Medical Properties Trust Faces High Risk-Reward Profile

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Feb 19 2026

0mins

Source: Fool

- Attractive Yield but High Risk: Medical Properties Trust offers a 6.6% yield, significantly higher than the S&P 500's 1.2% and the average REIT's 3.8%, yet this high yield reflects the company's history of two dividend cuts, prompting investors to assess risks carefully.

- Dividend Cuts Impact: The company's stock has fallen about 75% over the past five years due to excessive debt leading to tenant payment issues; although the dividend was recently increased, its financial health remains a concern.

- High Debt Levels: While Medical Properties Trust's debt levels have been trending down, they are still high compared to other attractive REITs like Realty Income and W.P. Carey, which yield around 4.9%, raising doubts about its future stability.

- Balancing Risk and Reward: Although Medical Properties Trust may have turned a corner, its dividend history and high leverage warrant caution, leading investors to potentially favor more stable yield stocks like Realty Income and W.P. Carey.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy O?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on O

Wall Street analysts forecast O stock price to fall

11 Analyst Rating

3 Buy

7 Hold

1 Sell

Hold

Current: 64.880

Low

60.00

Averages

62.59

High

67.50

Current: 64.880

Low

60.00

Averages

62.59

High

67.50

About O

Realty Income Corporation is a real estate investment trust. The Company is engaged in acquiring and managing freestanding commercial properties that generate rental revenue under long-term net lease agreements with its commercial clients. It is engaged in a single business activity, which is the leasing of property to clients, generally on a net basis. That business activity spans various geographic boundaries and includes property types and clients engaged in various industries. The Company owns or holds interests in approximately 15,621 properties located in all 50 United States (U.S.) states, the United Kingdom, France, Germany, Ireland, Italy, Portugal, and Spain with clients doing business in 89 industries. Its property types include retail, industrial, gaming and others, such as agriculture and office. Its primary industry concentrations include grocery stores, convenience stores, dollar stores, drug stores, home improvement, restaurants-quick service and others.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Future Outlook for Realty Income Trust

- Strong Market Position: Realty Income boasts a market cap of approximately $60 billion and owns over 15,500 properties, making it the largest net lease REIT in the U.S. and Europe, demonstrating its robust competitiveness and stability in the market.

- Lease Structure Advantage: The net lease structure allows tenants to cover most property-level costs, significantly reducing business risk for Realty Income, ensuring stable cash flow and long-term profitability.

- Capital Market Advantage: Realty Income's size and financial strength enable it to complete acquisitions quickly and efficiently, enhancing its competitiveness in capital markets and further solidifying its market leadership.

- Dividend Growth Potential: Currently offering a 5% dividend yield, Realty Income is expected to achieve 41 annual dividend increases over the next decade, making it a reliable choice for long-term investors seeking stable returns.

