Tech Stocks Surge, Led by Marvell and HPE

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 2 days ago

0mins

Source: CNBC

- Marvell Stock Surge: Shares of Marvell soared 25% after Nvidia CEO Jensen Huang suggested it could become the next trillion-dollar company, which not only boosted investor confidence but may also attract more institutional interest in its growth potential.

- Hewlett Packard Enterprise Beats Estimates: HPE's stock also jumped 25% after it posted quarterly earnings and revenue guidance that exceeded analysts' expectations, along with an increase in its full-year earnings guidance, showcasing the company's strong performance and competitiveness in the IT sector.

- Victoria's Secret Raises Full-Year Guidance: The lingerie retailer raised its full-year sales forecast to between $7.03 billion and $7.13 billion after beating fiscal first-quarter earnings expectations, reflecting its success in reducing tariff costs and enhancing profitability.

- Credo Technology Shares Decline: Despite reporting a fourth-quarter earnings beat with adjusted earnings of $1.16 per share and revenue of $437 million, Credo's shares fell 3%, indicating market concerns over its future growth, even as it provided current-quarter revenue guidance that surpassed consensus forecasts.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy HPE?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on HPE

Wall Street analysts forecast HPE stock price to fall

16 Analyst Rating

8 Buy

8 Hold

0 Sell

Moderate Buy

Current: 55.150

Low

21.00

Averages

27.13

High

31.00

Current: 55.150

Low

21.00

Averages

27.13

High

31.00

About HPE

Hewlett Packard Enterprise Company is a global technology company focused on developing intelligent solutions that allow customers to capture, analyze and act upon data seamlessly from edge to cloud. Its customers range from small-and-medium-sized businesses to large global enterprises and governmental entities. Its segments include Server, Hybrid Cloud, Networking, Financial Services, and Corporate Investments and Other. Its Server segment offerings consist of general-purpose servers for multi-workload computing, workload-optimized servers, and integrated systems. Its Hybrid Cloud segment offers a range of cloud-native and hybrid solutions across storage, private cloud and the infrastructure software-as-a-service space. The Networking segment develops and sells high-performance networking and security products and services. Its Financial Services segment provides flexible investment solutions, such as leasing, financing, IT consumption, utility programs, and asset management services.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Hewlett Packard Enterprise Shares Surge 25% on Strong Q2 Results and Outlook

- Strong Earnings Beat: Hewlett Packard Enterprise (HPE) reported fiscal Q2 results that exceeded expectations, leading to a premarket share surge of approximately 25%, indicating analysts' optimism about future growth prospects.

- Price Target Increase: Morgan Stanley raised HPE's price target from $33 to $71, highlighting that inelastic server demand and market share gains are expected to drive future profitability, with FY27 EPS projected at $4.16.

- Robust Market Demand: Analysts noted that despite rising memory costs, HPE is able to protect margins due to customers' willingness to absorb higher DRAM/NAND prices, with double-digit year-over-year growth in server orders reflecting the strategic importance of servers for enterprises.

- Positive Future Outlook: Bank of America maintained a Buy rating and increased the price target to $80, citing significant topline growth potential for FY27, with management indicating no signs of order pull-forwards, cancellations, or double ordering, suggesting future growth will be driven by networking and AI advancements.

See More

HPE Reports 40% Revenue Growth in Q2

- Record Revenue: HPE's fiscal second-quarter revenue surged 40% year-over-year to $10.7 billion, reflecting strong performance in AI system orders and overall market demand, which is expected to drive future growth further.

- Surge in AI Orders: New AI systems orders reached $1.8 billion, with the AI systems backlog growing to $5.9 billion, indicating sustained demand from enterprise customers for AI solutions, potentially enhancing the company's market share and competitiveness.

- Networking Revenue Surge: Following the acquisition of Juniper Networks, HPE's networking revenue skyrocketed 148% year-over-year to $2.7 billion, although growth was only 10% when excluding the acquisition impact, still showcasing strong momentum in the networking sector.

- Improved Profitability: HPE's cloud and AI segment achieved an operating margin of 12.4% in the quarter, nearly doubling from last year's 6.6%, although still below the networking segment's 21.6%, indicating potential for profitability improvement in a high-demand environment.

See More

Hewlett Packard Enterprise Shares Surge 130% Amid Record Earnings

- Significant Revenue Growth: Hewlett Packard Enterprise reported a 40% year-over-year revenue increase to $10.7 billion in its fiscal Q2 2026, exceeding market expectations and demonstrating strong performance in the enterprise hardware sector, thereby solidifying its market position in AI servers.

- Surge in AI System Orders: The company secured $1.8 billion in new AI systems orders during the same quarter, raising its AI systems backlog to $5.9 billion, indicating a rapid increase in demand from enterprise customers for AI solutions, which enhances future revenue potential.

