Vertex Acquires Crinetics for $85 Per Share in Cash

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 4 hours ago

0mins

Source: NASDAQ.COM

- Acquisition Overview: Vertex has agreed to acquire Crinetics for $85 per share in cash, totaling approximately $10 billion in equity value, with the deal expected to close in Q3 2026, marking a significant expansion into a new disease area for Vertex.

- New Drug Assets: Crinetics brings PALSONIFY, the first and only once-daily oral therapy approved for acromegaly, which is expected to fill a market gap; combined with other candidates, these assets boast over $5 billion in peak sales potential.

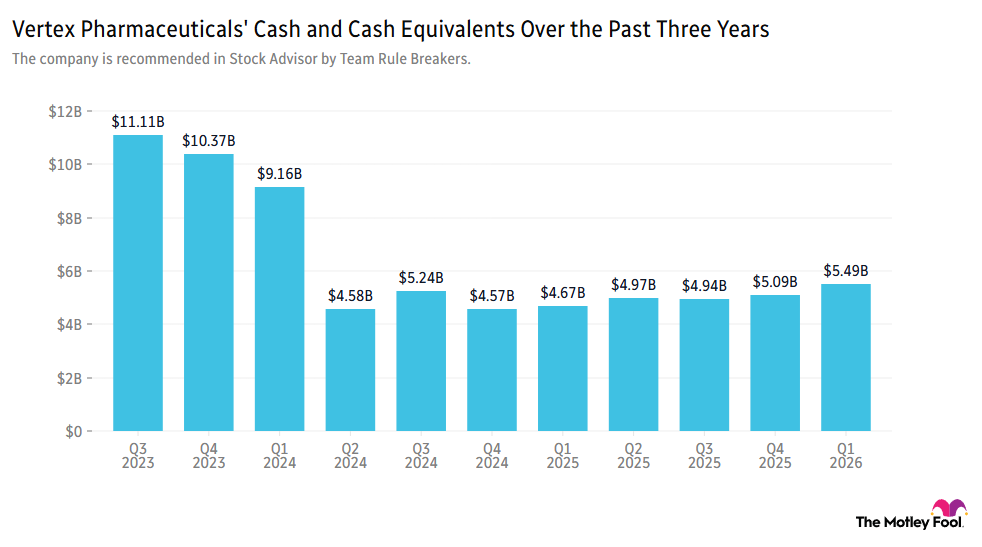

- Financing Structure: The acquisition will be funded through a mix of cash on hand and debt, with Vertex securing $4.5 billion in bridge financing, while holding approximately $13 billion in cash and marketable securities, indicating strong financial health.

- Strategic Implications: This acquisition not only provides Vertex with a new growth engine to meet diversification needs but also aligns with its strategy of targeting serious diseases, with positive impacts on adjusted operating income anticipated by 2029.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy VRTX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on VRTX

Wall Street analysts forecast VRTX stock price to fall

22 Analyst Rating

17 Buy

5 Hold

0 Sell

Strong Buy

Current: 528.040

Low

414.00

Averages

515.88

High

604.00

Current: 528.040

Low

414.00

Averages

515.88

High

604.00

About VRTX

Vertex Pharmaceuticals Incorporated is a global biotechnology company that invests in scientific innovation to create transformative medicines for people with serious diseases, with a focus on specialty markets. It has seven approved medicines: five that treat the underlying cause of cystic fibrosis (CF), one that treats severe sickle cell disease (SCD) and transfusion dependent beta thalassemia (TDT), and one that treats moderate-to-severe acute pain. Its pipeline includes clinical-stage programs in CF, SCD, beta thalassemia, acute and peripheral neuropathic pain, APOL1-mediated kidney disease, IgA nephropathy and other autoimmune renal diseases and cytopenias, type 1 diabetes, myotonic dystrophy type 1, and autosomal dominant polycystic kidney disease. Its marketed medicines are TRIKAFTA/KAFTRIO (elexacaftor/tezacaftor/ivacaftor and ivacaftor), SYMDEKO/SYMKEVI (elexacaftor/tezacaftor/ivacaftor and ivacaftor), ORKAMBI (lumacaftor/ivacaftor), and KALYDECO (ivacaftor).

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Vertex Pharmaceuticals Hits All-Time High Amid Growth Potential

- Strong Stock Performance: Vertex Pharmaceuticals' stock has risen approximately 17% this year, significantly outperforming the S&P 500's 10% return, and has reached an all-time high, indicating strong market confidence in its future prospects.

- Sales Growth Challenges: Despite an 8% year-over-year sales increase totaling around $3 billion, the declining growth rate suggests the company faces short-term growth challenges, prompting investors to carefully assess future potential.

- Valuation Risks: Vertex is currently trading at a price-to-earnings ratio of about 31, well above the S&P 500's 25, and with a PEG ratio of 2.0, indicating that future growth may already be overvalued, posing downside risks.

- Cautious Investment Advice: While Vertex's long-term growth potential is viewed positively, analysts recommend that investors consider other growth stocks with better value due to the current high valuation.

