Deal Dispatch: Trump Settlement Clears Way For Paramount Merger, Euronext Eyes Greece, KKR Strikes Twice

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jul 04 2025

0mins

Source: Benzinga

Mergers and Acquisitions Activity: Abry Partners is seeking a buyer for Sermo, with bids expected between $600 million and $800 million. Verint Systems is also exploring a sale, while KKR has agreed to acquire Spectris for £4.1 billion, indicating ongoing M&A activity despite a decline in deal volumes globally.

Bankruptcy and Financial Settlements: Del Monte Foods has filed for Chapter 11 bankruptcy to facilitate a turnaround, securing $912.5 million in financing during the process. Additionally, Paramount Global settled a lawsuit with Donald Trump for $16 million, which may aid its merger with Skydance Media.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy HPE?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on HPE

Wall Street analysts forecast HPE stock price to fall

16 Analyst Rating

8 Buy

8 Hold

0 Sell

Moderate Buy

Current: 56.150

Low

21.00

Averages

27.13

High

31.00

Current: 56.150

Low

21.00

Averages

27.13

High

31.00

About HPE

Hewlett Packard Enterprise Company is a global technology company focused on developing intelligent solutions that allow customers to capture, analyze and act upon data seamlessly from edge to cloud. Its customers range from small-and-medium-sized businesses to large global enterprises and governmental entities. Its segments include Server, Hybrid Cloud, Networking, Financial Services, and Corporate Investments and Other. Its Server segment offerings consist of general-purpose servers for multi-workload computing, workload-optimized servers, and integrated systems. Its Hybrid Cloud segment offers a range of cloud-native and hybrid solutions across storage, private cloud and the infrastructure software-as-a-service space. The Networking segment develops and sells high-performance networking and security products and services. Its Financial Services segment provides flexible investment solutions, such as leasing, financing, IT consumption, utility programs, and asset management services.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Hewlett Packard Enterprise Shares Surge 25% on Strong Q2 Results and Outlook

- Strong Earnings Beat: Hewlett Packard Enterprise (HPE) reported fiscal Q2 results that exceeded expectations, leading to a premarket share surge of approximately 25%, indicating analysts' optimism about future growth prospects.

- Price Target Increase: Morgan Stanley raised HPE's price target from $33 to $71, highlighting that inelastic server demand and market share gains are expected to drive future profitability, with FY27 EPS projected at $4.16.

- Robust Market Demand: Analysts noted that despite rising memory costs, HPE is able to protect margins due to customers' willingness to absorb higher DRAM/NAND prices, with double-digit year-over-year growth in server orders reflecting the strategic importance of servers for enterprises.

- Positive Future Outlook: Bank of America maintained a Buy rating and increased the price target to $80, citing significant topline growth potential for FY27, with management indicating no signs of order pull-forwards, cancellations, or double ordering, suggesting future growth will be driven by networking and AI advancements.

