Investment Insights: Analysis of Chevron and Vertiv Prospects

Written by Emily J. Thompson, Senior Investment Analyst

Updated: May 13 2026

0mins

Source: CNBC

- Chevron Investment Advice: With oil prices returning to current levels, Chevron's stock previously saw significant increases, currently offering a 3.8% dividend yield and strong cash flow, indicating its stability and attractiveness in the market.

- Vertiv Order Outlook: Vertiv is experiencing strong order performance, with recommendations for investors to build positions gradually; despite potential short-term price fluctuations, its long-term growth potential is widely regarded, reflecting market confidence in its product demand.

- Sterling Infrastructure Risk Warning: Following a 52% increase in stock price, analysts advise against further investment in Sterling Infrastructure at current levels, emphasizing the importance of cautious investing in a high-volatility market.

- GoodRx Market Performance: GoodRx's stock performance remains relatively stable, with analysts noting limited downside risk, suggesting investors should monitor its future market performance and potential growth opportunities.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy GDRX?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on GDRX

Wall Street analysts forecast GDRX stock price to rise

10 Analyst Rating

4 Buy

4 Hold

2 Sell

Hold

Current: 2.610

Low

2.60

Averages

4.46

High

7.00

Current: 2.610

Low

2.60

Averages

4.46

High

7.00

About GDRX

GoodRx Holdings, Inc. is a platform for medication savings in the United States, used by consumers and healthcare professionals. The Company connects consumers, healthcare professionals, payers, pharmacy benefit managers (PBMs), pharma manufacturers, and retail pharmacies to make saving on medications easier. The Company's offerings include prescription marketplace and pharma manufacturer solutions. Its prescription marketplace consists of its prescription transactions offering and its supplemental subscription and telehealth offerings. Through its GoodRx Care platform, the Company offers consumers access to telehealth visits on a cash-pay basis outside of insurance. The Company partners with pharma manufacturers to advertise and integrate their affordable solutions into its platform. These solutions, provided by pharma manufacturers, include co-pay cards, patient assistance programs, care portals, and other savings options to ensure consumers can access their medications.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Biodesix Shares Surge 10.5% on Price Target Upgrade

- Stock Surge: Biodesix shares rose 10.5% to $16.81 in the last trading session, with trading volume significantly above average, indicating strong investor optimism.

- Price Target Upgrade: Canaccord Genuity raised Biodesix's price target from $22.00 to $27.00 while maintaining a 'Buy' rating, further fueling the stock's upward momentum.

- Financial Expectations: Biodesix is expected to report a quarterly loss of $0.85 per share, reflecting a year-over-year increase of 46.9%, while revenues are projected at $26.1 million, up 30.4%, showcasing robust growth in revenue.

- Earnings Estimate Revision: Over the past 30 days, the consensus EPS estimate for Biodesix has been revised 4% higher, and such positive revisions typically correlate with stock price appreciation, indicating market confidence in its future performance.

See More

GoodRx Launches Monthly Subscription Plan for Affordable Medications

- Subscription Plan Launch: GoodRx has introduced a monthly subscription plan called GoodRx Companion, priced at $14.99, which provides customers access to low-cost and free generic drugs, significantly reducing medication expenses and enhancing accessibility for users.

- Telehealth Services: The plan includes $19 telehealth visits for common conditions such as flu, UTIs, and skin care, further expanding customer options for medical services and addressing the growing demand for online healthcare solutions.

- Diverse Offerings: In addition to medications, GoodRx Companion offers discounts on dental, vision, and lab imaging services, reflecting the company's diversification strategy in the healthcare sector aimed at improving overall customer health management experiences.

- Upgraded Financial Outlook: GoodRx has raised its 2026 revenue outlook to between $765 million and $785 million, with adjusted EBITDA projected to be at least $235 million, indicating strong growth potential in the Pharma Direct segment and boosting investor confidence.

See More

GoodRx Launches $14.99 Membership to Lower Healthcare Costs

- Membership Launch: GoodRx has introduced the $14.99 GoodRx Companion membership service, designed to lower everyday healthcare costs by integrating free and low-cost generic medications, affordable online care visits, and discounts on additional healthcare services, thereby enhancing its competitive position in the healthcare market.