See More

Vertex Pharmaceuticals Signs LOI for Cystic Fibrosis Therapy Access

- LOI for New Therapy: Vertex Pharmaceuticals has signed a Letter of Intent with the pan-Canadian Pharmaceutical Alliance to provide the new triple combination therapy PrALYFTREK for cystic fibrosis patients aged six and older, marking a significant advancement in treatment options for patients.

- Eligible Patients: Approximately 3,800 individuals across Canada are now eligible for ALYFTREK, with up to 60 potentially gaining access to a therapy that addresses the underlying cause of their disease for the first time, highlighting the therapy's potential impact.

- Regulatory Backing: The LOI follows positive reimbursement recommendations from Canada's Drug Agency and INESSS in December 2025 and April 2026, respectively, reflecting regulatory support for innovative medicines and facilitating market access for the therapy.

- Future Discussions: Vertex will engage with provinces and territories to support the public listing of ALYFTREK, a critical step that will enable the therapy to be funded through publicly funded drug programs across Canada, significantly enhancing patient accessibility.

See More

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Fiserv Discusses Sale of Payments Business with Major Banks

- Stock Surge: Fiserv shares rallied over 5% after The Wall Street Journal reported discussions with major banks like JPMorgan and Bank of America regarding the sale of its payments infrastructure business, potentially leading to strategic restructuring and enhanced market competitiveness.

- Acquisition Deal: Vertex Pharmaceuticals announced a $10 billion acquisition of Crinetics Pharmaceuticals to expand its product line in rare hormonal disease treatments, although Vertex shares dipped nearly 1%, this deal is expected to strengthen its market position.

- Stock Upgrade: First Solar's stock rose nearly 3% after Deutsche Bank upgraded its rating from neutral to buy, with analysts citing potential trade policy shifts as a reason for investors to buy the dip, boosting market confidence.

- EV Stock Decline: Rivian shares tumbled 9% despite revenue and delivery guidance exceeding market expectations, as the company announced a plan to sell 75 million new shares for a significant capital raise, negatively impacting investor sentiment.

See More

Sellas Life Sciences Stock Gains Retail Trader Favor Amid Bullish Sentiment

- Retail Trader Enthusiasm: In a poll of 3,400 users, Sellas Life Sciences (SLS) garnered 50% of the votes, significantly outpacing Ondas Holdings at 24% and ImmunityBio at 18%, indicating strong investor confidence in its future potential.

- Clinical Trial Progress: Sellas' Phase 3 Regal trial in acute myeloid leukemia (AML) has reached 78 of the 80 events needed for final analysis, making the next two events critical catalysts that could drive stock price volatility.

- Acquisition Speculation: CEO Angelos Stergiou's optimistic remarks on social media and gratitude towards strategic partners have intensified market speculation regarding potential buyouts, likely attracting more investor interest.

- Significant Market Value Increase: Sellas' market value surged from $73 million at the start of 2024 to over $1.5 billion by mid-2026, reflecting heightened investor attention around the Regal readout, while the company ended Q1 with $107.1 million in cash, showcasing a robust financial position.

See More

Vertex Acquires Crinetics for $85 Per Share in $10 Billion Deal

- Acquisition Overview: Vertex Pharmaceuticals is acquiring Crinetics for $85 per share in cash, totaling approximately $10 billion, or about $8.8 billion net of cash, indicating Vertex's strong strategic intent.

- Significant Stock Reaction: Crinetics' shares surged over 99% in after-hours trading to $83.64, reflecting a positive market response to the acquisition, which may enhance Crinetics' market position.

- Product Line Expansion: The acquisition will provide Vertex with key assets like PALSONIFY (paltusotine) and Atumelnant, which are expected to generate over $5 billion in annual revenue, significantly boosting Vertex's revenue growth.

- Robust Financing Arrangement: Vertex plans to finance the acquisition through a combination of cash and debt, supported by $4.5 billion of fully committed bridge financing from Bank of America and Morgan Stanley, ensuring the transaction proceeds smoothly.

See More

Vertex Pharmaceuticals Hits All-Time High Amid Growth Potential

- Strong Stock Performance: Vertex Pharmaceuticals' stock has risen approximately 17% this year, significantly outperforming the S&P 500's 10% return, and has reached an all-time high, indicating strong market confidence in its future prospects.

- Sales Growth Challenges: Despite an 8% year-over-year sales increase totaling around $3 billion, the declining growth rate suggests the company faces short-term growth challenges, prompting investors to carefully assess future potential.

- Valuation Risks: Vertex is currently trading at a price-to-earnings ratio of about 31, well above the S&P 500's 25, and with a PEG ratio of 2.0, indicating that future growth may already be overvalued, posing downside risks.

- Cautious Investment Advice: While Vertex's long-term growth potential is viewed positively, analysts recommend that investors consider other growth stocks with better value due to the current high valuation.

