Nvidia Unveils 2026 AI Plans at GTC

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Mar 16 2026

0mins

Source: Fool

- AI Infrastructure Investment: At the GTC conference in San Jose, Nvidia anticipates over $600 billion in AI infrastructure spending by 2026, which is expected to drive vertical integration from chips to full AI systems, further solidifying its leadership in the AI market.

- Meta Layoff Plans: Meta is planning to cut 20% of its workforce to offset substantial AI infrastructure costs, aiming to achieve savings through increased use of AI agents and assistance for human workers, thereby enhancing operational efficiency and profitability.

- Tesla Semiconductor Manufacturing: CEO Elon Musk announced the imminent launch of Tesla's in-house semiconductor manufacturing, which is expected to boost production capacity and reduce reliance on external suppliers, enhancing the company's technological autonomy.

- Market Volatility Impact: The S&P 500 fell 1.6% last week due to turmoil from the Middle East conflict, but Goldman Sachs predicts a potential rebound to 7,600 points by the end of 2026 driven by rising corporate earnings, indicating the market's underlying recovery potential.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy META?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on META

Wall Street analysts forecast META stock price to rise

44 Analyst Rating

37 Buy

6 Hold

1 Sell

Strong Buy

Current: 635.290

Low

655.15

Averages

824.71

High

1117

Current: 635.290

Low

655.15

Averages

824.71

High

1117

About META

Meta Platforms, Inc. is building human connections, powered by artificial intelligence and immersive technologies. The Company's products enable people to connect and share with friends and family through mobile devices, personal computers, virtual reality (VR) and mixed reality (MR) headsets, augmented reality (AR), and wearables. It also helps people discover and learn about what is going on in the world around them, enabling people to share their experiences, ideas, photos, videos, and other content with audiences ranging from their closest family members and friends to the public at large. The Company's segments include Family of Apps (FoA) and Reality Labs (RL). FoA segment includes Facebook, Instagram, Messenger, WhatsApp and Threads. RL segment includes its virtual, augmented, and mixed reality related consumer hardware, software and content. Its product offerings in VR include its Meta Quest devices, as well as software and content available through the Meta Horizon Store.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Meta Platforms Stock Cheap Yet Growing Rapidly

- Stock Performance: Meta Platforms' stock is currently down 20% from its all-time high in July 2025, indicating a lack of investor enthusiasm despite the broader market reaching new highs.

- Revenue Growth: In Q1 2026, Meta reported a 33% year-over-year revenue increase, primarily driven by rising ad impressions and prices, showcasing its strong performance in the advertising sector.

- Valuation Advantage: Trading at less than 20 times forward earnings, Meta is cheaper than the S&P 500's 21.8 times, highlighting its attractive valuation amidst rapid growth, appealing to value investors.

- AI Strategy: Meta aims to leverage AI technology in its products, with plans to launch a superintelligence platform, which, if successful, could significantly enhance its market position and drive future growth.

