Biohaven Ltd's Depression Drug Trial Fails to Meet Primary Endpoint, Shares Plunge 14.3%

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Dec 26 2025

0mins

Source: Benzinga

- Drug Trial Failure: Biohaven Ltd announced that its depression drug BHV-7000 failed to significantly reduce depressive symptoms in a six-week clinical trial, causing shares to plummet 14.3% to $9.27 in pre-market trading, reflecting a substantial decline in market confidence regarding its R&D capabilities.

- Severe Market Reaction: The news of the trial's failure triggered panic among investors, leading to a rapid decline in Biohaven's stock price during pre-market trading, indicating the high sensitivity of the biopharmaceutical sector to clinical outcomes, which may impact the company's future financing and R&D plans.

- Increased Competitive Pressure: With Biohaven's drug trial failure, market attention shifts to other competitors, particularly in the depression treatment space, potentially leading investors to reassess the market outlook and investment value of related companies.

- Wider Industry Implications: Biohaven's failure could have a ripple effect across the biopharmaceutical industry, particularly in terms of R&D investments and clinical trial designs, prompting other companies to more cautiously evaluate their drug development strategies.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy BHVN?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on BHVN

Wall Street analysts forecast BHVN stock price to rise

13 Analyst Rating

9 Buy

4 Hold

0 Sell

Moderate Buy

Current: 11.400

Low

11.00

Averages

18.00

High

30.00

Current: 11.400

Low

11.00

Averages

18.00

High

30.00

About BHVN

Biohaven Ltd. is a biopharmaceutical company focused on the discovery, development and commercialization of treatments in key therapeutic areas, including immunology, neuroscience, and oncology. It is advancing its portfolio of therapeutics, leveraging its drug development experience and multiple proprietary drug development platforms. Its clinical and preclinical programs include Kv7 ion channel modulation for epilepsy; Molecular Degrader of Extracellular Proteins (MoDE) and Targeted Removal of Aberrant Protein (TRAP) extracellular protein degradation for immunological diseases; and myostatin-activin pathway targeting agent for neuromuscular and metabolic diseases, including obesity. Its pipeline includes TYK2/JAK1 Inhibitor (brain-penetrant), IgG Degrader, Gd-IgA1 TRAP Degrader, Taldefgrobep Alfa, Kv7 Activator, TRPM3 Antagonist FGFR3 ADC, CD30 ADC, Trop2 ADC +/- PD1, and others. Its advanced product candidate from its glutamate receptor antagonist platform is troriluzole.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Valuation Analysis of U.S. Small-Cap Healthcare Stocks

- Valuation Score Overview: Seeking Alpha's valuation grade assesses healthcare stocks' relative price attractiveness within their sector using metrics like P/E, PEG, and EV/Sales, aiding investors in identifying potential investment opportunities.

- Market Performance Highlight: Among healthcare stocks with market caps between $300M and $2B, Biohaven (BHVN) is rated as the most expensive, indicating its high valuation level in the market, which may influence investor purchasing decisions.

- Other High-Valuation Companies: Companies like Greenwich LifeSciences (GLSI), HealthStream (HSTM), and Immix Biopharma (IMMX) received F grades, suggesting they are viewed as high-risk investments in the current market environment, potentially leading to investor caution.

- Financing Dynamics: Immix Biopharma recently priced a $150M stock offering at $8.94 per share, and despite valuation pressures, its stock rose following the release of mid-stage trial data for AL amyloidosis therapy, indicating market interest in its potential.