See More

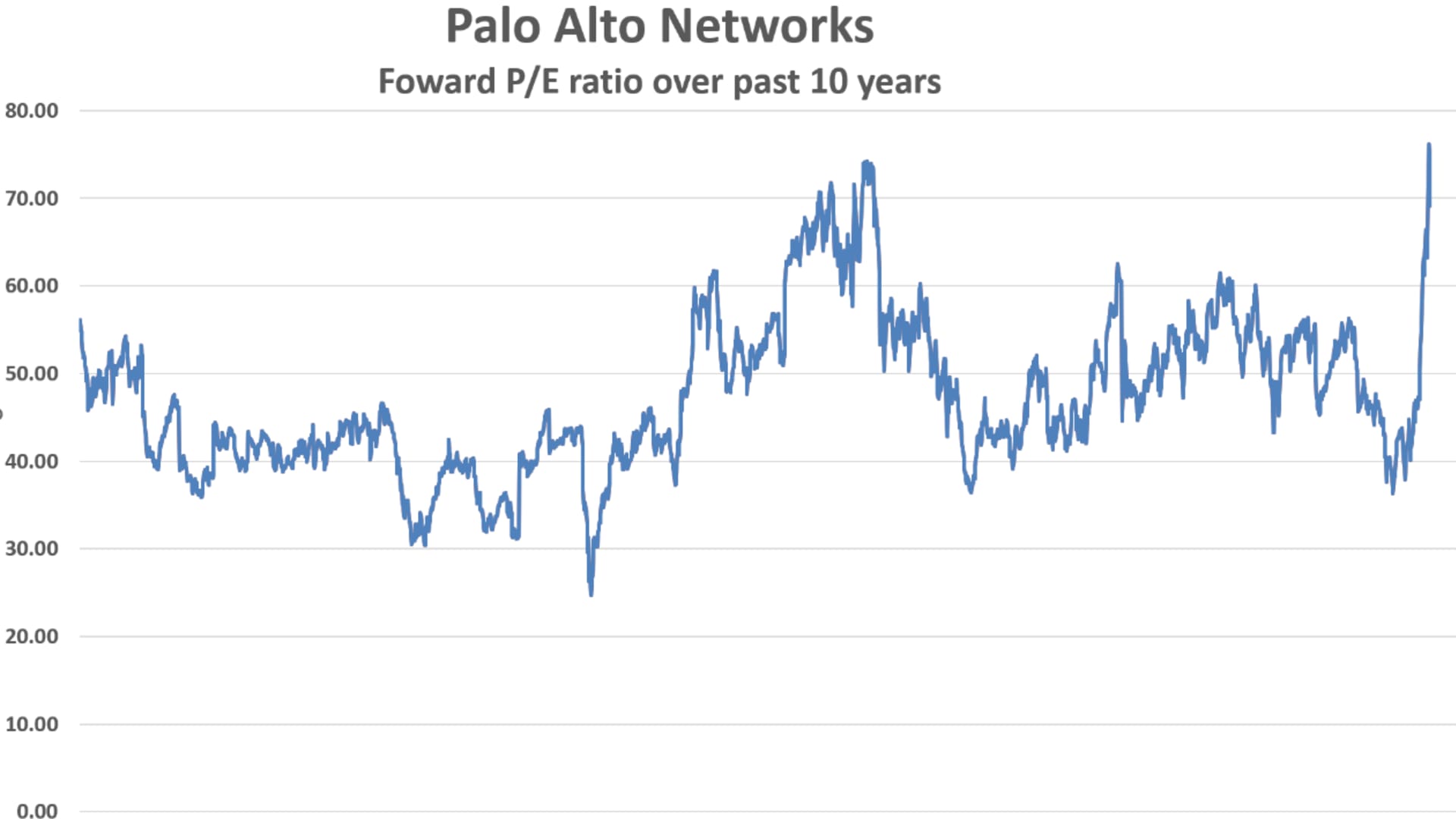

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More

U.S. Stocks Hit Record Highs, HPE and Marvell Surge

- Market Records: The S&P 500 index closed at an all-time high for the sixth consecutive day, surpassing 7,600 for the first time, indicating a robust market recovery and increased investor confidence, which may attract more capital inflows into equities.

- HPE Surge: Hewlett Packard Enterprise shares soared 19%, marking its best single-day performance ever, as CEO Antonio Neri stated the company has the “best portfolio we’ve ever had,” enhancing its competitive edge and driving future growth.

- Marvell's Major Gain: Marvell's stock jumped 32%, also achieving its largest one-day gain in history, after Nvidia's CEO Jensen Huang suggested it could be the “next trillion-dollar company,” providing investors with strong growth expectations.

- CME and Cboe Under Pressure: Shares of CME Group and Cboe Global Markets are on track for their worst week since 2020 following the regulatory approval of bitcoin futures, reflecting market concerns and selling pressure on cryptocurrency-related stocks.

See More

U.S. Stocks Hit Record Highs, Macy's Sales Surge

- Market Performance: The S&P 500 index achieved an all-time closing high for the sixth consecutive day, surpassing 7,600 points for the first time, reflecting strong market recovery and heightened investor confidence, particularly driven by technology stocks.

- Macy's Sales Surge: Macy's reported its strongest first-quarter comparable sales performance in four years, with the CEO stating that better-than-expected sales and profitability led to an upward revision of the full-year forecast, indicating early success in its turnaround strategy.

- Hewlett Packard Enterprise Soars: Hewlett Packard Enterprise shares surged 19%, marking its best single-day gain ever, as the CEO claimed the company has the

See More

Broadcom Stock Hits Record Highs Amid Surge in AI Demand

- Strong Stock Performance: Broadcom's stock surged 4.7% on Tuesday to a record high of $481.57, reflecting strong investor confidence in its future performance, particularly against the backdrop of soaring AI demand.

- Significant AI Revenue Growth: The company projects semiconductor revenue of $14.8 billion for Q2, representing a 76% year-over-year increase, with AI revenue expected to soar 140% to $10.7 billion, highlighting its critical role in AI data center development.

- Robust Customer Demand: Broadcom's long-term agreement with Google extends through 2031, ensuring continued production of custom processors, while its expanding partnership with Meta indicates strong market demand for its custom silicon.

- Optimistic Market Outlook: Analysts are generally bullish on Broadcom's future, forecasting that its AI backlog will exceed $150 billion by 2027, driving further market share growth and bolstering investor confidence.

See More

Hewlett Packard Enterprise Shares Surge 25% on Strong Q2 Results and Outlook

- Strong Earnings Beat: Hewlett Packard Enterprise (HPE) reported fiscal Q2 results that exceeded expectations, leading to a premarket share surge of approximately 25%, indicating analysts' optimism about future growth prospects.

- Price Target Increase: Morgan Stanley raised HPE's price target from $33 to $71, highlighting that inelastic server demand and market share gains are expected to drive future profitability, with FY27 EPS projected at $4.16.