- Medication Savings Advantage: The membership offers over 200 common generic medications for free and hundreds more for under $10, available at nearly every pharmacy nationwide, significantly reducing drug expenses for patients, particularly those managing chronic conditions or taking multiple medications.

- Online Care Services: GoodRx Companion also provides $19 telehealth visits for common conditions such as UTIs, skin care, and flu, further improving consumer access and convenience in healthcare services, addressing the growing demand for online medical care.

- Strategic Expansion: This launch not only enriches GoodRx's subscription product line but also creates a recurring revenue stream, strengthening long-term relationships with consumers and aligning with market demands for more flexible healthcare solutions, thereby solidifying GoodRx's leadership in the healthcare services sector.

See More

Trump Administration Expands TrumpRx with Generic Medications

- Platform Expansion: The Trump administration announced the addition of over 600 generic medications to the TrumpRx website, aiming to lower prescription drug costs in the U.S. by providing transparent pricing and enhancing consumer choice.

- New Tools Launched: The platform now features tools that connect patients with the lowest-priced pharmacies in their area and offers home delivery options for prescriptions, improving user experience and facilitating easier access to medications.

- Partnerships Established: The administration is partnering with industry players like Mark Cuban's Cost Plus Drug Company, Amazon Pharmacy, and GoodRx to promote direct-to-consumer drug sales, ensuring price transparency for consumers.

- User Engagement and Savings: Since its launch, TrumpRx has recorded over 10 million visits and saved Americans more than $400 million, although it remains unclear if all patients will benefit from this platform compared to traditional purchasing methods.

See More

Investment Insights: Analysis of Chevron and Vertiv Prospects

- Chevron Investment Advice: With oil prices returning to current levels, Chevron's stock previously saw significant increases, currently offering a 3.8% dividend yield and strong cash flow, indicating its stability and attractiveness in the market.

- Vertiv Order Outlook: Vertiv is experiencing strong order performance, with recommendations for investors to build positions gradually; despite potential short-term price fluctuations, its long-term growth potential is widely regarded, reflecting market confidence in its product demand.

- Sterling Infrastructure Risk Warning: Following a 52% increase in stock price, analysts advise against further investment in Sterling Infrastructure at current levels, emphasizing the importance of cautious investing in a high-volatility market.

- GoodRx Market Performance: GoodRx's stock performance remains relatively stable, with analysts noting limited downside risk, suggesting investors should monitor its future market performance and potential growth opportunities.