See More

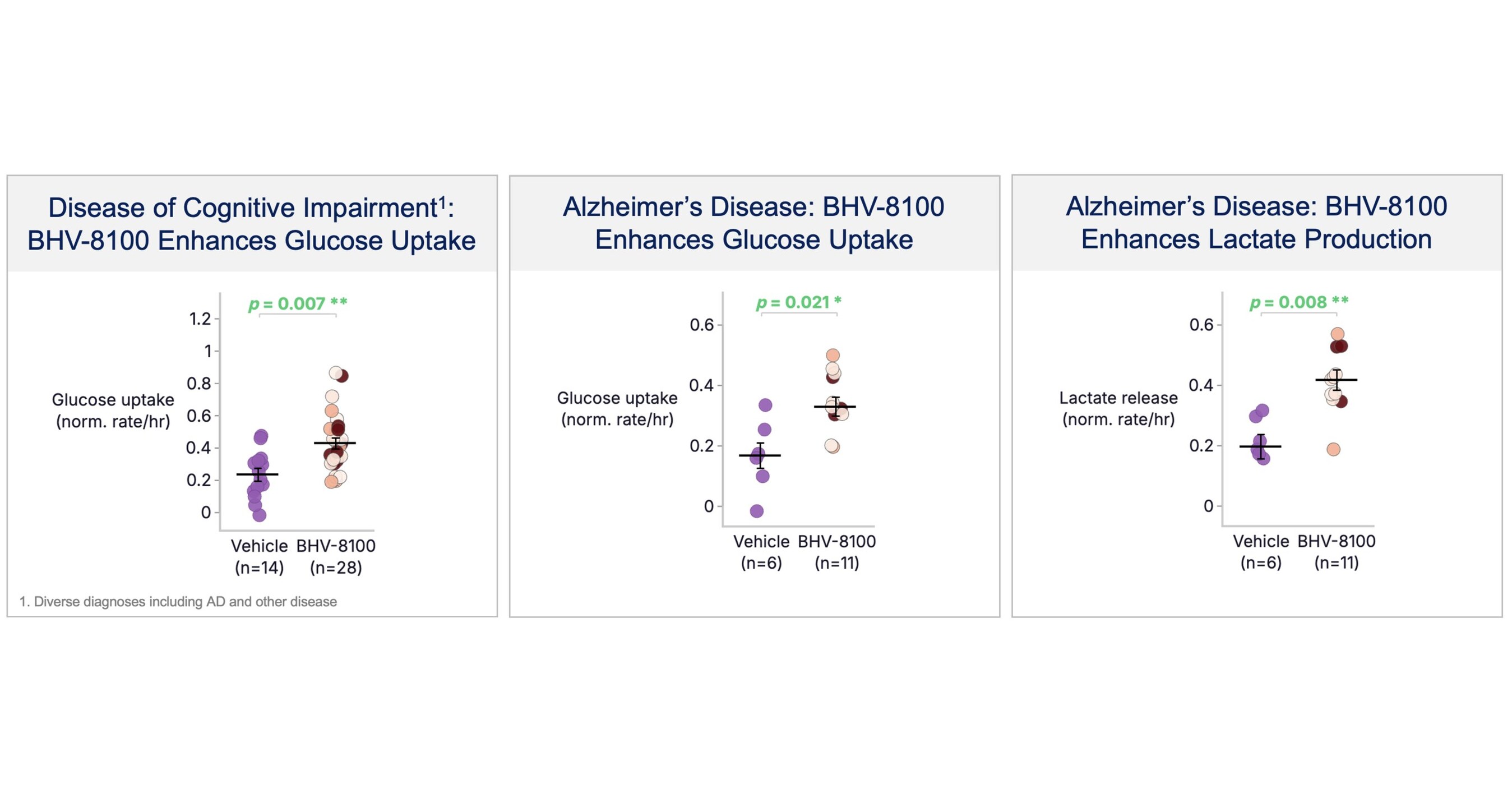

Biohaven Initiates First-in-Human Dosing for BHV-8100, a Novel PKM2 Modulator

- First-in-Human Dosing Initiated: Biohaven has announced the initiation of first-in-human dosing for BHV-8100, an oral PKM2 modulator aimed at treating various metabolic and immune-related diseases, marking a significant advancement in the company's innovative drug development efforts.

- Potential Therapeutic Breakthrough: BHV-8100 aims to correct energy deficits by modulating PKM2, improving bioenergetics in patients with neurodegenerative and retinal diseases, potentially offering hope to millions, particularly in the fields of Alzheimer's and retinal disorders.

- Clinical Data Support: Biohaven's collaboration with Bexorg's BrainEx platform utilizes human brain testing to confirm BHV-8100's target pharmacology and pharmacokinetics, ensuring its efficacy and safety in clinical trials.

- Significant Market Potential: Alzheimer's disease affects over 6.5 million Americans with annual treatment costs exceeding $300 billion, and BHV-8100 is poised to fill a gap in the retinal disease market, projected to exceed $15 billion globally by 2030, highlighting its substantial commercial potential.

See More

Biohaven Initiates First-in-Human Study for BHV-8100, a Novel PKM2 Modulator

- First-in-Human Study Initiated: Biohaven has announced the initiation of the first-in-human study for BHV-8100, an oral, brain-penetrant PKM2 modulator aimed at treating systemic and central nervous system disorders, marking a significant advancement in the company's innovative drug development.

