Booking Holdings: Navigating AI Challenges and Opportunities

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 10 2026

0mins

Source: Fool

- Industry Recovery: The travel industry has been on an upward trajectory since the pandemic, with Booking Holdings leveraging this trend to achieve nearly $27 billion in revenue, reflecting a 13% year-over-year increase, showcasing its strong market performance and profitability.

- Competitive Advantage: Booking owns several well-known travel platforms, including Booking.com and Priceline, connecting over 4 million accommodation options worldwide, with 90% of room nights booked coming from independent hotels and small chains, highlighting its scale and broad property supply advantage.

- Strategic Expansion: Through its Connected Trip strategy, Booking is not only offering hotel-plus-flight packages but also expanding into car rentals and attraction ticket sales, with airline ticket sales increasing by 37% year-over-year in 2025 and attraction tickets nearly 80%, creating sustainable growth drivers for shareholders.

- AI Risks and Opportunities: While AI poses competitive pressures, Booking's investment in generative AI and its rich data resources can enhance user experience; management targets approximately 8% annual bookings growth and over 15% annualized earnings-per-share growth, providing an attractive setup for investors.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BKNG?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BKNG

Wall Street analysts forecast BKNG stock price to rise

25 Analyst Rating

18 Buy

7 Hold

0 Sell

Moderate Buy

Current: 167.430

Low

5407

Averages

6153

High

6850

Current: 167.430

Low

5407

Averages

6153

High

6850

About BKNG

Booking Holdings Inc. is a provider of travel and restaurant online reservation and related services. The Company offers its services through five primary consumer-facing brands: Booking.com, Priceline, Agoda, KAYAK, and OpenTable. Through its brands, consumers can book an array of accommodations (including hotels, motels, resorts, homes, apartments, bed and breakfasts, hostels, and other alternative and traditional accommodation properties) and a flight to their destinations; make a car rental reservation or arrange for an airport taxi; make a dinner reservation; or book a vacation package, tour, activity, or cruise. Consumers can also use its meta-search services to easily compare travel reservation information, such as flight, hotel, and rental car reservations from hundreds of online travel platforms at once. Booking.com offers accommodation reservation services for approximately 4.0 million properties in over 220 countries and territories and in over 40 languages.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

2026 FIFA World Cup Expected to Boost North American Tourism

- Event-Driven Spending: According to a William Blair report, the 2026 FIFA World Cup is expected to boost tourism and hospitality spending in North America, although the overall economic growth impact is limited, primarily benefiting leisure and hospitality sectors.

- Spectator Spending Trends: Data from the 2025 FIFA Club World Cup indicated that spending in stadium-area zip codes rose approximately 7% year-over-year during the event, driven largely by restaurant and bar expenditures, showcasing strong spectator demand for the tournament.

- Dynamic Ticket Pricing: While FIFA's dynamic pricing has pushed some ticket prices to record highs, several match prices have recently been lowered due to softened sales, reflecting market sensitivity and uncertainty regarding ticket demand.

- Market Performance Impact: Historical analysis shows that stock trading volumes tend to decline during World Cup matches, particularly in countries with strong football followings, and that World Cup-winning nations have historically outperformed global equities by an average of 5.5% in the month following the final.

See More

Agoda Recommends Water Park Destinations in Asia

- Family Fun Recommendations: Agoda's recommended water park destinations include Sunway Lost World of Tambun in Malaysia, which combines an amusement park and hot springs, attracting family visitors and enhancing local tourism appeal.

- Diverse Experiences: Thailand's Vana Nava Waterpark in Hua Hin is known for its state-of-the-art slides, offering thrilling experiences for all ages, while Hua Hin's beautiful beaches and night markets provide rich leisure options for travelers.

- Modern Facilities: Mikazuki Water Park in Da Nang, Vietnam features a variety of slides and pools catering to both thrill-seekers and those looking to relax, with Da Nang's stunning beaches and cultural sites further boosting its tourism appeal.

- Cultural and Entertainment Fusion: Japan's Oiso Long Beach combines traditional charm with modern attractions, offering diverse water activities while allowing visitors to explore the cultural and historical offerings of Kanagawa Prefecture, enhancing the overall travel experience.

