LifeMD Shares Dive Following Q3 Earnings Report: Here's the Reason

Earnings Report Overview: LifeMD Inc. reported a third-quarter adjusted loss of seven cents per share, missing analyst expectations, with revenue of $60.17 million also falling short of the $62.06 million estimate.

Revenue Growth and Challenges: Despite a 13% year-over-year revenue increase, the company faces challenges in the weight management market due to competition from low-cost providers.

Outlook Adjustments: LifeMD revised its fourth-quarter revenue expectations to $45 million to $46 million, significantly lower than the $63.07 million analyst estimate, and reduced its fiscal 2025 revenue outlook to $192 million to $193 million.

Stock Performance: Following the earnings report, LifeMD's stock price dropped by 15.64% to $3.99 in extended trading.

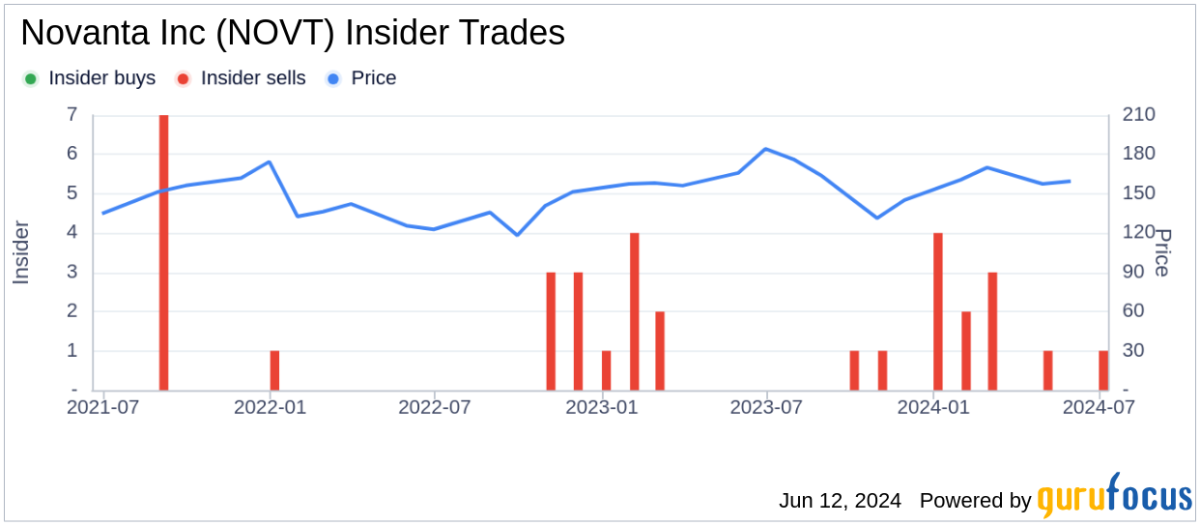

Trade with 70% Backtested Accuracy

Analyst Views on LFMD

About LFMD

About the author

LifeMD Appoints New CFO, Shares Rise 7%

- Executive Change: LifeMD appointed Atul Kavthekar as CFO effective March 16, replacing Marc Benathen, who will remain until March 31, 2026, to ensure a smooth leadership transition, highlighting the company's commitment to stability in its executive team.

- Stock Surge: Following the announcement, LifeMD shares rose nearly 7% in premarket trading, reflecting market confidence in the new CFO and optimistic expectations for the company's future growth trajectory.

- Financial Targets: LifeMD outlined a target of over $250 million in annualized revenue run rate by Q4 2026, driven by record demand for GLP-1 drugs and expanded partnerships, indicating the company's strategy to capitalize on a rapidly growing market.

- Analyst Rating: Cantor Fitzgerald reiterated its Overweight rating on LifeMD after the company reported strong Q4 results, demonstrating analysts' positive outlook on the company's future performance, which may further bolster investor confidence.

LifeMD Appoints New CFO to Support Growth Phase

- Executive Change: LifeMD has appointed Atul Kavthekar as the new CFO effective immediately, a move aimed at supporting the company's next phase of growth, indicating a strong commitment to future development.

- Transition Plan: Current CFO Marc Benathen will remain until March 31, 2026, to ensure a smooth transition, which helps maintain operational stability and continuity within the company.

- Positive Market Reaction: Following the CFO appointment, LifeMD's shares rose, reflecting investor confidence in the company's future, particularly after Cantor Fitzgerald reiterated its Overweight rating.

- Optimistic Financial Outlook: LifeMD's strong performance in Q4 2025 further bolstered market confidence in the company's financial health, laying a solid foundation for future growth.