- Favorable Pharmacokinetics: Preliminary data indicates that BHV-8100 demonstrates a favorable pharmacokinetic profile in healthy participants, supporting a convenient once-daily dosing regimen and showing good tolerability at projected therapeutic exposures, highlighting its potential for clinical application.

- Metabolic Function Restoration: BHV-8100 exhibits a threefold improvement in glucose utilization in brain tissues from Alzheimer's patients, indicating its effectiveness in reversing metabolic dysfunction, which may provide new hope for treating neurodegenerative diseases.

- Broad Indication Potential: The drug shows significant benefits across various preclinical models, including restoring metabolic deficits, reducing inflammation, and preventing neurodegeneration, suggesting its wide applicability in neurology, ophthalmology, and immunology.

See More

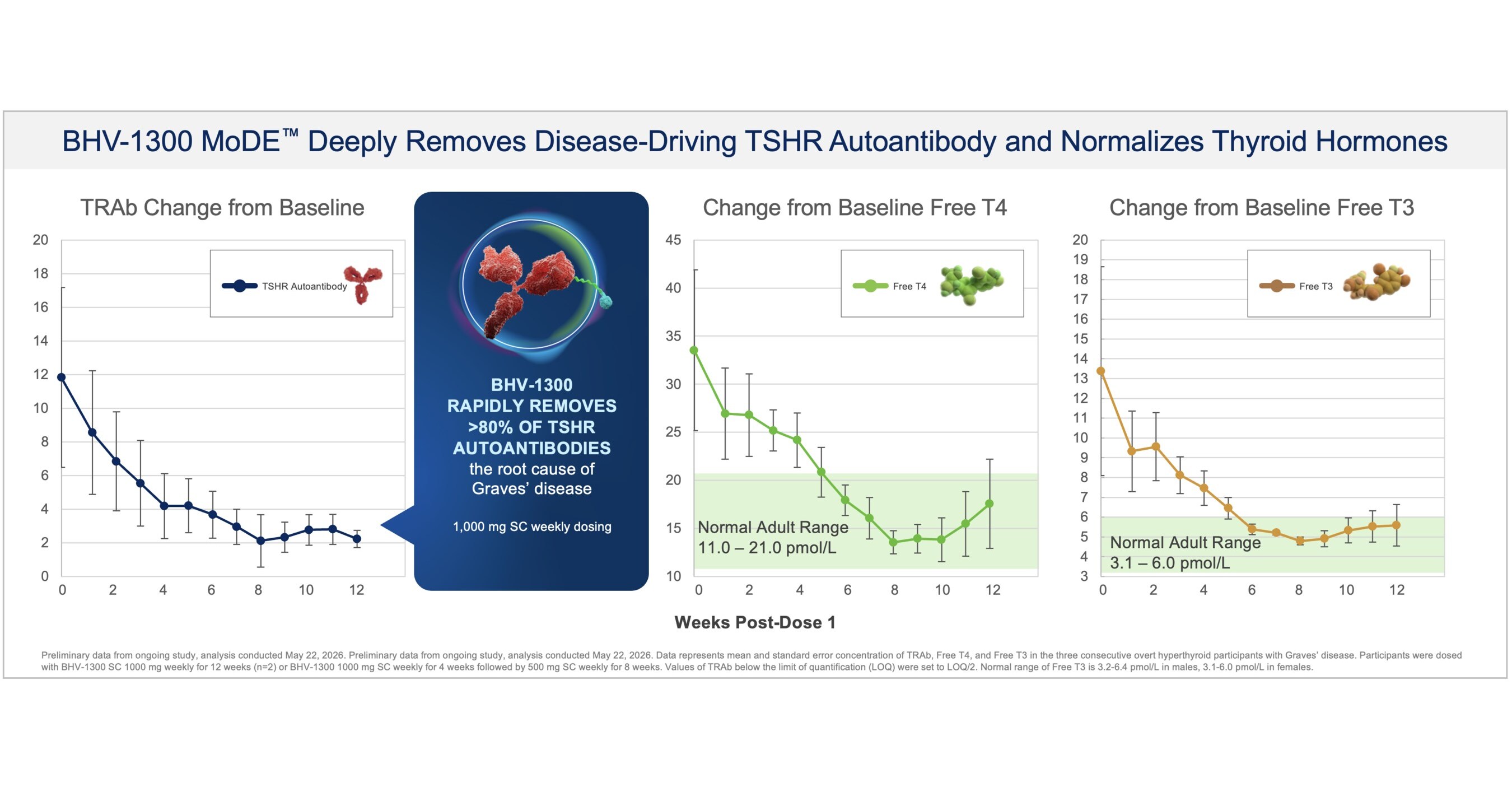

Biohaven Reports New Clinical Data on Innovative Therapies

- Clinical Data Release: Biohaven presented new patient data on its BHV-1300 MoDE degrader for Graves' disease and BHV-1400 TRAP degrader for IgA nephropathy at the Yale Innovation Summit, showcasing the potential of its therapies to transform treatment options for autoimmune diseases.