See More

Analysis of XLY ETF's 52-Week Price Fluctuations

- Price Range Analysis: The XLY ETF's 52-week low is $103.855 per share, with a high of $125.01, and the latest trade at $121.49 indicates relative stability in the current market, potentially attracting investor interest.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average can provide valuable insights for investors, helping them assess market trends and identify potential buying opportunities to optimize investment decisions.

- ETF Trading Mechanism: Exchange-traded funds (ETFs) trade similarly to stocks, where investors are buying and selling 'units' that can be created or destroyed based on investor demand, offering flexibility in adapting to market fluctuations.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs highlights those experiencing notable inflows (new units created) or outflows (old units destroyed), as these liquidity changes can impact the performance of individual stocks within the ETF, thereby affecting the overall investment portfolio.

See More

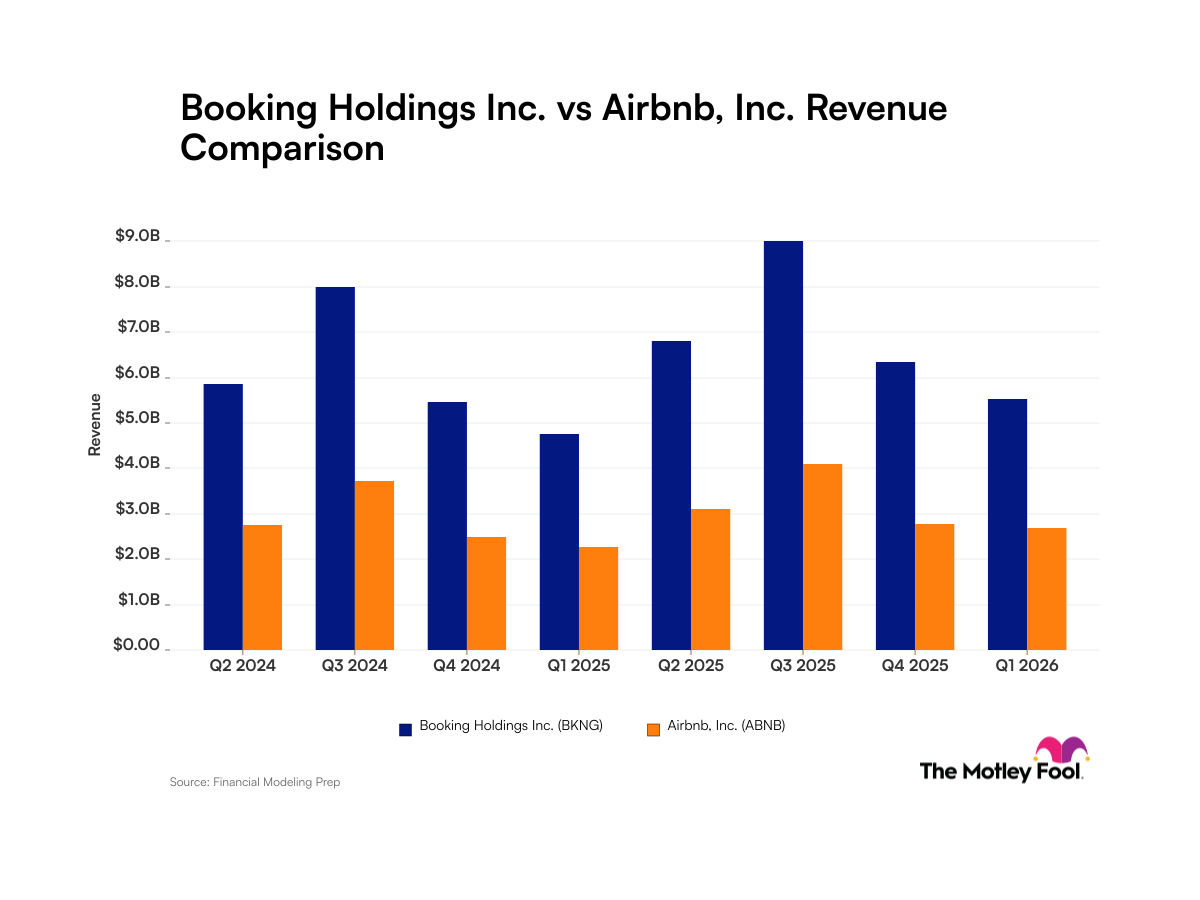

Quarterly Revenue Analysis for Booking and Airbnb

- Quarterly Revenue Performance: Booking reported $5.5 billion in revenue for Q1 2026, reflecting a 16% year-over-year growth, while Airbnb's revenue for the same period was $2.7 billion, showing an 18% increase, indicating both companies are actively expanding in the market.

