Carnival Captures 42% Market Share with $2.6B Free Cash Flow

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Jan 08 2026

0mins

Source: NASDAQ.COM

- Market Leadership: Carnival commands a 42% market share in the cruise industry, although it captures only 36% of industry revenue, its mainstream brand appeals to a broad consumer base, ensuring a competitive edge in the budget-friendly travel market.

- Financial Recovery: Following the pandemic, Carnival generated $2.6 billion in free cash flow in fiscal 2025, indicating a strong recovery trajectory, while reducing its debt by approximately $800 million, reflecting improved financial management.

- Operational Efficiency: With an occupancy rate of 105%, exceeding the industry standard of 100%, Carnival demonstrates exceptional performance in recovering market demand and is expanding its fleet to meet future growth needs.

- Valuation Advantage: Carnival's price-to-earnings ratio stands at 16, lower than competitors Royal Caribbean and Norwegian Cruise Line, suggesting that its stock is attractive in the current market environment, potentially drawing more investor interest.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy CCL?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on CCL

Wall Street analysts forecast CCL stock price to rise

18 Analyst Rating

14 Buy

4 Hold

0 Sell

Strong Buy

Current: 26.580

Low

33.00

Averages

37.41

High

45.00

Current: 26.580

Low

33.00

Averages

37.41

High

45.00

About CCL

Carnival Corporation is a global cruise and leisure travel company. The Company has a portfolio of cruise lines, including AIDA Cruises, Carnival Cruise Line, Costa Cruises, Cunard, Holland America Line, P&O Cruises (Australia), P&O Cruises (UK), Princess Cruises, and Seabourn. The Company's segment includes NAA cruise operations, Europe cruise operations (Europe), Cruise Support and Tour and Other. Its Cruise Support segment includes its portfolio of port destinations and exclusive islands as well as other services, all of which are operated for the benefit of its cruise brands. In addition to its cruise operations, it owns Holland America Princess Alaska Tours, a tour company in Alaska and the Canadian Yukon, which complements its Alaska cruise operations. Its Tour and Other segment represents the hotel and transportation operations of Holland America Princess Alaska Tours and other operations. Its tour company owns and operates hotels, lodges, glass-domed railcars and motorcoaches.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Holland America Line Launches Anniversary Sale with Major Discounts

- Anniversary Sale Launch: Holland America Line is celebrating its 153rd anniversary with a month-long sale from April 2 to 30, 2026, offering up to 30% off cruise fares and onboard credits up to $400 per stateroom, aimed at enticing both loyal and new travelers to experience their thoughtfully crafted itineraries.

- Family Travel Incentives: The promotion allows third and fourth guests aged 18 and under to cruise for free on select sailings, significantly reducing costs for family vacations and enhancing Holland America's appeal in the family travel segment.

- Combination Offer Policy: The Anniversary Sale can be combined with the

See More

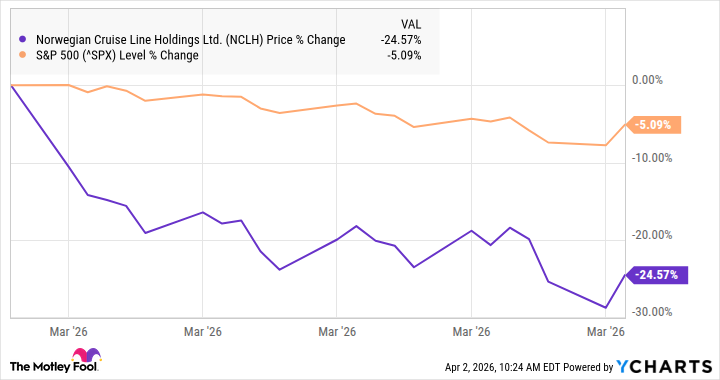

Norwegian Cruise Line's Poor Performance Leads to Stock Decline

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, driven by higher capacity days, yet fell short of the $2.34 billion estimate, indicating management execution gaps that led to decreased market confidence.

- Significant Stock Decline: The stock plummeted 24% last month due to disappointing earnings and geopolitical instability from the Iran war, reflecting investor concerns about the company's future prospects amidst rising oil prices.