- R&D Day Event: The data was unveiled during Biohaven's 2026 R&D and Analyst Day at Yale School of Management, highlighting the company's innovative capabilities in the biopharmaceutical sector and its focus on autoimmune diseases, which may attract increased investor interest.

- Platform Technology Advantage: Biohaven's proprietary MoDE™ and TRAP™ degrader platforms demonstrate unique drug development capabilities that could provide a competitive edge in future clinical trials, enhancing its position in the biopharmaceutical market.

- Broad Market Prospects: With the rising number of autoimmune disease patients, Biohaven's new therapies are poised to address unmet medical needs, further driving the company's expansion and revenue growth in the global market.

See More

Biohaven's New Therapies Show Significant Antibody Reduction

- Efficacy of BHV-1300: In a 12-week study, patients with Graves' disease receiving 1000 mg of BHV-1300 weekly showed an average reduction of over 80% in pathogenic TSHR-IgG1 antibodies, indicating the drug's potential as a first effective disease-modifying therapy for Graves' disease.

- Rapid Normalization of Thyroid Hormones: Patients experienced normalization of T4 levels within a median of 3 weeks and T3 levels within 5 weeks after the first administration, demonstrating BHV-1300's ability to quickly restore thyroid function, addressing a critical unmet need for effective treatments.

- Rapid Action of BHV-1400: In patients with IgA nephropathy, BHV-1400 achieved over 60% mean reduction in Gd-IgA1 antibodies within 48 hours and 70% within one month, showcasing its rapid and profound impact on treating IgAN.

- Good Safety Profile: Both BHV-1300 and BHV-1400 showed no serious adverse events during clinical trials, with most adverse reactions being mild and self-resolving, indicating a competitive safety advantage that may encourage more patients to participate in upcoming Phase 3 trials.

