Middle East Turmoil Fuels Renewed Interest in Wind Energy Investments

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 1 day ago

0mins

Source: seekingalpha

- Positive Wind Outlook: The IEA projects that wind generation will more than double by 2040, driven by robust structural electricity demand growth from AI data centers and industrial electrification, despite ongoing short-term policy uncertainties and offshore project cost pressures.

- Shifting Market Dynamics: The wind energy sector is transitioning from a growth-only model to one focused on profitability, necessitating a detailed analysis of each player's strategic decisions and past financial performance as the industry matures.

- Acquisition Opportunities: AES Corp. (AES) is being acquired at an attractive valuation, highlighting market interest in quality assets, while GE Vernova (GEV) and Vistra (VST) are positioned to benefit from surging orders once their wind divisions stabilize.

- High Policy Dependency: While wind energy and other renewables like solar are experiencing growth, they remain highly dependent on policy decisions, with profitability and margins under pressure, necessitating close attention to strategic adjustments by companies in the sector.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GEV?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GEV

Wall Street analysts forecast GEV stock price to fall

24 Analyst Rating

20 Buy

4 Hold

0 Sell

Strong Buy

Current: 1073.080

Low

714.00

Averages

858.23

High

1087

Current: 1073.080

Low

714.00

Averages

858.23

High

1087

About GEV

GE Vernova Inc. is a purpose-built global energy company that includes Power, Wind, and Electrification segments and is supported by its accelerator businesses. It designs, manufactures, delivers, and services technologies to create a sustainable electric power system, enabling electrification and decarbonization. Power segment includes the design, manufacture, and servicing of gas, nuclear, hydro, and steam technologies, providing a critical foundation of dispatchable, flexible, stable, and reliable power. Wind segment includes its wind generation technologies, inclusive of onshore and offshore wind turbines and blades. Electrification segment includes grid solutions, power conversion and storage, and electrification software technologies required for the transmission, distribution, conversion, storage, and orchestration of electricity from point of generation to point of consumption. Its accelerator business includes advanced research, consulting services and financial services.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Nuclear Industry Partnerships Accelerate Development

- Accelerated Industry Collaboration: Brookfield Asset Management and The Nuclear Company have partnered to deploy Westinghouse AP1000 and AP300 reactors, marking significant progress in the rapid deployment of new reactors, which is expected to drive the implementation of nuclear projects in the U.S.

- Exploration of Innovative Models: Blue Energy's collaboration with GE Vernova to develop a gas-plus-nuclear hybrid approach showcases the private sector's execution capabilities in nuclear innovation deployment, potentially attracting more investments and boosting market confidence.

- Rising Public Support: A recent Gallup poll indicates record public support for nuclear energy, alongside a decline in enthusiasm for solar and wind, providing a positive policy environment and market foundation for nuclear development.

- Investment Opportunities in Indices: The VettaFi Nuclear Renaissance Index (NUKZX) offers investors exposure to companies benefiting from nuclear development trends, including key reactor technology owners and equipment providers, which are expected to generate substantial revenue from these new projects.

See More

Middle East Turmoil Fuels Renewed Interest in Wind Energy Investments

- Positive Wind Outlook: The IEA projects that wind generation will more than double by 2040, driven by robust structural electricity demand growth from AI data centers and industrial electrification, despite ongoing short-term policy uncertainties and offshore project cost pressures.

- Shifting Market Dynamics: The wind energy sector is transitioning from a growth-only model to one focused on profitability, necessitating a detailed analysis of each player's strategic decisions and past financial performance as the industry matures.

- Acquisition Opportunities: AES Corp. (AES) is being acquired at an attractive valuation, highlighting market interest in quality assets, while GE Vernova (GEV) and Vistra (VST) are positioned to benefit from surging orders once their wind divisions stabilize.

- High Policy Dependency: While wind energy and other renewables like solar are experiencing growth, they remain highly dependent on policy decisions, with profitability and margins under pressure, necessitating close attention to strategic adjustments by companies in the sector.