See More

Realty Income Announces Dividend Increase

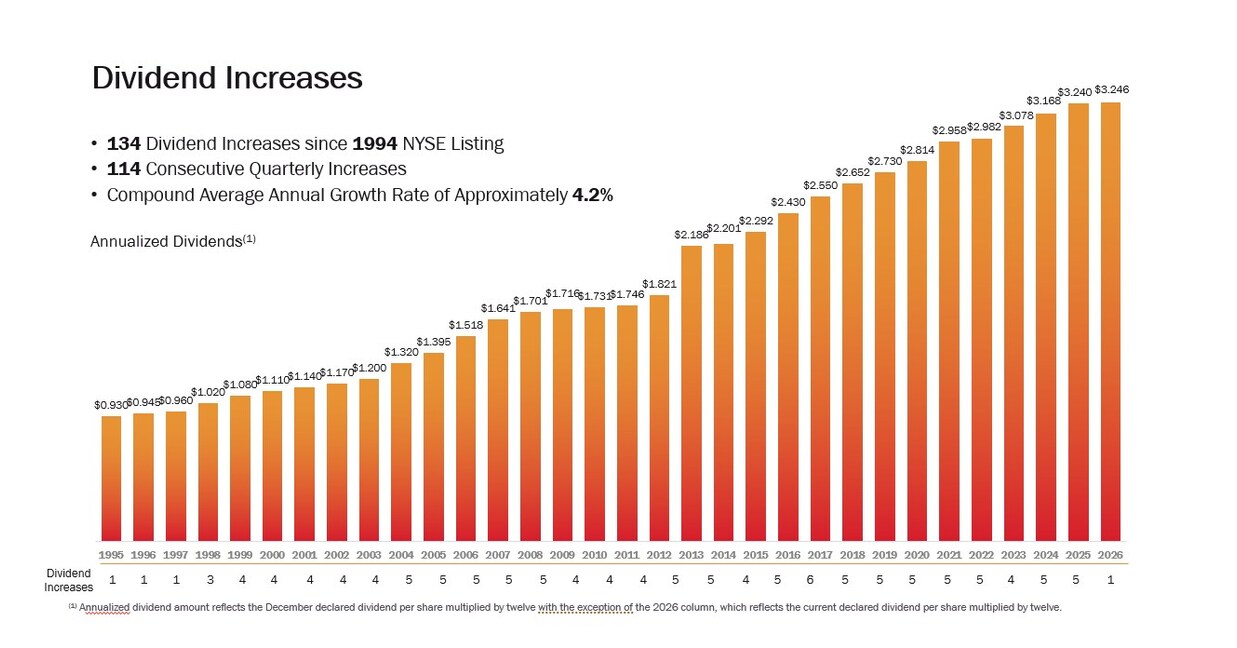

- Dividend Increase: Realty Income raised its monthly cash dividend from $0.2700 to $0.2705 per share, resulting in an annualized dividend of $3.246, which underscores the company's robust cash flow and profitability, likely attracting more investor interest.

- Record of Consistent Dividend Growth: This dividend declaration marks the 134th increase since Realty Income's listing on the NYSE in 1994, reflecting the company's ability to sustain growth over the past 31 years, thereby enhancing its reputation as 'The Monthly Dividend Company®'.

- Strong Asset Portfolio: As of the end of 2025, Realty Income boasts over 15,500 properties across the U.S. and other countries, providing a solid asset base that supports its ability to pay and increase dividends, further solidifying its market position.

- Investor Confidence Boost: CEO Sumit Roy emphasized that the strong, diversified portfolio underpins the steady growth of dividends, which is expected to enhance investor confidence in the company's future performance and promote long-term stock price appreciation.

See More

Realty Income Increases Monthly Dividend to $0.2705 per Share

- Dividend Increase: Realty Income has raised its monthly cash dividend from $0.2700 to $0.2705 per share, marking the 134th increase since its NYSE listing in 1994, which underscores the company's strong cash flow and profitability.

- Annualized Dividend Comparison: The new monthly dividend translates to an annualized amount of $3.246 per share, compared to the previous $3.240, reflecting the company's commitment to returning value to shareholders and enhancing investor confidence.

- Robust Asset Portfolio: As of December 31, 2025, Realty Income boasts over 15,500 properties across all 50 U.S. states and other countries, ensuring diverse and stable income sources, which further solidifies its market position.

- Consistent Dividend Payments: The company has declared 669 consecutive monthly dividends since its inception and is a member of the S&P 500 Dividend Aristocrats, demonstrating long-term stability and reliability in dividend payments, attracting more investors seeking steady income.

See More

Realty Income: A Steady Investment Opportunity in REITs

- High Occupancy Assurance: Since its IPO in 1994, Realty Income has maintained an occupancy rate never below 96%, achieving 98.6% at year-end 2023, and 98.7% and 98.9% in 2024 and 2025 respectively, ensuring stable rental income and shareholder returns even amid tenant store closures.

- Reliable Monthly Dividends: Realty Income is one of the few REITs that pays monthly dividends, having raised its payout 133 times since its IPO, currently offering a forward yield of 5%, with its adjusted funds from operations (AFFO) per share growing 2% in 2023 and expected to reach $4.38-$4.42 by 2026, comfortably covering the $3.24 per share dividend.

