Three Stocks Investors Should Consider Buying Now

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 hour ago

0mins

Should l Buy SMCI?

Source: Fool

- Market Pullback Opportunity: As of March 13, the S&P 500 was approximately 5% below its all-time high, with the Dow and Nasdaq down about 7% and 8% respectively, indicating that despite market volatility, historical trends suggest such pullbacks often present buying opportunities for investors.

- Super Micro Computer Potential: Super Micro Computer (SMCI) has strong ties with Nvidia, with projected earnings per share exceeding 10 times by fiscal 2027, and an estimated 88% sales growth this year, highlighting its robust demand in the AI server market.

- Pinterest's Advertising Opportunities: Pinterest (PINS) reached 619 million global monthly active users in Q4, and despite competitive pressures, its ad revenue is expected to grow by 21% to 40% in 2025, showcasing its strong pricing power in the digital advertising space.

- Adobe's Share Buybacks: Adobe (ADBE) generated $2.96 billion in cash flow in Q1 2023 and repurchased 8.1 million shares, reducing its outstanding shares by 32%, indicating that despite challenges, its stock remains an attractive value investment.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy SMCI?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on SMCI

Wall Street analysts forecast SMCI stock price to rise

12 Analyst Rating

5 Buy

5 Hold

2 Sell

Hold

Current: 31.510

Low

34.00

Averages

46.82

High

63.00

Current: 31.510

Low

34.00

Averages

46.82

High

63.00

About SMCI

Super Micro Computer, Inc. provides application-optimized Total IT solutions. It delivers rack-scale solutions optimized for various workloads, including artificial intelligence and high-performance computing, where acceleration is critical. It produces a portfolio of server and storage solutions for enterprise data centers, cloud service providers and edge computing (5G Telco, Retail and embedded). Total IT Solutions include complete servers, storage systems, modular blade servers, workstations, full-rack scale solutions, networking devices, server sub-systems, server management and security software. It provides global support and services to help its customers install, upgrade and maintain their computing infrastructure, including liquid-cooling operations. It offers platforms in rackmount, blade, multi-node and embedded form factors, which support single, dual and multiprocessor architectures. Its key product lines include SuperBlade and MicroBlade, SuperStorage, Twin and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

