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy VRTX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on VRTX

Wall Street analysts forecast VRTX stock price to rise

22 Analyst Rating

17 Buy

5 Hold

0 Sell

Strong Buy

Current: 429.820

Low

414.00

Averages

515.88

High

604.00

Current: 429.820

Low

414.00

Averages

515.88

High

604.00

About VRTX

Vertex Pharmaceuticals Incorporated is a global biotechnology company that invests in scientific innovation to create transformative medicines for people with serious diseases, with a focus on specialty markets. It has seven approved medicines: five that treat the underlying cause of cystic fibrosis (CF), one that treats severe sickle cell disease (SCD) and transfusion dependent beta thalassemia (TDT), and one that treats moderate-to-severe acute pain. Its pipeline includes clinical-stage programs in CF, SCD, beta thalassemia, acute and peripheral neuropathic pain, APOL1-mediated kidney disease, IgA nephropathy and other autoimmune renal diseases and cytopenias, type 1 diabetes, myotonic dystrophy type 1, and autosomal dominant polycystic kidney disease. Its marketed medicines are TRIKAFTA/KAFTRIO (elexacaftor/tezacaftor/ivacaftor and ivacaftor), SYMDEKO/SYMKEVI (elexacaftor/tezacaftor/ivacaftor and ivacaftor), ORKAMBI (lumacaftor/ivacaftor), and KALYDECO (ivacaftor).

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

CRISPR Therapeutics Shows Promising Upside Potential

- Strong Stock Performance: CRISPR Therapeutics' shares have surged 56% over the past year, significantly outperforming the S&P 500's 30% gain, indicating robust market confidence in its growth prospects.

- Optimistic Analyst Targets: According to Yahoo! Finance, CRISPR's average price target is $82.55, suggesting nearly 51% upside from current levels, while Piper Sandler's analyst has set a target of $110, indicating the stock could potentially double in the next 12 months.

- Catalysts from Clinical Trials: The ongoing development of the anticoagulant CTX611 could yield crucial clinical trial data in the coming months, targeting a $20 billion market, and positive results could significantly boost the stock price.

- Market Expansion Potential: The Casgevy drug, developed in collaboration with Vertex Pharmaceuticals, has yet to generate significant sales despite its 2023 approval due to its complex administration and high cost; however, the recent request for approval for children aged 5 to 11 could greatly expand its market potential, with annual revenues expected to exceed $1 billion in the coming years.

See More

Vertex Pharmaceuticals Set to Announce Q2 Earnings on May 11

- Earnings Announcement: Vertex Pharmaceuticals is set to release its Q2 2023 earnings report on May 11 after market close, with consensus EPS estimate at $4.75, reflecting a 5.1% year-over-year increase, and revenue estimate at $3.22 billion, up 8.8% year-over-year.

- Historical Performance Review: Over the past two years, Vertex has exceeded EPS estimates 50% of the time and revenue estimates 63% of the time, indicating a degree of stability in its financial performance amidst market fluctuations.

- Expectation Adjustment Dynamics: In the last three months, EPS estimates have seen 2 upward revisions and 9 downward revisions, while revenue estimates experienced 8 upward revisions and 4 downward revisions, reflecting market uncertainty regarding the company's future performance.

- Long-term Revenue Outlook: Vertex projects revenue for 2026 to be between $12.95 billion and $13.1 billion, while targeting over $500 million from non-CF products, showcasing the company's strategic focus on diversifying its product lines.

See More

Vertex Pharmaceuticals: Investment Returns and Future Outlook

- Significant Investment Returns: An investment of $20,000 in Vertex Pharmaceuticals during its 1991 IPO would now exceed $1 million, reflecting a commendable 14% compound annual growth rate, which outperforms the S&P 500's 11% over the same period, indicating the company's robust long-term growth potential.

- Core Market Dominance: Vertex Pharmaceuticals leads the cystic fibrosis (CF) market, treating approximately 95% of CF patients in the U.S., although its revenue growth has slowed, with an 8% year-over-year increase to $2.99 billion in Q1, suggesting sustained market demand despite challenges.

- Diversification Challenges: While Vertex aims to reduce its reliance on CF, it anticipates $500 million in non-CF revenue this year, a significant increase from $10 million in 2024, yet this growth remains insufficient, highlighting ongoing challenges in its diversification efforts.

- Future Growth Potential: Vertex is seeking approval for Casgevy, a gene-editing drug for sickle cell disease and transfusion-dependent beta-thalassemia, which could drive future growth, alongside advancing povetacicept for IgA nephropathy, showcasing the potential for an expanded product portfolio.