See More

NuScale Power Faces Growth Challenges Amidst Market Decline

- Market Performance Decline: NuScale Power's stock has plummeted from $57 last October to $12 today, reducing its market cap from approximately $17 billion to $4 billion, indicating market concerns over its future profitability.

- Revenue Growth Requirement: To support a $40 billion market cap, NuScale must increase its 2025 revenue from $31.5 million to $1.7 billion, a daunting 54-fold increase, especially given the lack of actual sales.

- Slow Project Progress: While NuScale is advancing its partnership with ENTRA1 Energy to deploy 6GW of small modular reactors in Tennessee, it has yet to deploy a single reactor, adding to investor uncertainty.

- Profitability Comparison: Compared to Constellation Energy's $115 billion and GE Vernova's $290 billion market valuations, NuScale's lack of profitability and ongoing cash burn make its future market performance even more uncertain.

See More

NuScale Power Stock Down 75% Yet Positive Outlook Persists

- Significant Stock Decline: NuScale Power's stock has plummeted 75% from its October high of $57 to approximately $12, resulting in a market cap of $4 billion, raising concerns about its future profitability despite still being considered expensive by conventional standards.

- Revenue Growth Challenge: With projected revenue of only $31.5 million in 2025, NuScale would need to increase its annual revenue to $1.7 billion to support a $120 stock price, representing a daunting 54-fold increase that poses substantial commercial hurdles.

- Positive Project Developments: The company is nearing the launch of its first project in Romania and plans to deploy up to 6 gigawatts of its small modular reactor technology in partnership with ENTRA1 Energy for the Tennessee Valley Authority, indicating potential market opportunities for its technology.

- Market Valuation Comparison: Unlike profitable competitors such as Constellation Energy and GE Vernova, NuScale has yet to achieve profitability or complete any SMR sales, creating significant uncertainty regarding its future market valuation and investor confidence.

See More

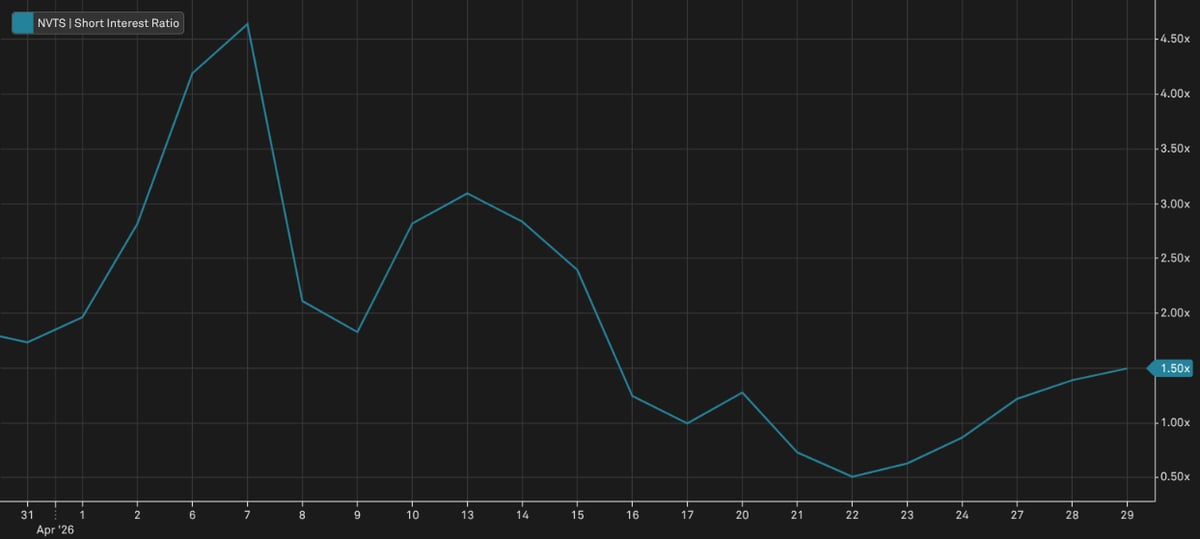

Navitas Semiconductor Stock Soars 121% Amid AI Investment Surge

- Stock Surge: Navitas Semiconductor's stock has surged 121% in 2026, with an impressive 88.1% increase in April alone, reflecting strong market confidence in its potential within the AI investment cycle, particularly as short sellers were forced to cover their positions, driving the price sharply higher.

