Microsoft to Report Q2 Results on Jan 28, AI Business May Be Turning Point

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 15 2026

0mins

Should l Buy MSFT?

Source: Fool

- Earnings Report Anticipation: Microsoft is set to announce its fiscal 2026 second-quarter results on January 28, with investors looking for further growth in its AI-related software and cloud businesses, especially after an 11% decline in stock price over the last three months, which could mark a turning point.

- Copilot Adoption Update: As of the fiscal 2026 first quarter, 90% of Fortune 500 companies are using Copilot, with global enterprises paying for over 400 million licenses for the 365 platform, indicating strong market demand that is expected to drive Microsoft's revenue growth.

- Azure Growth Acceleration: Microsoft's Azure cloud computing platform achieved a 40% revenue growth in the fiscal 2026 first quarter, with demand for AI data center capacity outstripping supply, resulting in a $392 billion order backlog, leading to plans to double data center capacity over the next two years.

- Stock Attractiveness: With Microsoft’s stock down 11% from its record high and a P/E ratio of 34.1, analysts project earnings of $15.75 per share by the end of fiscal 2026, suggesting a realistic 15% price increase potential over the next six months if growth continues.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MSFT?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MSFT

Wall Street analysts forecast MSFT stock price to rise

34 Analyst Rating

32 Buy

2 Hold

0 Sell

Strong Buy

Current: 399.410

Low

500.00

Averages

631.36

High

678.00

Current: 399.410

Low

500.00

Averages

631.36

High

678.00

About MSFT

Microsoft Corporation is a technology company that develops and supports software, services, devices, and solutions. Its Productivity and Business Processes segment consists of products and services in its portfolio of productivity, communication, and information services, spanning a variety of devices and platforms. It comprises Microsoft 365 Commercial products and cloud services; Microsoft 365 Consumer products and cloud services; LinkedIn, and Dynamics products and cloud services. The Intelligent Cloud segment consists of its public, private, and hybrid server products and cloud services. It comprises server products and cloud services, including Azure, and enterprise and partner services, including Enterprise Support Services. Its More Personal Computing segment primarily comprises Windows and Devices, including Windows OEM licensing; Gaming, including Xbox hardware and Xbox content; Search and news advertising, comprising Bing and Copilot, Microsoft News, and Microsoft Edge.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Microsoft Raises Enterprise Subscription Price by 65%

- Price Increase Strategy: Microsoft has announced that its top-tier Microsoft 365 E7 enterprise plan will see a monthly fee increase to $99, representing a 65% hike from the previous price, aimed at boosting AI revenue to offset the $72 billion spent on infrastructure over the past two quarters.

- Market Potential Exploration: Currently, Microsoft has only 15 million paying Copilot accounts, while there are 450 million Microsoft 365 commercial customers, indicating significant potential for Microsoft to tap into a larger pool of high-paying AI customers who have yet to upgrade.

- Increased Competitive Pressure: With ChatGPT boasting over 50 million paying subscribers, Microsoft faces intense competition and must quickly attract enterprise users to subscribe to its AI services to prevent them from shifting to alternative AI solutions.

- Growth Monitoring Necessity: Although Microsoft's cloud service sales rose by 17% in the second quarter, commercial seats only increased by 6%, prompting investors to closely monitor the acceleration of both sales and paying subscribers to assess the effectiveness of Microsoft's new AI strategy.

See More

Surge in Demand for AI Data Center Construction

- Massive Investment: The four hyperscalers, including Alphabet, Microsoft, Meta, and Amazon, have committed nearly $700 billion in capital expenditures this year to support the construction of AI data centers, reflecting strong confidence in future technological infrastructure.

- Job Creation: Amazon's $12 billion investment in a new AI data center in Louisiana is expected to create 540 full-time jobs directly and generate an additional 1,700 roles for electricians, technicians, and security specialists, significantly boosting the local economy.

- Skills Shortage Intensifies: According to Randstad's analysis, demand for robotic technicians is projected to increase by 107% from 2022 to 2026, while HVAC system engineers will see a 67% rise, indicating that the shortage of skilled labor poses a significant challenge to industry growth.

- Wage Growth Trend: Due to the scarcity of specialized workers, advertised wages for HVAC engineers have risen by 10% to 15% over the past four years, while professionals moving into high-level data center roles often experience a 25% to 30% salary increase, highlighting the urgent demand for technical talent in the sector.