- Competitive Market Dynamics: Although Booking's revenue significantly exceeds that of Airbnb, the latter's faster growth rate suggests that its efforts to diversify into hotels and additional services may pose a competitive threat to Booking's market share.

- Seasonal Sales Fluctuations: The third quarter typically serves as a peak sales period for both companies, with significant sales boosts during the summer travel season, highlighting the seasonal nature of travel demand.

- Future Outlook and Challenges: Booking forecasts a revenue increase of 4% to 6% year-over-year for Q2, a stark decline from its 16% growth in Q1, primarily due to the impact of conflicts with Iran, which may negatively affect its future performance.

See More

Financial Comparison Between Booking and Airbnb

- Revenue Scale Comparison: Booking consistently generates significantly higher total revenue than Airbnb across all reporting periods, with Booking reporting $5.5 billion in sales for Q1 2026 compared to Airbnb's $2.7 billion, indicating Booking's dominant market position.

- Quarterly Revenue Fluctuations: Both companies experience revenue declines in Q1 but see substantial increases in Q3 due to the summer travel season, with Booking's growth rate at 16% and Airbnb's at 18%, suggesting Airbnb's market expansion strategies are effective.

- Market Challenges and Outlook: Booking's stock fell to a 52-week low of $150.14 on May 20 due to conflicts with Iran, forecasting only a 4% to 6% year-over-year revenue increase for Q2, which is a stark contrast to its Q1 growth, reflecting external pressures on its business.

- Investor Considerations: Despite Booking's larger revenue scale, analysts note it was not included in the “best stocks” list, prompting investors to carefully evaluate its future growth potential, especially in a competitive market landscape.

See More

OpenTable Expands with New Toronto Office Lease

- New Office Opening: OpenTable has signed a multi-year lease at Allied's 134 Peter Street in Downtown Toronto, securing over 24,000 square feet of premium office space, marking a significant milestone in its commitment to the Canadian market and international expansion.

- Team Expansion Plans: The new office is expected to accommodate over 200 employees, with OpenTable actively hiring across engineering, product, marketing, and more to support global product innovation and local operations.

- Tech Talent Utilization: By establishing a new office in Toronto, OpenTable can tap into the city's world-class tech talent pool, thereby driving global product innovation and further solidifying its position in the Canadian restaurant industry.

- Confidence in the Industry: OpenTable's expansion in Toronto is seen as a strong show of confidence in the Canadian restaurant sector, supporting local economies and communities while enhancing service for restaurant operators and diners.

See More

2026 FIFA World Cup Expected to Boost North American Tourism

- Event-Driven Spending: According to a William Blair report, the 2026 FIFA World Cup is expected to boost tourism and hospitality spending in North America, although the overall economic growth impact is limited, primarily benefiting leisure and hospitality sectors.

- Spectator Spending Trends: Data from the 2025 FIFA Club World Cup indicated that spending in stadium-area zip codes rose approximately 7% year-over-year during the event, driven largely by restaurant and bar expenditures, showcasing strong spectator demand for the tournament.

- Dynamic Ticket Pricing: While FIFA's dynamic pricing has pushed some ticket prices to record highs, several match prices have recently been lowered due to softened sales, reflecting market sensitivity and uncertainty regarding ticket demand.

- Market Performance Impact: Historical analysis shows that stock trading volumes tend to decline during World Cup matches, particularly in countries with strong football followings, and that World Cup-winning nations have historically outperformed global equities by an average of 5.5% in the month following the final.

See More

Agoda Recommends Water Park Destinations in Asia

- Family Fun Recommendations: Agoda's recommended water park destinations include Sunway Lost World of Tambun in Malaysia, which combines an amusement park and hot springs, attracting family visitors and enhancing local tourism appeal.

- Diverse Experiences: Thailand's Vana Nava Waterpark in Hua Hin is known for its state-of-the-art slides, offering thrilling experiences for all ages, while Hua Hin's beautiful beaches and night markets provide rich leisure options for travelers.