See More

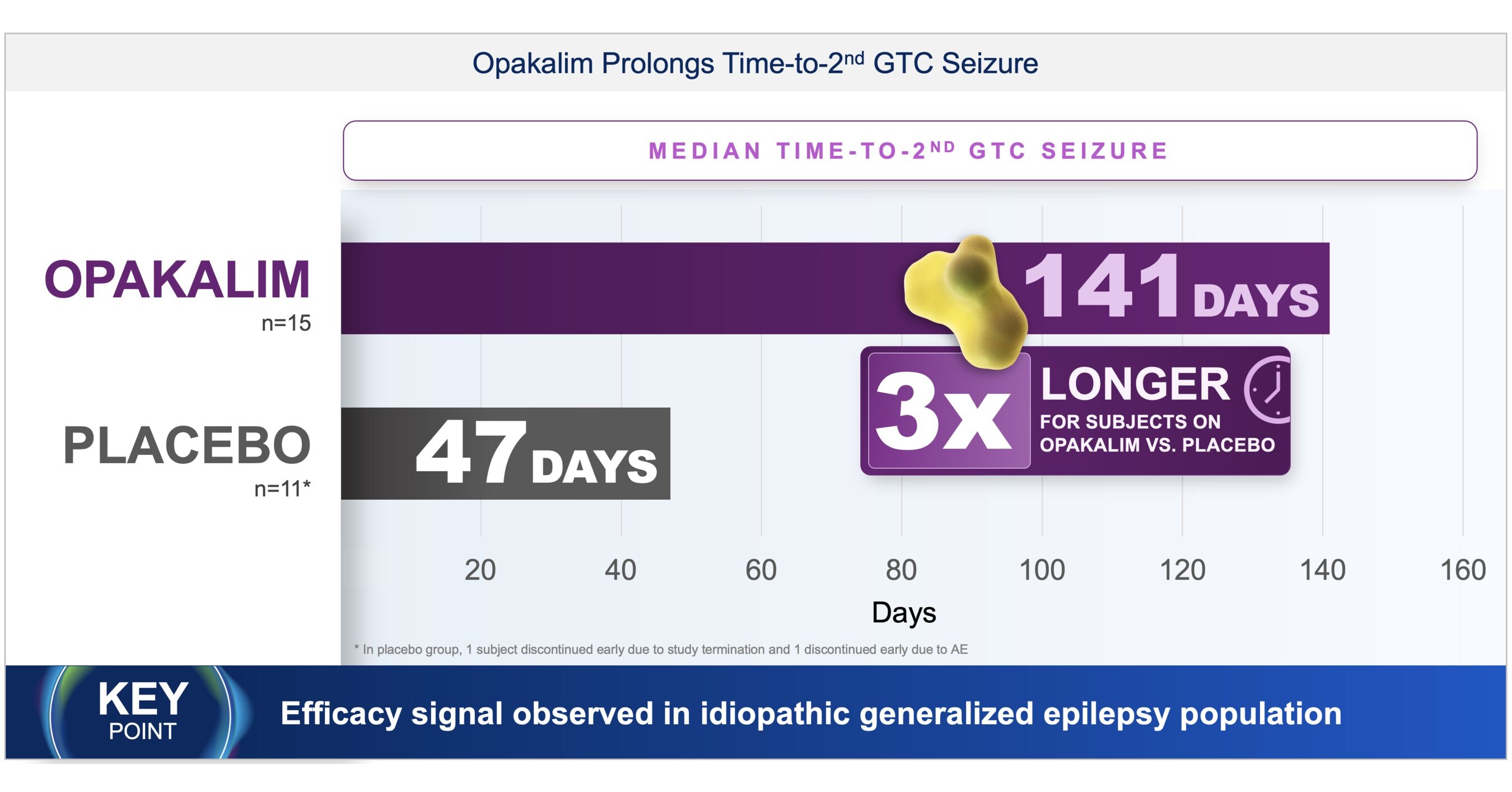

Biohaven Reports New Data on Opakalim for Epilepsy Treatment

- Clinical Trial Progress: Biohaven will present new data on Opakalim's Phase 2/3 studies for focal epilepsy at its upcoming R&D Day, indicating its potential to provide more effective treatment options for patients in seizure control.

- Safety Advantages: Opakalim demonstrated zero rates of somnolence, dizziness, and fatigue in a small proof-of-concept study, suggesting that its selective Kv7.2/7.3 activation mechanism may offer better tolerability, enhancing patients' quality of life.

- Patient Case Update: A 9-year-old patient with KCNQ2-DEE showed seizure control after transitioning to Opakalim, highlighting the drug's efficacy in treatment-resistant epilepsy patients and supporting its clinical application potential.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 randomized double-blind studies in the second half of 2026, aiming to support Opakalim's registration and advance its commercialization efforts.

See More

Valuation Analysis of U.S. Small-Cap Healthcare Stocks

- Valuation Score Overview: Seeking Alpha's valuation grade assesses healthcare stocks' relative price attractiveness within their sector using metrics like P/E, PEG, and EV/Sales, aiding investors in identifying potential investment opportunities.

- Market Performance Highlight: Among healthcare stocks with market caps between $300M and $2B, Biohaven (BHVN) is rated as the most expensive, indicating its high valuation level in the market, which may influence investor purchasing decisions.

- Other High-Valuation Companies: Companies like Greenwich LifeSciences (GLSI), HealthStream (HSTM), and Immix Biopharma (IMMX) received F grades, suggesting they are viewed as high-risk investments in the current market environment, potentially leading to investor caution.

- Financing Dynamics: Immix Biopharma recently priced a $150M stock offering at $8.94 per share, and despite valuation pressures, its stock rose following the release of mid-stage trial data for AL amyloidosis therapy, indicating market interest in its potential.

See More

Biohaven Initiates First-in-Human Dosing for BHV-8100, a Novel PKM2 Modulator

- First-in-Human Dosing Initiated: Biohaven has announced the initiation of first-in-human dosing for BHV-8100, an oral PKM2 modulator aimed at treating various metabolic and immune-related diseases, marking a significant advancement in the company's innovative drug development efforts.

- Potential Therapeutic Breakthrough: BHV-8100 aims to correct energy deficits by modulating PKM2, improving bioenergetics in patients with neurodegenerative and retinal diseases, potentially offering hope to millions, particularly in the fields of Alzheimer's and retinal disorders.

- Clinical Data Support: Biohaven's collaboration with Bexorg's BrainEx platform utilizes human brain testing to confirm BHV-8100's target pharmacology and pharmacokinetics, ensuring its efficacy and safety in clinical trials.