- Market Trends: The Philadelphia Semiconductor Index rose 38% in April, indicating ongoing robust demand for AI-related investments, and Navitas, as a leading manufacturer of gallium nitride and silicon carbide chips, is well-positioned to benefit from this trend, with management shifting focus towards data centers and high-performance computing.

- Technological Innovation: In mid-March, Navitas announced its latest power delivery board capable of direct conversion from 800 V to 6 V, a critical component of the 800 VDC data center technology being developed by Nvidia, further solidifying its position in the industry.

- Profitability Outlook: With the continued growth in data center investments, Navitas could potentially become profitable and cash-generative in the coming years, especially as companies like GE Vernova raise their full-year guidance, creating optimistic expectations for Navitas's future performance.

See More

Vertiv Stock Soars 121.5% Amid Strong AI Data Center Demand

- Significant Stock Surge: Vertiv's stock has surged 121.5% in 2026, with a remarkable 31.1% increase in April alone, reflecting strong investor confidence in its role within the AI data center infrastructure sector.

- Earnings Beat Expectations: The company raised its full-year net sales guidance to $13.5 billion to $14 billion from a previous range of $13.25 billion to $13.75 billion, indicating robust business growth momentum.

- Increased Profit Forecast: The adjusted full-year earnings per share (EPS) expectation has risen from $6.02 to $6.35, showcasing the company's optimistic outlook for the second half of the year, with the CEO highlighting sustained strong demand for data centers.

- Collaboration with Nvidia: Vertiv's partnership with Nvidia is advancing the development of 800 VDC data center power infrastructure, focusing on power and cooling solutions compatible with AI architecture, thereby solidifying its position in the rapidly evolving AI market.

See More

Nuclear Industry Partnerships Accelerate Development

- Accelerated Industry Collaboration: Brookfield Asset Management and The Nuclear Company have partnered to deploy Westinghouse AP1000 and AP300 reactors, marking significant progress in the rapid deployment of new reactors, which is expected to drive the implementation of nuclear projects in the U.S.

- Exploration of Innovative Models: Blue Energy's collaboration with GE Vernova to develop a gas-plus-nuclear hybrid approach showcases the private sector's execution capabilities in nuclear innovation deployment, potentially attracting more investments and boosting market confidence.

- Rising Public Support: A recent Gallup poll indicates record public support for nuclear energy, alongside a decline in enthusiasm for solar and wind, providing a positive policy environment and market foundation for nuclear development.

- Investment Opportunities in Indices: The VettaFi Nuclear Renaissance Index (NUKZX) offers investors exposure to companies benefiting from nuclear development trends, including key reactor technology owners and equipment providers, which are expected to generate substantial revenue from these new projects.

See More

Middle East Turmoil Fuels Renewed Interest in Wind Energy Investments

- Positive Wind Outlook: The IEA projects that wind generation will more than double by 2040, driven by robust structural electricity demand growth from AI data centers and industrial electrification, despite ongoing short-term policy uncertainties and offshore project cost pressures.

- Shifting Market Dynamics: The wind energy sector is transitioning from a growth-only model to one focused on profitability, necessitating a detailed analysis of each player's strategic decisions and past financial performance as the industry matures.

- Acquisition Opportunities: AES Corp. (AES) is being acquired at an attractive valuation, highlighting market interest in quality assets, while GE Vernova (GEV) and Vistra (VST) are positioned to benefit from surging orders once their wind divisions stabilize.

- High Policy Dependency: While wind energy and other renewables like solar are experiencing growth, they remain highly dependent on policy decisions, with profitability and margins under pressure, necessitating close attention to strategic adjustments by companies in the sector.

