Moody's Q1 2026 Earnings Call Highlights

Written by Emily J. Thompson, Senior Investment Analyst

Updated: Apr 22 2026

0mins

Source: seekingalpha

- Strong Revenue Growth: Moody's achieved an 8% revenue growth in Q1 2026 despite geopolitical volatility, demonstrating the company's resilience and robust business foundation, which is expected to continue driving future performance.

- Enhanced Profitability: The adjusted operating margin reached 53.2%, up 150 basis points year-over-year, reflecting effective cost management, while the adjusted diluted EPS stood at $4.33, bolstering investor confidence.

- Expanded Buyback Plan: Moody's raised its 2026 share buyback guidance to approximately $2.5 billion, indicating strong confidence in future cash flows and commitment to shareholder returns, further enhancing shareholder value.

- AI Integration Progress: Through Model Context Protocol integrations, Moody's licensed intelligence can now be accessed directly within enterprise AI environments, marking a forward-looking approach in technology innovation and market demand, strengthening direct relationships with customers.

Trade with 70% Backtested Accuracy

Stop guessing "Should I Buy MCO?" and start using high-conviction signals backed by rigorous historical data.

Sign up today to access powerful investing tools and make smarter, data-driven decisions.

Analyst Views on MCO

Wall Street analysts forecast MCO stock price to rise

10 Analyst Rating

8 Buy

2 Hold

0 Sell

Strong Buy

Current: 450.450

Low

526.00

Averages

586.50

High

660.00

Current: 450.450

Low

526.00

Averages

586.50

High

660.00

About MCO

Moody's Corporation is a global provider of integrated perspectives on risk that empowers organizations and investors to make decisions. The Company's segments include Moody's Analytics (MA) and Moody's Investors Service (MIS). MA segment comprises three interconnected businesses: Research & Insights, which provides credit research, economic analysis and scenario modeling used in investment and risk decisions; Data & Information, which is powered by the database on companies and credit and serves as a critical input to financial analysis and AI model development/risk assessment, and Decision Solutions, a set of cloud-based platforms embedding Moody's data and analytics directly into regulated banking, insurance and KYC workflows. MIS segment publishes credit ratings and provides assessment services on a range of debt obligations, programs and facilities, and the entities that issue such obligations in markets worldwide, including various corporate, and structured finance securities.

About the author

Emily J. Thompson

Emily J. Thompson, a Chartered Financial Analyst (CFA) with 12 years in investment research, graduated with honors from the Wharton School. Specializing in industrial and technology stocks, she provides in-depth analysis for Intellectia’s earnings and market brief reports.

Rising Energy Costs Impact Consumer Spending

- Increased Household Spending: Since the onset of the Iran War, the average American household has spent an additional $447.19 on energy costs, cumulatively costing nearly $60 billion, indicating heightened financial pressure on consumers that may lead to more cautious spending and impact economic growth.

- Surging Fuel Prices: Gasoline prices have surged over 47% since March, now averaging $4.39 per gallon, while diesel has risen to $5.52 per gallon, resulting in over $20 billion in additional consumer expenses, further straining household budgets.

- Declining Consumer Confidence: Although consumer spending rose by 0.5% from March to April, stagnant income growth and a personal savings rate that fell to 2.6% suggest that consumers are increasingly relying on credit and savings to maintain spending levels amid inflationary pressures.

- Pessimistic Future Outlook: Goldman Sachs anticipates that rising energy prices will continue to erode consumer purchasing power, particularly affecting lower-income households, which may lead to a further contraction in spending patterns and increase the risk of economic slowdown.

See More

Buffett's Investment Legacy Continues

- American Express Success: Buffett's investment in American Express since 1964, holding 22% of shares, has resulted in consistent profitability despite economic fluctuations, and is expected to continue generating substantial returns for Berkshire.

- Alphabet's Diversified Growth: Alphabet's annual revenue surged from $258 billion to nearly $403 billion over the past five years, with its core search engine and cloud services performing strongly, laying a solid foundation for future growth despite some businesses not yet being profitable.

- Apple's Market Leadership: With a market value exceeding $700 billion, Apple remains a significant holding for Berkshire, as its products and services continue to thrive, particularly in the services ecosystem, ensuring future growth potential.

