Firefly Aerospace Rated Buy by B. Riley, Stock Rises

Firefly Aerospace's stock surged by 16.61% as it crossed above the 5-day SMA, reflecting strong investor confidence.

B. Riley Securities has issued a Buy rating for Firefly Aerospace, highlighting its leadership in space exploration and a significant $1.29 billion backlog. Analysts noted the company's recent achievements, including being the first commercial entity to achieve a soft landing on the Moon, which solidifies its pioneering status in commercial spaceflight. The $855 million acquisition of SciTec is expected to enhance Firefly's capabilities in AI ground processing and potential space-based missile detection, further boosting its competitiveness in the defense sector.

The optimistic outlook from analysts, with a price target of $60, suggests that Firefly Aerospace is well-positioned for growth as NASA increases its lunar exploration budget, indicating a strong growth trajectory for the company.

Trade with 70% Backtested Accuracy

Analyst Views on FLY

About FLY

About the author

Linde's Strategic Positioning with SpaceX's IPO

- Market Opportunity: Linde's space business is rapidly growing, with expectations that SpaceX's IPO could double its commercial aerospace business to over $1 billion, highlighting its significance in emerging markets.

- Investment Expansion: Linde is investing $100 million in a new plant in Texas to enhance its gas supply capabilities for SpaceX, ensuring timely deliveries and strengthening its competitive position in the space industry.

- Historical Legacy: Founded in 1879, Linde has over 60 years of experience in the space sector, contributing to key missions from the Apollo program to Artemis II, showcasing its deep-rooted involvement in aerospace.

- Future Outlook: With SpaceX planning to significantly increase launch frequencies in the coming years, Linde anticipates benefiting from this trend, further solidifying its market position as an indispensable gas supplier in the space industry.

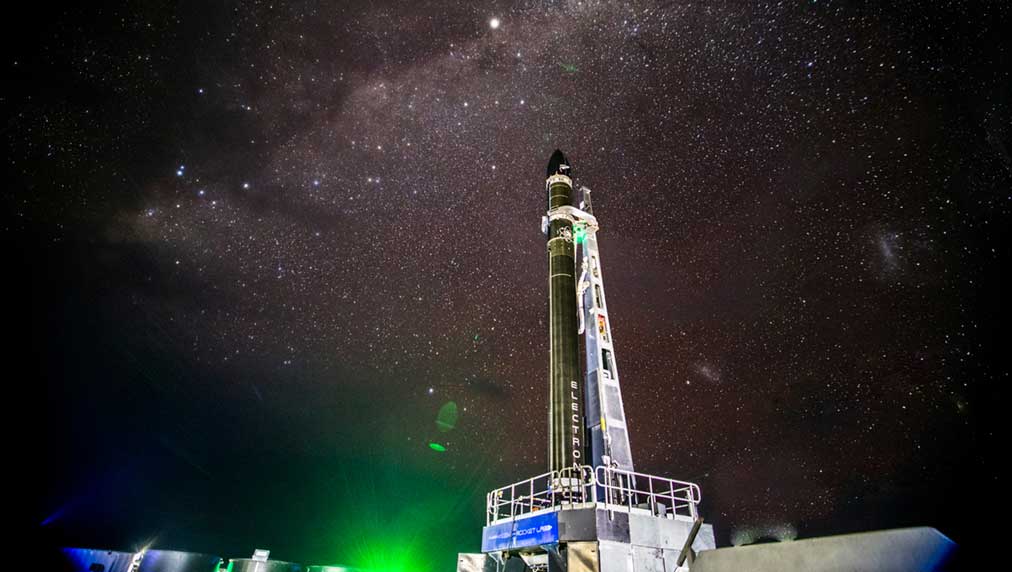

Rocket Lab Shares Hit Record High Following Strong Q1 Results and Major Launch Deal

- Strong Earnings Beat: Rocket Lab reported $136.7 million in Q1 revenue, exceeding FactSet's estimate of $132.1 million, indicating robust performance in the space economy and likely driving further stock price increases.

- Significant Backlog Growth: The company's backlog doubled year-over-year to $2.2 billion, reflecting surging demand for space systems and satellites, particularly fueled by President Trump's Golden Dome project and NASA's Artemis missions.

- Major Contract Signed: Rocket Lab secured its largest contract ever with a confidential customer for its Neutron and Electron rockets, solidifying its market leadership and laying the groundwork for future revenue growth.

- Acquisition Strategy: The company announced the acquisition of space robotics maker Motiv Space Systems, aimed at enhancing its technological capabilities and market competitiveness to meet the escalating demand in the space economy.

