Tech Stocks Decline, State Street Technology ETF Under Pressure

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 20 2026

0mins

Should l Buy NVDA?

Source: Yahoo Finance

- Market Weakness: Tech stocks were lower on Tuesday afternoon, reflecting a cautious investor sentiment towards market prospects, which may lead to short-term capital outflows from the tech sector.

- ETF Pressure: The State Street Technology Select Sector SPDR ETF showed poor performance, indicating a weakening investor confidence in the tech industry, which could impact the stock prices of related companies.

- Investor Sentiment Shift: As market volatility increases, investors may reassess their portfolios in tech stocks, leading to reduced liquidity and potentially affecting market stability.

- Uncertain Outlook: The decline in tech stocks may signal more uncertainty in the market over the coming weeks, prompting investors to closely monitor economic data and policy changes affecting the tech sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy NVDA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on NVDA

Wall Street analysts forecast NVDA stock price to rise

41 Analyst Rating

39 Buy

1 Hold

1 Sell

Strong Buy

Current: 175.750

Low

200.00

Averages

264.97

High

352.00

Current: 175.750

Low

200.00

Averages

264.97

High

352.00

About NVDA

NVIDIA Corporation is an artificial intelligence (AI) infrastructure company. The Company is engaged in accelerated computing to help solve the challenging computational problems. Its segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing and networking platforms and AI solutions and software, and automotive platforms and autonomous and electric vehicle solutions, including software. The Graphics segment includes GeForce GPUs for gaming and personal computers (PCs), and Quadro/NVIDIA RTX GPUs for enterprise workstation graphics. Its technology stack includes the foundational NVIDIA CUDA development platform that runs on all NVIDIA GPUs, as well as hundreds of domain-specific software libraries, frameworks, algorithms, software development kits (SDKs), and application programming interfaces (APIs). Its platforms address four markets, which include Data Center, Gaming, Professional Visualization, and Automotive.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nvidia's Earnings Report Shows Strong Growth

- Significant Revenue Growth: Nvidia's revenue in Q4 of fiscal 2026 surged 73% year-over-year to $68.1 billion, primarily driven by its data center segment, which generated $62.3 billion in revenue, up 75% year-over-year.

- Profitability Improvement: The company reported non-GAAP earnings per share of $1.62, an 82% increase year-over-year, while maintaining an impressive adjusted gross margin of 75.2%, showcasing its strong pricing power and production scale within its hardware ecosystem.

- Optimistic Future Outlook: Management anticipates first-quarter revenue for fiscal 2027 to be approximately $78 billion, indicating that the company's growth in the AI sector is still in its early stages, with the data center business expanding nearly 13 times since fiscal 2023.

- Valuation Outlook Analysis: Despite a current price-to-earnings ratio of about 36, the forward P/E ratio is expected to drop to 21 over the next four quarters, and if the company meets Wall Street's earnings expectations, the stock price could appreciate by 12% over the next year, reaching around $197.

See More

Nvidia Reopens Key AI Market in China Amid Risks

- Market Reopening: Nvidia has reopened its operations in China, one of the world's most crucial AI markets, presenting potential for revenue growth despite existing policy risks that complicate the narrative.

- Policy Risks: While the opportunities in the Chinese market are significant, uncertainties surrounding government regulations and market access could impact Nvidia's long-term strategic positioning in the region.

- Investment Opportunities: Analysts suggest that despite the high costs associated with re-entering the market, Nvidia could leverage technological innovation and adaptability to capture growth opportunities in China, enhancing its global competitiveness.

- Future Outlook: As demand for AI technology continues to rise in China, Nvidia's market strategy will need to be agile to navigate the complex policy landscape and maximize returns on its investments in the region.

See More

Chinese Semiconductor Industry Hits Record Revenue

- Significant Revenue Growth: Semiconductor Manufacturing International Co. (SMIC) reported a revenue of $9.3 billion for 2025, a 16% increase year-on-year, with projections suggesting revenues could exceed $11 billion in 2026, highlighting the robust growth potential of China's semiconductor sector driven by AI demand.

- Strong Performance from Hua Hong: Hua Hong Semiconductor achieved a record revenue of $659.9 million in Q4, with future sales expected between $650 million and $660 million, reflecting sustained domestic demand for semiconductors and the company's solid market positioning.