See More

AI Data Center Boom Drives Surge in Skilled Labor Demand

- Significant Wage Growth: According to Kelly Services, specialized professionals transitioning to data center roles see a salary increase of 25% to 30%, reflecting not only the urgent demand for skilled labor but also the industry's increasing emphasis on talent acquisition and retention.

- Massive Investment: The four hyperscalers (Alphabet, Microsoft, Meta, and Amazon) have committed nearly $700 billion in 2023 for data center construction, with Amazon investing $12 billion in a new facility in Louisiana, expected to create 540 full-time jobs, thereby boosting the local economy.

- Labor Shortage Crisis: Randstad's analysis indicates a 107% increase in demand for robotic technicians and a 67% rise for HVAC engineers from 2022 to 2026, highlighting the escalating labor shortage as AI infrastructure demand surges, which may lead to overall wage increases in the sector.

- Emergence of New Collar Jobs: The rapid growth of data centers is fostering a unique environment where traditional blue-collar and white-collar workers will collaborate, creating a

See More

Accenture and Microsoft Collaborate on AI Implementation Strategy

- Forward Deployed Engineering: Accenture and Microsoft have developed a forward deployed engineering (FDE) strategy that connects software engineers directly with customers to customize and integrate AI tools, thereby accelerating enterprise AI implementation.

- Rapid Implementation Capability: This new strategy is expected to reduce the implementation time for enterprise AI initiatives from months to days, which not only enhances client responsiveness but also enables businesses to achieve measurable outcomes in AI transformation more swiftly.

- Combining Industry Expertise: The integration of Microsoft's AI platform with Accenture's industry expertise allows FDE teams to quickly deliver high-quality outcomes for customers, further strengthening both companies' competitive positions in the AI sector.

- Strategic Synergy: Manish Sharma, Accenture's Chief Strategy and Services Officer, emphasizes that the collaboration between strategy and engineering is crucial for enterprise AI success, and this partnership is set to drive greater efficiency and effectiveness in AI transformations.

See More

Gates Foundation's Investment Overview

- Asset Management Scale: Since its inception in 2000, the Gates Foundation has spent over $102 billion on charitable causes, with total trust assets currently at $86 billion, showcasing its significant influence in global philanthropy.

- Investment Concentration: The foundation's portfolio consists of 23 stocks, with 96% of its assets concentrated in its top 10 holdings, indicating a highly concentrated investment strategy, with its largest holding, Berkshire Hathaway, accounting for 28% of the portfolio.

- Berkshire Hathaway Contributions: As of the end of 2025, the foundation owned approximately 19.4 million Class B shares of Berkshire Hathaway, valued at about $9.8 billion, primarily due to Warren Buffett's long-term charitable contributions totaling $43.3 billion in stock over the years.

- Microsoft Holding Background: Microsoft ranks as the foundation's fourth-largest holding at 10.5%, primarily stemming from Bill Gates' donations, reflecting his ongoing support for the foundation while also demonstrating the foundation's flexibility in capital management.