LifeMD Appoints New CFO and Executives

- Executive Changes: LifeMD has appointed Atul Kavthekar as CFO effective immediately, while current CFO Marc Benathen will depart on March 31 to support the transition, indicating a strategic shift in leadership.

- Market Reaction: In pre-market trading, LFMDP shares rose 7.28% to $4.2697 on Nasdaq, reflecting investor optimism regarding the new leadership team.

- New CFO Background: Kavthekar brings nearly three decades of financial leadership experience across healthcare, pharmacy, and e-commerce, and is expected to leverage his expertise in capital markets and M&A to drive company growth.

- New Marketing Strategy: Chris Pisano has been appointed as CMO, overseeing brand strategy and digital marketing, and with over 25 years of industry experience, aims to enhance LifeMD's market positioning and brand impact.

LifeMD Stock Soars After Strong Q4 Performance and Upgraded Rating

- Stock Surge: LifeMD's stock soared by as much as 23.56% to $3.86 on Tuesday after Cantor Fitzgerald reiterated its Overweight rating, reflecting strong market confidence in the company's growth prospects.

- Performance Beat: The company reported a Q4 loss of $0.04 per share with revenue increasing by 3.9% to $46.87 million, both metrics exceeding analyst expectations, indicating the effectiveness of its business model.

- Cautious Guidance: Although Q1 revenue guidance of $48 million to $49 million fell short of the $49.33 million consensus, the full-year revenue forecast of $220 million to $230 million remains above market expectations.

- Profitability Outlook: LifeMD anticipates returning to profitability in Q2 as customer acquisition costs decline and patient volumes surge, projecting an annualized revenue run rate exceeding $250 million and adjusted EBITDA surpassing $25 million by Q4 2026.

LifeMD Reports Strong Q4 and Full Year 2025 Earnings Growth

- Significant Revenue Growth: LifeMD reported Q4 2025 revenue of $46.9 million, a 4% year-over-year increase, with full-year revenue reaching $194.1 million, reflecting a robust 25% growth that underscores the company's strong market performance and growth potential.

- Margin Fluctuations: While the gross margin for Q4 2025 improved to 87.1%, an increase of 570 basis points year-over-year, the full-year gross margin slightly decreased to 85.7%, indicating challenges in cost management and profitability.

- Cash Flow and Subscriber Growth: By the end of 2025, LifeMD held $36.8 million in cash with no debt, and active subscribers approached 323,000, marking a 16% year-over-year increase, providing a solid financial foundation for future expansion and investments.

- Future Outlook and Challenges: The company anticipates Q1 2026 revenue between $48 million and $49 million, facing high customer acquisition costs and competitive pressures, yet continues to invest in marketing and AI technologies to enhance operational efficiency.

LifeMD, Inc. Reports Strong Q4 2025 Earnings with Positive Outlook

- Significant User Growth: LifeMD ended Q4 2025 with over 322,000 active subscribers, onboarding approximately 1,200 new patients daily and attracting over 120,000 unique daily website visitors, indicating strong momentum in patient acquisition that is expected to drive revenue growth further.

- Strong Financial Performance: The company reported Q4 revenue of $46.9 million, a 4% increase year-over-year, with a gross margin of 87.1% and a net income of $19 million, reflecting significant improvements in cost control and profitability that bolster investor confidence.

- Deepening Strategic Partnerships: The successful launch of oral Wegovy in collaboration with Novo Nordisk positions LifeMD as one of the few virtual care providers fully integrated with major pharmaceutical companies, which is expected to further expand market share and enhance brand influence.

- Optimistic Future Outlook: Management anticipates Q1 2026 revenue in the range of $48 million to $49 million, with a full-year revenue target of $220 million to $230 million, demonstrating confidence in future growth while planning to return to adjusted EBITDA profitability in Q2.

LifeMD Appoints New CFO, Shares Rise 7%

- Executive Change: LifeMD appointed Atul Kavthekar as CFO effective March 16, replacing Marc Benathen, who will remain until March 31, 2026, to ensure a smooth leadership transition, highlighting the company's commitment to stability in its executive team.

- Stock Surge: Following the announcement, LifeMD shares rose nearly 7% in premarket trading, reflecting market confidence in the new CFO and optimistic expectations for the company's future growth trajectory.

- Financial Targets: LifeMD outlined a target of over $250 million in annualized revenue run rate by Q4 2026, driven by record demand for GLP-1 drugs and expanded partnerships, indicating the company's strategy to capitalize on a rapidly growing market.

- Analyst Rating: Cantor Fitzgerald reiterated its Overweight rating on LifeMD after the company reported strong Q4 results, demonstrating analysts' positive outlook on the company's future performance, which may further bolster investor confidence.

