Microsoft's AI Business Surpasses $37 Billion Annual Revenue

Written by Emily J. Thompson, Senior Investment Analyst

Updated: 7 hours ago

0mins

Source: Fool

- AI Revenue Surge: Microsoft's AI business has surpassed a $37 billion annual revenue run rate, demonstrating how AI demand is effectively translating into cloud and software revenue, thereby reinforcing its competitive advantage in the market.

- Stock Price Increase: Microsoft shares rose by 5.25% to close at $450.24, primarily driven by strong AI-driven revenue growth and robust performance in Xbox and software, reflecting investor confidence in the company's future growth prospects.

- Surge in Trading Volume: The trading volume reached 77.2 million shares, which is 124% above the three-month average, indicating a significant increase in market interest in Microsoft stock, potentially signaling optimistic investor sentiment regarding its future performance.

- In-House AI Model Development: Microsoft is preparing to develop more in-house AI models to cut costs and enhance flexibility, a strategy that not only helps control expenses but may also improve its pricing and margin advantages in AI workloads.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 426.990

Low

500.00

Averages

631.36

High

678.00

Current: 426.990

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company. The Company develops and supports software, services, devices, and solutions. The Company’s segments include Productivity and Business Processes, Intelligent Cloud, and More Personal Computing. The Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services. This segment primarily comprises: Office Commercial, Office Consumer, LinkedIn, and Dynamics business solutions. The Intelligent Cloud segment consists of server products and cloud services, including Azure and other cloud services, SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), and Nuance and GitHub; and Enterprise Services, including enterprise support services, industry solutions and Nuance professional services. The More Personal Computing segment primarily comprises Windows, Devices, Gaming, and search and news advertising.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft Stock Investment Opportunity Arises

- Historically Cheap: Microsoft stock is currently trading at around 24 times earnings, significantly lower than its historical average over the past decade, making it an attractive investment opportunity, especially after the bear market of 2022, which has drawn investor interest.

- New Agreement with OpenAI: Microsoft is set to benefit from its new agreement with OpenAI in the next fiscal quarter, with projected income rising to $6 billion from the previously anticipated $4 billion, alleviating investor concerns about cash flow while reducing overall exposure to OpenAI.

- Launch of E7 Platform: On May 1, Microsoft launched Microsoft 365 E7 at $99 per user per month, expected to boost revenue by 2.4% to 2.5%, integrating various products and enhancing enterprise management of AI agents, which could lead to significant revenue increases.

- Analyst Optimism: With 95% of analysts rating Microsoft as a buy and a median 12-month price target of $550, approximately 30% above its current price, there is strong market confidence in Microsoft's growth potential moving forward.

See More

Dell Technologies Secures $10 Billion Contract, Stock Hits All-Time High

- Contract Awarded: Dell Technologies has secured a five-year, $10 billion contract from the U.S. Department of Defense to provide software solutions, including Microsoft 365, which is expected to save the agency $422 million annually, enhancing the company's competitive position in the government sector.

- Stock Surge: After climbing for the seventh consecutive trading session, Dell's stock reached an all-time high of $429.15 before closing at $420.91, reflecting a 32.76% increase, indicating strong investor enthusiasm following the company's robust earnings performance.

- Strong Financial Performance: In the first quarter, Dell reported a staggering 256% increase in net income to $3.4 billion, with net revenues rising 88% to $43.8 billion year-over-year, showcasing the company's strong growth momentum and profitability in the market.

- Market Outlook: While Dell Technologies demonstrates significant investment potential, analysts suggest that certain AI stocks may offer greater upside potential and lower downside risk, prompting investors to carefully assess market dynamics.

See More

Analysis of Three Cheapest Tech Stocks in Magnificent Seven

- Nvidia's Market Position: Nvidia's leadership in the GPU market has allowed it to benefit from the AI boom over the past three years, and despite its forward P/E of 23.8 making it the second cheapest tech stock, concerns about future competition and CPU demand persist in the market.

- Microsoft's Investment Outlook: Microsoft plans to spend $190 billion on capital expenditures in 2026, primarily to support its cloud computing and AI businesses; although the market remains skeptical about its declining stock price, its forward P/E of 24.5 indicates strong investment potential.

- Meta Platforms' User Growth Challenges: With a forward P/E of about 19.3, Meta Platforms faces pressures from declining daily active users and increased capital expenditures, yet its vast user ecosystem and AI-driven advertising business still provide diverse monetization opportunities.