- Improved Profitability: Despite missing revenue expectations, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, demonstrating effective cost control, yet failing to reverse the overall negative trend.

- Board Changes: Following pressure from activist investor Elliott Investment Management, Norwegian has appointed five new board members, which, while not immediately boosting stock prices, may lay the groundwork for future strategic adjustments and improvements.

See More

Norwegian Cruise Line Misses Q4 Revenue Estimates

- Revenue Miss: Norwegian Cruise Line's Q4 revenue rose 6% to $2.2 billion, falling short of the $2.34 billion estimate, as higher capacity days contributed to growth but execution gaps significantly impacted performance.

- Profitability Improvement: Adjusted EBITDA increased by 11% to $2.73 billion, while adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, indicating effective cost management despite revenue challenges.

- Bleak Outlook: The company forecasts flat net yields for 2026, with cruise costs expected to rise by 0.9%, which will pressure profitability; adjusted EPS guidance of $2.38 is below the consensus of $2.60, reflecting ongoing challenges.

- Board Changes: Following pressure from activist investor Elliott Management, Norwegian appointed five new board members, which, while not boosting stock prices immediately, may set the stage for future improvements in governance and performance.

See More

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

US Stocks Close Mixed Amid Oil Surge and Economic Data

- Market Fluctuations: The S&P 500 Index closed up 0.11%, while the Dow Jones Industrial Average fell 0.13%, and the Nasdaq 100 Index rose 0.11%, reflecting volatility influenced by surging oil prices and economic data.

- Positive Economic Data: Weekly initial unemployment claims unexpectedly fell by 9,000 to 202,000, indicating a stronger labor market than the anticipated increase to 212,000, which could impact the Fed's interest rate policy.

- Impact of Oil Surge: Crude oil prices soared over 11% due to President Trump's tougher stance on Iran, leading to sharp declines in airline and cruise line stocks, with United Airlines and Carnival both down more than 3%.

- Corporate Developments: SBA Communications surged over 18% as it explores potential acquisition options, while Globalstar rose over 13% amid reports of Amazon's interest in acquiring the company, highlighting market focus on M&A activity.

See More

Stock Markets Pressured by Soaring Oil Prices

- Oil Price Surge Pressures Markets: Stock indexes are under pressure as crude oil prices soar over 8% following President Trump's aggressive stance on Iran, leading to a 0.06% drop in the S&P 500, a 0.23% decline in the Dow, and a 0.20% fall in the Nasdaq 100, indicating heightened inflation concerns among investors.

- Unexpected Jobless Claims Drop: Despite market pressures, initial jobless claims fell by 9,000 to 202,000, indicating a stronger labor market than anticipated, which may provide some support for stocks and alleviate investor fears of an economic slowdown.

- Divergent Energy Sector Performance: Energy producers like Diamondback Energy rose over 2% due to soaring WTI prices, while airline stocks such as American Airlines and Carnival fell more than 4% as rising fuel costs cut into profits, highlighting a clear divergence across sectors.

- Tech Stocks Decline: Chipmakers and AI infrastructure stocks retreated, with ARM Holdings leading the Nasdaq 100 down over 5%, reflecting waning confidence in tech stocks and potentially impacting future investment decisions.

See More

Holland America Line Launches Anniversary Sale with Major Discounts

- Anniversary Sale Launch: Holland America Line is celebrating its 153rd anniversary with a month-long sale from April 2 to 30, 2026, offering up to 30% off cruise fares and onboard credits up to $400 per stateroom, aimed at enticing both loyal and new travelers to experience their thoughtfully crafted itineraries.

- Family Travel Incentives: The promotion allows third and fourth guests aged 18 and under to cruise for free on select sailings, significantly reducing costs for family vacations and enhancing Holland America's appeal in the family travel segment.

- Combination Offer Policy: The Anniversary Sale can be combined with the

See More

Norwegian Cruise Line's Poor Performance Leads to Stock Decline

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, driven by higher capacity days, yet fell short of the $2.34 billion estimate, indicating management execution gaps that led to decreased market confidence.

- Significant Stock Decline: The stock plummeted 24% last month due to disappointing earnings and geopolitical instability from the Iran war, reflecting investor concerns about the company's future prospects amidst rising oil prices.