See More

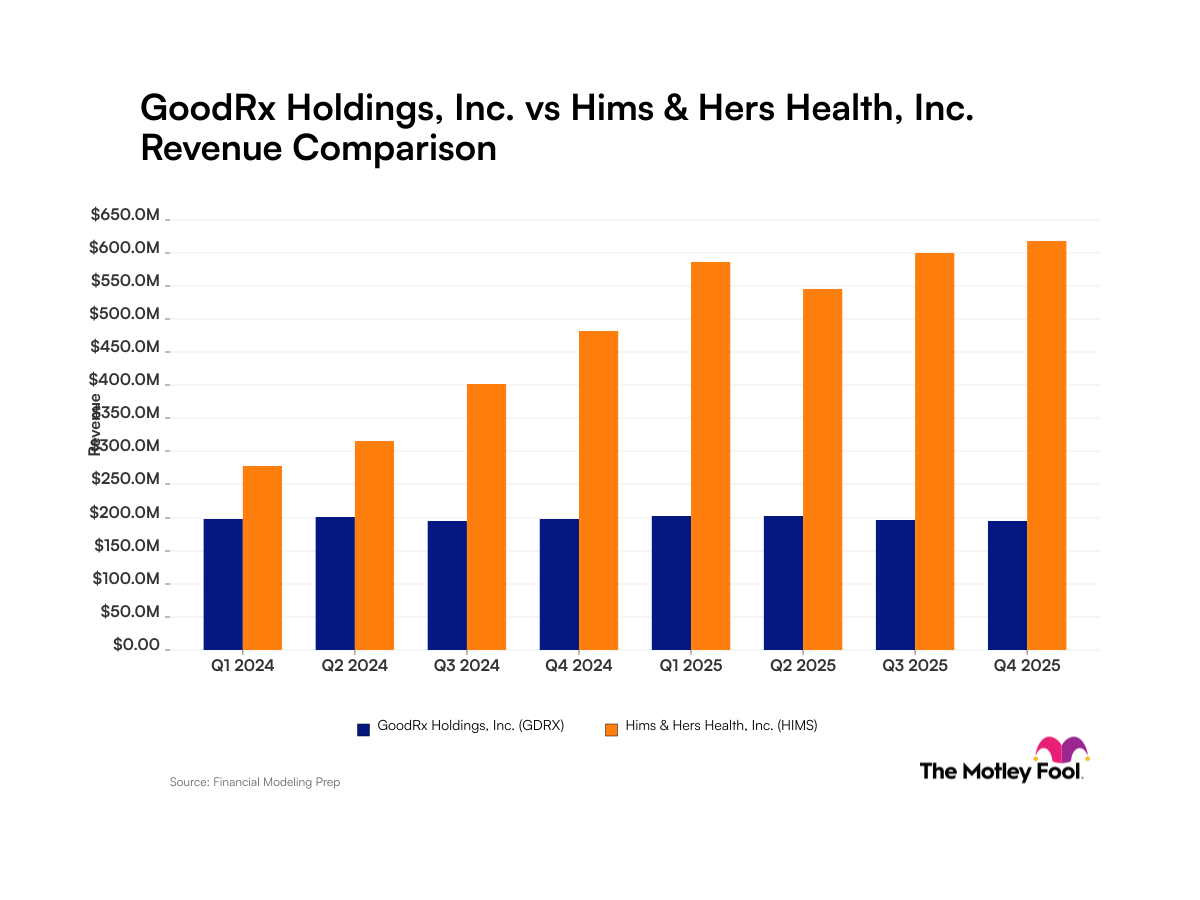

GoodRx and Hims & Hers Financial Report Analysis

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business surged 82% to $52 million, accounting for 27% of total revenue, indicating potential growth amidst a competitive landscape.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing strong demand in the telehealth sector.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, providing robust market support for Hims & Hers' alternative platform, further driving revenue growth.

- Investor Reaction: GoodRx's stock rose over 10% following its Q1 earnings report, reflecting investor optimism regarding its Pharma Direct business, despite overall revenue stagnation, indicating sustained confidence in future growth prospects.

See More

Biodesix Shares Surge 10.5% on Price Target Upgrade

- Stock Surge: Biodesix shares rose 10.5% to $16.81 in the last trading session, with trading volume significantly above average, indicating strong investor optimism.

- Price Target Upgrade: Canaccord Genuity raised Biodesix's price target from $22.00 to $27.00 while maintaining a 'Buy' rating, further fueling the stock's upward momentum.

- Financial Expectations: Biodesix is expected to report a quarterly loss of $0.85 per share, reflecting a year-over-year increase of 46.9%, while revenues are projected at $26.1 million, up 30.4%, showcasing robust growth in revenue.

- Earnings Estimate Revision: Over the past 30 days, the consensus EPS estimate for Biodesix has been revised 4% higher, and such positive revisions typically correlate with stock price appreciation, indicating market confidence in its future performance.

See More

GoodRx Launches Monthly Subscription Plan for Affordable Medications

- Subscription Plan Launch: GoodRx has introduced a monthly subscription plan called GoodRx Companion, priced at $14.99, which provides customers access to low-cost and free generic drugs, significantly reducing medication expenses and enhancing accessibility for users.

- Telehealth Services: The plan includes $19 telehealth visits for common conditions such as flu, UTIs, and skin care, further expanding customer options for medical services and addressing the growing demand for online healthcare solutions.

- Diverse Offerings: In addition to medications, GoodRx Companion offers discounts on dental, vision, and lab imaging services, reflecting the company's diversification strategy in the healthcare sector aimed at improving overall customer health management experiences.