- Acquisition Impact Analysis: While networking revenue surged 148% year-over-year to $2.7 billion, excluding the Juniper Networks acquisition, networking growth was only about 10%, highlighting the need for the company to focus on sustainable growth in its core business post-acquisition.

- Supply Chain Challenges: Management indicated that supply constraints, particularly in memory, will affect the speed at which orders convert to revenue, with elevated costs expected to persist into 2027, which may pressure profit margins and warrant caution from investors.

See More

CrowdStrike Reports Strong Earnings but Stock Drops Post-Results

- Earnings Beat: CrowdStrike's fiscal Q1 2027 revenue surged 26% year-over-year to $1.39 billion, exceeding the $1.36 billion consensus estimate, indicating strong performance in the cybersecurity sector, although the stock fell over 11% due to profit-taking by short-term investors.

- Adjusted EPS Growth: The adjusted earnings per share (EPS) for the quarter reached $1.10, a 51% increase over the $1.07 estimate, showcasing significant profitability improvements, despite the market's tepid response, highlighting investor sensitivity to short-term fluctuations.

- Stock Split Announcement: CrowdStrike announced a 4-for-1 stock split, with trading on a split-adjusted basis expected to begin on July 2, aimed at enhancing stock accessibility for investors, even though stock splits do not inherently create additional value for shareholders.

- Optimistic Future Guidance: The company raised its total revenue outlook for fiscal 2027 to between $5.91 billion and $5.96 billion, surpassing the $5.89 billion expectation, reflecting management's confidence in future growth, while also adjusting EPS forecasts upward, indicating ongoing business growth potential.

