Turkcell Forms Strategic Alliance with Google Cloud

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Nov 12 2025

0mins

Should l Buy GOOG?

- Partnership Announcement: Turkcell has formed a strategic partnership with Google Cloud to enhance digital infrastructure in Turkiye.

- New Cloud Region: Google Cloud is set to launch a new cloud region in Turkiye, which will support Turkcell's data center and cloud business.

- Investment Commitment: The partnership involves a multi-year investment aimed at strengthening Turkcell's capabilities in the cloud sector.

- Impact on Local Market: This collaboration is expected to significantly improve the digital landscape and cloud services available in Turkiye.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GOOG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GOOG

Wall Street analysts forecast GOOG stock price to fall

15 Analyst Rating

14 Buy

1 Hold

0 Sell

Strong Buy

Current: 395.300

Low

255.00

Averages

336.08

High

400.00

Current: 395.300

Low

255.00

Averages

336.08

High

400.00

About GOOG

Alphabet Inc. is a holding company. The Company's segments include Google Services, Google Cloud, and Other Bets. The Google Services segment includes products and services such as ads, Android, Chrome, devices, Google Maps, Google Play, Search, and YouTube. The Google Cloud segment includes infrastructure and platform services, collaboration tools, and other services for enterprise customers. Its Other Bets segment is engaged in the sale of healthcare-related services and Internet services. Its Google Cloud provides enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform provides access to solutions such as artificial intelligence (AI) offerings, including its AI infrastructure, Vertex AI platform, and Gemini for Google Cloud; cybersecurity, and data and analytics. Google Workspace includes cloud-based communication and collaboration tools for enterprises, such as Calendar, Gmail, Docs, Drive, and Meet.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Cloud Computing Fuels AI Investment Opportunities

- Amazon's Cloud Advantage: While Amazon's e-commerce business accounted for 79% of total sales, its cloud segment, AWS, delivered 59% of operating profits, highlighting its strong profitability, with plans to expand market share through $200 billion in capital expenditures over the next few years.

- Google Cloud's Rapid Growth: Google Cloud achieved an impressive 63% year-over-year growth in Q1, driven by sales of TPU chips produced in partnership with Broadcom, indicating its increasing competitiveness in the cloud computing sector.

- Microsoft's Steady Performance: Microsoft's Azure cloud platform reported 40% revenue growth last quarter, although its growth rate did not accelerate, it still demonstrates strong performance in the cloud market, and its relatively low price-to-earnings ratio makes it an attractive investment option.

- Long-Term Investment Potential: The ongoing investments and growth potential of these three companies in the cloud computing space position them for significant free cash flow growth in the coming years, especially as applications in the AI sector continue to expand.

See More

Google Explores Investments in AI Infrastructure and Manufacturing in India

- Investment Plans: Google is exploring investments in AI infrastructure and the manufacturing of servers and drones in India, indicating its strong focus on the Indian market and optimism about future growth potential.

- Major Commitment: In October 2025, Google announced a $15 billion investment over five years to build a data center and AI hub in Visakhapatnam, marking its largest commitment in India to date.

- Project Launch: Google has officially broken ground on its India AI Hub project in collaboration with AdaniConneX and Nxtra by Airtel, which will include a 1 GW hyperscale AI data center, further advancing local technological development.

- Land Allocation: The Government of Andhra Pradesh has allocated approximately 600 acres of land in the Turluvada, Rambilli, and Adavivaram areas for the project, ensuring smooth progress and meeting future infrastructure needs.

See More

Sirius XM Stock Soars on YouTube Partnership Announcement

- Stock Surge: Sirius XM's shares rallied 16.7% in April, primarily driven by a new partnership with YouTube, which is expected to significantly enhance advertising revenue potential, reflecting market confidence in its advertising technology.

- Analyst Upgrade: Rosenblatt analyst Barton Crockett raised Sirius XM's price target from $24 to $46 and upgraded the rating from 'neutral' to 'buy', citing the YouTube deal as a major endorsement of Sirius' advertising capabilities.

- Earnings Beat Expectations: Sirius XM reported first-quarter earnings on the last day of April that exceeded expectations, with revenue growing 1%, adjusted EBITDA rising 6%, and earnings per share increasing 22% to $0.72, indicating effective cost management.

- Future Growth Potential: While the subscription business faces challenges, the new advertising segment could drive growth, and analysts believe the value of its spectrum assets may lead to a re-rating of the company's valuation, showcasing market optimism about its future.