- Benefiting from Lower Interest Rates: Realty Income faced challenges during the interest rate hikes of 2022 and 2023, but with the Fed cutting rates six times in 2024 and 2025, investors are rotating back to high-quality REITs, a trend likely to continue with potential changes in Fed leadership.

- Attractive Valuation: Trading at just 15 times this year's AFFO estimate, Realty Income's low valuation, combined with its high yield and stable growth, makes it a compelling stock to buy amidst geopolitical tensions and volatile commodity prices.

See More

Realty Income: A Steady Monthly Dividend Stock

- Stable Dividend Policy: Realty Income has maintained an occupancy rate above 96% since its IPO in 1994, achieving 98.6% at year-end 2023 and projected to reach 98.9% by 2025, providing a solid foundation for its monthly dividend payout of up to 5%.

- Growth Outlook: In 2023, Realty Income's adjusted funds from operations (AFFO) per share grew by 2%, with a forecasted increase of 5% in 2024, reaching $4.28 in 2025, and an expected growth of 2%-3% in 2026, easily covering its dividend of $3.24 per share.

- Attractive Valuation: Realty Income trades at $65 with a price-to-earnings ratio of only 15 times, making it an appealing investment choice amid geopolitical tensions and commodity price volatility, given its stable growth and high yield.

- Market Trend Recovery: Following six interest rate cuts by the Fed in 2024 and 2025, investors are rotating back to high-quality REITs like Realty Income, which could enhance its market appeal and performance in the coming years.

See More

Realty Income Stock Hits Three-Year High, Still a Buy

- Stock Price Surge: Realty Income's stock has recently surged to its highest point in nearly three years, and despite a P/E ratio of 57, which is close to double the S&P 500 average of 30, it continues to attract investor interest.

- Stable Cash Flow: The company owns over 15,500 single-tenant net-leased properties with an occupancy rate of nearly 99%, ensuring steady cash flows, with tenants including major firms like Walmart and FedEx.

- Sustainable Dividends: Realty Income's normalized FFO for 2025 is projected at $4.27 per share, significantly above the annual dividend cost of $3.24, ensuring a sustainable dividend yield of 4.8%.

- Opportunities from Lower Rates: The recent cut in interest rates allows the company to pursue more deals, which not only helps boost stock prices but may also increase dividends, creating a virtuous cycle that attracts more investors.

See More

Future Outlook for Realty Income Trust

- Strong Market Position: Realty Income boasts a market cap of approximately $60 billion and owns over 15,500 properties, making it the largest net lease REIT in the U.S. and Europe, demonstrating its robust competitiveness and stability in the market.

- Lease Structure Advantage: The net lease structure allows tenants to cover most property-level costs, significantly reducing business risk for Realty Income, ensuring stable cash flow and long-term profitability.

- Capital Market Advantage: Realty Income's size and financial strength enable it to complete acquisitions quickly and efficiently, enhancing its competitiveness in capital markets and further solidifying its market leadership.

- Dividend Growth Potential: Currently offering a 5% dividend yield, Realty Income is expected to achieve 41 annual dividend increases over the next decade, making it a reliable choice for long-term investors seeking stable returns.

See More

Realty Income Announces Dividend Increase

- Dividend Increase: Realty Income raised its monthly cash dividend from $0.2700 to $0.2705 per share, resulting in an annualized dividend of $3.246, which underscores the company's robust cash flow and profitability, likely attracting more investor interest.

- Record of Consistent Dividend Growth: This dividend declaration marks the 134th increase since Realty Income's listing on the NYSE in 1994, reflecting the company's ability to sustain growth over the past 31 years, thereby enhancing its reputation as 'The Monthly Dividend Company®'.

- Strong Asset Portfolio: As of the end of 2025, Realty Income boasts over 15,500 properties across the U.S. and other countries, providing a solid asset base that supports its ability to pay and increase dividends, further solidifying its market position.

- Investor Confidence Boost: CEO Sumit Roy emphasized that the strong, diversified portfolio underpins the steady growth of dividends, which is expected to enhance investor confidence in the company's future performance and promote long-term stock price appreciation.