- Robust Market Demand: Analysts noted that despite rising memory costs, HPE is able to protect margins due to customers' willingness to absorb higher DRAM/NAND prices, with double-digit year-over-year growth in server orders reflecting the strategic importance of servers for enterprises.

- Positive Future Outlook: Bank of America maintained a Buy rating and increased the price target to $80, citing significant topline growth potential for FY27, with management indicating no signs of order pull-forwards, cancellations, or double ordering, suggesting future growth will be driven by networking and AI advancements.

See More

Palo Alto Networks Shares Drop 4% Despite Strong Earnings

- Earnings Beat: Palo Alto Networks shares fell over 4% despite exceeding quarterly expectations, indicating market concerns about the company's long-term outlook despite strong financial results.

- Hardware Growth Outlook: The company raised its hardware growth forecast for the coming quarters, particularly for firewall installations in data centers and enterprise campuses, but management's guidance for fiscal 2030 subscription revenue did not see a significant increase, potentially disappointing investors.

- Market Reaction Analysis: The stock surged approximately 86% over the past two months, yet CEO Nikesh Arora cautioned during the earnings call against expecting substantial earnings growth in the short term, which may have triggered sell-offs from short-term traders.

- Valuation Context: With a price-to-earnings ratio nearing 75, the stock is at its highest valuation in a decade, and while future growth is anticipated, the high valuation may lead investors to adopt a cautious stance regarding sustained price increases.

See More

Market Dynamics and Company Performance Analysis

- Market Volatility Analysis: Following the S&P 500's record high, the market is slightly fluctuating due to uncertainties surrounding Iran and tariffs, indicating investor sensitivity to geopolitical risks that may affect short-term investment decisions.

- Cybersecurity Outlook: Palo Alto Networks experienced stock volatility post-earnings, as the CEO highlighted cybersecurity risks posed by artificial intelligence, yet market confidence in its future performance remains shaky, reflecting investor caution towards tech stocks.

- Beauty Industry Growth: Ulta Beauty reported a 5.3% same-store sales growth in Q1, exceeding expectations and indicating consumer demand for value, although the stock has declined from its highs, suggesting market concerns about future growth.

- Telecom Industry Challenges: Oppenheimer downgraded AT&T to hold due to potential threats to long-term broadband subscriber growth from satellite internet competition, reflecting market worries about traditional telecom businesses and hinting at the impact of emerging technologies on the sector.

See More

U.S. Stocks Hit Record Highs, HPE and Marvell Surge

- Market Records: The S&P 500 index closed at an all-time high for the sixth consecutive day, surpassing 7,600 for the first time, indicating a robust market recovery and increased investor confidence, which may attract more capital inflows into equities.

- HPE Surge: Hewlett Packard Enterprise shares soared 19%, marking its best single-day performance ever, as CEO Antonio Neri stated the company has the “best portfolio we’ve ever had,” enhancing its competitive edge and driving future growth.

- Marvell's Major Gain: Marvell's stock jumped 32%, also achieving its largest one-day gain in history, after Nvidia's CEO Jensen Huang suggested it could be the “next trillion-dollar company,” providing investors with strong growth expectations.

- CME and Cboe Under Pressure: Shares of CME Group and Cboe Global Markets are on track for their worst week since 2020 following the regulatory approval of bitcoin futures, reflecting market concerns and selling pressure on cryptocurrency-related stocks.

See More

U.S. Stocks Hit Record Highs, Macy's Sales Surge

- Market Performance: The S&P 500 index achieved an all-time closing high for the sixth consecutive day, surpassing 7,600 points for the first time, reflecting strong market recovery and heightened investor confidence, particularly driven by technology stocks.

- Macy's Sales Surge: Macy's reported its strongest first-quarter comparable sales performance in four years, with the CEO stating that better-than-expected sales and profitability led to an upward revision of the full-year forecast, indicating early success in its turnaround strategy.

- Hewlett Packard Enterprise Soars: Hewlett Packard Enterprise shares surged 19%, marking its best single-day gain ever, as the CEO claimed the company has the

See More

Broadcom Stock Hits Record Highs Amid Surge in AI Demand

- Strong Stock Performance: Broadcom's stock surged 4.7% on Tuesday to a record high of $481.57, reflecting strong investor confidence in its future performance, particularly against the backdrop of soaring AI demand.

- Significant AI Revenue Growth: The company projects semiconductor revenue of $14.8 billion for Q2, representing a 76% year-over-year increase, with AI revenue expected to soar 140% to $10.7 billion, highlighting its critical role in AI data center development.

- Robust Customer Demand: Broadcom's long-term agreement with Google extends through 2031, ensuring continued production of custom processors, while its expanding partnership with Meta indicates strong market demand for its custom silicon.

- Optimistic Market Outlook: Analysts are generally bullish on Broadcom's future, forecasting that its AI backlog will exceed $150 billion by 2027, driving further market share growth and bolstering investor confidence.

See More