- Long-Term Investor Outlook: While the forward P/E ratio is a crucial metric for assessing stock value, Nvidia, Microsoft, and Meta Platforms demonstrate strong long-term investment potential due to their innovative capabilities and competitive advantages.

See More

Valuation Analysis of the Magnificent Seven Tech Giants

- Nvidia's Market Position: As the leader in the GPU market, Nvidia has benefited from the AI boom over the past three years, and despite its forward P/E of 23.8, it remains the second cheapest among the Magnificent Seven, indicating significant future growth potential.

- Microsoft's Capital Expenditure: Microsoft plans to invest $190 billion in capital expenditures in 2026, primarily to support its cloud computing and AI businesses; although the market remains skeptical about its future performance, its forward P/E of 24.5 suggests investment value.

- Meta Platforms' User Growth: With a forward P/E of about 19.3, Meta faces pressures from declining daily active users and increased capital expenditures, yet its vast user ecosystem and AI-driven advertising business provide strong growth potential.

- Long-Term Investment Outlook: While the forward P/E ratio is a crucial metric for assessing stock value, Nvidia, Microsoft, and Meta still demonstrate robust long-term investment prospects due to their innovative capabilities and competitive advantages.

See More

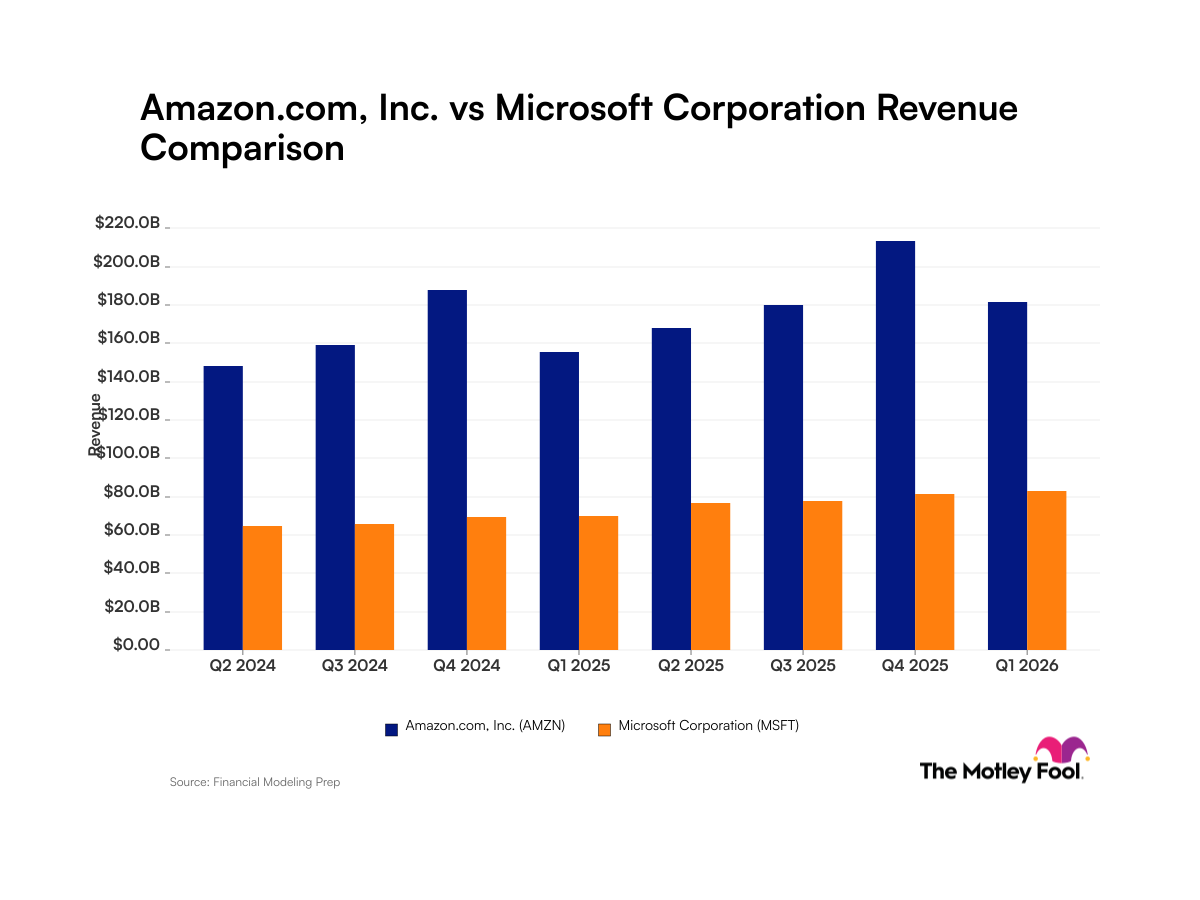

Financial Comparison Between Amazon and Microsoft

- Revenue Comparison: Amazon reported total revenue of $181.5 billion, reflecting a 17% year-over-year increase, while Microsoft achieved $82.9 billion, with an 18% growth, indicating strong performances from both companies despite Amazon's higher total revenue.

- Cloud Growth: Amazon's AWS generated $37.6 billion in sales during Q1, marking a 28% year-over-year increase, while Microsoft's cloud revenue also rose 29% to $54.5 billion, highlighting the intensifying competition in the AI sector between the two giants.

- Profit Margin Discrepancy: Amazon's net income margin stands at 17%, significantly lower than Microsoft's 38%, which reflects Microsoft's superior cost control and profitability, potentially influencing investor perceptions of both companies' long-term viability.

- Market Share Competition: While Amazon leads in cloud computing market share, Microsoft's AI business saw an impressive annual revenue run rate increase of 123%, showcasing its potential in technological innovation and market adaptability, prompting investors to monitor future market dynamics.

See More

Amazon and Microsoft Quarterly Revenue Analysis

- Amazon Revenue Growth: In Q1 2026, Amazon reported revenue of $181.5 billion, a 17% year-over-year increase, with its cloud computing segment, AWS, achieving sales of $37.6 billion, reflecting a robust 28% growth year-over-year, underscoring its strong demand in the AI sector and market leadership.