- Coca-Cola's High-Profit Model: Coca-Cola operates with net profit margins in the mid-20% range and has consistently increased its dividends, earning the title of 'Dividend King', with a business model that relies on selling foundational syrups, ensuring stable cash flow and long-term investor returns.

See More

Greg Abel's First Quarter Report Reveals Investment Strategy

- Portfolio Adjustments: In his first quarterly report, Abel adjusted the $330 billion equity portfolio by adding positions in Delta Airlines and Macy's, while tripling the stake in Alphabet, indicating his proactive approach to high-conviction stocks while maintaining Buffett's investment style.

- Small Position Sell-Off: In the first quarter, Abel and his team sold out of 16 smaller positions, including Visa and Mastercard, which accounted for about a third of Berkshire's total holdings, demonstrating decisive action in optimizing the investment portfolio.

- Core Holdings Retained: Despite the significant sell-off, Abel retained core holdings such as Apple, American Express, and Coca-Cola, reflecting his respect for and continuation of the company's traditional investment strategies established by Buffett.

- Positive Market Reaction: Following the announcement of Abel's investment strategy, Berkshire Hathaway's stock ticked higher, reflecting market confidence in his management capabilities and further solidifying the company's position in the investment community.

See More

Berkshire Hathaway's Abel Restructures Equity Portfolio

- Portfolio Restructuring: Greg Abel cut 16 small positions in the first quarter, including long-held Visa and Mastercard, demonstrating a strategic focus on concentrated high-conviction stocks while maintaining Buffett's traditional investment style.

- New Investment Directions: Abel added positions in Delta Airlines and Macy's, and tripled the investment in Alphabet, indicating a strategy aligned with Buffett's tech stock preferences, which may attract younger investors.

- Increased Concentration: Excluding investments in Japan, Berkshire now holds only 29 positions, retaining Buffett favorites like Apple, American Express, and Coca-Cola, reflecting ongoing confidence in classic quality assets.

- Positive Market Reaction: Despite the reduction of about one-third of the portfolio, Berkshire's stock price rose following the announcement, indicating market approval of Abel's investment strategy and suggesting optimistic expectations for future performance.