See More

Realty Income Increases Monthly Dividend to $0.2705 per Share

- Dividend Increase: Realty Income has raised its monthly cash dividend from $0.2700 to $0.2705 per share, marking the 134th increase since its NYSE listing in 1994, which underscores the company's strong cash flow and profitability.

- Annualized Dividend Comparison: The new monthly dividend translates to an annualized amount of $3.246 per share, compared to the previous $3.240, reflecting the company's commitment to returning value to shareholders and enhancing investor confidence.

- Robust Asset Portfolio: As of December 31, 2025, Realty Income boasts over 15,500 properties across all 50 U.S. states and other countries, ensuring diverse and stable income sources, which further solidifies its market position.

- Consistent Dividend Payments: The company has declared 669 consecutive monthly dividends since its inception and is a member of the S&P 500 Dividend Aristocrats, demonstrating long-term stability and reliability in dividend payments, attracting more investors seeking steady income.

See More

Realty Income: A Steady Investment Opportunity in REITs

- High Occupancy Assurance: Since its IPO in 1994, Realty Income has maintained an occupancy rate never below 96%, achieving 98.6% at year-end 2023, and 98.7% and 98.9% in 2024 and 2025 respectively, ensuring stable rental income and shareholder returns even amid tenant store closures.

- Reliable Monthly Dividends: Realty Income is one of the few REITs that pays monthly dividends, having raised its payout 133 times since its IPO, currently offering a forward yield of 5%, with its adjusted funds from operations (AFFO) per share growing 2% in 2023 and expected to reach $4.38-$4.42 by 2026, comfortably covering the $3.24 per share dividend.

- Benefiting from Lower Interest Rates: Realty Income faced challenges during the interest rate hikes of 2022 and 2023, but with the Fed cutting rates six times in 2024 and 2025, investors are rotating back to high-quality REITs, a trend likely to continue with potential changes in Fed leadership.

- Attractive Valuation: Trading at just 15 times this year's AFFO estimate, Realty Income's low valuation, combined with its high yield and stable growth, makes it a compelling stock to buy amidst geopolitical tensions and volatile commodity prices.

See More

Realty Income: A Steady Monthly Dividend Stock

- Stable Dividend Policy: Realty Income has maintained an occupancy rate above 96% since its IPO in 1994, achieving 98.6% at year-end 2023 and projected to reach 98.9% by 2025, providing a solid foundation for its monthly dividend payout of up to 5%.

- Growth Outlook: In 2023, Realty Income's adjusted funds from operations (AFFO) per share grew by 2%, with a forecasted increase of 5% in 2024, reaching $4.28 in 2025, and an expected growth of 2%-3% in 2026, easily covering its dividend of $3.24 per share.

- Attractive Valuation: Realty Income trades at $65 with a price-to-earnings ratio of only 15 times, making it an appealing investment choice amid geopolitical tensions and commodity price volatility, given its stable growth and high yield.

- Market Trend Recovery: Following six interest rate cuts by the Fed in 2024 and 2025, investors are rotating back to high-quality REITs like Realty Income, which could enhance its market appeal and performance in the coming years.

See More

Realty Income Stock Hits Three-Year High, Still a Buy

- Stock Price Surge: Realty Income's stock has recently surged to its highest point in nearly three years, and despite a P/E ratio of 57, which is close to double the S&P 500 average of 30, it continues to attract investor interest.

- Stable Cash Flow: The company owns over 15,500 single-tenant net-leased properties with an occupancy rate of nearly 99%, ensuring steady cash flows, with tenants including major firms like Walmart and FedEx.

- Sustainable Dividends: Realty Income's normalized FFO for 2025 is projected at $4.27 per share, significantly above the annual dividend cost of $3.24, ensuring a sustainable dividend yield of 4.8%.

- Opportunities from Lower Rates: The recent cut in interest rates allows the company to pursue more deals, which not only helps boost stock prices but may also increase dividends, creating a virtuous cycle that attracts more investors.

See More