- Microsoft Steady Revenue: Microsoft generated $82.9 billion in revenue for Q1 2026, marking an 18% year-over-year increase, with its AI business experiencing a remarkable annual revenue run rate increase of 123%, indicating its competitiveness in the rapidly evolving cloud computing market, particularly with cloud revenue rising 29% to $54.5 billion.

- Market Competition Landscape: Amazon and Microsoft are in fierce competition within the cloud computing sector, with Amazon leading in market share while Microsoft follows closely, both investing heavily in AI products to meet the surging customer demand, thereby driving overall revenue growth.

- Strategic Investments and Future Outlook: Both Amazon and Microsoft have made significant investments in AI infrastructure, with Amazon's AWS upgrades supporting rapid growth in its cloud business, while Microsoft's AI segment also shows strong growth potential, attracting investor interest in the future trajectories of both companies.

See More

Microsoft Stock Investment Opportunity Arises

- Historically Cheap: Microsoft stock is currently trading at around 24 times earnings, significantly lower than its historical average over the past decade, making it an attractive investment opportunity, especially after the bear market of 2022, which has drawn investor interest.

- New Agreement with OpenAI: Microsoft is set to benefit from its new agreement with OpenAI in the next fiscal quarter, with projected income rising to $6 billion from the previously anticipated $4 billion, alleviating investor concerns about cash flow while reducing overall exposure to OpenAI.

- Launch of E7 Platform: On May 1, Microsoft launched Microsoft 365 E7 at $99 per user per month, expected to boost revenue by 2.4% to 2.5%, integrating various products and enhancing enterprise management of AI agents, which could lead to significant revenue increases.

- Analyst Optimism: With 95% of analysts rating Microsoft as a buy and a median 12-month price target of $550, approximately 30% above its current price, there is strong market confidence in Microsoft's growth potential moving forward.

See More

Dell Technologies Secures $10 Billion Contract, Stock Hits All-Time High

- Contract Awarded: Dell Technologies has secured a five-year, $10 billion contract from the U.S. Department of Defense to provide software solutions, including Microsoft 365, which is expected to save the agency $422 million annually, enhancing the company's competitive position in the government sector.

- Stock Surge: After climbing for the seventh consecutive trading session, Dell's stock reached an all-time high of $429.15 before closing at $420.91, reflecting a 32.76% increase, indicating strong investor enthusiasm following the company's robust earnings performance.

- Strong Financial Performance: In the first quarter, Dell reported a staggering 256% increase in net income to $3.4 billion, with net revenues rising 88% to $43.8 billion year-over-year, showcasing the company's strong growth momentum and profitability in the market.

