BRODSKY & SMITH SHAREHOLDER UPDATE: Notifying Investors of the Following Investigations: WideOpenWest, Inc. (NYSE - WOW), BankFinancial Corporation (Nasdaq - BFIN), STAAR Surgical Company (Nasdaq – STAA), Y-mAbs Therapeutics, Inc. (Nasdaq – YMAB)

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Aug 12 2025

0mins

Source: Globenewswire

Investigations Announced: Brodsky & Smith is reminding investors of ongoing investigations into several companies, including WideOpenWest, BankFinancial Corporation, STAAR Surgical Company, and Y-mAbs Therapeutics, regarding potential breaches of fiduciary duties by their boards during acquisition processes.

Acquisition Details: Each company mentioned is set to be acquired at specified cash values per share, raising concerns about whether the deals provide fair value to shareholders.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy STAA?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on STAA

Wall Street analysts forecast STAA stock price to fall

3 Analyst Rating

0 Buy

3 Hold

0 Sell

Hold

Current: 32.470

Low

30.75

Averages

30.75

High

30.75

Current: 32.470

Low

30.75

Averages

30.75

High

30.75

About STAA

STAAR Surgical Company designs, develops, manufactures, and sells implantable lenses for the eye and accessory delivery systems used to deliver the lenses into the eye. The Company markets and sells its ICLs for refractive surgery to treat myopia (nearsightedness) as its EVO family of lenses. Its EVO family of lenses includes its EVO ICL, EVO+ ICL, and EVO Visian ICL. The Company's newest offering, EVO Viva, has an extended depth of focus (EDoF) optic, which is designed to treat myopia with presbyopia (age-related loss of ability to focus). It also market and sell an ICL lens to treat hyperopia (farsightedness), called Visian ICL. It makes its ICL product offerings available in multiple models, powers and lengths, including some with toric ICL (TICL) versions to correct for astigmatism (blurred vision). The Company’s principal products are ICLs used in refractive surgery, including its EVO family of lenses.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Staar Surgical Q1 Results Exceed Expectations, Analysts Turn Bullish

- Strong Earnings Beat: Staar Surgical reported Q1 net sales of $93.5 million, surpassing Wall Street's expectations of $78.72 million, indicating robust performance amid market recovery and likely driving stock price appreciation.

- Analyst Upgrades: Wedbush upgraded Staar Surgical from 'Neutral' to 'Outperform' and raised its price target from $26 to $40, reflecting optimistic expectations for the company's future growth and potentially prompting a re-rating of its valuation.

- Recovery in China: The company noted that net sales in China were primarily driven by a recovery in market demand, positioning it favorably for growth in the upcoming quarters, suggesting that the company is at or near an inflection point for recovery.

- Improved Retail Sentiment: On Stocktwits, retail sentiment around Staar Surgical improved from 'Bullish' to 'Extremely Bullish', with message volume significantly increasing, indicating heightened investor confidence in the company's future performance.

See More

STAAR Surgical Surges 10% After Massive Q1 Earnings Beat

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, exceeding estimates by $0.40, with revenue soaring 119.5% year-over-year to $93.5 million, surpassing analyst expectations by $14.78 million, indicating robust market demand and recovery in profitability.

- China as Growth Driver: Sales from China reached $47.4 million, driven by strong demand for the newly launched EVO+ lenses, with management noting that distributor inventory is fully normalized, meaning growth is fueled by real customer demand rather than inventory restocking.

- Significant Profit Recovery: The company swung to a net income of $5.2 million from a loss of $54.2 million last year, with adjusted EBITDA at $24.4 million, showcasing strong margin recovery and operating leverage, which further boosts investor confidence.

- Optimistic Market Outlook: Although management did not provide full-year revenue guidance, they expect a strong Q2 and continue to target around 75% gross margin for FY26, with analysts raising STAAR's 12-month price targets from $26 to $40, reflecting optimistic market sentiment regarding future growth.

See More

STAAR Surgical Surpasses Q1 2026 Expectations, Upgraded by Wedbush

- Significant Revenue Growth: STAAR Surgical reported $93.5 million in revenue for Q1 2026, achieving over 100% year-over-year growth and exceeding consensus estimates by $14.8 million, indicating a strong recovery in its Chinese operations and continued double-digit growth in the U.S.

- Analyst Rating Upgrade: Wedbush Securities upgraded STAAR's rating from Neutral to Outperform, reflecting confidence in the company's future performance, particularly in light of the recovery in the Chinese market, which is expected to drive continued growth in the upcoming quarters.

- Positive Management Outlook: Although the company declined to issue guidance again, management's positive remarks during the conference call suggest that STAAR is positioned to outperform initial analyst expectations, especially as it approaches the historically strong seasonal demand during China's summer peak in Q2/Q3.