- Improved Profitability: Despite missing revenue expectations, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, demonstrating effective cost control, yet failing to reverse the overall negative trend.

- Board Changes: Following pressure from activist investor Elliott Investment Management, Norwegian has appointed five new board members, which, while not immediately boosting stock prices, may lay the groundwork for future strategic adjustments and improvements.

See More

Norwegian Cruise Line Misses Q4 Revenue Estimates

- Revenue Miss: Norwegian Cruise Line's Q4 revenue rose 6% to $2.2 billion, falling short of the $2.34 billion estimate, as higher capacity days contributed to growth but execution gaps significantly impacted performance.

- Profitability Improvement: Adjusted EBITDA increased by 11% to $2.73 billion, while adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, indicating effective cost management despite revenue challenges.

- Bleak Outlook: The company forecasts flat net yields for 2026, with cruise costs expected to rise by 0.9%, which will pressure profitability; adjusted EPS guidance of $2.38 is below the consensus of $2.60, reflecting ongoing challenges.

- Board Changes: Following pressure from activist investor Elliott Management, Norwegian appointed five new board members, which, while not boosting stock prices immediately, may set the stage for future improvements in governance and performance.

See More

Norwegian Cruise Line Reports Disappointing Earnings, Stock Falls 24%

- Disappointing Earnings Report: Norwegian Cruise Line's fourth-quarter revenue rose 6% to $2.2 billion, falling short of market expectations of $2.34 billion, indicating management execution gaps that have eroded market confidence.

- Improved Profitability: Despite revenue misses, adjusted EBITDA increased by 11% to $2.73 billion, and adjusted earnings per share surged 46% to $0.28, exceeding expectations of $0.27, demonstrating effective cost control measures.

- Bleak Future Outlook: Norwegian anticipates flat net yields for 2026, with adjusted earnings per share projected at $2.38, below the consensus estimate of $2.60, highlighting ongoing fundamental challenges facing the company.

- Investor Attention: Activist investor Elliott Investment Management called for urgent board reforms, resulting in the appointment of five new board members, which, while not boosting stock prices immediately, may lay the groundwork for future improvements.

See More

US Stocks Close Mixed Amid Oil Surge and Economic Data

- Market Fluctuations: The S&P 500 Index closed up 0.11%, while the Dow Jones Industrial Average fell 0.13%, and the Nasdaq 100 Index rose 0.11%, reflecting volatility influenced by surging oil prices and economic data.

- Positive Economic Data: Weekly initial unemployment claims unexpectedly fell by 9,000 to 202,000, indicating a stronger labor market than the anticipated increase to 212,000, which could impact the Fed's interest rate policy.

- Impact of Oil Surge: Crude oil prices soared over 11% due to President Trump's tougher stance on Iran, leading to sharp declines in airline and cruise line stocks, with United Airlines and Carnival both down more than 3%.

- Corporate Developments: SBA Communications surged over 18% as it explores potential acquisition options, while Globalstar rose over 13% amid reports of Amazon's interest in acquiring the company, highlighting market focus on M&A activity.

See More

Stock Markets Pressured by Soaring Oil Prices

- Oil Price Surge Pressures Markets: Stock indexes are under pressure as crude oil prices soar over 8% following President Trump's aggressive stance on Iran, leading to a 0.06% drop in the S&P 500, a 0.23% decline in the Dow, and a 0.20% fall in the Nasdaq 100, indicating heightened inflation concerns among investors.

- Unexpected Jobless Claims Drop: Despite market pressures, initial jobless claims fell by 9,000 to 202,000, indicating a stronger labor market than anticipated, which may provide some support for stocks and alleviate investor fears of an economic slowdown.

- Divergent Energy Sector Performance: Energy producers like Diamondback Energy rose over 2% due to soaring WTI prices, while airline stocks such as American Airlines and Carnival fell more than 4% as rising fuel costs cut into profits, highlighting a clear divergence across sectors.

- Tech Stocks Decline: Chipmakers and AI infrastructure stocks retreated, with ARM Holdings leading the Nasdaq 100 down over 5%, reflecting waning confidence in tech stocks and potentially impacting future investment decisions.

See More