See More

Vertex Pharmaceuticals' Future Outlook Appears Promising

- Core Business Slowdown: Vertex Pharmaceuticals reported an 8% year-over-year revenue increase to $2.99 billion in Q1, which, while not terrible, reflects a general downward trend in growth over recent years, indicating weakness in its core market.

- Non-CF Revenue Potential: The company expects at least $500 million in non-CF revenue for 2023, a significant increase from $10 million in 2024, suggesting that its diversification efforts are beginning to pay off.

- New Drug Development Progress: Vertex is seeking approval for Casgevy, a gene-editing medicine for sickle cell disease and transfusion-dependent beta-thalassemia, aimed at providing early treatment for patients aged 5 to 11, highlighting its significant market potential.

- Future Growth Outlook: As Vertex continues to develop new products in the CF space and expand its portfolio, it is expected to achieve stronger revenue and earnings growth in the coming years, presenting a positive long-term outlook.

See More

Vertex Pharmaceuticals Confident in Renal Franchise

- Renal Business Outlook: Vertex Pharmaceuticals (VRTX) management expresses strong confidence in its emerging renal franchise, indicating that the strategic positioning in this area is beginning to yield results, which is expected to drive future revenue growth.

- Market Potential: With the increasing global demand for treatments for kidney diseases, Vertex's renal product line is poised to capture significant market share in the coming years, thereby enhancing the company's overall competitiveness.

- R&D Investment: The company continues to increase its investment in research and development related to kidney diseases, aiming to meet unmet medical needs through innovative therapies, further solidifying its leadership position in the biopharmaceutical industry.

- Management Confidence: The management's confidence reflects a positive assessment of product development progress, which is expected to attract more investor attention and improve the company's performance in the capital markets.

See More

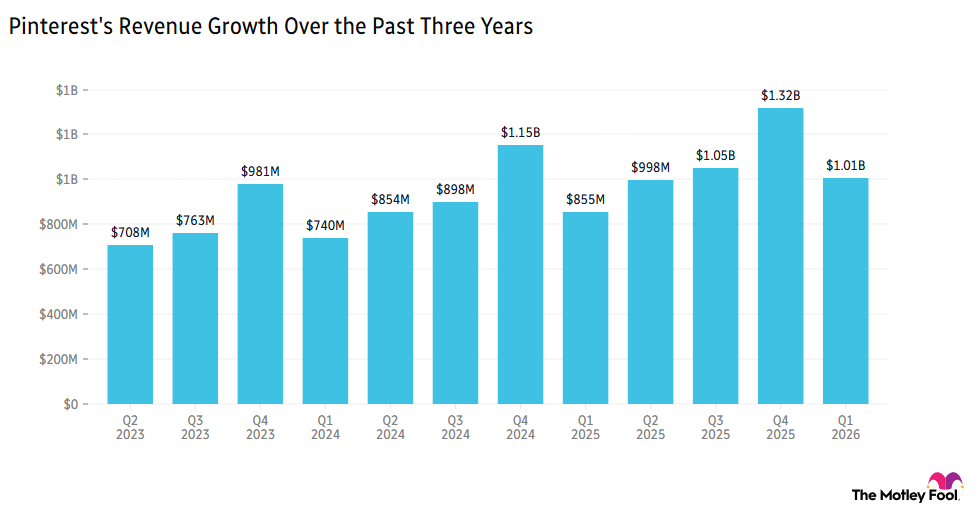

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.

See More

CRISPR Therapeutics Shows Promising Upside Potential

- Strong Stock Performance: CRISPR Therapeutics' shares have surged 56% over the past year, significantly outperforming the S&P 500's 30% gain, indicating robust market confidence in its growth prospects.

- Optimistic Analyst Targets: According to Yahoo! Finance, CRISPR's average price target is $82.55, suggesting nearly 51% upside from current levels, while Piper Sandler's analyst has set a target of $110, indicating the stock could potentially double in the next 12 months.

- Catalysts from Clinical Trials: The ongoing development of the anticoagulant CTX611 could yield crucial clinical trial data in the coming months, targeting a $20 billion market, and positive results could significantly boost the stock price.

- Market Expansion Potential: The Casgevy drug, developed in collaboration with Vertex Pharmaceuticals, has yet to generate significant sales despite its 2023 approval due to its complex administration and high cost; however, the recent request for approval for children aged 5 to 11 could greatly expand its market potential, with annual revenues expected to exceed $1 billion in the coming years.

See More

Vertex Pharmaceuticals Set to Announce Q2 Earnings on May 11

- Earnings Announcement: Vertex Pharmaceuticals is set to release its Q2 2023 earnings report on May 11 after market close, with consensus EPS estimate at $4.75, reflecting a 5.1% year-over-year increase, and revenue estimate at $3.22 billion, up 8.8% year-over-year.