Rocket Lab Stock Soars 30% to Record High Following Strong Earnings and Major Launch Deal

- Revenue Beat: Rocket Lab reported first-quarter revenue of $136.7 million, exceeding FactSet's estimate of $132.1 million, indicating robust performance in its space systems business and likely driving further stock price increases.

- Historic Contract: The company signed its largest contract ever with a confidential customer for its Neutron and Electron rockets, which is expected to provide strong support for future revenue growth.

- Backlog Surge: Rocket Lab's backlog more than doubled from $110 million a year ago to $2.2 billion, reflecting a dramatic increase in demand for space economy services, especially with SpaceX's upcoming IPO.

- Optimistic Outlook: The company anticipates second-quarter revenue between $225 million and $240 million, surpassing Wall Street's estimate of $207.5 million, showcasing strong market demand and growth potential.

Rocket Lab Reports Earnings, Stock Breaks New Ground

- Earnings Release: Rocket Lab released its latest earnings report late Thursday, indicating ongoing growth in the aerospace launch services sector, although specific financial figures have yet to be disclosed, the market response has been positive.

- Stock Performance: RKLB stock has recently formed a stable base and successfully cleared a key entry point, suggesting increased investor confidence in the company's future growth, which may attract more capital inflow.

- Market Outlook: With the rapid development of the aerospace industry, Rocket Lab's business model and technological innovations position it favorably in the competitive landscape, expected to further drive revenue growth and market share expansion.

- Investor Interest: Analysts maintain an optimistic view on Rocket Lab's prospects, believing that its financial performance and market strategies will yield long-term returns for shareholders, drawing increased attention from institutional investors.

Starfighters Space Hires Blue Origin Executives to Boost Operations

- Executive Appointments: Starfighters Space (NYSE:FJET) has appointed two senior leaders from Blue Origin's New Glenn program, Jose Arias as VP of Space Operations and Catrina L. Medeiros as Director of STARLAUNCH Operations, aiming to enhance operational efficiency and market competitiveness.

- Integration Cycle Reduction: Arias's achievement of compressing integration cycles from 76 days to 13 at Blue Origin will directly enhance Starfighters' capability in high-frequency mission execution, thereby improving its operational effectiveness in the commercial space sector.

- Strategic Partnerships: The executive hires coincide with ongoing collaborations with GE Aerospace, Blackstar Orbital, and Mu-G Technologies, indicating the company's proactive approach to technology and market expansion, which strengthens its influence in the aerospace industry.

- Market Dynamics: Amid SpaceX's impending IPO, space companies are reassessing their talent and capital allocations, and Starfighters' executive recruitment is viewed as a crucial move to gain a competitive edge in a rapidly evolving market.

Firefly Aerospace Rated Buy by B. Riley, Stock Rises

- Market Leadership: B. Riley Securities' Buy rating for Firefly Aerospace (FLY) underscores the company's leadership in space exploration, with analysts highlighting its achievement as the first commercial entity to achieve a soft landing on the Moon, solidifying its status as a pioneer in commercial spaceflight.

- Growth Potential: FLY boasts a $1.29 billion backlog, and as NASA accelerates its lunar base construction, the company is poised for significant growth in its small- to medium-lift rocket launch business, further consolidating its market position.

- Technological Innovation: The $855 million acquisition of SciTec enhances FLY's AI ground processing and on-orbit capabilities, with analysts noting this could provide potential space-based missile detection and interception capabilities, boosting its competitiveness in the defense sector.

- Optimistic Outlook: With a price target of $60 set by B. Riley, FLY is expected to achieve revenues of $420 million to $450 million in the coming years as NASA increases its lunar exploration budget, indicating a strong growth trajectory.

Linde's Strategic Positioning with SpaceX's IPO

- Market Opportunity: Linde's space business is rapidly growing, with expectations that SpaceX's IPO could double its commercial aerospace business to over $1 billion, highlighting its significance in emerging markets.

- Investment Expansion: Linde is investing $100 million in a new plant in Texas to enhance its gas supply capabilities for SpaceX, ensuring timely deliveries and strengthening its competitive position in the space industry.

- Historical Legacy: Founded in 1879, Linde has over 60 years of experience in the space sector, contributing to key missions from the Apollo program to Artemis II, showcasing its deep-rooted involvement in aerospace.

- Future Outlook: With SpaceX planning to significantly increase launch frequencies in the coming years, Linde anticipates benefiting from this trend, further solidifying its market position as an indispensable gas supplier in the space industry.