LifeMD Appoints New CFO to Support Growth Phase

- Executive Change: LifeMD has appointed Atul Kavthekar as the new CFO effective immediately, a move aimed at supporting the company's next phase of growth, indicating a strong commitment to future development.

- Transition Plan: Current CFO Marc Benathen will remain until March 31, 2026, to ensure a smooth transition, which helps maintain operational stability and continuity within the company.

- Positive Market Reaction: Following the CFO appointment, LifeMD's shares rose, reflecting investor confidence in the company's future, particularly after Cantor Fitzgerald reiterated its Overweight rating.

- Optimistic Financial Outlook: LifeMD's strong performance in Q4 2025 further bolstered market confidence in the company's financial health, laying a solid foundation for future growth.

LifeMD Appoints New CFO and Executives

- Executive Changes: LifeMD has appointed Atul Kavthekar as CFO effective immediately, while current CFO Marc Benathen will depart on March 31 to support the transition, indicating a strategic shift in leadership.

- Market Reaction: In pre-market trading, LFMDP shares rose 7.28% to $4.2697 on Nasdaq, reflecting investor optimism regarding the new leadership team.

- New CFO Background: Kavthekar brings nearly three decades of financial leadership experience across healthcare, pharmacy, and e-commerce, and is expected to leverage his expertise in capital markets and M&A to drive company growth.

- New Marketing Strategy: Chris Pisano has been appointed as CMO, overseeing brand strategy and digital marketing, and with over 25 years of industry experience, aims to enhance LifeMD's market positioning and brand impact.

LifeMD Stock Soars After Strong Q4 Performance and Upgraded Rating

- Stock Surge: LifeMD's stock soared by as much as 23.56% to $3.86 on Tuesday after Cantor Fitzgerald reiterated its Overweight rating, reflecting strong market confidence in the company's growth prospects.

- Performance Beat: The company reported a Q4 loss of $0.04 per share with revenue increasing by 3.9% to $46.87 million, both metrics exceeding analyst expectations, indicating the effectiveness of its business model.

- Cautious Guidance: Although Q1 revenue guidance of $48 million to $49 million fell short of the $49.33 million consensus, the full-year revenue forecast of $220 million to $230 million remains above market expectations.

- Profitability Outlook: LifeMD anticipates returning to profitability in Q2 as customer acquisition costs decline and patient volumes surge, projecting an annualized revenue run rate exceeding $250 million and adjusted EBITDA surpassing $25 million by Q4 2026.

LifeMD Reports Strong Q4 and Full Year 2025 Earnings Growth

- Significant Revenue Growth: LifeMD reported Q4 2025 revenue of $46.9 million, a 4% year-over-year increase, with full-year revenue reaching $194.1 million, reflecting a robust 25% growth that underscores the company's strong market performance and growth potential.

- Margin Fluctuations: While the gross margin for Q4 2025 improved to 87.1%, an increase of 570 basis points year-over-year, the full-year gross margin slightly decreased to 85.7%, indicating challenges in cost management and profitability.

- Cash Flow and Subscriber Growth: By the end of 2025, LifeMD held $36.8 million in cash with no debt, and active subscribers approached 323,000, marking a 16% year-over-year increase, providing a solid financial foundation for future expansion and investments.

- Future Outlook and Challenges: The company anticipates Q1 2026 revenue between $48 million and $49 million, facing high customer acquisition costs and competitive pressures, yet continues to invest in marketing and AI technologies to enhance operational efficiency.

LifeMD, Inc. Reports Strong Q4 2025 Earnings with Positive Outlook

- Significant User Growth: LifeMD ended Q4 2025 with over 322,000 active subscribers, onboarding approximately 1,200 new patients daily and attracting over 120,000 unique daily website visitors, indicating strong momentum in patient acquisition that is expected to drive revenue growth further.

- Strong Financial Performance: The company reported Q4 revenue of $46.9 million, a 4% increase year-over-year, with a gross margin of 87.1% and a net income of $19 million, reflecting significant improvements in cost control and profitability that bolster investor confidence.

- Deepening Strategic Partnerships: The successful launch of oral Wegovy in collaboration with Novo Nordisk positions LifeMD as one of the few virtual care providers fully integrated with major pharmaceutical companies, which is expected to further expand market share and enhance brand influence.

- Optimistic Future Outlook: Management anticipates Q1 2026 revenue in the range of $48 million to $49 million, with a full-year revenue target of $220 million to $230 million, demonstrating confidence in future growth while planning to return to adjusted EBITDA profitability in Q2.