- Upgraded Financial Outlook: GoodRx has raised its 2026 revenue outlook to between $765 million and $785 million, with adjusted EBITDA projected to be at least $235 million, indicating strong growth potential in the Pharma Direct segment and boosting investor confidence.

See More

GoodRx Launches $14.99 Membership to Lower Healthcare Costs

- Membership Launch: GoodRx has introduced the $14.99 GoodRx Companion membership service, designed to lower everyday healthcare costs by integrating free and low-cost generic medications, affordable online care visits, and discounts on additional healthcare services, thereby enhancing its competitive position in the healthcare market.

- Medication Savings Advantage: The membership offers over 200 common generic medications for free and hundreds more for under $10, available at nearly every pharmacy nationwide, significantly reducing drug expenses for patients, particularly those managing chronic conditions or taking multiple medications.

- Online Care Services: GoodRx Companion also provides $19 telehealth visits for common conditions such as UTIs, skin care, and flu, further improving consumer access and convenience in healthcare services, addressing the growing demand for online medical care.

- Strategic Expansion: This launch not only enriches GoodRx's subscription product line but also creates a recurring revenue stream, strengthening long-term relationships with consumers and aligning with market demands for more flexible healthcare solutions, thereby solidifying GoodRx's leadership in the healthcare services sector.

See More

Trump Administration Expands TrumpRx with Generic Medications

- Platform Expansion: The Trump administration announced the addition of over 600 generic medications to the TrumpRx website, aiming to lower prescription drug costs in the U.S. by providing transparent pricing and enhancing consumer choice.

- New Tools Launched: The platform now features tools that connect patients with the lowest-priced pharmacies in their area and offers home delivery options for prescriptions, improving user experience and facilitating easier access to medications.

- Partnerships Established: The administration is partnering with industry players like Mark Cuban's Cost Plus Drug Company, Amazon Pharmacy, and GoodRx to promote direct-to-consumer drug sales, ensuring price transparency for consumers.

- User Engagement and Savings: Since its launch, TrumpRx has recorded over 10 million visits and saved Americans more than $400 million, although it remains unclear if all patients will benefit from this platform compared to traditional purchasing methods.

See More

Investment Insights: Analysis of Chevron and Vertiv Prospects

- Chevron Investment Advice: With oil prices returning to current levels, Chevron's stock previously saw significant increases, currently offering a 3.8% dividend yield and strong cash flow, indicating its stability and attractiveness in the market.

- Vertiv Order Outlook: Vertiv is experiencing strong order performance, with recommendations for investors to build positions gradually; despite potential short-term price fluctuations, its long-term growth potential is widely regarded, reflecting market confidence in its product demand.

- Sterling Infrastructure Risk Warning: Following a 52% increase in stock price, analysts advise against further investment in Sterling Infrastructure at current levels, emphasizing the importance of cautious investing in a high-volatility market.

- GoodRx Market Performance: GoodRx's stock performance remains relatively stable, with analysts noting limited downside risk, suggesting investors should monitor its future market performance and potential growth opportunities.

See More

GoodRx and Hims & Hers Financial Report Analysis

- GoodRx Revenue Trends: GoodRx reported a 4.4% year-over-year decline in Q1 2026 sales to $194 million, yet its Pharma Direct business surged 82% to $52 million, accounting for 27% of total revenue, indicating potential growth amidst a competitive landscape.

- Hims & Hers Growth Performance: Hims & Hers achieved a remarkable 59% year-over-year revenue increase in Q4 2025, reaching $617.8 million, alongside a 13% growth in subscribers, showcasing strong demand in the telehealth sector.

- Market Environment Impact: With the average annual cost of family health plans hitting $27,000 in 2026, fewer Americans have access to primary care, providing robust market support for Hims & Hers' alternative platform, further driving revenue growth.

- Investor Reaction: GoodRx's stock rose over 10% following its Q1 earnings report, reflecting investor optimism regarding its Pharma Direct business, despite overall revenue stagnation, indicating sustained confidence in future growth prospects.

See More