See More

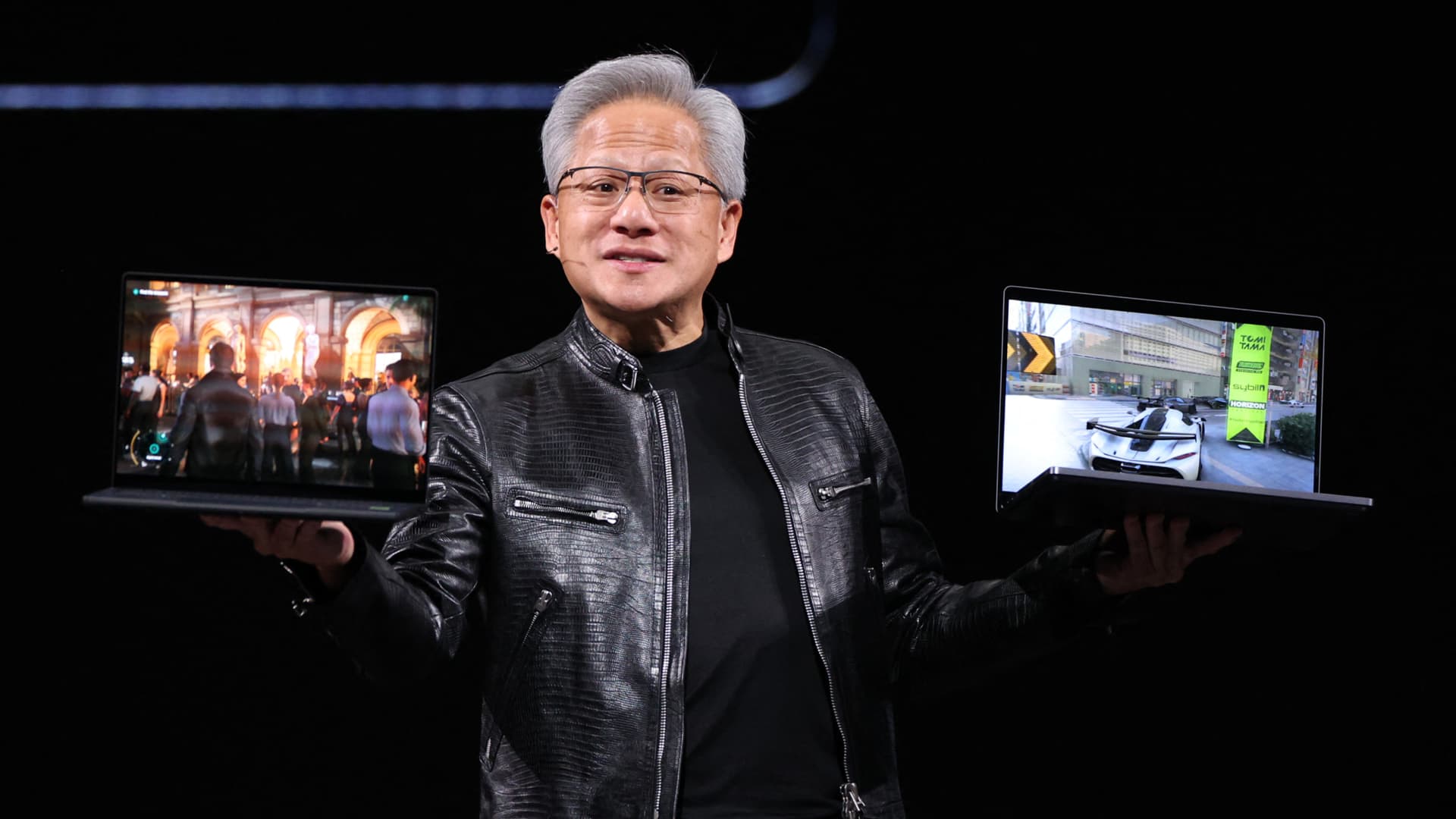

Nvidia Unveils N1X Processor, Set to Transform Personal Computing Market

- Processor Launch: Nvidia unveiled the N1X processor developed in collaboration with Microsoft at Computex in Taipei, marking its entry into the personal computer market with plans to release over 30 laptops and 10 desktops, significantly enhancing its competitive edge.

- Technological Innovation: The new processor integrates Nvidia's Blackwell GPU with an Arm-based N1X CPU designed by MediaTek, manufactured using TSMC's 3-nanometer technology, which is expected to drive a shift in the PC industry towards Arm architecture, challenging traditional x86 processors from Intel and AMD.

- Market Potential: Nvidia anticipates the PC processor market will reach $200 billion, and the introduction of the N1X processor not only addresses the high-performance computing needs of AI workloads but also reinforces the company's leadership position in the rapidly growing AI market.

- Energy Efficiency Improvement: Nvidia's Vera CPU is now in full production, capable of generating data center tokens 1.8 times faster than x86, showcasing exceptional energy efficiency and performance, positioning it as a key growth driver for future AI factories.

See More

Broadcom Shares Hit All-Time High, Market Cap Exceeds $2.1 Trillion

- Stock Surge: Broadcom's shares jumped nearly 5% on Friday to close at $446.77, marking an all-time high and pushing its market capitalization past $2.1 trillion, reflecting strong market confidence in its future growth prospects.

- AI Revenue Growth: In fiscal Q1 2026, Broadcom's AI revenue reached $8.4 billion, up 106% year-over-year, driving semiconductor solutions revenue to a record $12.5 billion, indicating robust performance and rapid market demand in the AI sector.

- Strong Cash Flow: The company generated $8.0 billion in free cash flow in Q1, representing 41% of revenue, and authorized a $10 billion stock buyback, showcasing its strong profitability and commitment to returning capital to shareholders.

- Valuation Risks: Despite Broadcom's significant growth potential, its price-to-earnings ratio stands at approximately 87, prompting investors to carefully assess the sustainability of future performance to avoid stock price volatility due to potential customer spending slowdowns.