See More

Vertex Pharmaceuticals Signs LOI for Cystic Fibrosis Therapy Access

- LOI for New Therapy: Vertex Pharmaceuticals has signed a Letter of Intent with the pan-Canadian Pharmaceutical Alliance to provide the new triple combination therapy PrALYFTREK for cystic fibrosis patients aged six and older, marking a significant advancement in treatment options for patients.

- Eligible Patients: Approximately 3,800 individuals across Canada are now eligible for ALYFTREK, with up to 60 potentially gaining access to a therapy that addresses the underlying cause of their disease for the first time, highlighting the therapy's potential impact.

- Regulatory Backing: The LOI follows positive reimbursement recommendations from Canada's Drug Agency and INESSS in December 2025 and April 2026, respectively, reflecting regulatory support for innovative medicines and facilitating market access for the therapy.

- Future Discussions: Vertex will engage with provinces and territories to support the public listing of ALYFTREK, a critical step that will enable the therapy to be funded through publicly funded drug programs across Canada, significantly enhancing patient accessibility.

See More

Vertex Acquires Crinetics for $10 Billion to Expand Rare Disease Portfolio

- Acquisition of Crinetics: Vertex Pharmaceuticals is acquiring Crinetics Pharmaceuticals for $10 billion, aiming to expand its business into endocrine diseases, with the potential to add up to $5 billion in annual revenue over the long term, although the market reacted negatively in the short term, pushing the stock down about 2%.

- Strategic Fit: Vertex CEO Reshma Kewalramani praised the acquisition as an excellent strategic fit, as Crinetics focuses on serious diseases in specialty markets with significant unmet needs, and it is expected to contribute revenue immediately through the ongoing launch of the Palsonify medicine.

- Revenue Growth Potential: The growing demand for therapeutics in endocrine diseases provides Vertex with a clear runway for double-digit revenue growth in the coming years, with Crinetics in the portfolio further solidifying its market position.

- Strong Market Performance: Since February 2022, Vertex's stock has outperformed the S&P 500 by 45%, demonstrating strong investor appeal, particularly in the current market environment.

See More

Fiserv Discusses Sale of Payments Business with Major Banks

- Stock Surge: Fiserv shares rallied over 5% after The Wall Street Journal reported discussions with major banks like JPMorgan and Bank of America regarding the sale of its payments infrastructure business, potentially leading to strategic restructuring and enhanced market competitiveness.

- Acquisition Deal: Vertex Pharmaceuticals announced a $10 billion acquisition of Crinetics Pharmaceuticals to expand its product line in rare hormonal disease treatments, although Vertex shares dipped nearly 1%, this deal is expected to strengthen its market position.

- Stock Upgrade: First Solar's stock rose nearly 3% after Deutsche Bank upgraded its rating from neutral to buy, with analysts citing potential trade policy shifts as a reason for investors to buy the dip, boosting market confidence.

- EV Stock Decline: Rivian shares tumbled 9% despite revenue and delivery guidance exceeding market expectations, as the company announced a plan to sell 75 million new shares for a significant capital raise, negatively impacting investor sentiment.

See More

Sellas Life Sciences Stock Gains Retail Trader Favor Amid Bullish Sentiment

- Retail Trader Enthusiasm: In a poll of 3,400 users, Sellas Life Sciences (SLS) garnered 50% of the votes, significantly outpacing Ondas Holdings at 24% and ImmunityBio at 18%, indicating strong investor confidence in its future potential.

- Clinical Trial Progress: Sellas' Phase 3 Regal trial in acute myeloid leukemia (AML) has reached 78 of the 80 events needed for final analysis, making the next two events critical catalysts that could drive stock price volatility.

- Acquisition Speculation: CEO Angelos Stergiou's optimistic remarks on social media and gratitude towards strategic partners have intensified market speculation regarding potential buyouts, likely attracting more investor interest.

- Significant Market Value Increase: Sellas' market value surged from $73 million at the start of 2024 to over $1.5 billion by mid-2026, reflecting heightened investor attention around the Regal readout, while the company ended Q1 with $107.1 million in cash, showcasing a robust financial position.

See More

Vertex Acquires Crinetics for $85 Per Share in $10 Billion Deal

- Acquisition Overview: Vertex Pharmaceuticals is acquiring Crinetics for $85 per share in cash, totaling approximately $10 billion, or about $8.8 billion net of cash, indicating Vertex's strong strategic intent.

- Significant Stock Reaction: Crinetics' shares surged over 99% in after-hours trading to $83.64, reflecting a positive market response to the acquisition, which may enhance Crinetics' market position.

- Product Line Expansion: The acquisition will provide Vertex with key assets like PALSONIFY (paltusotine) and Atumelnant, which are expected to generate over $5 billion in annual revenue, significantly boosting Vertex's revenue growth.

- Robust Financing Arrangement: Vertex plans to finance the acquisition through a combination of cash and debt, supported by $4.5 billion of fully committed bridge financing from Bank of America and Morgan Stanley, ensuring the transaction proceeds smoothly.

See More