See More

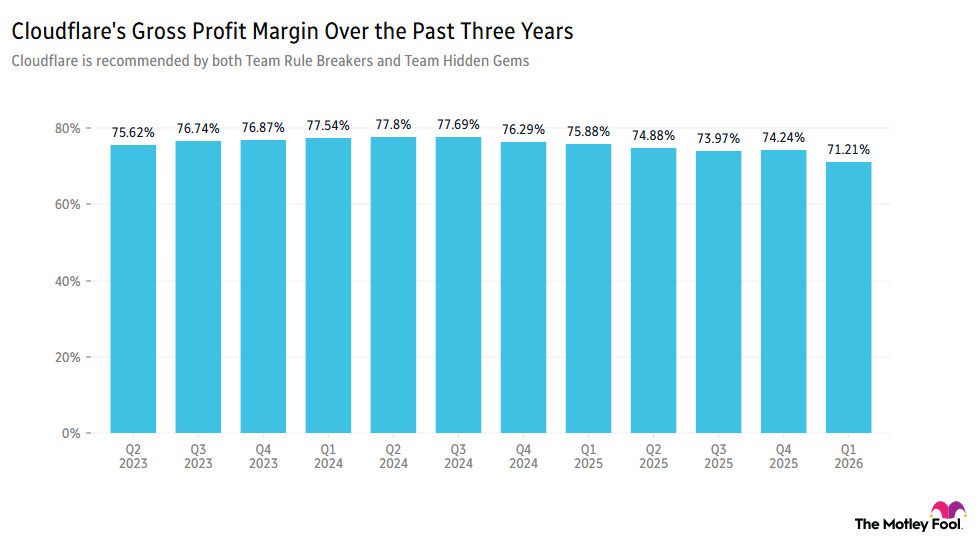

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More

Nvidia Faces Challenges and Opportunities in AI Chip Market

- Market Share Control: Nvidia commands an impressive 81% of the AI data center chip market, demonstrating its dominance despite competition from customers like Amazon and Google who are developing their own chips.

- Optimistic Sales Forecast: Nvidia forecasts total sales of $1 trillion for its Blackwell and Vera Rubin architectures across 2026 and 2027, indicating strong confidence in future growth despite increasing market competition.

- Customers Turned Competitors: Companies like Amazon and Google are designing their own chips to reduce costs, with Amazon's Trainium chip business experiencing a remarkable 40% sequential growth in Q1 2026, highlighting its strong growth potential in the AI chip market.

- Technological Innovation Against Competition: Nvidia is countering competition by launching its Vera server CPU as a standalone product, with expectations that its server CPU business could become a multibillion-dollar market, showcasing the company's proactive strategy in technological innovation.

See More

Hyperscalers Intensify AI Chip Competition Against Nvidia

- Market Share Shift: Nvidia controls approximately 81% of the AI data center chip market, but its dominance is gradually weakening as companies like Amazon and Google launch their own chips, potentially impacting future revenue growth.

- Amazon Chip Business Growth: Amazon's semiconductor business recorded a 40% sequential growth in Q1 2026, with an annual revenue run rate exceeding $20 billion, indicating strong demand and long-term growth potential in the AI chip market.

- Google TPU Business Outlook: Google's TPU business is seen as a key growth driver, with investment firms estimating its market value could reach $900 billion, suggesting that Google is enhancing its competitiveness in the AI chip sector.

- Nvidia's Response Strategy: Nvidia is countering competition by launching its Vera server CPU as a standalone product and reducing AI inference costs, and despite facing pressure, it is expected to maintain healthy growth in data center sales.

See More

Cloud Computing Fuels AI Investment Opportunities

- Amazon's Cloud Advantage: While Amazon's e-commerce business accounted for 79% of total sales, its cloud segment, AWS, delivered 59% of operating profits, highlighting its strong profitability, with plans to expand market share through $200 billion in capital expenditures over the next few years.

- Google Cloud's Rapid Growth: Google Cloud achieved an impressive 63% year-over-year growth in Q1, driven by sales of TPU chips produced in partnership with Broadcom, indicating its increasing competitiveness in the cloud computing sector.

- Microsoft's Steady Performance: Microsoft's Azure cloud platform reported 40% revenue growth last quarter, although its growth rate did not accelerate, it still demonstrates strong performance in the cloud market, and its relatively low price-to-earnings ratio makes it an attractive investment option.

- Long-Term Investment Potential: The ongoing investments and growth potential of these three companies in the cloud computing space position them for significant free cash flow growth in the coming years, especially as applications in the AI sector continue to expand.