See More

Broadcom's AI Revenue Soars 106%, Market Cap Exceeds $2.1 Trillion

- AI Revenue Surge: Broadcom's AI revenue reached $8.4 billion in fiscal Q1 2026, marking a 106% year-over-year increase that surpassed company guidance, driving semiconductor solutions revenue to a record $12.5 billion, up 52%, and total revenue to $19.3 billion, up 29%.

- Future Growth Outlook: Management anticipates AI chip revenue exceeding $100 billion by 2027, with clients including Google, Meta, and OpenAI, highlighting Broadcom's significant potential and strategic importance in the AI market.

- Cash Flow and Buybacks: Broadcom reported free cash flow of $8.0 billion in fiscal Q1 2026, representing 41% of revenue, and returned $10.9 billion to shareholders through stock buybacks, demonstrating the company's strong financial health.

- Customer Concentration Risk: Broadcom's top five customers accounted for approximately 50% of its revenue in Q1, and while these clients have driven rapid growth, any pushback on pricing or slowdown in spending could negatively impact the company's performance.

See More

SpaceX Poised to Become Next Trillion-Dollar Company

- New Member of Trillion-Dollar Club: SpaceX is planning an IPO in a few weeks with a target valuation of nearly $2 trillion, which, if achieved, would set a record for the largest IPO in history, showcasing its immense potential in the aerospace and tech sectors.

- Financial Challenges and Growth: Despite reporting a net loss of approximately $4.9 billion last year and over $12 billion in capital expenditures for its AI division, SpaceX's annual revenue has surged from $10 billion to $18 billion, indicating a mix of challenges and opportunities in its rapid growth.

- Rising Capital Expenditures: The company has seen capital expenditures exceeding $3 billion for its space operations and $4 billion for connectivity, with both areas experiencing rising investments over the past three years, reflecting its commitment to technological advancement.

- Investor Risk Assessment: While SpaceX may attract aggressive investors, its success hinges on achieving various technological goals, making it less suitable for conservative investors seeking stable returns.

See More

SpaceX IPO Could Make It the Next Trillion-Dollar Company

- Trillion-Dollar Club: In recent years, tech giants like Apple and Nvidia have surpassed $1 trillion in market value, with SpaceX planning an IPO in a few weeks aiming for a valuation close to $2 trillion, which would set a record for the largest IPO in history.

- Financial Challenges: While SpaceX's annual revenue surged from $10 billion in 2023 to $18 billion, its AI division incurred over $12 billion in capital expenditures last year, resulting in a net loss of approximately $4.9 billion, indicating that profitability remains a significant hurdle.

- Rising Capital Expenditures: SpaceX's capital expenditures for its space and connectivity units exceeded $3 billion and $4 billion respectively, with these figures rising over the past three years, highlighting the company's commitment to technological advancement and potential for future growth.

- Investor Risk Assessment: Although SpaceX's IPO is attracting aggressive investors, its success hinges on achieving various technological milestones, necessitating careful evaluation of the high-risk, high-reward nature of this investment opportunity.

See More

Meta Platforms Stock Cheap Yet Growing Rapidly

- Stock Performance: Meta Platforms' stock is currently down 20% from its all-time high in July 2025, indicating a lack of investor enthusiasm despite the broader market reaching new highs.

- Revenue Growth: In Q1 2026, Meta reported a 33% year-over-year revenue increase, primarily driven by rising ad impressions and prices, showcasing its strong performance in the advertising sector.

- Valuation Advantage: Trading at less than 20 times forward earnings, Meta is cheaper than the S&P 500's 21.8 times, highlighting its attractive valuation amidst rapid growth, appealing to value investors.

- AI Strategy: Meta aims to leverage AI technology in its products, with plans to launch a superintelligence platform, which, if successful, could significantly enhance its market position and drive future growth.

See More

Nvidia Unveils N1X Processor, Set to Transform Personal Computing Market

- Processor Launch: Nvidia unveiled the N1X processor developed in collaboration with Microsoft at Computex in Taipei, marking its entry into the personal computer market with plans to release over 30 laptops and 10 desktops, significantly enhancing its competitive edge.

- Technological Innovation: The new processor integrates Nvidia's Blackwell GPU with an Arm-based N1X CPU designed by MediaTek, manufactured using TSMC's 3-nanometer technology, which is expected to drive a shift in the PC industry towards Arm architecture, challenging traditional x86 processors from Intel and AMD.