See More

NuScale Power Faces Growth Challenges Amidst Market Decline

- Market Performance Decline: NuScale Power's stock has plummeted from $57 last October to $12 today, reducing its market cap from approximately $17 billion to $4 billion, indicating market concerns over its future profitability.

- Revenue Growth Requirement: To support a $40 billion market cap, NuScale must increase its 2025 revenue from $31.5 million to $1.7 billion, a daunting 54-fold increase, especially given the lack of actual sales.

- Slow Project Progress: While NuScale is advancing its partnership with ENTRA1 Energy to deploy 6GW of small modular reactors in Tennessee, it has yet to deploy a single reactor, adding to investor uncertainty.

- Profitability Comparison: Compared to Constellation Energy's $115 billion and GE Vernova's $290 billion market valuations, NuScale's lack of profitability and ongoing cash burn make its future market performance even more uncertain.

See More

NuScale Power Stock Down 75% Yet Positive Outlook Persists

- Significant Stock Decline: NuScale Power's stock has plummeted 75% from its October high of $57 to approximately $12, resulting in a market cap of $4 billion, raising concerns about its future profitability despite still being considered expensive by conventional standards.

- Revenue Growth Challenge: With projected revenue of only $31.5 million in 2025, NuScale would need to increase its annual revenue to $1.7 billion to support a $120 stock price, representing a daunting 54-fold increase that poses substantial commercial hurdles.

- Positive Project Developments: The company is nearing the launch of its first project in Romania and plans to deploy up to 6 gigawatts of its small modular reactor technology in partnership with ENTRA1 Energy for the Tennessee Valley Authority, indicating potential market opportunities for its technology.

- Market Valuation Comparison: Unlike profitable competitors such as Constellation Energy and GE Vernova, NuScale has yet to achieve profitability or complete any SMR sales, creating significant uncertainty regarding its future market valuation and investor confidence.

See More

Navitas Semiconductor Stock Soars 121% Amid AI Investment Surge

- Stock Surge: Navitas Semiconductor's stock has surged 121% in 2026, with an impressive 88.1% increase in April alone, reflecting strong market confidence in its potential within the AI investment cycle, particularly as short sellers were forced to cover their positions, driving the price sharply higher.

- Market Trends: The Philadelphia Semiconductor Index rose 38% in April, indicating ongoing robust demand for AI-related investments, and Navitas, as a leading manufacturer of gallium nitride and silicon carbide chips, is well-positioned to benefit from this trend, with management shifting focus towards data centers and high-performance computing.

- Technological Innovation: In mid-March, Navitas announced its latest power delivery board capable of direct conversion from 800 V to 6 V, a critical component of the 800 VDC data center technology being developed by Nvidia, further solidifying its position in the industry.

- Profitability Outlook: With the continued growth in data center investments, Navitas could potentially become profitable and cash-generative in the coming years, especially as companies like GE Vernova raise their full-year guidance, creating optimistic expectations for Navitas's future performance.

See More

Vertiv Stock Soars 121.5% Amid Strong AI Data Center Demand

- Significant Stock Surge: Vertiv's stock has surged 121.5% in 2026, with a remarkable 31.1% increase in April alone, reflecting strong investor confidence in its role within the AI data center infrastructure sector.

- Earnings Beat Expectations: The company raised its full-year net sales guidance to $13.5 billion to $14 billion from a previous range of $13.25 billion to $13.75 billion, indicating robust business growth momentum.

- Increased Profit Forecast: The adjusted full-year earnings per share (EPS) expectation has risen from $6.02 to $6.35, showcasing the company's optimistic outlook for the second half of the year, with the CEO highlighting sustained strong demand for data centers.

- Collaboration with Nvidia: Vertiv's partnership with Nvidia is advancing the development of 800 VDC data center power infrastructure, focusing on power and cooling solutions compatible with AI architecture, thereby solidifying its position in the rapidly evolving AI market.

See More