- Market Outlook: While Dell Technologies demonstrates significant investment potential, analysts suggest that certain AI stocks may offer greater upside potential and lower downside risk, prompting investors to carefully assess market dynamics.

See More

Analysis of Three Cheapest Tech Stocks in Magnificent Seven

- Nvidia's Market Position: Nvidia's leadership in the GPU market has allowed it to benefit from the AI boom over the past three years, and despite its forward P/E of 23.8 making it the second cheapest tech stock, concerns about future competition and CPU demand persist in the market.

- Microsoft's Investment Outlook: Microsoft plans to spend $190 billion on capital expenditures in 2026, primarily to support its cloud computing and AI businesses; although the market remains skeptical about its declining stock price, its forward P/E of 24.5 indicates strong investment potential.

- Meta Platforms' User Growth Challenges: With a forward P/E of about 19.3, Meta Platforms faces pressures from declining daily active users and increased capital expenditures, yet its vast user ecosystem and AI-driven advertising business still provide diverse monetization opportunities.

- Long-Term Investor Outlook: While the forward P/E ratio is a crucial metric for assessing stock value, Nvidia, Microsoft, and Meta Platforms demonstrate strong long-term investment potential due to their innovative capabilities and competitive advantages.

See More

Valuation Analysis of the Magnificent Seven Tech Giants

- Nvidia's Market Position: As the leader in the GPU market, Nvidia has benefited from the AI boom over the past three years, and despite its forward P/E of 23.8, it remains the second cheapest among the Magnificent Seven, indicating significant future growth potential.

- Microsoft's Capital Expenditure: Microsoft plans to invest $190 billion in capital expenditures in 2026, primarily to support its cloud computing and AI businesses; although the market remains skeptical about its future performance, its forward P/E of 24.5 suggests investment value.

- Meta Platforms' User Growth: With a forward P/E of about 19.3, Meta faces pressures from declining daily active users and increased capital expenditures, yet its vast user ecosystem and AI-driven advertising business provide strong growth potential.

- Long-Term Investment Outlook: While the forward P/E ratio is a crucial metric for assessing stock value, Nvidia, Microsoft, and Meta still demonstrate robust long-term investment prospects due to their innovative capabilities and competitive advantages.

See More

Financial Comparison Between Amazon and Microsoft

- Revenue Comparison: Amazon reported total revenue of $181.5 billion, reflecting a 17% year-over-year increase, while Microsoft achieved $82.9 billion, with an 18% growth, indicating strong performances from both companies despite Amazon's higher total revenue.

- Cloud Growth: Amazon's AWS generated $37.6 billion in sales during Q1, marking a 28% year-over-year increase, while Microsoft's cloud revenue also rose 29% to $54.5 billion, highlighting the intensifying competition in the AI sector between the two giants.

- Profit Margin Discrepancy: Amazon's net income margin stands at 17%, significantly lower than Microsoft's 38%, which reflects Microsoft's superior cost control and profitability, potentially influencing investor perceptions of both companies' long-term viability.

- Market Share Competition: While Amazon leads in cloud computing market share, Microsoft's AI business saw an impressive annual revenue run rate increase of 123%, showcasing its potential in technological innovation and market adaptability, prompting investors to monitor future market dynamics.

See More

Amazon and Microsoft Quarterly Revenue Analysis

- Amazon Revenue Growth: In Q1 2026, Amazon reported revenue of $181.5 billion, a 17% year-over-year increase, with its cloud computing segment, AWS, achieving sales of $37.6 billion, reflecting a robust 28% growth year-over-year, underscoring its strong demand in the AI sector and market leadership.

- Microsoft Steady Revenue: Microsoft generated $82.9 billion in revenue for Q1 2026, marking an 18% year-over-year increase, with its AI business experiencing a remarkable annual revenue run rate increase of 123%, indicating its competitiveness in the rapidly evolving cloud computing market, particularly with cloud revenue rising 29% to $54.5 billion.

- Market Competition Landscape: Amazon and Microsoft are in fierce competition within the cloud computing sector, with Amazon leading in market share while Microsoft follows closely, both investing heavily in AI products to meet the surging customer demand, thereby driving overall revenue growth.

- Strategic Investments and Future Outlook: Both Amazon and Microsoft have made significant investments in AI infrastructure, with Amazon's AWS upgrades supporting rapid growth in its cloud business, while Microsoft's AI segment also shows strong growth potential, attracting investor interest in the future trajectories of both companies.

See More