- Price Target Increase: Analyst Michael Piccolo raised his price target on STAAR from $26 to $40, based on increased revenue estimates for FY26 and a reassessment of valuation multiples, reflecting an optimistic outlook on the company's growth potential moving forward.

See More

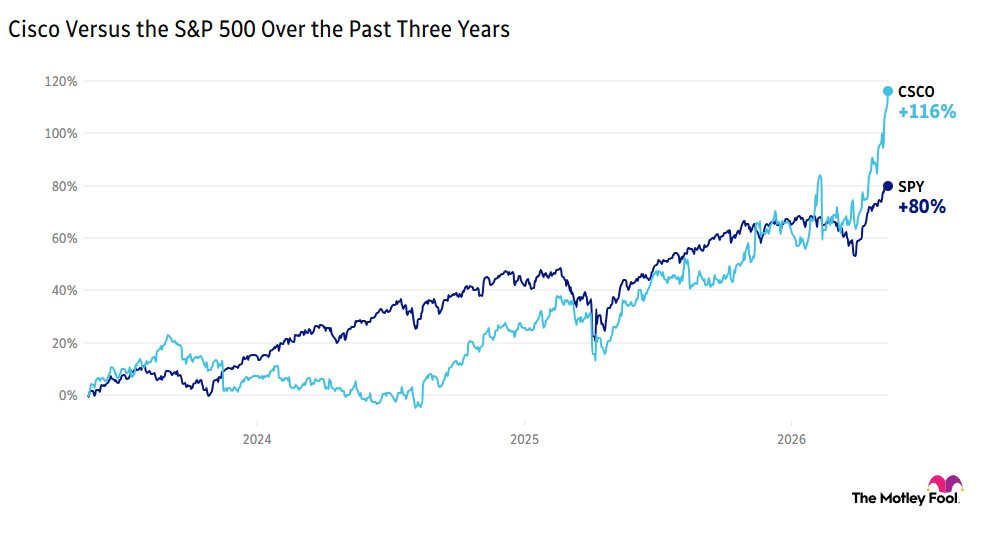

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

STAAR Surgical Q1 2026 Earnings Call Highlights

- Significant Sales Growth: In Q1 2026, STAAR Surgical reported net sales of $93.5 million, a remarkable 119.6% increase year-over-year, with $47.4 million coming from the Chinese market, indicating strong global performance and a recovery in sales, particularly in China.

- Improved Profitability: The adjusted EBITDA reached $24.4 million with a gross profit margin of 73.6%, reflecting substantial progress in cost control and profitability enhancement, although total operating expenses were $60.9 million, highlighting the need for ongoing cost management during expansion.

- EVO+ ICL Launch Progress: The successful launch of EVO+ ICL in China, with meaningful volumes shipped and inventory levels normalized to contractual targets, demonstrates the company's adaptability in new product promotion and market demand, which is expected to drive future sales growth.

- Cautious Future Outlook: While management remains optimistic about a $225 million spending target for 2026, they refrained from providing specific revenue guidance due to macroeconomic and geopolitical uncertainties, indicating a cautious approach to future market conditions.

See More

STAAR Surgical Q1 Earnings Exceed Expectations

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, surpassing expectations by $0.40, indicating a significant improvement in the company's profitability.

- Revenue Surge: Q1 revenue reached $93.5 million, a remarkable 119.5% year-over-year increase, exceeding market expectations by $14.78 million, reflecting rapid growth driven by strong market demand.

- Gross Margin Improvement: The gross margin improved from 65.8% a year ago to 73.6%, demonstrating significant progress in cost control and product pricing, thereby enhancing overall profitability.

- Net Income Recovery: The company achieved a net income of $5.2 million, or $0.10 per diluted share, compared to a net loss of $54.2 million a year ago, showcasing a substantial recovery in financial health.

See More

Staar Surgical Q1 Results Exceed Expectations, Analysts Turn Bullish

- Strong Earnings Beat: Staar Surgical reported Q1 net sales of $93.5 million, surpassing Wall Street's expectations of $78.72 million, indicating robust performance amid market recovery and likely driving stock price appreciation.

- Analyst Upgrades: Wedbush upgraded Staar Surgical from 'Neutral' to 'Outperform' and raised its price target from $26 to $40, reflecting optimistic expectations for the company's future growth and potentially prompting a re-rating of its valuation.

- Recovery in China: The company noted that net sales in China were primarily driven by a recovery in market demand, positioning it favorably for growth in the upcoming quarters, suggesting that the company is at or near an inflection point for recovery.

- Improved Retail Sentiment: On Stocktwits, retail sentiment around Staar Surgical improved from 'Bullish' to 'Extremely Bullish', with message volume significantly increasing, indicating heightened investor confidence in the company's future performance.

See More

STAAR Surgical Surges 10% After Massive Q1 Earnings Beat

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, exceeding estimates by $0.40, with revenue soaring 119.5% year-over-year to $93.5 million, surpassing analyst expectations by $14.78 million, indicating robust market demand and recovery in profitability.