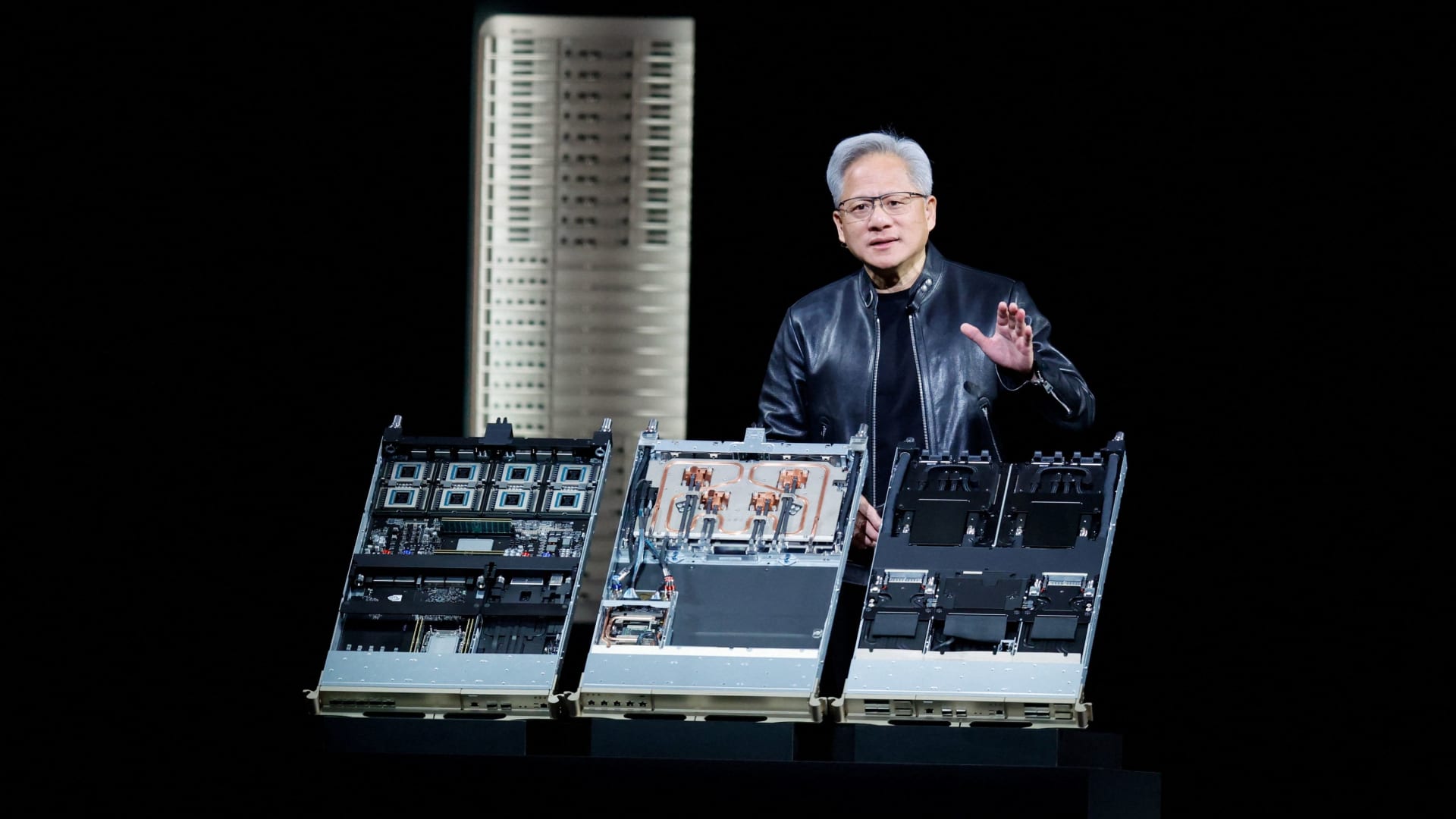

Supermicro Unveils NVIDIA Vera Rubin System Portfolio

- New System Launch: Supermicro has unveiled its NVL72, HGX Rubin NVL8, and Vera CPU systems powered by the NVIDIA Vera Rubin platform, designed to meet the demands of data centers transforming into AI factories, which is expected to significantly enhance clients' computing and storage capabilities.

- Liquid Cooling Technology: The new systems utilize Supermicro's advanced liquid cooling technology, capable of supporting up to 3.6 Exaflops of inference power and 75 TB of fast memory, thereby providing higher efficiency and performance in AI inference and high-performance computing.

- Modular Infrastructure: Supermicro's DCBBS solutions enable data center operators to quickly deploy validated rack solutions, reducing integration risks and shortening time-to-online, which is anticipated to drive widespread implementation of AI factories.

- Market Leadership: The Vera Rubin systems will serve as the first AI infrastructure fully supporting liquid cooling in the market, expected to further solidify Supermicro's leadership position in cloud computing and AI, addressing the growing market demand.

See More

Three Stocks Investors Should Consider Buying Now

- Market Pullback Opportunity: As of March 13, the S&P 500 was approximately 5% below its all-time high, with the Dow and Nasdaq down about 7% and 8% respectively, indicating that despite market volatility, historical trends suggest such pullbacks often present buying opportunities for investors.

- Super Micro Computer Potential: Super Micro Computer (SMCI) has strong ties with Nvidia, with projected earnings per share exceeding 10 times by fiscal 2027, and an estimated 88% sales growth this year, highlighting its robust demand in the AI server market.

- Pinterest's Advertising Opportunities: Pinterest (PINS) reached 619 million global monthly active users in Q4, and despite competitive pressures, its ad revenue is expected to grow by 21% to 40% in 2025, showcasing its strong pricing power in the digital advertising space.

- Adobe's Share Buybacks: Adobe (ADBE) generated $2.96 billion in cash flow in Q1 2023 and repurchased 8.1 million shares, reducing its outstanding shares by 32%, indicating that despite challenges, its stock remains an attractive value investment.

See More

Nvidia Remains a Buy Amid Market Turmoil

- Market Volatility Impact: The stock market experienced significant declines on Wednesday, with the Dow Jones Industrial Average dropping over 750 points, or 1.6%, due to soaring oil prices and high inflation data, reflecting investor concerns about the economic outlook.

- Nvidia Investment Opportunity: Despite the overall market weakness, Jim Cramer continues to recommend Nvidia, believing that its leadership in AI and the upcoming release of a new inference chip will drive its stock price higher, with expected orders reaching $1 trillion by 2027.

- Optimistic Earnings Forecast: Analysts at Cantor Fitzgerald project Nvidia's earnings per share to reach $15 by 2027, making its valuation relatively low at about 12 times the 2027 EPS, compared to the S&P 500's price-to-earnings ratio of 18.

- Positive Long-Term Outlook: Although Nvidia faces short-term pressures from rising oil prices and uncertainties surrounding Federal Reserve policies, Cramer emphasizes the company's strong long-term growth potential, suggesting that its combination of low valuation and rapid growth makes it an attractive investment choice.