- Historical Performance Review: Over the past two years, Vertex has exceeded EPS estimates 50% of the time and revenue estimates 63% of the time, indicating a degree of stability in its financial performance amidst market fluctuations.

- Expectation Adjustment Dynamics: In the last three months, EPS estimates have seen 2 upward revisions and 9 downward revisions, while revenue estimates experienced 8 upward revisions and 4 downward revisions, reflecting market uncertainty regarding the company's future performance.

- Long-term Revenue Outlook: Vertex projects revenue for 2026 to be between $12.95 billion and $13.1 billion, while targeting over $500 million from non-CF products, showcasing the company's strategic focus on diversifying its product lines.

See More

Vertex Pharmaceuticals: Investment Returns and Future Outlook

- Significant Investment Returns: An investment of $20,000 in Vertex Pharmaceuticals during its 1991 IPO would now exceed $1 million, reflecting a commendable 14% compound annual growth rate, which outperforms the S&P 500's 11% over the same period, indicating the company's robust long-term growth potential.

- Core Market Dominance: Vertex Pharmaceuticals leads the cystic fibrosis (CF) market, treating approximately 95% of CF patients in the U.S., although its revenue growth has slowed, with an 8% year-over-year increase to $2.99 billion in Q1, suggesting sustained market demand despite challenges.

- Diversification Challenges: While Vertex aims to reduce its reliance on CF, it anticipates $500 million in non-CF revenue this year, a significant increase from $10 million in 2024, yet this growth remains insufficient, highlighting ongoing challenges in its diversification efforts.

- Future Growth Potential: Vertex is seeking approval for Casgevy, a gene-editing drug for sickle cell disease and transfusion-dependent beta-thalassemia, which could drive future growth, alongside advancing povetacicept for IgA nephropathy, showcasing the potential for an expanded product portfolio.

See More

Vertex Pharmaceuticals' Future Outlook Appears Promising

- Core Business Slowdown: Vertex Pharmaceuticals reported an 8% year-over-year revenue increase to $2.99 billion in Q1, which, while not terrible, reflects a general downward trend in growth over recent years, indicating weakness in its core market.

- Non-CF Revenue Potential: The company expects at least $500 million in non-CF revenue for 2023, a significant increase from $10 million in 2024, suggesting that its diversification efforts are beginning to pay off.

- New Drug Development Progress: Vertex is seeking approval for Casgevy, a gene-editing medicine for sickle cell disease and transfusion-dependent beta-thalassemia, aimed at providing early treatment for patients aged 5 to 11, highlighting its significant market potential.

- Future Growth Outlook: As Vertex continues to develop new products in the CF space and expand its portfolio, it is expected to achieve stronger revenue and earnings growth in the coming years, presenting a positive long-term outlook.

See More

Vertex Pharmaceuticals Confident in Renal Franchise

- Renal Business Outlook: Vertex Pharmaceuticals (VRTX) management expresses strong confidence in its emerging renal franchise, indicating that the strategic positioning in this area is beginning to yield results, which is expected to drive future revenue growth.

- Market Potential: With the increasing global demand for treatments for kidney diseases, Vertex's renal product line is poised to capture significant market share in the coming years, thereby enhancing the company's overall competitiveness.

- R&D Investment: The company continues to increase its investment in research and development related to kidney diseases, aiming to meet unmet medical needs through innovative therapies, further solidifying its leadership position in the biopharmaceutical industry.

- Management Confidence: The management's confidence reflects a positive assessment of product development progress, which is expected to attract more investor attention and improve the company's performance in the capital markets.

See More

Pinterest Surges on Record User Growth and Positive Revenue Guidance

- Strong User Growth: Pinterest (PINS) surged over 15% ahead of market open, driven by an 11% year-over-year increase in monthly active users (MAU), marking the tenth consecutive quarter of double-digit growth, indicating that enhanced user engagement will support future profitability.

- Optimistic Revenue Guidance: Pinterest's revenue guidance exceeded expectations, with CEO Bill Ready emphasizing the company's commitment to aligning profitability with user engagement, thereby boosting investor confidence and driving stock price increases.

- Positive Market Reaction: Analyst Rich Greifner highlighted that Pinterest's large and engaged user base, characterized by high commercial intent, makes it an attractive platform for advertisers, further solidifying its competitive position in the advertising market.

- Favorable Industry Outlook: As Pinterest's user growth and revenue expectations improve, market confidence in its future performance is likely to attract more investor interest, propelling further development in the social media sector.

See More