See More

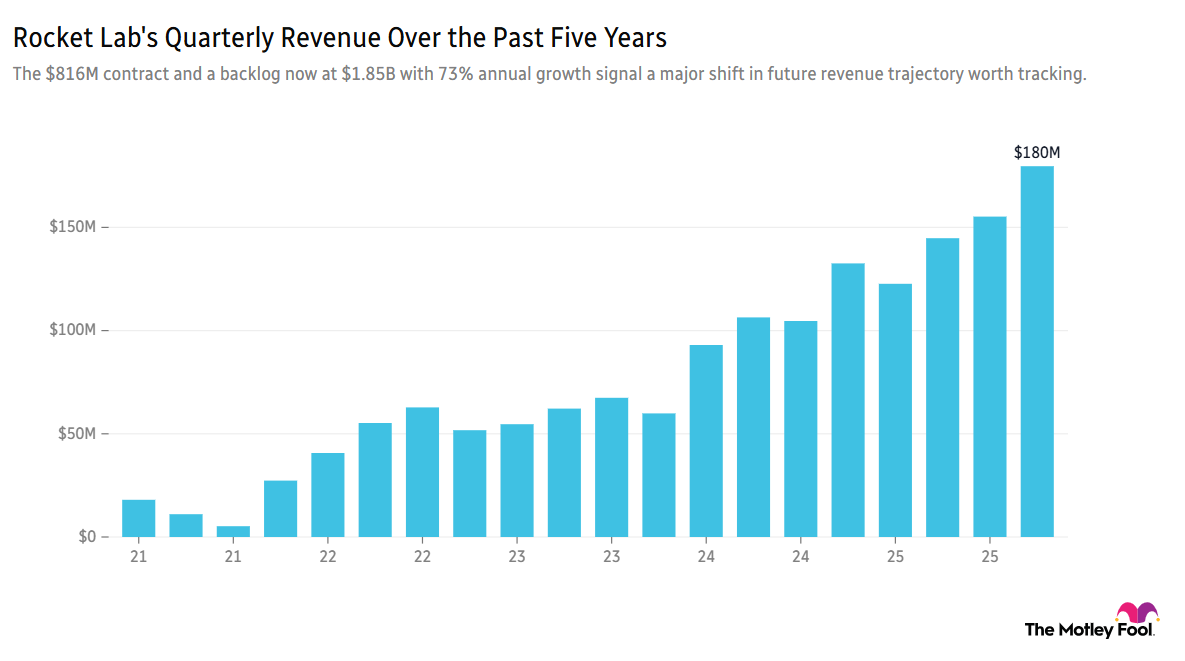

Rocket Lab Shares Surge 10% on New $816M Defense Contract

- Contract Boosts Stock: Rocket Lab (RKLB) shares surged 10.21% after securing an $816 million defense contract with the U.S. Space Development Agency, reflecting investor optimism ahead of upcoming launches dubbed 'Eight Days A Week' and 'Daughter of the Stars'.

- Market Volatility Impact: Despite a 3% pre-market dip due to a newly announced equity offering valued at up to $1 billion, Rocket Lab's stock performance remains 55% ahead of the S&P 500 since August 2025, indicating strong market resilience.

- AI Chip Competition Intensifies: Nvidia has received approval to ship its H200 processors to customers in China, as CEO Jensen Huang announced at the GTC conference, with the export deal cleared by both U.S. and Chinese authorities, further heating up the AI sector competition.

- Lululemon Earnings Impact: Lululemon (LULU) shares fell about 2% following its fourth-quarter earnings report, which showed an 18% year-over-year decline in EPS, although it still surpassed Wall Street expectations, highlighting the brand's strong customer loyalty in a challenging market.

See More

Microsoft Raises Enterprise Subscription Price by 65%

- Price Increase Strategy: Microsoft has announced that its top-tier Microsoft 365 E7 enterprise plan will see a monthly fee increase to $99, representing a 65% hike from the previous price, aimed at boosting AI revenue to offset the $72 billion spent on infrastructure over the past two quarters.

- Market Potential Exploration: Currently, Microsoft has only 15 million paying Copilot accounts, while there are 450 million Microsoft 365 commercial customers, indicating significant potential for Microsoft to tap into a larger pool of high-paying AI customers who have yet to upgrade.

- Increased Competitive Pressure: With ChatGPT boasting over 50 million paying subscribers, Microsoft faces intense competition and must quickly attract enterprise users to subscribe to its AI services to prevent them from shifting to alternative AI solutions.

- Growth Monitoring Necessity: Although Microsoft's cloud service sales rose by 17% in the second quarter, commercial seats only increased by 6%, prompting investors to closely monitor the acceleration of both sales and paying subscribers to assess the effectiveness of Microsoft's new AI strategy.

See More

Surge in Demand for AI Data Center Construction

- Massive Investment: The four hyperscalers, including Alphabet, Microsoft, Meta, and Amazon, have committed nearly $700 billion in capital expenditures this year to support the construction of AI data centers, reflecting strong confidence in future technological infrastructure.

- Job Creation: Amazon's $12 billion investment in a new AI data center in Louisiana is expected to create 540 full-time jobs directly and generate an additional 1,700 roles for electricians, technicians, and security specialists, significantly boosting the local economy.

- Skills Shortage Intensifies: According to Randstad's analysis, demand for robotic technicians is projected to increase by 107% from 2022 to 2026, while HVAC system engineers will see a 67% rise, indicating that the shortage of skilled labor poses a significant challenge to industry growth.