Rocket Lab Shares Hit Record High Following Strong Q1 Results and Major Launch Deal

- Strong Earnings Beat: Rocket Lab reported $136.7 million in Q1 revenue, exceeding FactSet's estimate of $132.1 million, indicating robust performance in the space economy and likely driving further stock price increases.

- Significant Backlog Growth: The company's backlog doubled year-over-year to $2.2 billion, reflecting surging demand for space systems and satellites, particularly fueled by President Trump's Golden Dome project and NASA's Artemis missions.

- Major Contract Signed: Rocket Lab secured its largest contract ever with a confidential customer for its Neutron and Electron rockets, solidifying its market leadership and laying the groundwork for future revenue growth.

- Acquisition Strategy: The company announced the acquisition of space robotics maker Motiv Space Systems, aimed at enhancing its technological capabilities and market competitiveness to meet the escalating demand in the space economy.

Rocket Lab Stock Soars 30% to Record High Following Strong Earnings and Major Launch Deal

- Revenue Beat: Rocket Lab reported first-quarter revenue of $136.7 million, exceeding FactSet's estimate of $132.1 million, indicating robust performance in its space systems business and likely driving further stock price increases.

- Historic Contract: The company signed its largest contract ever with a confidential customer for its Neutron and Electron rockets, which is expected to provide strong support for future revenue growth.

- Backlog Surge: Rocket Lab's backlog more than doubled from $110 million a year ago to $2.2 billion, reflecting a dramatic increase in demand for space economy services, especially with SpaceX's upcoming IPO.

- Optimistic Outlook: The company anticipates second-quarter revenue between $225 million and $240 million, surpassing Wall Street's estimate of $207.5 million, showcasing strong market demand and growth potential.

Rocket Lab Reports Earnings, Stock Breaks New Ground

- Earnings Release: Rocket Lab released its latest earnings report late Thursday, indicating ongoing growth in the aerospace launch services sector, although specific financial figures have yet to be disclosed, the market response has been positive.

- Stock Performance: RKLB stock has recently formed a stable base and successfully cleared a key entry point, suggesting increased investor confidence in the company's future growth, which may attract more capital inflow.

- Market Outlook: With the rapid development of the aerospace industry, Rocket Lab's business model and technological innovations position it favorably in the competitive landscape, expected to further drive revenue growth and market share expansion.

- Investor Interest: Analysts maintain an optimistic view on Rocket Lab's prospects, believing that its financial performance and market strategies will yield long-term returns for shareholders, drawing increased attention from institutional investors.

Starfighters Space Hires Blue Origin Executives to Boost Operations

- Executive Appointments: Starfighters Space (NYSE:FJET) has appointed two senior leaders from Blue Origin's New Glenn program, Jose Arias as VP of Space Operations and Catrina L. Medeiros as Director of STARLAUNCH Operations, aiming to enhance operational efficiency and market competitiveness.

- Integration Cycle Reduction: Arias's achievement of compressing integration cycles from 76 days to 13 at Blue Origin will directly enhance Starfighters' capability in high-frequency mission execution, thereby improving its operational effectiveness in the commercial space sector.

- Strategic Partnerships: The executive hires coincide with ongoing collaborations with GE Aerospace, Blackstar Orbital, and Mu-G Technologies, indicating the company's proactive approach to technology and market expansion, which strengthens its influence in the aerospace industry.

- Market Dynamics: Amid SpaceX's impending IPO, space companies are reassessing their talent and capital allocations, and Starfighters' executive recruitment is viewed as a crucial move to gain a competitive edge in a rapidly evolving market.

Firefly Aerospace Rated Buy by B. Riley, Stock Rises

- Market Leadership: B. Riley Securities' Buy rating for Firefly Aerospace (FLY) underscores the company's leadership in space exploration, with analysts highlighting its achievement as the first commercial entity to achieve a soft landing on the Moon, solidifying its status as a pioneer in commercial spaceflight.

- Growth Potential: FLY boasts a $1.29 billion backlog, and as NASA accelerates its lunar base construction, the company is poised for significant growth in its small- to medium-lift rocket launch business, further consolidating its market position.

- Technological Innovation: The $855 million acquisition of SciTec enhances FLY's AI ground processing and on-orbit capabilities, with analysts noting this could provide potential space-based missile detection and interception capabilities, boosting its competitiveness in the defense sector.

- Optimistic Outlook: With a price target of $60 set by B. Riley, FLY is expected to achieve revenues of $420 million to $450 million in the coming years as NASA increases its lunar exploration budget, indicating a strong growth trajectory.