- Modern Facilities: Mikazuki Water Park in Da Nang, Vietnam features a variety of slides and pools catering to both thrill-seekers and those looking to relax, with Da Nang's stunning beaches and cultural sites further boosting its tourism appeal.

- Cultural and Entertainment Fusion: Japan's Oiso Long Beach combines traditional charm with modern attractions, offering diverse water activities while allowing visitors to explore the cultural and historical offerings of Kanagawa Prefecture, enhancing the overall travel experience.

See More

Analysis of XLY ETF's 52-Week Price Fluctuations

- Price Range Analysis: The XLY ETF's 52-week low is $103.855 per share, with a high of $125.01, and the latest trade at $121.49 indicates relative stability in the current market, potentially attracting investor interest.

- Technical Analysis Tool: Comparing the latest share price to the 200-day moving average can provide valuable insights for investors, helping them assess market trends and identify potential buying opportunities to optimize investment decisions.

- ETF Trading Mechanism: Exchange-traded funds (ETFs) trade similarly to stocks, where investors are buying and selling 'units' that can be created or destroyed based on investor demand, offering flexibility in adapting to market fluctuations.

- Inflows and Outflows Monitoring: Weekly monitoring of changes in shares outstanding for ETFs highlights those experiencing notable inflows (new units created) or outflows (old units destroyed), as these liquidity changes can impact the performance of individual stocks within the ETF, thereby affecting the overall investment portfolio.

See More

Quarterly Revenue Analysis for Booking and Airbnb

- Quarterly Revenue Performance: Booking reported $5.5 billion in revenue for Q1 2026, reflecting a 16% year-over-year growth, while Airbnb's revenue for the same period was $2.7 billion, showing an 18% increase, indicating both companies are actively expanding in the market.

- Competitive Market Dynamics: Although Booking's revenue significantly exceeds that of Airbnb, the latter's faster growth rate suggests that its efforts to diversify into hotels and additional services may pose a competitive threat to Booking's market share.

- Seasonal Sales Fluctuations: The third quarter typically serves as a peak sales period for both companies, with significant sales boosts during the summer travel season, highlighting the seasonal nature of travel demand.

- Future Outlook and Challenges: Booking forecasts a revenue increase of 4% to 6% year-over-year for Q2, a stark decline from its 16% growth in Q1, primarily due to the impact of conflicts with Iran, which may negatively affect its future performance.

See More

Financial Comparison Between Booking and Airbnb

- Revenue Scale Comparison: Booking consistently generates significantly higher total revenue than Airbnb across all reporting periods, with Booking reporting $5.5 billion in sales for Q1 2026 compared to Airbnb's $2.7 billion, indicating Booking's dominant market position.

- Quarterly Revenue Fluctuations: Both companies experience revenue declines in Q1 but see substantial increases in Q3 due to the summer travel season, with Booking's growth rate at 16% and Airbnb's at 18%, suggesting Airbnb's market expansion strategies are effective.

- Market Challenges and Outlook: Booking's stock fell to a 52-week low of $150.14 on May 20 due to conflicts with Iran, forecasting only a 4% to 6% year-over-year revenue increase for Q2, which is a stark contrast to its Q1 growth, reflecting external pressures on its business.

- Investor Considerations: Despite Booking's larger revenue scale, analysts note it was not included in the “best stocks” list, prompting investors to carefully evaluate its future growth potential, especially in a competitive market landscape.

See More

OpenTable Expands with New Toronto Office Lease

- New Office Opening: OpenTable has signed a multi-year lease at Allied's 134 Peter Street in Downtown Toronto, securing over 24,000 square feet of premium office space, marking a significant milestone in its commitment to the Canadian market and international expansion.

- Team Expansion Plans: The new office is expected to accommodate over 200 employees, with OpenTable actively hiring across engineering, product, marketing, and more to support global product innovation and local operations.

- Tech Talent Utilization: By establishing a new office in Toronto, OpenTable can tap into the city's world-class tech talent pool, thereby driving global product innovation and further solidifying its position in the Canadian restaurant industry.

- Confidence in the Industry: OpenTable's expansion in Toronto is seen as a strong show of confidence in the Canadian restaurant sector, supporting local economies and communities while enhancing service for restaurant operators and diners.

See More