- Surge in Memory Chip Demand: ChangXin Memory Technologies (CXMT) saw a 130% year-on-year revenue increase, surpassing 55 billion yuan ($8 billion), indicating the rise of Chinese firms in the high-bandwidth memory market amid global shortages.

- Ongoing Technical Challenges: Despite record revenues, Chinese semiconductor companies still lag behind their U.S., South Korean, and Taiwanese counterparts in technological capabilities, particularly in producing advanced chips at scale, facing ongoing pressure from U.S. export controls.

See More

Investment Risk Alert: Etsy, Nike, Tesla

- Etsy Sales Decline: Etsy's gross merchandise sales fell by 5.3% year-over-year in 2025, and while there was a slight recovery in Q4 excluding Reverb sales, the overall decrease in active buyers and sellers alongside a drop in net income indicates a weakening market position.

- Nike's Weak Performance: In its Q3 fiscal 2026 report, Nike showed flat year-over-year revenue despite a 5% increase in wholesale revenue, as direct sales declined by 4%, highlighting ongoing market share losses, particularly with a 7% drop in sales in China.

- Tesla's Growth Obstacles: Despite exceeding a $1 trillion market cap, Tesla's revenue dipped by 3% year-over-year in 2025, with a 10% decline in automobile sales and a 46% drop in GAAP net income, indicating significant challenges in sustaining growth in the electric vehicle market.

- Investor Confidence Shaken: With the declining performance of Etsy, Nike, and Tesla, investor confidence in these once high-flying stocks is waning, prompting analysts to suggest considering divestment ahead of upcoming earnings reports to avoid potential larger losses.

See More

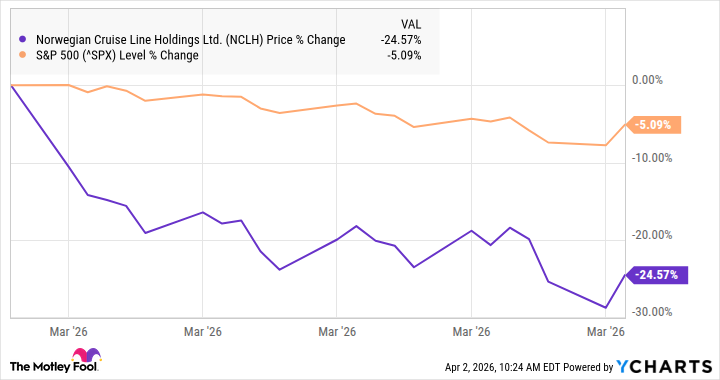

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

Nvidia Projects $1 Trillion in Sales by 2027

- Surging Sales Projections: Nvidia CEO Jensen Huang announced at the 2026 GTC event that the company expects lifetime sales of its current-generation Blackwell chips and next-generation Vera Rubin chips to reach $1 trillion by the end of 2027, indicating significant future growth potential.

- Significant Revenue Growth: Analysts predict Nvidia's revenue for FY 2027 will hit $369 billion, a 71% year-over-year increase, with FY 2028 expected to reach $480 billion, reflecting strong demand and market share expansion in the AI sector.

- Market's Tepid Response: Despite Huang's robust sales forecast indicating strong growth potential, the market has reacted lukewarmly, with Nvidia's stock price declining since the announcement, suggesting investors may be underestimating the company's long-term growth prospects.

- Investment Opportunity Emerges: Currently, Nvidia's P/E ratio stands at 35, significantly higher than the S&P 500's 23.8, indicating that the market expects 2026 to be a strong year while overlooking Nvidia's long-term profitability in AI development, prompting investors to consider buying while the stock remains undervalued.

See More

Nvidia's Earnings Report Shows Strong Growth

- Significant Revenue Growth: Nvidia's revenue in Q4 of fiscal 2026 surged 73% year-over-year to $68.1 billion, primarily driven by its data center segment, which generated $62.3 billion in revenue, up 75% year-over-year.

- Profitability Improvement: The company reported non-GAAP earnings per share of $1.62, an 82% increase year-over-year, while maintaining an impressive adjusted gross margin of 75.2%, showcasing its strong pricing power and production scale within its hardware ecosystem.

- Optimistic Future Outlook: Management anticipates first-quarter revenue for fiscal 2027 to be approximately $78 billion, indicating that the company's growth in the AI sector is still in its early stages, with the data center business expanding nearly 13 times since fiscal 2023.