See More

Google Explores Investments in AI Infrastructure and Manufacturing in India

- Investment Plans: Google is exploring investments in AI infrastructure and the manufacturing of servers and drones in India, indicating its strong focus on the Indian market and optimism about future growth potential.

- Major Commitment: In October 2025, Google announced a $15 billion investment over five years to build a data center and AI hub in Visakhapatnam, marking its largest commitment in India to date.

- Project Launch: Google has officially broken ground on its India AI Hub project in collaboration with AdaniConneX and Nxtra by Airtel, which will include a 1 GW hyperscale AI data center, further advancing local technological development.

- Land Allocation: The Government of Andhra Pradesh has allocated approximately 600 acres of land in the Turluvada, Rambilli, and Adavivaram areas for the project, ensuring smooth progress and meeting future infrastructure needs.

See More

Sirius XM Stock Soars on YouTube Partnership Announcement

- Stock Surge: Sirius XM's shares rallied 16.7% in April, primarily driven by a new partnership with YouTube, which is expected to significantly enhance advertising revenue potential, reflecting market confidence in its advertising technology.

- Analyst Upgrade: Rosenblatt analyst Barton Crockett raised Sirius XM's price target from $24 to $46 and upgraded the rating from 'neutral' to 'buy', citing the YouTube deal as a major endorsement of Sirius' advertising capabilities.

- Earnings Beat Expectations: Sirius XM reported first-quarter earnings on the last day of April that exceeded expectations, with revenue growing 1%, adjusted EBITDA rising 6%, and earnings per share increasing 22% to $0.72, indicating effective cost management.

- Future Growth Potential: While the subscription business faces challenges, the new advertising segment could drive growth, and analysts believe the value of its spectrum assets may lead to a re-rating of the company's valuation, showcasing market optimism about its future.

See More

Cloudflare's AI Reform Triggers Stock Plunge

- Significant Stock Drop: Cloudflare's stock plummeted over 18% ahead of the market open as investors perceived the company's late entry into AI as a major concern, despite management's assertion of it being the 'biggest tailwind we've ever seen,' compounded by a 4.67% year-over-year decline in gross profit margins that undermined market confidence.

- Layoff Implementation: The company announced a layoff of 1,100 employees, representing 20% of its current workforce, with management stating in an internal email the need to 'be intentional in how we architect our company for the agentic AI era,' which could impact operational efficiency and employee morale.

- Strong Revenue Growth: Despite the drop in gross margins, Cloudflare reported a 34% year-over-year revenue increase and raised its outlook for fiscal year 2026 revenue and earnings, indicating that investments in AI may yield returns in the future.

- Outstanding Market Performance: Since November 2022, Cloudflare's stock has outperformed the S&P 500 by 285%, suggesting that despite current challenges, investors remain optimistic about the company's long-term potential.

See More

Nvidia Faces Challenges and Opportunities in AI Chip Market

- Market Share Control: Nvidia commands an impressive 81% of the AI data center chip market, demonstrating its dominance despite competition from customers like Amazon and Google who are developing their own chips.

- Optimistic Sales Forecast: Nvidia forecasts total sales of $1 trillion for its Blackwell and Vera Rubin architectures across 2026 and 2027, indicating strong confidence in future growth despite increasing market competition.

- Customers Turned Competitors: Companies like Amazon and Google are designing their own chips to reduce costs, with Amazon's Trainium chip business experiencing a remarkable 40% sequential growth in Q1 2026, highlighting its strong growth potential in the AI chip market.

- Technological Innovation Against Competition: Nvidia is countering competition by launching its Vera server CPU as a standalone product, with expectations that its server CPU business could become a multibillion-dollar market, showcasing the company's proactive strategy in technological innovation.

See More

Hyperscalers Intensify AI Chip Competition Against Nvidia

- Market Share Shift: Nvidia controls approximately 81% of the AI data center chip market, but its dominance is gradually weakening as companies like Amazon and Google launch their own chips, potentially impacting future revenue growth.

- Amazon Chip Business Growth: Amazon's semiconductor business recorded a 40% sequential growth in Q1 2026, with an annual revenue run rate exceeding $20 billion, indicating strong demand and long-term growth potential in the AI chip market.

- Google TPU Business Outlook: Google's TPU business is seen as a key growth driver, with investment firms estimating its market value could reach $900 billion, suggesting that Google is enhancing its competitiveness in the AI chip sector.

- Nvidia's Response Strategy: Nvidia is countering competition by launching its Vera server CPU as a standalone product and reducing AI inference costs, and despite facing pressure, it is expected to maintain healthy growth in data center sales.

See More