See More

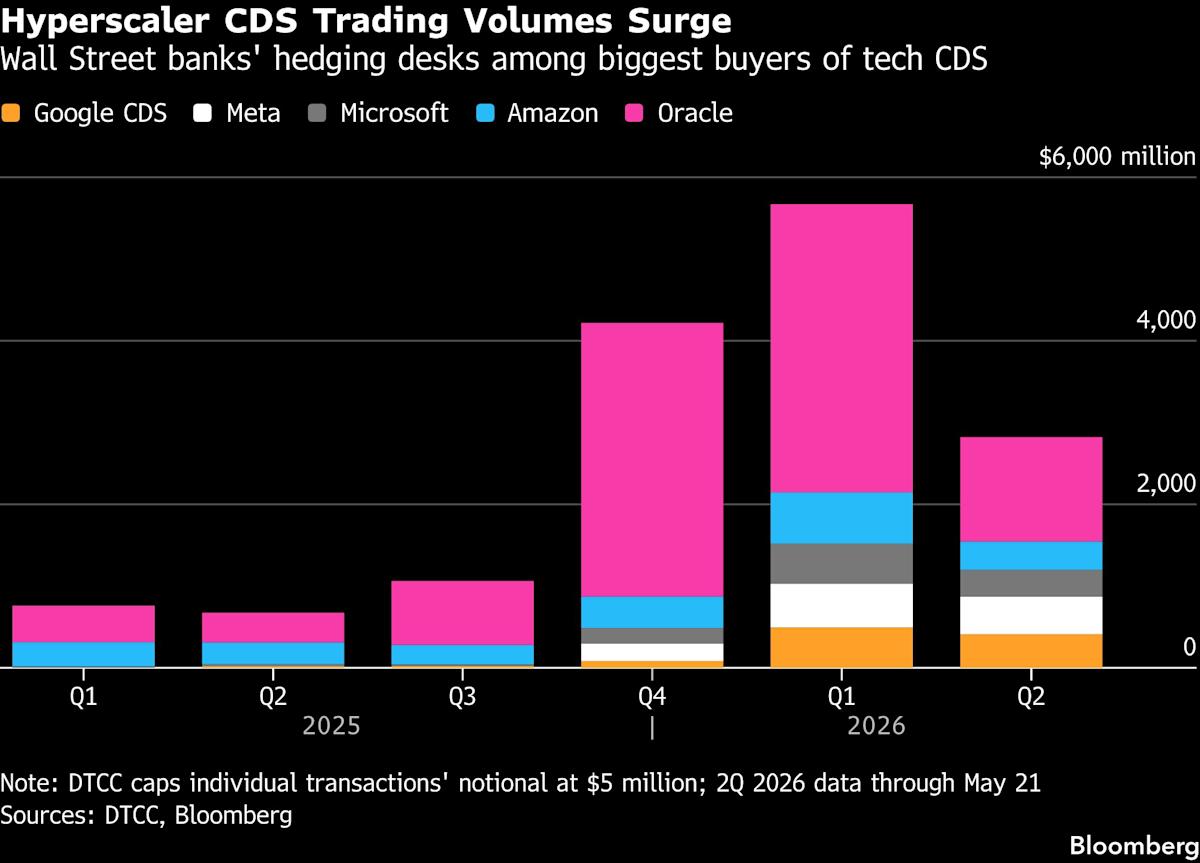

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Berkshire Hathaway's Major Portfolio Shake-Up Under New CEO

- Portfolio Restructuring: Berkshire Hathaway, under new CEO Greg Abel, has undergone its most active trading quarter in recent memory, completely selling out of several companies and increasing stakes in others, reflecting a thorough review of holdings and a strategic focus on high-conviction investments.

- Strong Performance of Apple: Apple (AAPL), as Berkshire's largest holding, continues to show robust cash flow and profit growth despite not heavily investing in AI, and its partnership with Google on the next generation of Siri indicates a solid market position, making it a likely choice for investors moving forward.

- Attractive Valuation of Moody's: Moody's (MCO) shares have fallen about 35% from their peak, now trading at a price-to-earnings ratio of 31, the lowest since early 2023, with analysts projecting an 11% annual earnings growth over the next three to five years, potentially presenting a classic buy-the-dip opportunity.

- Coca-Cola's Dividend King Status: Coca-Cola (KO), the only Dividend King on the list with over 50 consecutive years of dividend increases, currently offers a 2.6% yield, and while its valuation is somewhat high, the consistent dividend growth makes it a strong candidate for long-term investment.

See More

Rising Energy Costs Impact Consumer Spending

- Increased Household Spending: Since the onset of the Iran War, the average American household has spent an additional $447.19 on energy costs, cumulatively costing nearly $60 billion, indicating heightened financial pressure on consumers that may lead to more cautious spending and impact economic growth.

- Surging Fuel Prices: Gasoline prices have surged over 47% since March, now averaging $4.39 per gallon, while diesel has risen to $5.52 per gallon, resulting in over $20 billion in additional consumer expenses, further straining household budgets.

- Declining Consumer Confidence: Although consumer spending rose by 0.5% from March to April, stagnant income growth and a personal savings rate that fell to 2.6% suggest that consumers are increasingly relying on credit and savings to maintain spending levels amid inflationary pressures.

- Pessimistic Future Outlook: Goldman Sachs anticipates that rising energy prices will continue to erode consumer purchasing power, particularly affecting lower-income households, which may lead to a further contraction in spending patterns and increase the risk of economic slowdown.

See More

Buffett's Investment Legacy Continues

- American Express Success: Buffett's investment in American Express since 1964, holding 22% of shares, has resulted in consistent profitability despite economic fluctuations, and is expected to continue generating substantial returns for Berkshire.

- Alphabet's Diversified Growth: Alphabet's annual revenue surged from $258 billion to nearly $403 billion over the past five years, with its core search engine and cloud services performing strongly, laying a solid foundation for future growth despite some businesses not yet being profitable.

- Apple's Market Leadership: With a market value exceeding $700 billion, Apple remains a significant holding for Berkshire, as its products and services continue to thrive, particularly in the services ecosystem, ensuring future growth potential.