- Market Potential: Nvidia anticipates the PC processor market will reach $200 billion, and the introduction of the N1X processor not only addresses the high-performance computing needs of AI workloads but also reinforces the company's leadership position in the rapidly growing AI market.

- Energy Efficiency Improvement: Nvidia's Vera CPU is now in full production, capable of generating data center tokens 1.8 times faster than x86, showcasing exceptional energy efficiency and performance, positioning it as a key growth driver for future AI factories.

See More

Broadcom Shares Hit All-Time High, Market Cap Exceeds $2.1 Trillion

- Stock Surge: Broadcom's shares jumped nearly 5% on Friday to close at $446.77, marking an all-time high and pushing its market capitalization past $2.1 trillion, reflecting strong market confidence in its future growth prospects.

- AI Revenue Growth: In fiscal Q1 2026, Broadcom's AI revenue reached $8.4 billion, up 106% year-over-year, driving semiconductor solutions revenue to a record $12.5 billion, indicating robust performance and rapid market demand in the AI sector.

- Strong Cash Flow: The company generated $8.0 billion in free cash flow in Q1, representing 41% of revenue, and authorized a $10 billion stock buyback, showcasing its strong profitability and commitment to returning capital to shareholders.

- Valuation Risks: Despite Broadcom's significant growth potential, its price-to-earnings ratio stands at approximately 87, prompting investors to carefully assess the sustainability of future performance to avoid stock price volatility due to potential customer spending slowdowns.

See More

Broadcom's AI Revenue Soars 106%, Market Cap Exceeds $2.1 Trillion

- AI Revenue Surge: Broadcom's AI revenue reached $8.4 billion in fiscal Q1 2026, marking a 106% year-over-year increase that surpassed company guidance, driving semiconductor solutions revenue to a record $12.5 billion, up 52%, and total revenue to $19.3 billion, up 29%.

- Future Growth Outlook: Management anticipates AI chip revenue exceeding $100 billion by 2027, with clients including Google, Meta, and OpenAI, highlighting Broadcom's significant potential and strategic importance in the AI market.

- Cash Flow and Buybacks: Broadcom reported free cash flow of $8.0 billion in fiscal Q1 2026, representing 41% of revenue, and returned $10.9 billion to shareholders through stock buybacks, demonstrating the company's strong financial health.

- Customer Concentration Risk: Broadcom's top five customers accounted for approximately 50% of its revenue in Q1, and while these clients have driven rapid growth, any pushback on pricing or slowdown in spending could negatively impact the company's performance.

See More

SpaceX Poised to Become Next Trillion-Dollar Company

- New Member of Trillion-Dollar Club: SpaceX is planning an IPO in a few weeks with a target valuation of nearly $2 trillion, which, if achieved, would set a record for the largest IPO in history, showcasing its immense potential in the aerospace and tech sectors.

- Financial Challenges and Growth: Despite reporting a net loss of approximately $4.9 billion last year and over $12 billion in capital expenditures for its AI division, SpaceX's annual revenue has surged from $10 billion to $18 billion, indicating a mix of challenges and opportunities in its rapid growth.

- Rising Capital Expenditures: The company has seen capital expenditures exceeding $3 billion for its space operations and $4 billion for connectivity, with both areas experiencing rising investments over the past three years, reflecting its commitment to technological advancement.

- Investor Risk Assessment: While SpaceX may attract aggressive investors, its success hinges on achieving various technological goals, making it less suitable for conservative investors seeking stable returns.

See More

SpaceX IPO Could Make It the Next Trillion-Dollar Company

- Trillion-Dollar Club: In recent years, tech giants like Apple and Nvidia have surpassed $1 trillion in market value, with SpaceX planning an IPO in a few weeks aiming for a valuation close to $2 trillion, which would set a record for the largest IPO in history.

- Financial Challenges: While SpaceX's annual revenue surged from $10 billion in 2023 to $18 billion, its AI division incurred over $12 billion in capital expenditures last year, resulting in a net loss of approximately $4.9 billion, indicating that profitability remains a significant hurdle.

- Rising Capital Expenditures: SpaceX's capital expenditures for its space and connectivity units exceeded $3 billion and $4 billion respectively, with these figures rising over the past three years, highlighting the company's commitment to technological advancement and potential for future growth.

- Investor Risk Assessment: Although SpaceX's IPO is attracting aggressive investors, its success hinges on achieving various technological milestones, necessitating careful evaluation of the high-risk, high-reward nature of this investment opportunity.

See More