See More

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

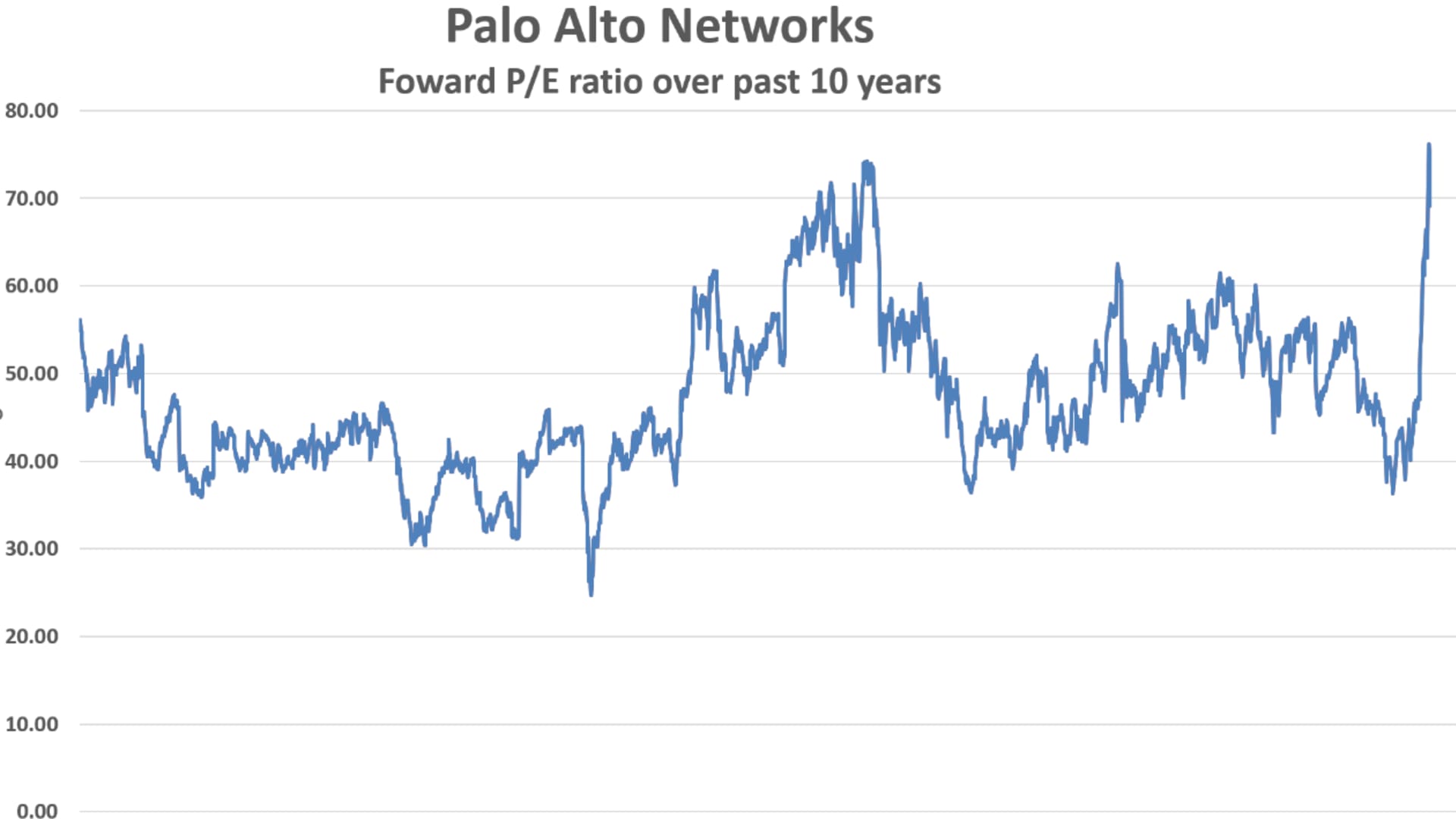

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More

Hewlett Packard Enterprise Shares Surge 25% on Strong Q2 Results and Outlook

- Strong Earnings Beat: Hewlett Packard Enterprise (HPE) reported fiscal Q2 results that exceeded expectations, leading to a premarket share surge of approximately 25%, indicating analysts' optimism about future growth prospects.

- Price Target Increase: Morgan Stanley raised HPE's price target from $33 to $71, highlighting that inelastic server demand and market share gains are expected to drive future profitability, with FY27 EPS projected at $4.16.

- Robust Market Demand: Analysts noted that despite rising memory costs, HPE is able to protect margins due to customers' willingness to absorb higher DRAM/NAND prices, with double-digit year-over-year growth in server orders reflecting the strategic importance of servers for enterprises.

- Positive Future Outlook: Bank of America maintained a Buy rating and increased the price target to $80, citing significant topline growth potential for FY27, with management indicating no signs of order pull-forwards, cancellations, or double ordering, suggesting future growth will be driven by networking and AI advancements.

See More

HPE Reports 40% Revenue Growth in Q2

- Record Revenue: HPE's fiscal second-quarter revenue surged 40% year-over-year to $10.7 billion, reflecting strong performance in AI system orders and overall market demand, which is expected to drive future growth further.

- Surge in AI Orders: New AI systems orders reached $1.8 billion, with the AI systems backlog growing to $5.9 billion, indicating sustained demand from enterprise customers for AI solutions, potentially enhancing the company's market share and competitiveness.

- Networking Revenue Surge: Following the acquisition of Juniper Networks, HPE's networking revenue skyrocketed 148% year-over-year to $2.7 billion, although growth was only 10% when excluding the acquisition impact, still showcasing strong momentum in the networking sector.

- Improved Profitability: HPE's cloud and AI segment achieved an operating margin of 12.4% in the quarter, nearly doubling from last year's 6.6%, although still below the networking segment's 21.6%, indicating potential for profitability improvement in a high-demand environment.

See More

Hewlett Packard Enterprise Shares Surge 130% Amid Record Earnings

- Significant Revenue Growth: Hewlett Packard Enterprise reported a 40% year-over-year revenue increase to $10.7 billion in its fiscal Q2 2026, exceeding market expectations and demonstrating strong performance in the enterprise hardware sector, thereby solidifying its market position in AI servers.

- Surge in AI System Orders: The company secured $1.8 billion in new AI systems orders during the same quarter, raising its AI systems backlog to $5.9 billion, indicating a rapid increase in demand from enterprise customers for AI solutions, which enhances future revenue potential.

- Acquisition Impact Analysis: While networking revenue surged 148% year-over-year to $2.7 billion, excluding the Juniper Networks acquisition, networking growth was only about 10%, highlighting the need for the company to focus on sustainable growth in its core business post-acquisition.

- Supply Chain Challenges: Management indicated that supply constraints, particularly in memory, will affect the speed at which orders convert to revenue, with elevated costs expected to persist into 2027, which may pressure profit margins and warrant caution from investors.

See More

CrowdStrike Reports Strong Earnings but Stock Drops Post-Results

- Earnings Beat: CrowdStrike's fiscal Q1 2027 revenue surged 26% year-over-year to $1.39 billion, exceeding the $1.36 billion consensus estimate, indicating strong performance in the cybersecurity sector, although the stock fell over 11% due to profit-taking by short-term investors.

- Adjusted EPS Growth: The adjusted earnings per share (EPS) for the quarter reached $1.10, a 51% increase over the $1.07 estimate, showcasing significant profitability improvements, despite the market's tepid response, highlighting investor sensitivity to short-term fluctuations.

- Stock Split Announcement: CrowdStrike announced a 4-for-1 stock split, with trading on a split-adjusted basis expected to begin on July 2, aimed at enhancing stock accessibility for investors, even though stock splits do not inherently create additional value for shareholders.

- Optimistic Future Guidance: The company raised its total revenue outlook for fiscal 2027 to between $5.91 billion and $5.96 billion, surpassing the $5.89 billion expectation, reflecting management's confidence in future growth, while also adjusting EPS forecasts upward, indicating ongoing business growth potential.

See More

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More