- Significant Market Potential: Alzheimer's disease affects over 6.5 million Americans with annual treatment costs exceeding $300 billion, and BHV-8100 is poised to fill a gap in the retinal disease market, projected to exceed $15 billion globally by 2030, highlighting its substantial commercial potential.

See More

Biohaven Initiates First-in-Human Study for BHV-8100, a Novel PKM2 Modulator

- First-in-Human Study Initiated: Biohaven has announced the initiation of the first-in-human study for BHV-8100, an oral, brain-penetrant PKM2 modulator aimed at treating systemic and central nervous system disorders, marking a significant advancement in the company's innovative drug development.

- Favorable Pharmacokinetics: Preliminary data indicates that BHV-8100 demonstrates a favorable pharmacokinetic profile in healthy participants, supporting a convenient once-daily dosing regimen and showing good tolerability at projected therapeutic exposures, highlighting its potential for clinical application.

- Metabolic Function Restoration: BHV-8100 exhibits a threefold improvement in glucose utilization in brain tissues from Alzheimer's patients, indicating its effectiveness in reversing metabolic dysfunction, which may provide new hope for treating neurodegenerative diseases.

- Broad Indication Potential: The drug shows significant benefits across various preclinical models, including restoring metabolic deficits, reducing inflammation, and preventing neurodegeneration, suggesting its wide applicability in neurology, ophthalmology, and immunology.

See More

Biohaven Reports New Clinical Data on Innovative Therapies

- Clinical Data Release: Biohaven presented new patient data on its BHV-1300 MoDE degrader for Graves' disease and BHV-1400 TRAP degrader for IgA nephropathy at the Yale Innovation Summit, showcasing the potential of its therapies to transform treatment options for autoimmune diseases.

- R&D Day Event: The data was unveiled during Biohaven's 2026 R&D and Analyst Day at Yale School of Management, highlighting the company's innovative capabilities in the biopharmaceutical sector and its focus on autoimmune diseases, which may attract increased investor interest.

- Platform Technology Advantage: Biohaven's proprietary MoDE™ and TRAP™ degrader platforms demonstrate unique drug development capabilities that could provide a competitive edge in future clinical trials, enhancing its position in the biopharmaceutical market.

- Broad Market Prospects: With the rising number of autoimmune disease patients, Biohaven's new therapies are poised to address unmet medical needs, further driving the company's expansion and revenue growth in the global market.

See More

Biohaven's New Therapies Show Significant Antibody Reduction

- Efficacy of BHV-1300: In a 12-week study, patients with Graves' disease receiving 1000 mg of BHV-1300 weekly showed an average reduction of over 80% in pathogenic TSHR-IgG1 antibodies, indicating the drug's potential as a first effective disease-modifying therapy for Graves' disease.

- Rapid Normalization of Thyroid Hormones: Patients experienced normalization of T4 levels within a median of 3 weeks and T3 levels within 5 weeks after the first administration, demonstrating BHV-1300's ability to quickly restore thyroid function, addressing a critical unmet need for effective treatments.

- Rapid Action of BHV-1400: In patients with IgA nephropathy, BHV-1400 achieved over 60% mean reduction in Gd-IgA1 antibodies within 48 hours and 70% within one month, showcasing its rapid and profound impact on treating IgAN.

- Good Safety Profile: Both BHV-1300 and BHV-1400 showed no serious adverse events during clinical trials, with most adverse reactions being mild and self-resolving, indicating a competitive safety advantage that may encourage more patients to participate in upcoming Phase 3 trials.

See More

Biohaven Reports New Data on Opakalim for Epilepsy Treatment

- Clinical Trial Progress: Biohaven will present new data on Opakalim's Phase 2/3 studies for focal epilepsy at its upcoming R&D Day, indicating its potential to provide more effective treatment options for patients in seizure control.

- Safety Advantages: Opakalim demonstrated zero rates of somnolence, dizziness, and fatigue in a small proof-of-concept study, suggesting that its selective Kv7.2/7.3 activation mechanism may offer better tolerability, enhancing patients' quality of life.

- Patient Case Update: A 9-year-old patient with KCNQ2-DEE showed seizure control after transitioning to Opakalim, highlighting the drug's efficacy in treatment-resistant epilepsy patients and supporting its clinical application potential.

- Future Outlook: Biohaven is on track to announce top-line results from two pivotal Phase 2/3 randomized double-blind studies in the second half of 2026, aiming to support Opakalim's registration and advance its commercialization efforts.

See More