See More

Micron Reports Strong Earnings, Revenue Nearly Triples

- Significant Revenue Growth: Micron's latest quarter revenue reached $23.86 billion, nearly tripling from $8.05 billion a year earlier and exceeding analyst expectations of $20.07 billion, showcasing the company's robust performance amid surging AI-driven memory demand.

- Improved Profitability: Adjusted earnings per share stood at $12.20, well above the market expectation of $9.31, while gross margin soared from 36.8% a year ago to 74.4%, reflecting the high-margin advantage of high-bandwidth memory products.

- Optimistic Future Outlook: Micron anticipates revenue of approximately $33.5 billion for the upcoming quarter, representing over 200% growth from $9.3 billion a year ago, indicating strong demand and execution in the memory market.

- Increased Capital Expenditure: Micron plans to significantly ramp up capital expenditures in fiscal 2027, exceeding $10 billion for the construction of two large manufacturing campuses in Idaho and New York, aimed at enhancing memory production capacity in the U.S. and solidifying its market position.

See More

Nvidia Restarts H200 Chip Production for China Market

- China Market Opportunity: Nvidia's CEO Jensen Huang announced the restart of H200 AI chip production for the Chinese market after receiving government approval, marking a significant re-entry into a market with substantial growth potential, which is expected to support future sales growth.

- Market Potential Assessment: Analysts estimate that the AI chip market in China represents a $50 billion opportunity, and capturing even a fraction of this market could significantly enhance both management and Wall Street's earnings forecasts, particularly for 2026 and beyond.

- Revenue Forecast Increase: Nvidia's management indicated at the GTC conference that the revenue floor for the 2025 to 2027 period is set at $1 trillion, with analysts suggesting that this figure excludes sales from new CPUs and the Groq chip, potentially raising actual revenue estimates to as high as $1.5 trillion.

- Stock Price Attractiveness: Despite the stock hovering around $180, the decline in forward P/E from 34 to 21 as future earnings estimates rise indicates increased attractiveness compared to the market, providing investors with an opportunity to accumulate shares at current price levels.

See More

Supermicro Unveils New AI Acceleration Solutions

- New Product Launch: Supermicro introduces new systems supporting NVIDIA RTX PRO 4500 Blackwell GPUs, aimed at addressing high-density computing needs in enterprise data centers and edge computing, which is expected to significantly enhance performance for AI and graphics computing applications.

- Enhanced Compatibility: The new systems are NVIDIA-certified, ensuring compatibility with NVIDIA RTX PRO Blackwell GPUs and related networks and software, thereby providing enterprises with comprehensive solutions to accelerate workload processing.

- Flexible Architecture Design: Supermicro's Building Block Solutions® architecture supports various GPU configurations, enabling efficient computing without altering existing data center infrastructure, helping businesses reduce time-to-online and improve return on investment.

- Edge Computing Optimization: The newly launched 1U and 2U edge AI solutions are optimized for power and thermal management, supporting up to four NVIDIA RTX PRO Blackwell GPUs, capable of processing AI inference requests under strict environmental constraints, reducing latency and data transfer costs.

See More

Supermicro Unveils NVIDIA Vera Rubin System Portfolio

- New System Launch: Supermicro has unveiled its NVL72, HGX Rubin NVL8, and Vera CPU systems powered by the NVIDIA Vera Rubin platform, designed to meet the demands of data centers transforming into AI factories, which is expected to significantly enhance clients' computing and storage capabilities.

- Liquid Cooling Technology: The new systems utilize Supermicro's advanced liquid cooling technology, capable of supporting up to 3.6 Exaflops of inference power and 75 TB of fast memory, thereby providing higher efficiency and performance in AI inference and high-performance computing.

- Modular Infrastructure: Supermicro's DCBBS solutions enable data center operators to quickly deploy validated rack solutions, reducing integration risks and shortening time-to-online, which is anticipated to drive widespread implementation of AI factories.

- Market Leadership: The Vera Rubin systems will serve as the first AI infrastructure fully supporting liquid cooling in the market, expected to further solidify Supermicro's leadership position in cloud computing and AI, addressing the growing market demand.

See More

Three Stocks Investors Should Consider Buying Now

- Market Pullback Opportunity: As of March 13, the S&P 500 was approximately 5% below its all-time high, with the Dow and Nasdaq down about 7% and 8% respectively, indicating that despite market volatility, historical trends suggest such pullbacks often present buying opportunities for investors.

- Super Micro Computer Potential: Super Micro Computer (SMCI) has strong ties with Nvidia, with projected earnings per share exceeding 10 times by fiscal 2027, and an estimated 88% sales growth this year, highlighting its robust demand in the AI server market.