- Valuation Outlook Analysis: Despite a current price-to-earnings ratio of about 36, the forward P/E ratio is expected to drop to 21 over the next four quarters, and if the company meets Wall Street's earnings expectations, the stock price could appreciate by 12% over the next year, reaching around $197.

See More

Nvidia Reopens Key AI Market in China Amid Risks

- Market Reopening: Nvidia has reopened its operations in China, one of the world's most crucial AI markets, presenting potential for revenue growth despite existing policy risks that complicate the narrative.

- Policy Risks: While the opportunities in the Chinese market are significant, uncertainties surrounding government regulations and market access could impact Nvidia's long-term strategic positioning in the region.

- Investment Opportunities: Analysts suggest that despite the high costs associated with re-entering the market, Nvidia could leverage technological innovation and adaptability to capture growth opportunities in China, enhancing its global competitiveness.

- Future Outlook: As demand for AI technology continues to rise in China, Nvidia's market strategy will need to be agile to navigate the complex policy landscape and maximize returns on its investments in the region.

See More

Chinese Semiconductor Industry Hits Record Revenue

- Significant Revenue Growth: Semiconductor Manufacturing International Co. (SMIC) reported a revenue of $9.3 billion for 2025, a 16% increase year-on-year, with projections suggesting revenues could exceed $11 billion in 2026, highlighting the robust growth potential of China's semiconductor sector driven by AI demand.

- Strong Performance from Hua Hong: Hua Hong Semiconductor achieved a record revenue of $659.9 million in Q4, with future sales expected between $650 million and $660 million, reflecting sustained domestic demand for semiconductors and the company's solid market positioning.

- Surge in Memory Chip Demand: ChangXin Memory Technologies (CXMT) saw a 130% year-on-year revenue increase, surpassing 55 billion yuan ($8 billion), indicating the rise of Chinese firms in the high-bandwidth memory market amid global shortages.

- Ongoing Technical Challenges: Despite record revenues, Chinese semiconductor companies still lag behind their U.S., South Korean, and Taiwanese counterparts in technological capabilities, particularly in producing advanced chips at scale, facing ongoing pressure from U.S. export controls.

See More

Investment Risk Alert: Etsy, Nike, Tesla

- Etsy Sales Decline: Etsy's gross merchandise sales fell by 5.3% year-over-year in 2025, and while there was a slight recovery in Q4 excluding Reverb sales, the overall decrease in active buyers and sellers alongside a drop in net income indicates a weakening market position.

- Nike's Weak Performance: In its Q3 fiscal 2026 report, Nike showed flat year-over-year revenue despite a 5% increase in wholesale revenue, as direct sales declined by 4%, highlighting ongoing market share losses, particularly with a 7% drop in sales in China.

- Tesla's Growth Obstacles: Despite exceeding a $1 trillion market cap, Tesla's revenue dipped by 3% year-over-year in 2025, with a 10% decline in automobile sales and a 46% drop in GAAP net income, indicating significant challenges in sustaining growth in the electric vehicle market.

- Investor Confidence Shaken: With the declining performance of Etsy, Nike, and Tesla, investor confidence in these once high-flying stocks is waning, prompting analysts to suggest considering divestment ahead of upcoming earnings reports to avoid potential larger losses.

See More

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

Nvidia Projects $1 Trillion in Sales by 2027

- Surging Sales Projections: Nvidia CEO Jensen Huang announced at the 2026 GTC event that the company expects lifetime sales of its current-generation Blackwell chips and next-generation Vera Rubin chips to reach $1 trillion by the end of 2027, indicating significant future growth potential.

- Significant Revenue Growth: Analysts predict Nvidia's revenue for FY 2027 will hit $369 billion, a 71% year-over-year increase, with FY 2028 expected to reach $480 billion, reflecting strong demand and market share expansion in the AI sector.

- Market's Tepid Response: Despite Huang's robust sales forecast indicating strong growth potential, the market has reacted lukewarmly, with Nvidia's stock price declining since the announcement, suggesting investors may be underestimating the company's long-term growth prospects.

- Investment Opportunity Emerges: Currently, Nvidia's P/E ratio stands at 35, significantly higher than the S&P 500's 23.8, indicating that the market expects 2026 to be a strong year while overlooking Nvidia's long-term profitability in AI development, prompting investors to consider buying while the stock remains undervalued.

See More