- China as Growth Driver: Sales from China reached $47.4 million, driven by strong demand for the newly launched EVO+ lenses, with management noting that distributor inventory is fully normalized, meaning growth is fueled by real customer demand rather than inventory restocking.

- Significant Profit Recovery: The company swung to a net income of $5.2 million from a loss of $54.2 million last year, with adjusted EBITDA at $24.4 million, showcasing strong margin recovery and operating leverage, which further boosts investor confidence.

- Optimistic Market Outlook: Although management did not provide full-year revenue guidance, they expect a strong Q2 and continue to target around 75% gross margin for FY26, with analysts raising STAAR's 12-month price targets from $26 to $40, reflecting optimistic market sentiment regarding future growth.

See More

STAAR Surgical Surpasses Q1 2026 Expectations, Upgraded by Wedbush

- Significant Revenue Growth: STAAR Surgical reported $93.5 million in revenue for Q1 2026, achieving over 100% year-over-year growth and exceeding consensus estimates by $14.8 million, indicating a strong recovery in its Chinese operations and continued double-digit growth in the U.S.

- Analyst Rating Upgrade: Wedbush Securities upgraded STAAR's rating from Neutral to Outperform, reflecting confidence in the company's future performance, particularly in light of the recovery in the Chinese market, which is expected to drive continued growth in the upcoming quarters.

- Positive Management Outlook: Although the company declined to issue guidance again, management's positive remarks during the conference call suggest that STAAR is positioned to outperform initial analyst expectations, especially as it approaches the historically strong seasonal demand during China's summer peak in Q2/Q3.

- Price Target Increase: Analyst Michael Piccolo raised his price target on STAAR from $26 to $40, based on increased revenue estimates for FY26 and a reassessment of valuation multiples, reflecting an optimistic outlook on the company's growth potential moving forward.

See More

Cisco's Transformation in the AI Era

- Earnings Surge: Cisco (CSCO) saw a 20% pre-market jump, driven by a positive outlook from its business restructuring, with CFO Mark Patterson indicating an expansion of its silicon portfolio to meet data center demands, thereby enhancing its competitive edge in the AI market.

- Job Cuts and Investments: CEO Chuck Robbins announced nearly 4,000 job cuts; however, the company plans to increase investments in AI, aiming to shift resources towards areas with the strongest demand and long-term value creation, ensuring sustainable growth in the future.

- Chinese Market Opportunities: Alibaba (BABA) and JD.com (JD) received U.S. approval to purchase Nvidia's H200 chips, although no deliveries have been made yet, indicating a significant potential revenue opportunity for Nvidia in the Chinese market, which could impact its dominance in the global chip market.

- AI-Driven Growth: Cellebrite DI (CLBT) is expected to report an 18% year-over-year revenue growth, primarily driven by strong demand for AI-driven investigative tools, showcasing the company's robust execution and adaptability in the AI sector.

See More

STAAR Surgical Q1 2026 Earnings Call Highlights

- Significant Sales Growth: In Q1 2026, STAAR Surgical reported net sales of $93.5 million, a remarkable 119.6% increase year-over-year, with $47.4 million coming from the Chinese market, indicating strong global performance and a recovery in sales, particularly in China.

- Improved Profitability: The adjusted EBITDA reached $24.4 million with a gross profit margin of 73.6%, reflecting substantial progress in cost control and profitability enhancement, although total operating expenses were $60.9 million, highlighting the need for ongoing cost management during expansion.

- EVO+ ICL Launch Progress: The successful launch of EVO+ ICL in China, with meaningful volumes shipped and inventory levels normalized to contractual targets, demonstrates the company's adaptability in new product promotion and market demand, which is expected to drive future sales growth.

- Cautious Future Outlook: While management remains optimistic about a $225 million spending target for 2026, they refrained from providing specific revenue guidance due to macroeconomic and geopolitical uncertainties, indicating a cautious approach to future market conditions.

See More

STAAR Surgical Q1 Earnings Exceed Expectations

- Earnings Beat: STAAR Surgical reported a Q1 non-GAAP EPS of $0.48, surpassing expectations by $0.40, indicating a significant improvement in the company's profitability.

- Revenue Surge: Q1 revenue reached $93.5 million, a remarkable 119.5% year-over-year increase, exceeding market expectations by $14.78 million, reflecting rapid growth driven by strong market demand.

- Gross Margin Improvement: The gross margin improved from 65.8% a year ago to 73.6%, demonstrating significant progress in cost control and product pricing, thereby enhancing overall profitability.

- Net Income Recovery: The company achieved a net income of $5.2 million, or $0.10 per diluted share, compared to a net loss of $54.2 million a year ago, showcasing a substantial recovery in financial health.

See More