- Pinterest's Advertising Opportunities: Pinterest (PINS) reached 619 million global monthly active users in Q4, and despite competitive pressures, its ad revenue is expected to grow by 21% to 40% in 2025, showcasing its strong pricing power in the digital advertising space.

- Adobe's Share Buybacks: Adobe (ADBE) generated $2.96 billion in cash flow in Q1 2023 and repurchased 8.1 million shares, reducing its outstanding shares by 32%, indicating that despite challenges, its stock remains an attractive value investment.

See More

Nvidia Remains a Buy Amid Market Turmoil

- Market Volatility Impact: The stock market experienced significant declines on Wednesday, with the Dow Jones Industrial Average dropping over 750 points, or 1.6%, due to soaring oil prices and high inflation data, reflecting investor concerns about the economic outlook.

- Nvidia Investment Opportunity: Despite the overall market weakness, Jim Cramer continues to recommend Nvidia, believing that its leadership in AI and the upcoming release of a new inference chip will drive its stock price higher, with expected orders reaching $1 trillion by 2027.

- Optimistic Earnings Forecast: Analysts at Cantor Fitzgerald project Nvidia's earnings per share to reach $15 by 2027, making its valuation relatively low at about 12 times the 2027 EPS, compared to the S&P 500's price-to-earnings ratio of 18.

- Positive Long-Term Outlook: Although Nvidia faces short-term pressures from rising oil prices and uncertainties surrounding Federal Reserve policies, Cramer emphasizes the company's strong long-term growth potential, suggesting that its combination of low valuation and rapid growth makes it an attractive investment choice.

See More

Micron Reports Strong Earnings, Revenue Nearly Triples

- Significant Revenue Growth: Micron's latest quarter revenue reached $23.86 billion, nearly tripling from $8.05 billion a year earlier and exceeding analyst expectations of $20.07 billion, showcasing the company's robust performance amid surging AI-driven memory demand.

- Improved Profitability: Adjusted earnings per share stood at $12.20, well above the market expectation of $9.31, while gross margin soared from 36.8% a year ago to 74.4%, reflecting the high-margin advantage of high-bandwidth memory products.

- Optimistic Future Outlook: Micron anticipates revenue of approximately $33.5 billion for the upcoming quarter, representing over 200% growth from $9.3 billion a year ago, indicating strong demand and execution in the memory market.

- Increased Capital Expenditure: Micron plans to significantly ramp up capital expenditures in fiscal 2027, exceeding $10 billion for the construction of two large manufacturing campuses in Idaho and New York, aimed at enhancing memory production capacity in the U.S. and solidifying its market position.

See More

Nvidia Restarts H200 Chip Production for China Market

- China Market Opportunity: Nvidia's CEO Jensen Huang announced the restart of H200 AI chip production for the Chinese market after receiving government approval, marking a significant re-entry into a market with substantial growth potential, which is expected to support future sales growth.

- Market Potential Assessment: Analysts estimate that the AI chip market in China represents a $50 billion opportunity, and capturing even a fraction of this market could significantly enhance both management and Wall Street's earnings forecasts, particularly for 2026 and beyond.

- Revenue Forecast Increase: Nvidia's management indicated at the GTC conference that the revenue floor for the 2025 to 2027 period is set at $1 trillion, with analysts suggesting that this figure excludes sales from new CPUs and the Groq chip, potentially raising actual revenue estimates to as high as $1.5 trillion.

- Stock Price Attractiveness: Despite the stock hovering around $180, the decline in forward P/E from 34 to 21 as future earnings estimates rise indicates increased attractiveness compared to the market, providing investors with an opportunity to accumulate shares at current price levels.

See More

Supermicro Unveils New AI Acceleration Solutions

- New Product Launch: Supermicro introduces new systems supporting NVIDIA RTX PRO 4500 Blackwell GPUs, aimed at addressing high-density computing needs in enterprise data centers and edge computing, which is expected to significantly enhance performance for AI and graphics computing applications.

- Enhanced Compatibility: The new systems are NVIDIA-certified, ensuring compatibility with NVIDIA RTX PRO Blackwell GPUs and related networks and software, thereby providing enterprises with comprehensive solutions to accelerate workload processing.

- Flexible Architecture Design: Supermicro's Building Block Solutions® architecture supports various GPU configurations, enabling efficient computing without altering existing data center infrastructure, helping businesses reduce time-to-online and improve return on investment.

- Edge Computing Optimization: The newly launched 1U and 2U edge AI solutions are optimized for power and thermal management, supporting up to four NVIDIA RTX PRO Blackwell GPUs, capable of processing AI inference requests under strict environmental constraints, reducing latency and data transfer costs.

See More