- Wage Growth Trend: Due to the scarcity of specialized workers, advertised wages for HVAC engineers have risen by 10% to 15% over the past four years, while professionals moving into high-level data center roles often experience a 25% to 30% salary increase, highlighting the urgent demand for technical talent in the sector.

See More

AI Data Center Boom Drives Surge in Skilled Labor Demand

- Significant Wage Growth: According to Kelly Services, specialized professionals transitioning to data center roles see a salary increase of 25% to 30%, reflecting not only the urgent demand for skilled labor but also the industry's increasing emphasis on talent acquisition and retention.

- Massive Investment: The four hyperscalers (Alphabet, Microsoft, Meta, and Amazon) have committed nearly $700 billion in 2023 for data center construction, with Amazon investing $12 billion in a new facility in Louisiana, expected to create 540 full-time jobs, thereby boosting the local economy.

- Labor Shortage Crisis: Randstad's analysis indicates a 107% increase in demand for robotic technicians and a 67% rise for HVAC engineers from 2022 to 2026, highlighting the escalating labor shortage as AI infrastructure demand surges, which may lead to overall wage increases in the sector.

- Emergence of New Collar Jobs: The rapid growth of data centers is fostering a unique environment where traditional blue-collar and white-collar workers will collaborate, creating a

See More

Accenture and Microsoft Collaborate on AI Implementation Strategy

- Forward Deployed Engineering: Accenture and Microsoft have developed a forward deployed engineering (FDE) strategy that connects software engineers directly with customers to customize and integrate AI tools, thereby accelerating enterprise AI implementation.

- Rapid Implementation Capability: This new strategy is expected to reduce the implementation time for enterprise AI initiatives from months to days, which not only enhances client responsiveness but also enables businesses to achieve measurable outcomes in AI transformation more swiftly.

- Combining Industry Expertise: The integration of Microsoft's AI platform with Accenture's industry expertise allows FDE teams to quickly deliver high-quality outcomes for customers, further strengthening both companies' competitive positions in the AI sector.

- Strategic Synergy: Manish Sharma, Accenture's Chief Strategy and Services Officer, emphasizes that the collaboration between strategy and engineering is crucial for enterprise AI success, and this partnership is set to drive greater efficiency and effectiveness in AI transformations.

See More

Gates Foundation's Investment Overview

- Asset Management Scale: Since its inception in 2000, the Gates Foundation has spent over $102 billion on charitable causes, with total trust assets currently at $86 billion, showcasing its significant influence in global philanthropy.

- Investment Concentration: The foundation's portfolio consists of 23 stocks, with 96% of its assets concentrated in its top 10 holdings, indicating a highly concentrated investment strategy, with its largest holding, Berkshire Hathaway, accounting for 28% of the portfolio.

- Berkshire Hathaway Contributions: As of the end of 2025, the foundation owned approximately 19.4 million Class B shares of Berkshire Hathaway, valued at about $9.8 billion, primarily due to Warren Buffett's long-term charitable contributions totaling $43.3 billion in stock over the years.

- Microsoft Holding Background: Microsoft ranks as the foundation's fourth-largest holding at 10.5%, primarily stemming from Bill Gates' donations, reflecting his ongoing support for the foundation while also demonstrating the foundation's flexibility in capital management.

See More

Rocket Lab Shares Surge 10% on New $816M Defense Contract

- Contract Boosts Stock: Rocket Lab (RKLB) shares surged 10.21% after securing an $816 million defense contract with the U.S. Space Development Agency, reflecting investor optimism ahead of upcoming launches dubbed 'Eight Days A Week' and 'Daughter of the Stars'.

- Market Volatility Impact: Despite a 3% pre-market dip due to a newly announced equity offering valued at up to $1 billion, Rocket Lab's stock performance remains 55% ahead of the S&P 500 since August 2025, indicating strong market resilience.

- AI Chip Competition Intensifies: Nvidia has received approval to ship its H200 processors to customers in China, as CEO Jensen Huang announced at the GTC conference, with the export deal cleared by both U.S. and Chinese authorities, further heating up the AI sector competition.

- Lululemon Earnings Impact: Lululemon (LULU) shares fell about 2% following its fourth-quarter earnings report, which showed an 18% year-over-year decline in EPS, although it still surpassed Wall Street expectations, highlighting the brand's strong customer loyalty in a challenging market.

See More