- Coca-Cola's High-Profit Model: Coca-Cola operates with net profit margins in the mid-20% range and has consistently increased its dividends, earning the title of 'Dividend King', with a business model that relies on selling foundational syrups, ensuring stable cash flow and long-term investor returns.

See More

Greg Abel's First Quarter Report Reveals Investment Strategy

- Portfolio Adjustments: In his first quarterly report, Abel adjusted the $330 billion equity portfolio by adding positions in Delta Airlines and Macy's, while tripling the stake in Alphabet, indicating his proactive approach to high-conviction stocks while maintaining Buffett's investment style.

- Small Position Sell-Off: In the first quarter, Abel and his team sold out of 16 smaller positions, including Visa and Mastercard, which accounted for about a third of Berkshire's total holdings, demonstrating decisive action in optimizing the investment portfolio.

- Core Holdings Retained: Despite the significant sell-off, Abel retained core holdings such as Apple, American Express, and Coca-Cola, reflecting his respect for and continuation of the company's traditional investment strategies established by Buffett.

- Positive Market Reaction: Following the announcement of Abel's investment strategy, Berkshire Hathaway's stock ticked higher, reflecting market confidence in his management capabilities and further solidifying the company's position in the investment community.

See More

Berkshire Hathaway's Abel Restructures Equity Portfolio

- Portfolio Restructuring: Greg Abel cut 16 small positions in the first quarter, including long-held Visa and Mastercard, demonstrating a strategic focus on concentrated high-conviction stocks while maintaining Buffett's traditional investment style.

- New Investment Directions: Abel added positions in Delta Airlines and Macy's, and tripled the investment in Alphabet, indicating a strategy aligned with Buffett's tech stock preferences, which may attract younger investors.

- Increased Concentration: Excluding investments in Japan, Berkshire now holds only 29 positions, retaining Buffett favorites like Apple, American Express, and Coca-Cola, reflecting ongoing confidence in classic quality assets.

- Positive Market Reaction: Despite the reduction of about one-third of the portfolio, Berkshire's stock price rose following the announcement, indicating market approval of Abel's investment strategy and suggesting optimistic expectations for future performance.

See More

Wall Street Banks Increase Credit Derivative Trading with Hyperscalers

- Surge in Derivative Demand: As hyperscalers like Meta and Alphabet raise over $250 billion for AI, Wall Street banks are experiencing a significant increase in credit derivative trading volumes, driving market activity and rising trading costs.

- Hedging Needs Rise: Banks are purchasing credit derivatives to mitigate risk exposure to single companies, allowing them to increase lending and derivative trading without breaching credit limits, thereby enhancing overall profitability.

- Hedge Fund Profit Opportunities: With credit derivatives for hyperscalers priced unusually high relative to their credit ratings, Andrew Weinberg of Saba Capital Management notes that now is an optimal time to sell high-rated credit default swaps, anticipating substantial returns.

- Market Structure Shift: As borrowing demands from hyperscalers continue to rise, banks' credit valuation adjustment (CVA) desks are actively engaging in trades, leading to record growth in CDS trading volumes, reflecting a dual demand for confidence and risk management in the market.

See More

Berkshire Hathaway's Major Portfolio Shake-Up Under New CEO

- Portfolio Restructuring: Berkshire Hathaway, under new CEO Greg Abel, has undergone its most active trading quarter in recent memory, completely selling out of several companies and increasing stakes in others, reflecting a thorough review of holdings and a strategic focus on high-conviction investments.

- Strong Performance of Apple: Apple (AAPL), as Berkshire's largest holding, continues to show robust cash flow and profit growth despite not heavily investing in AI, and its partnership with Google on the next generation of Siri indicates a solid market position, making it a likely choice for investors moving forward.

- Attractive Valuation of Moody's: Moody's (MCO) shares have fallen about 35% from their peak, now trading at a price-to-earnings ratio of 31, the lowest since early 2023, with analysts projecting an 11% annual earnings growth over the next three to five years, potentially presenting a classic buy-the-dip opportunity.

- Coca-Cola's Dividend King Status: Coca-Cola (KO), the only Dividend King on the list with over 50 consecutive years of dividend increases, currently offers a 2.6% yield, and while its valuation is somewhat high, the consistent dividend growth makes it a strong candidate for long-term investment.

See More